Bespoke’s Morning Lineup – 7/25/22 – The Week We’ve All Been Waiting For (Or Dreading)

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s a recession when your neighbor loses his job; it’s a depression when you lose yours.” – Harry Truman

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

The weather has been hot across much of the country the last several days, and that heat will move to the markets this week with a busy schedule of economic data, peak earnings season, and the FOMC announcing its latest policy decision.

Ahead of the kickoff of trading, equity futures and bond yields are modestly higher along with crude oil and copper. On the downside, Bitcoin is down over 3% while gold is flat. Over in Europe, Germany’s ifo index tracking the business climate fell more than expected as a recession looks increasingly likely.

Today’s Morning Lineup discusses earnings news out of Europe and the Americas, economic data from around the world, and much more.

With all the earnings and economic data on the calendar this week, investors will likely have a much better read on the economy and its direction on Friday. Several indicators have already pointed to the increased likelihood of a recession, and the yield curve has also been indicating a more precarious economic picture. While the spread between the yields on the 10-year and 2-year US Treasuries has been negative for three weeks now, the spread between the 10-year and the 3-month yields has yet to move to inverted levels. A few months ago, the relative steepness of the Fed’s preferred yield curve measure was cited as a reason why a recession was not in the cards. However, after flattening by nearly 200 bps to just 40 bps in the last three months, even this part of the curve (light blue line) looks much less comforting.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 7/24/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Human Resources

The job market is beginning to show cracks by Abha Bhattarai and Lauren Gurley (MSN/WaPo)

As financial markets take a header, spending on high-end goods and services is starting to slow and the result is a weaker job market; layoffs are also being announced across mortgage lenders, auto manufacturers, convenience stores, and more. [Link]

With Few Able and Fewer Willing, U.S. Military Can’t Find Recruits by Dave Philipps (Yahoo!/NYT)

Enlistments have plunged thanks to COVID-19, strong labor markets, and less cultural interest in the military, leading to higher enlistment bonuses and more aggressive recruiting tactics. [Link]

Cost of Living

People Are Losing It Over These $90 Chicken Tenders In Montauk… (Guest of A Guest)

Hamptons life has always been an expensive proposition, but one menu item in a Montauk haunt caught social media attention this week as a particularly egregious bit of price gouging. [Link]

Inflation for Americans at each age (USA Facts)

A fascinating infographic that re-weights CPI to show how inflation impacts people with different ages, since consumer spending patterns vary across the age spectrum. [Link]

America’s favorite family outings are increasingly out of reach by Zachary Crockett (The Hustle)

Widely-accessible leisure activities that used to be par for the course are now completely out of reach for most families: baseball games, movies, and Disneyland trips have all more than doubled in cost. [Link]

Life Science

Blots On A Field? By Charles Piller (Science)

A short seller-funded tear-down of groundbreaking science tying protein plaques to Alzheimer’s disease has turned out to be little more than a mirage and may even rise to the level of fraud. [Link]

New York reports 1st US polio case in nearly a decade by Mike Stobbe (AP)

An unvaccinated person has been paralyzed by the polio virus in New York, with the virus originally coming from a live-virus vaccine that is not available in the United States and must have been transmitted to the patient by someone visiting the US. [Link]

‘Holy grail’ of blood tests could diagnose any type of cancer years in advance (Study Finds)

Many cancers appear to release a protein marker in the early stages of a tumor’s development, when the disease is much easier to treat. [Link]

Politics

A guide to Chile’s constitutions, old and new by Ana Lankes (Medium)

Chile’s constitution has been re-written and will go to a plebiscite later this year. Some history on why the re-write took place and how it looks like it might fare in the approval vote. [Link]

Black Districts Gutted as Suburban Flight Reshapes Congress Maps by Gregory Korte (Bloomberg)

Once a staple of multiracial democracy in the United States, majority-Black Congressional districts have started to disappear in the wake of the Supreme Courts paring-back of the Voting Rights Act. [Link; soft paywall]

Energy

BlackRock Is Buying Renewable Natural Gas Producer for $700 Million by Amrith Ramkumar (WSJ)

While natural gas produced from manure and food waste is still expensive, the market is growing as investors and customers look for gas that is produced from a closed loop rather than extracted from the ground. [Link; paywall]

Sizewell C nuclear plant gets go-ahead from government (BBC)

