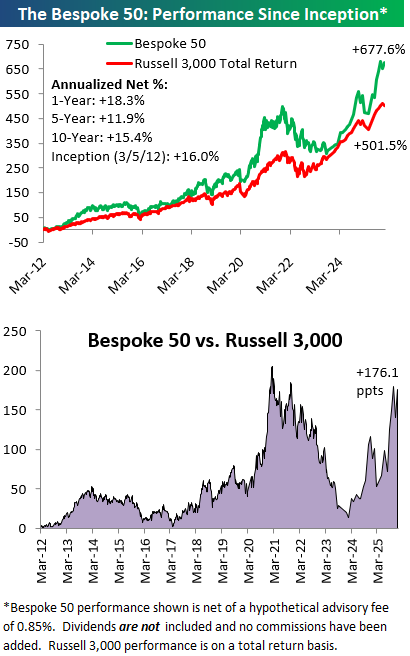

The Bespoke 50 Growth Stocks – 12/18/25

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There were 5 changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 12/18/25 – Fool Me Once

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Our coding teams are realizing productivity gains of 30% or more using agentic AI.” Mark Murphy, CFO Micron

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures got off to a positive start this morning ahead of a busy morning for economic data. Initial and continuing jobless claims came in better than expected, while the Philly Fed report for December came in weaker than forecasts. The number of the morning was CPI, and while there were no m/m readings since October data was not compiled, the y/y reading came in much weaker than expected at 2.7% versus forecasts for 3.1%. Core CPI was weaker at 2.6% versus forecasts for an increase of 3.0%.

In response to the report, futures have added on to their gains with the S&P 500 now indicated to open 0.5% higher while the Nasdaq is up 0.8%. Treasury yields are down about 3 bps across the curve, and crude oil is marginally higher. Gold is down about half of one percent, while Bitcoin is up 2.5%.

Asian stocks were biased to the downside with the Nikkei falling over 1% for the third time this week. South Korea fell 1.5%, but Hong Kong and China were both up marginally. In Europe, investors are more optimistic as the STOXX 600 trades up 0.3%. It’s been a busy morning for central bank announcements as the ECB left rates unchanged, and the BoE cut rates by 25 bps in a 5-4 decision.

There’s obviously been tons of hype related to AI, and the increases in productivity that it promises. That’s why stocks like Nvidia (NVDA) and many of the hyperscalers have done so well. Moving forward, investors will increasingly demand to see concrete examples across the economy of productivity boosts from companies using AI. Last night’s earnings call from Micron (MU) provided one of those examples when the company’s CFO noted that its programming teams have seen a 30% boost to productivity from using AI.

That’s good to see, but it’s not why MU’s stock is trading up nearly 14% in the pre-market. Last night, the company reported one of the more impressive triple plays we’ve ever seen. While EPS beat expectations by over 20% and revenues were 5% ahead of forecasts, the jaw-dropping aspect of the report was the guidance, as the company sees next quarter’s revenues exceeding consensus forecasts by at least 25%, and they raised EPS guidance by at least 75%. MU’s stock was up 40% in the three months leading up to the report, so investors were expecting a strong report, but the results were still impressive.

MU’s double-digit percentage pre-market gain has investors breathing a sigh of relief, but you can’t fault anyone for being a little cynical after seeing how some other AI-related stocks recently performed in reaction to what, at face value, looked like impressive reports.

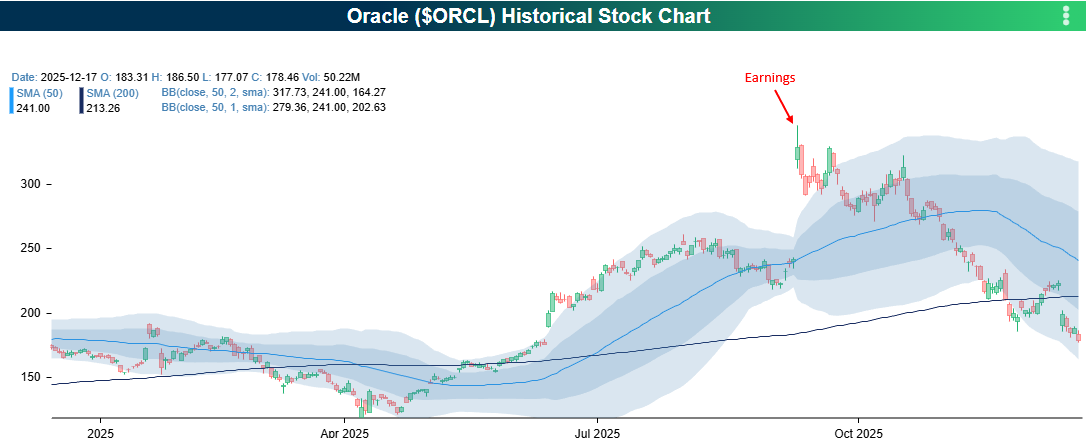

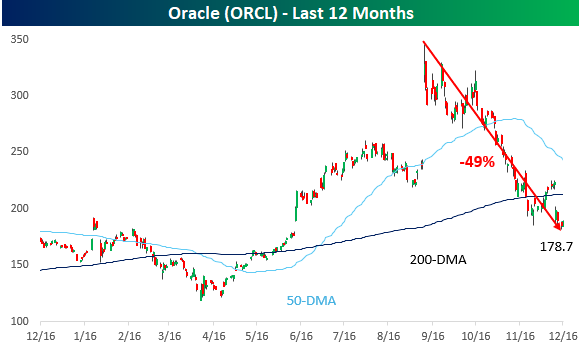

It started with Oracle (ORCL) in September. After reporting earnings after the close on 9/9, the stock traded up an astonishing 36%. Since then, all those gains and more have evaporated as the stock has been essentially cut in half.

