Bespoke’s Morning Lineup – 10/11/22 – The Roller Coaster Continues

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Sometimes the wheel turns slowly, but it turns.” – Lorne Michaels

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Equity futures were sharply lower this morning but have rebounded sharply in the last hour. There’s no specific catalyst to the move, but the BoE’s expansion of its bond-buying program has certainly helped. The monthly look at small business sentiment from the NFIB came in slightly higher than expected (92.1 vs 91.6) and increased slightly relative to August’s reading. There are no other economic data on the calendar today, but Cleveland Fed president Loretta Mester will be speaking at noon, and remember that in late September she made some rather hawkish comments suggesting that hell or high water wouldn’t deter the Fed from hiking rates to combat inflation.

Between value and growth stocks yesterday, we saw a modest divergence where the S&P 500 Growth ETF (IVW) traded at a new low while the Value ETF (IVE) did not. At face value, that divergence would sound like a negative for growth stocks. Looking at the price charts of each ETF, though, shows that while the growth ETF made a new low yesterday breaking through its September and summer lows, the value ETF had already broken below its summer lows in late September. So yes, value has outperformed over the last few days, but the technical picture for both is lousy.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 10/10/22

B.I.G. Tips – Tesla (TSLA) Loses Its Charge

Energy Surges Without the S&P

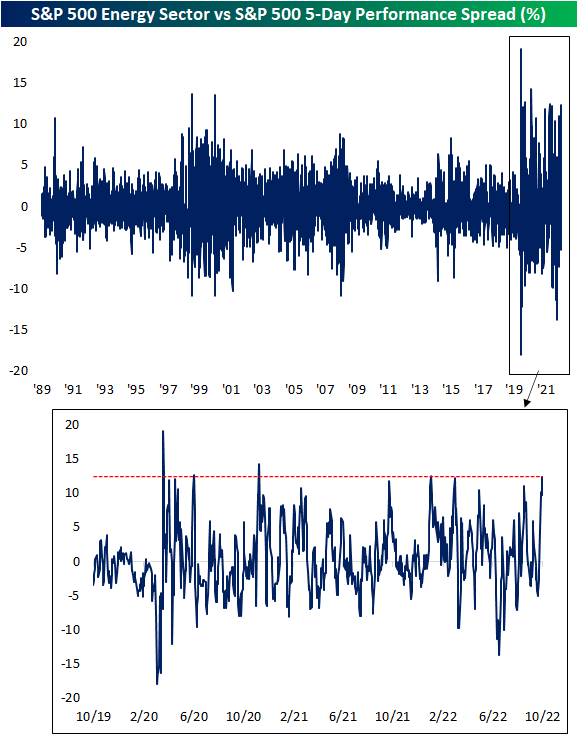

Taking a glance across sector ETFs in our Trend Analyzer tool, performance last week through Friday’s close wasn’t fully lost as many sectors managed to hold onto their gains from earlier in the week while others like Real Estate (XLRE), Utilities (XLU), and Consumer Discretionary (XLY) finished more firmly in the red. As was the case earlier this year, the most standout sector has continued to be Energy (XLE). Although the sector has been pretty much trending sideways since the late spring and remains down double digit percentage points from its 52-week high, short term performance has been impressive. Last week the sector ETF rose 13.6% to move from one standard deviation below its 50-day to one standard deviation above. Meanwhile, every other sector remains oversold.

Compared to the S&P 500’s modest gains on the week, Energy’s outperformance has little precedence prior to the pandemic. Below we show the spread of the five day performance of the S&P 500 Energy sector and the S&P 500. Rounding out last week with a high of 12.4 percentage points, the spread hit the highest level since the first week of January. Prior to that, March, June, and November 2020 were the only other recent occurrences with as large of a spread. In our data going back to 1990, the only other time that Energy has outperformed the broader market by as much in a one week span was October 2000 and April 1999. Click here to learn more about Bespoke’s premium stock market research service.

