High Yield Finds Support

The S&P 500 is cutting back on some of its losses today as the index is up around 0.4% as of this writing. From a technical perspective, the S&P 500 is currently around similar levels to the June highs, but other than that there is no clear technical support. High yield bonds are another story. Investors often turn to credit markets for confirmation of moves the equities, and while earlier this week credit spreads were ripping higher to confirm the drop in equities, the high-yield bond ETF (HYG) is showing a more promising sign for bulls today. As shown below, HYG has pulled back 3.33% from its high less than two weeks ago, but over the past three sessions, that decline has been paused as the ETF has found support at its 50-DMA (which has also begun to trend sideways). That is the reverse of what has frequently been observed in the past year as the 50-DMA has gone from resistance to support. At multiple points throughout the past year, the 50-DMA frequently marked a stopping point in short-term rallies. This week, the opposite has appeared to be the case. Click here to learn more about Bespoke’s premium stock market research service.

2022 Slams Stocks and Bonds

It is no secret that 2022 has not exactly been the year of the 60/40 portfolio. This year has left nothing safe with both stocks and bonds hit hard. Both are in the red by 10%+ on a year to date basis headed into the final week of August. In the charts below, we show the year to date total returns of the S&P 500 (y-axis) and the year to date total returns of various ICE Bank of America bond indices (x-axis) through August for each year going back to their respective inceptions (each index began in 1973 except for high yield which began in 1987). No matter which way you cut it, 2022 has been the worst year of the past half century for stocks and bonds combined.

With the S&P 500 down a little over 12% YTD, aggregate bonds (government and corporate bonds combined) are only around one percentage point better. For the comparable time of the year, the only years that also have seen both bonds and stocks sitting on a loss through August were 1973, 1974, and 1981. The same applies for government bonds. The corporate investment grade bond index has a bit more variety of years with stocks and bonds falling in 1974, 1981, 2008, and 2015. Again though, none of those other years have seen as sharp of a decline as 2022, and the S&P 500’s drop in the same time also ranks as one of the worst. 2022 is the only year that the high yield bond index has fallen simultaneously with stocks, however as we noted earlier, it does not have as long of a history as those other categories. Click here to learn more about Bespoke’s premium stock market research service.

Chart of the Day: Breadth Surge Recedes

Bespoke’s Morning Lineup – 8/24/22 – Flat as the Yield Curve

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you want to succeed you should strike out on new paths, rather than travel the worn paths of accepted success.” – John D. Rockefeller

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Trading this morning has been directionless, but it’s better than the alternative of weakness which has been the prevailing tone. Fed Chair Powell’s Jackson Hole Speech on Friday continues to be the main focus of investors, and expectations for the tone of the speech are low. Have you spoken to anyone in the last seven days who thinks Powell’s message will be a positive for the market?

In economic news this morning, Durable Goods for July were unchanged, which was weaker than expected, but ex Transportation, the reading came in better than expected (+0.3% vs +0.1%). The only other report on the calendar is Pending Home Sales at 10 AM.

Treasury yields are mostly lower across the curve except for the two-year which is 2 bps higher and further flattening or inverting various portions of the yield curve. In commodities, crude oil continues to run higher following reports yesterday that OPEC would consider cutting production and that has pushed WTI up to just under $95 per barrel.

As oil prices have moved back into the mid-90s per barrel and natural gas surges to multi-year highs, the Energy sector has gotten a jump. Since its July 14th low, the Energy sector has rallied more than 20% taking it from extreme oversold to extreme overbought levels in the span of six weeks, and as of yesterday’s close, the sector is less than 11% from its 52-week high in June.

Perhaps even more impressive than the rebound in price has been the about-face in the percentage of stocks in the sector trading above their 50-day moving average (DMA). While not a single stock in the sector was above its 50-DMA less than three weeks ago, as of yesterday’s close all but one name was above that level (bottom chart). The lone hold-out has been Baker Hughes (BKR), but even it is now just barely 2% below its 50-DMA. Falling oil prices and the prospects of lower inflation have played an important role in the broader market’s summer rally, but the recent trends for oil and natural gas and stocks in the Energy sector may be starting to shift.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 8/23/22