The UK is moving to expand existing nuclear facilities in Suffolk, with French utility Electricite de France leading the project which will cost tens of billions and see 3.2 GW of electricity supplied with a useful life of 60 years. [Link]

The curious incident of the gas and the turbines by Alexandra Scaggs (FT Alphaville)

A fascinating dive into a financial markets rumor that spread like wildfire and proved to be deeply misleading in terms of actual government policy. [Link; registration required]

Weird News

Final DIY Project: Build Your Own Coffin by James R. Hagerty (WSJ)

It’s one thing to pick your coffin out before you go, but entirely another to build it by hand and have it ready when you kick off this mortal coil. [Link; paywall]

JPMorgan Trader Spoofed So Fast Colleagues Urged Ice on Fingers by Eddie Spence (Bloomberg)

A trader working at Bear Stearns and JPMorgan in the 2000s reportedly spoofed orders so aggressively that colleagues suggest he ice down his hand. [Link; soft paywall]

Media

Media Confidence Ratings at Record Lows by Megan Brenan (Gallup)

Gallup’s tracking of confidence in newspapers and television news has fallen to record lows over the last few years, with only 11% of people reporting “a great deal” or “quite a lot” of confidence in television and 16% for newspapers. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – 7/22/22 – You Ain’t Seen Nothing Yet

This week’s Bespoke Report newsletter is now available for members.

This week’s Bespoke Report covers everything in the markets this week from the weaker economic numbers to the early indication for this earnings season. We also looked at the significance of some key technical events this week as well as what to expect from the FOMC ahead of next week’s FOMC meeting. To read all about it these events as well as the latest Technical, Sentiment, Historical, and Fundamental trends make sure to check out this week’s report.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Daily Sector Snapshot — 7/22/22

Charts of the Week from Bespoke — 7/22/22

Below are some of our favorite charts from our work this week. Try Bespoke’s premium research service today to receive our unique stock market charts and analysis in your inbox daily. Click here to start a one-month trial now!

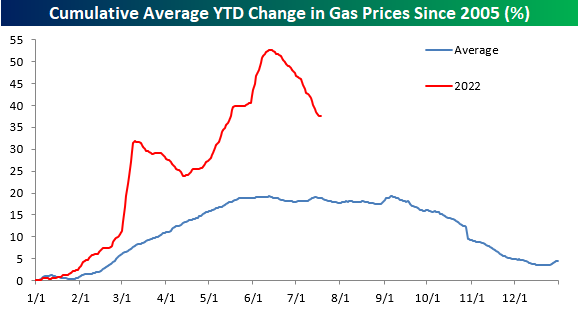

We started the week noting the steep drop in gas prices that we’ve seen from highs made in mid-June. While gas prices are indeed down, they’re still up much more than usual year-to-date. From a seasonal perspective, this is normally a time of year when gas prices are trending lower, so this year’s drop is not out of the norm. In the chart below, the red line shows this year’s change in gas prices, while the blue line shows the average pattern that gas prices have taken throughout the year going back to 2005.

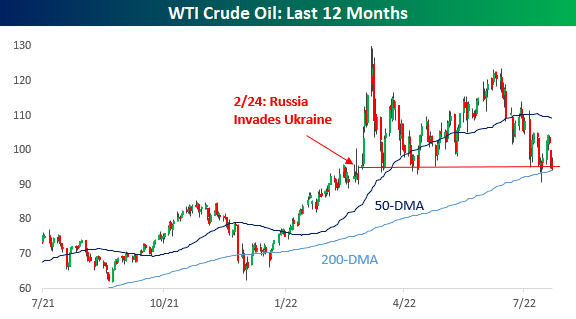

Gas prices are of course driven by the price of crude oil, and in Friday’s Morning Lineup, we noted that crude oil prices have now fallen back to the level they were at when Russia launched its invasion of Ukraine back in late February:

On Wednesday we wrote about weekly mortgage data that continues to show steep drops in activity. As shown below, with mortgage rates rising sharply to levels not seen in more than a decade this year, refinancing activity has fallen to its lowest level since November 2000!