Chart of the Day – It Doesn’t (At Least in the Past) Get Any Better Than This

Bespoke’s Morning Lineup – 10/10/22 – Treasury Market Closed

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“For the execution of the journey to the Indies I did not make use of intelligence, mathematics or maps.” – Christopher Columbus

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

The bond market is closed today, so at least Treasury yields can’t go up. We wish we could say the same thing about yields across the Atlantic, though, where British gilt yields are all higher and getting back up near their closing highs from less than two weeks ago.

Equity markets are open for trading today, and after opening sharply lower last night, futures have rebounded to move close to the unchanged level. That’s the type of environment we’re in these days when just a modestly negative open to start the day is considered a win. With banks and the treasury market closed for trading, there is no economic data on the calendar today, so expect volumes to be on the light side.

How bad is sentiment out there? In looking through the various Bloomberg headlines this morning, the following three were all out one after the other:

- “Deutsche Bank Strategists See 12% Drop in US EPS Next Year”

- “MS Strategists See Bear Market Continuing Until Earnings Reset”

- “Goldman’s Kostin Sees Strong Dollar as Headwind for US Earnings”

Like the birds overhead, sentiment heading into earnings season has been moving south. Bulls can only hope that sentiment has moved south enough already.

Over the last several years, Columbus Day has seen some extreme market moves. The two best Columbus day performances for the S&P 500 were in 2008 (+11.58%) and 2011 (3.41%), and the one thing both of those years have in common is that they were lousy years for stocks heading into Columbus Day To the downside, the worst Columbus Day performance was in 2014 when the S&P 500 declined 1.65%, and no other year besides 2014 over the last 25 has seen a decline of more than 1%.

While the two best Columbus Days for the S&P 500 came in years when stocks were already down big YTD, there isn’t really much of an inverse correlation between YTD performance and Columbus Day returns. In the seven years over the last 25 when the S&P 500 was down YTD heading into the holiday, the median Columbus Day performance was a gain of 0.13% with positive returns four out of seven times (57%). In the 18 remaining years when stocks were up YTD heading into the holiday, the S&P 500’s median performance on Columbus Day was a gain of 0.05% with gains 10 out of 18 times (56%).

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Bespoke Brunch Reads: 10/9/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day trial!

Ukraine

Russia’s Elites Are Starting to Admit the Possibility of Defeat by Tatiana Stanovaya (Carnegie Endowment)

There are emerging signs that Russian elites are losing patience with the disastrous prosecution of the war in Ukraine after months of solid support. [Link]

She’s a Doctor. He Was a Limo Driver. They Pitched a $30 Million Arms Deal. by Justin Scheck (NYT)

A rush to supply arms to Ukraine has led to shady, untested ventures sprawling across countries delivering large scale shipments of weapons to the embattled country. [Link; soft paywall]

Rate Hikes

U.N. Calls On Fed, Other Central Banks to Halt Interest-Rate Increases by Paul Hannon (WSJ)

The United Nations Conference on Trade and Development (UNCTAD) argued that the speed and size of Fed rate hikes risk a global recession and are getting carried away. [Link; paywall]

Fed’s Rate Increases Defy All the Rules by Greg Ip (WSJ)

The Federal Reserve’s monetary policy has departed from a series of different rules that relate inflation, unemployment, and the policy rate. [Link; paywall]

Lives Lived

I just learned I only have months to live. This is what I want to say. by Jack Thomas (Boston Globe)

A heartfelt essay on the meaning of a life spent with family, words, and the many details of life that the author will mis when he shoves off this mortal coil. [Link]

Layoffs

Peloton is slashing 500 more jobs as its CEO says it has 6 months to turn itself around by Grace Dean (Business Insider/MSN)

The exercise technology company has announced a fourth round of layoffs with a fresh 12% of workers being dropped as part of a sprawling turnaround plan that has seen headcount cut in half from its peak. [Link]