Chart of the Day: New Home Sales Down the Drain

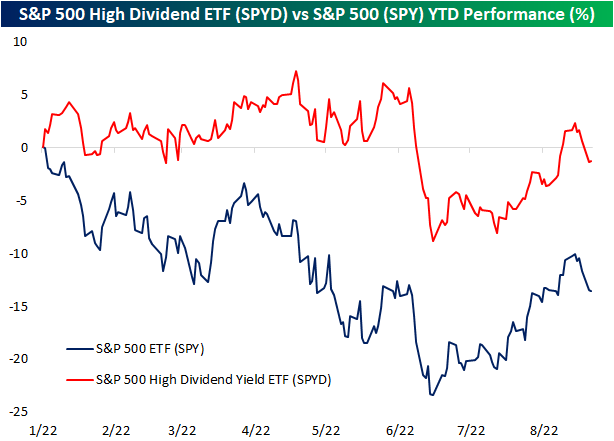

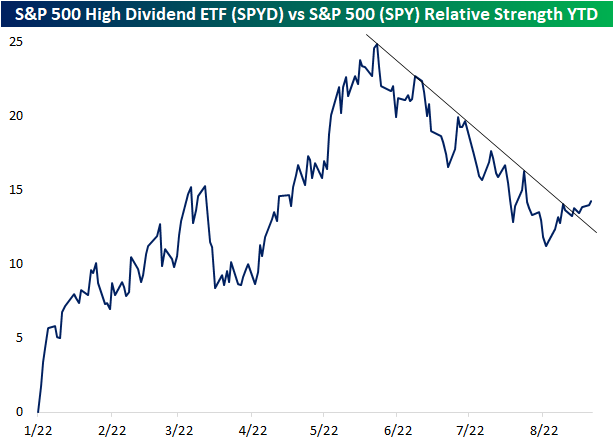

Dividend Breakout Despite Declines

In last Thursday’s Chart of the Day, we highlighted how important dividends are for long-term investment performance. While dividends do help to boost investment returns over the long term, in the short term there is often an ebb and flow of dividend-focused ETFs under and outperforming in terms of price moves. For example, up until June, the S&P 500’s highest yielders measured by the SPDR S&P 500 High Dividend Yield ETF (SPYD) had mostly been trading in the green whereas the S&P 500 (SPY) was deep in the red.

With equities broadly taking a turn lower over the past week, SPYD has held up relatively well when compared to the S&P 500 (SPY). Even though SPYD has not avoided declines (as we also showed in our decile analysis, the highest dividend payers have only slightly better performance than non-dividend payers), the relative strength line of SPYD versus SPY has broken out of the past couple of months’ downtrend. That being said, it has not been a sharp move higher like what was observed in the first half of the year, particularly in the second quarter. In other words, the highest yielders are back to outperforming the broader market but not to the same extent as earlier in the year. Click here to learn more about Bespoke’s premium stock market research service.

Two Month Rally Rotation

Using the Russell 3,000 as a benchmark, US equities peaked exactly a week ago and have traded lower in all but one session since. In all, the Russell 3000 has fallen 4.33% in that time on weak breadth, albeit certain stocks have been hit far harder than others. Breaking the index down into deciles ranked by a variety of factors, performance has generally been the reverse of what we highlighted earlier this month in regards to the rally off of the June 16th low.

Over the past week, stocks with higher multiples and smaller market caps have fallen the most. Those are also the ones that had become the most elevated above their moving averages after outperforming during the two-month rally from mid-June to mid-August. Conversely, those stocks with more attractive valuations have tended to perform better, although, here too there have been low single-digit percentage declines across deciles. One other interesting point worth noting is how the highest dividend payers have been hit just as hard as other deciles for that category which is a big difference when compared to the spring when the highest dividend payers were the only pocket of positive performance. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke Stock Scores — 8/23/22

Dollar & Euro At Parity

For the first time in nearly twenty years, the US dollar is more valuable that the Euro, as the EURUSD spot cross dropped below parity (1.00) on Monday (8/22). The last time that the euro was trading at this level versus the dollar, the iPhone wasn’t even a glimmer in Steve Jobs’ eye as it was still more than four years away from its debut! The most recent run through parity comes as the Fed hikes rates aggressively, which inherently boosts demand for US dollars as foreign investors seek more favorable yields. As of this writing, the 10-year US Treasury Treasury note yields 3.0%, while the German and French equivalents are yielding 1.3% and 1.9%, respectively. The spreads are even wider for nearer-term maturities. In addition, Europe is attempting to phase out Russian energy exports, which means that the bloc has had to turn to the US as an alternative source. This, too, increases dollar demand. The chart below summarizes the major events that have impacted the Euro since the turn of the century. It’s been a wild ride! Click here to start a two-week trial to Bespoke Premium and receive our paid content in real-time.

The decline in the value of the euro has wide-ranging effects across the economy. For US companies with operations in Europe, the stronger dollar makes transactions conducted in euros less valuable. Broadly speaking, though, the S&P 500 Index has essentially no correlation to the EURUSD cross. In fact, on a monthly basis, the correlation since the turn of the century has been -0.19, which implies almost no correlation between the two. Looking at the last ten years, the S&P 500 has surged as the euro has lost value, but from 2003 through the 2007 high, the S&P 500 likewise performed very well even as the euro surged. While a weaker euro most definitely has implications for a number of individual companies, the broader impact on markets hasn’t been as impactful. Click here to start a two-week trial to Bespoke Premium and receive our paid content in real-time.