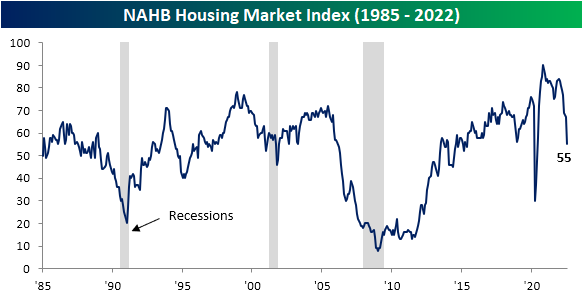

Less activity and much higher costs have caused homebuilders to sour on housing. As we noted in a post on Monday and as shown below, the NAHB’s housing market sentiment index has fallen sharply in recent months to its lowest level since May 2020 just after the pandemic began.

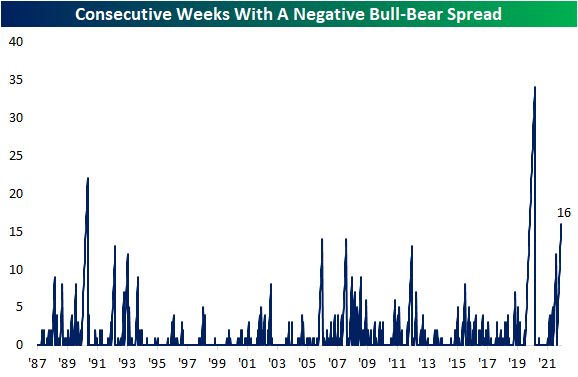

There’s plenty of negative sentiment to go around throughout both the economy and the investment community. In our weekly post on investor sentiment, we highlighted the chart below that shows streaks of weeks where there have been more bears than bulls in the weekly American Association of Individual Investors survey. At 16 consecutive weeks, this is the third longest streak over the past 35 years!

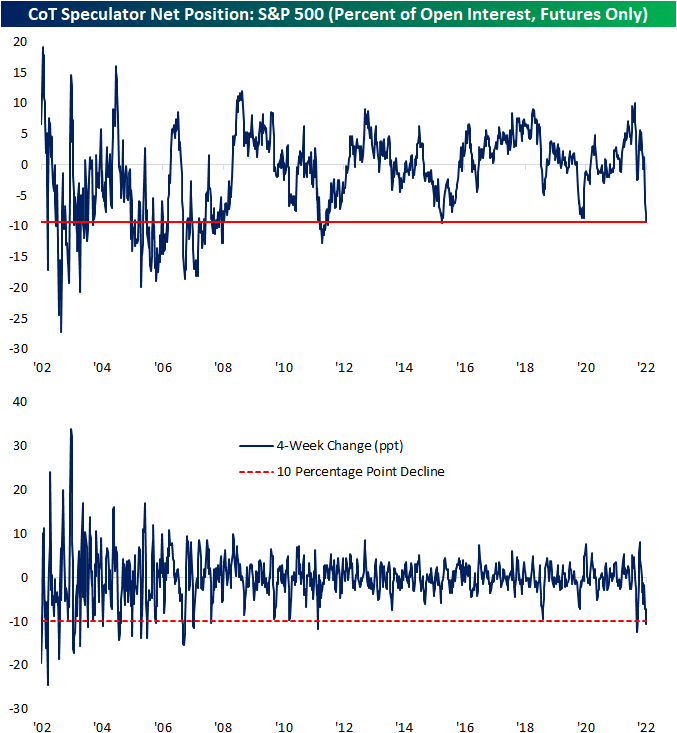

We publish detailed analysis of the CFTC’s weekly Commitment of Traders report in our Closer report every Monday (the Closer is only available to Bespoke Institutional subscribers). The Commitment of Traders report shows how long or short futures traders are on various asset classes based on their positions in the futures market. As shown below, speculator positioning recently turned extremely bearish on the S&P 500. These types of indicators are typically viewed from a contrarian lens, but you can read more about this specific indicator in our blog post from earlier in the week.

In good news, the “prices paid” component of this month’s Philadelphia Fed Manufacturing survey saw another sharp drop for July. While it’s still elevated, this inflation reading has fallen sharply since peaking in April, and signs that inflation has peaked are a key reason why stocks have managed to bounce a bit over the last month or so. You can read more about this month’s Philly Fed report in our post on the subject from Thursday.

Our Morning Lineup is one of our most popular reports for subscribers. We’re biased, but we think it’s the best daily pre-market report in existence! (See for yourself with a one-month Bespoke Premium trial.) The chart below was highlighted in our Morning Lineup on Wednesday after the Nasdaq ended a streak of over 60 trading days below its 50-day moving average. Since the Nasdaq was created in the early 1970s, there have only been 18 other streaks of 60 or more trading days below the 50-DMA. It’s not common, but at least it’s over!