New Tech

100% Electric Vehicles = 11% Of New Vehicle Sales Globally! by José Pontes (CleanTechnica)

Fully electric vehicle sales were up 60% YoY and area headed for 1mm units in September; the August sales pace was good for 1 car in 10 globally and that share is only growing. [Link]

Walgreens Turns to Prescription-Filling Robots to Free Up Pharmacists by Sharon Terlep (WSJ)

Machine-based dispensaries have helped Walgreens fill prescriptions by raising productivity; total cost savings are more than $1bn. [Link; paywall]

Real Estate

Hybrid Working, Commuting Time, and the Coming Long-Term Boom in Home Construction by Jordan Rappaport (KC Fed)

With more workers able to spend only a couple of days per week at the office, out-lying suburbs and exurbs could be the source of a major building boom in the coming decades. [Link; 35 page PDF]

House Prices: 7 Years in Purgatory by Bill McBride (Calculated Risk)

Widely-cited housing observer Bill McBride has gotten a lot more bearish on the housing market after the pandemic era surge has reversed into monthly declines: he sees long-term declines ahead for both real and nominal home prices. [Link]

Global Trade

WTO Sees Sharp Slowdown in Global Trade, Pointing to Possible Recession by Paul Hannon (WSJ)

The World Trade Organization sees trade activity growing by 1% in 2023, versus 3.5% growth this year and a 3.4% growth rate previously forecasted. High energy prices, war, and surging interest rates are all key factors. [Link; paywall]

China property woes trigger decline in global cement output by Oliver Telling, Thomas Hale, and Andy Lin (FT)

Collapsing real estate investment in China has driven global cement output down 8% in the first half of 2022 versus the first half of 2021; Chinese cement production (which is about half of the global market) fell 15%. [Link; paywall]

Cargo Shipowners Cancel Sailings as Global Trade Flips From Backlogs to Empty Containers by Costas Paris (WSJ)

After 2021 and early 2022 saw catastrophically high demand for ocean freight capacity, shipping lines are cancelling sailings amidst shipping rates in freefall and collapsing bidding for capacity from North American retail clients. [Link; paywall]

Contras

The Fund That Helped Investors Bet Against Cathie Wood Is Taking on Jim Cramer by Claire Ballentine (Bloomberg)

The ETF provider that gained prominence through a fund designed to move inverse to Cathie Wood’s ARK Invest funds is targeting another big “take the other side” opportunity: bets against stocks recommended by Jim Cramer on CNBC. [Link; soft paywall]

Social Media

Supreme Court takes up a divisive issue: Should tech companies have immunity over problematic user content? by Lawrence Hurley and David Ingram (NBC)

The Supreme Court has agreed to hear a case that could strip internet companies of immunity over content posted by their users; changes could mean much more aggressive content moderation across the political spectrum from companies like Twitter, Facebook, and Google. [Link]

The Call of The Wild

Coyotes Came to New York City, but Not for Our Pizza by Bethany Brookshire (NYT)

While coyotes enjoy the occasional nibble of human chow, even urban packs subsist mostly on the wild foods that they would be eating in any other environment. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – 10/7/22 – Read Our Lips: No Easing Ahead

This week’s Bespoke Report newsletter is now available for members.

Markets tried and failed once again this week to catch a Fed pivot, but with the central bank refusing to believe inflation has peaked optimism was eventually dashed. Another strong jobs report on Friday sent stocks tumbling in yet another tightening of financial conditions. It’s not just stocks, either. We discuss the move higher in Treasury yields, the rise in the dollar, and rising corporate bond yields from a long-term perspective and in the context of the Fed’s campaign to keep pushing policy tighter. OPEC+ was also in the headlines this week, and we give a full analysis, along with summaries of PMI indices in the United States, a preview of earnings season, analysis of mortgage rates’ surge, discussion of the housing market, recaps of multiple labor market data releases received this week, and much more in this week’s Bespoke Report.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.