As we close out another hot summer trading week, below is a look at where key US index ETFs stand in their “trading ranges” after the recent surge we’ve seen for stocks. Usually, after an ETF sees a gain of more than 5% in a one-week span, it’s trading well into “overbought” territory. But given how depressed the US stock market had gotten heading into July, most of the index ETFs we follow are still trading in “neutral” territory.

Bespoke Premium and Institutional subscribers can use our interactive Trend Analyzer tool that looks similar to the graphic below. It’s helpful for monitoring indices, sectors, stocks, baskets of stocks, and custom portfolios. We also cover the concept of “overbought” and “oversold” in our work regularly, so if you’d like to learn more about how we monitor price movements, start a one-month Premium trial today!

Later today we’ll be sending subscribers our weekly Bespoke Report newsletter, so be on the lookout for that in your inbox if you’ve already signed up for your trial. We hope you have a great weekend!

Bespoke’s Morning Lineup – 7/22/22 – The Calm Before the Storm

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The impossible could not have happened, therefore the impossible must be possible in spite of appearances.” – Agatha Christie

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Major US equities are heading into the last day before the weekend holding strong gains for the week. In addition to breaking above their respective 50-day moving averages, the S&P 500 is up 3.5% week to date while the Nasdaq is up over 5%. Futures for both indices are modestly lower this morning, but it could have been worse given some of the weak tech earnings since the close yesterday. Outside of equities, crude oil is lower while US Treasury yields are plunging with the 10-year yield down to 2.8% and the 3m10y treasury yield curve down to just 35 basis points (bps). It’s not inverted yet, but it’s moving quickly in that direction.

Things are pretty quiet given the Summer Friday, but enjoy the calm while it lasts. With earnings season ramping up next week, including reports from the four largest companies in the S&P 500, things could get rocky.

Today’s Morning Lineup discusses earnings news out of Europe and the US, the latest ECB decision, events in the Ukraine and Italy, and economic data from around the world including UK home prices and weekly US mortgage application data.

Crude oil is trading down over 1.5% this morning putting it on pace for the third straight day of declines of over 1%. That would be the longest streak of 1%+ daily declines since mid-March. As we type this, WTI is barely trading above its 200-DMA which is a level it has not closed below since last December. Current levels also coincide with where it was trading right before Putin invaded Ukraine back in late February. After briefly surging above $130 per barrel right after the invasion, crude oil has now declined nearly 28% from that peak. Look for these declines to start showing up in the monthly inflation numbers in the months ahead.

Energy stocks live and die by the price of oil (and natural gas), so it should come as no surprise that with crude oil down by over a quarter and natural gas still down from its early June high (although it has rallied sharply in the last two weeks), energy stocks have been under pressure. After peaking above $90 in early June, the Energy Select Sector SPDR (XLE) has pulled back more than 20%, and like WTI, is trading just above its 200-DMA and right around levels it was trading at prior to the Russian invasion of Ukraine. For both energy commodities and the stocks in the sector, their future direction will depend on the push of geo-political tensions and supply concerns versus the pull of increasingly weaker economic growth.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke’s Weekly Sector Snapshot — 7/21/22

The Bespoke 50 Growth Stocks — 7/21/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Philly Fed Collapsing

Tacking on to the list of weaker than expected US economic releases this morning was a big drop in the Philadelphia Fed’s Manufacturing Business Outlook Survey. After a contractionary -3.3 reading last month, forecasts were calling for the headline number to rise back into expansion. Instead, it posted an even larger decline down to -12.3; the lowest reading since May 2020. Expectations have been even worse. That month-over-month decline in July ranked in the bottom decile of all monthly moves in the history of the survey dating back to 1968. Even more depressing, the low level reached is the worst reading since December 1979.

Given the huge drop in the headline index, breadth left much to be desired this month. The categories are almost evenly split between those in contraction and expansion while there is also a wide dispersion between where each category stands relative to their respective ranges. For example, while New Orders has become very depressed – only in the 3rd percentile of all months after the double digit month over month decline in July – the index for Number of Employees has held up relatively well in the 93rd percentile. The whole of the report paints a fairly dour outlook for the region’s manufacturing economy, but expectations are broadly weaker than current conditions with multiple categories reaching new record lows.

As previously mentioned, New Orders is the weakest current conditions index. The reading fell from -12.4 to -24.8 in the past month. Prior to the spring of 2020, the last time this index was as low was during the Global Financial Crisis era. Expectations are even worse. Last month’s decline was much more severe at 23.5 points versus 5 points in July, however, the continued drop has brought the index to the lowest level since September 1979. Although demand has slumped, Shipments actually accelerated with the current conditions index slightly below median while expectations saw a large 9.2 point MoM jump. Unfilled Orders expectations similarly moved higher versus last month but that was only a more modest bounce as the index remains in the bottom 1% of all months. Current Conditions are more modestly in contraction in the 27th percentile after falling another 3.4 points in July.

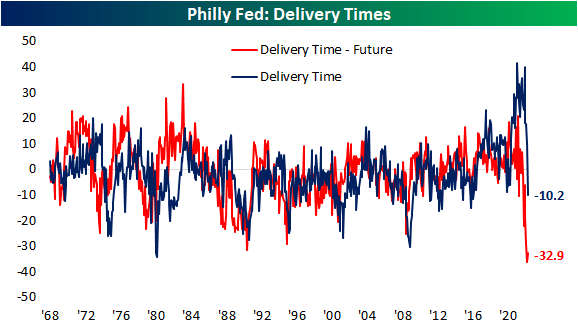

One of the most striking changes over the past few months has been in regards to supply chains. Higher readings in the Delivery Times index indicate that manufacturers are seeing products taking longer to reach their destinations and vice versa for lower readings. Throughout the pandemic, this index sat at unprecedentedly high levels. All of that has been reversed now, though, as Delivery Times moved from expansion into contraction. Not only are delivery times now falling, but the July reading was the lowest reading since May 2016. In other words, on net, a larger share of respondents are seeing declines rather than increases in how long it takes for products to be delivered. Meanwhile, expectations are at the extreme low end of their historical range, coming slightly off last month’s record low. All that is to say supply chains are seeing massive improvements to stress as demand rapidly cools.

Prices have also been experiencing a sharp reversal with Prices Paid at the lowest level since January of last year and Prices Received at the lowest level since last March. Click here to learn more about Bespoke’s premium stock market research service.

Third Longest Streak of Negative Bull-Bear Spread on Record

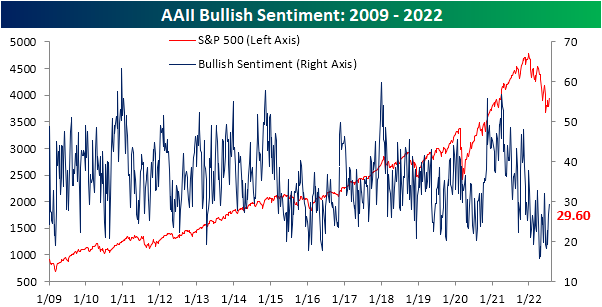

Last week, over a quarter of respondents to the AAII sentiment survey reported bullish sentiment for the first time in over a month. As the S&P 500 has made a considerable move to the upside, bulls have continued to come back this week rising to 29.6%. The percentage of respondents reporting as optimistic has now come back within one standard deviation of its historical average and is at the highest level since the first week of June.

Bearish sentiment has fallen in lockstep with the increase in bullish sentiment. After coming in at over 50% two weeks ago, the reading has shed 10.6 percentage points. Albeit improved, bearish sentiment remains well above the historical average and the double-digit two-week decline is actually the seventh of the year. In other words, the sharp drop in bearish sentiment is not exactly unusual compared to other moves this year as it still has further to go until it reaches a more “normal” level.

Regardless, with inverse moves in bulls and bears the bull-bear spread has risen to -12.6. That is the highest reading since the first week of June and, as shown in the second chart below, the 16th consecutive week with bears outnumbering bulls. Clearing two other streaks from the early 2000s, that is now the third longest streak on record behind the 22 and 34-week-long streaks ending in December 1990 and October 2020, respectively.

Not all of the losses to bears went to bulls. Neutral sentiment also rose this week rising to 28.2% from 26.6% last week. That is the highest level in three weeks as neutral sentiment has generally been less volatile than bulls and bears recently. Click here to learn more about Bespoke’s premium stock market research service.