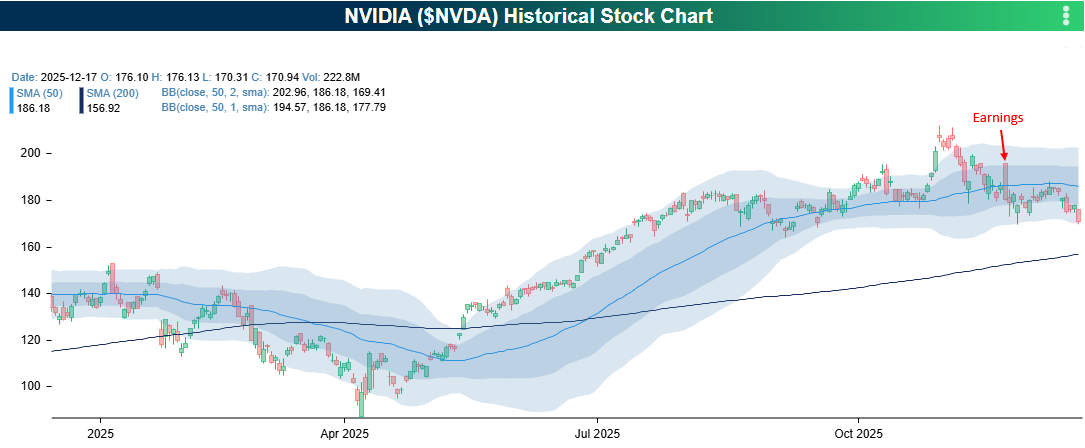

On 11/19, Nvidia (NVDA) reported an earnings triple play, and the following morning, the stock gapped up over 5% and took the rest of the market along for the ride with it. Quickly after the market opened, though, shares nosedived nearly 8% intraday to finish the session down over 3%. Since then, the stock is down another 5%.

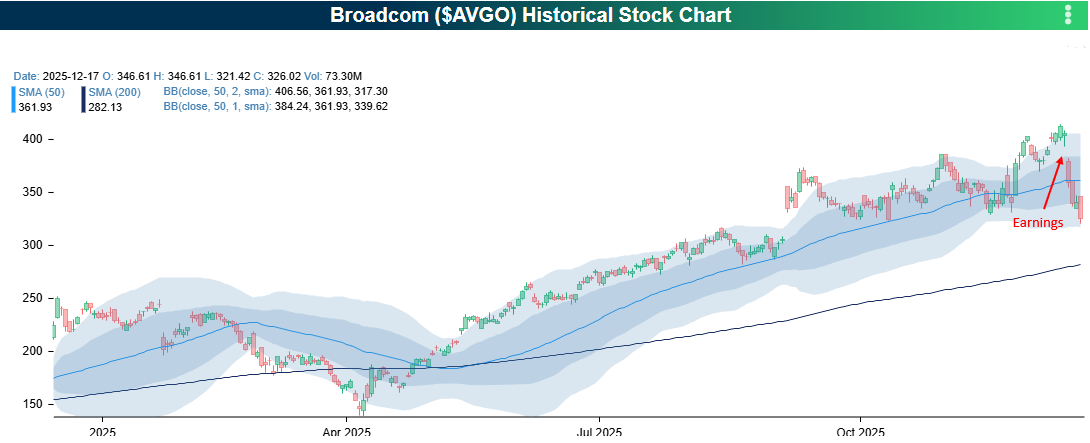

Then, last week, Broadcom (AVGO) reported another triple play, but that wasn’t enough to provide any positive traction in the stock. On 12/12, AVGO gapped down over 5% and is down close to another 15% since that opening trade.

All this is a long way of saying, yeah, it’s great to see MU rallying in reaction to earnings, but unless the stock can hold onto those gains through at least one full session of trading, you can understand if an investor wants to be at least a little skeptical. Fool me once, shame on you. Fool me twice, shame on me. Fool me three times, I’m the fool. Fool me four times, it’s a trend!

The Closer – AI Narratives, Quick Crosses, CFOs – 12/17/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at the ripple effects from news over Oracle’s (ORCL) capex (page 1 and 2) followed by a review of the S&P 500’s technical picture, including the quick reversal from a 52-week high (page 3). We then finish with a dive into the latest CFO survey with an emphasis on the AI and employment related special questions (pages 4 and 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 12/17/25

Bespoke Baskets Update – December 2025

Chart of the Day: Going for Four

Oracle Pain Continues

Investor sentiment towards Oracle (ORCL) is taking another hit today on reports from the FT and Reuters that Blue Owl Capital, which typically funds and leases data centers back to Oracle, pulled out of a project in Michigan designed to serve OpenAI. With over $100 billion in outstanding debt, investors continue to grow more concerned about the company’s borrowing to fund its AI ambitions.

Those concerns have obviously manifested themselves in ORCL’s stock price. With this morning’s 5%+ decline, the stock has basically been cut in half from its intraday high in September. Shockingly, even with that decline, the stock is still hanging on to a single-digit percentage gain YTD. It’s not often that stocks fall 50% and remain up on the year.

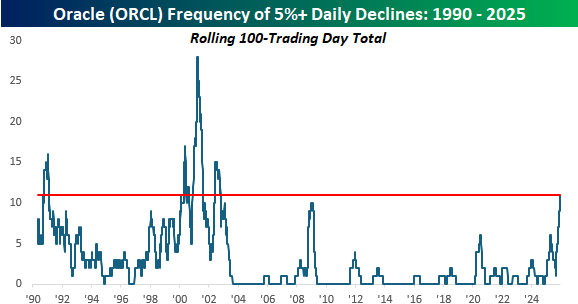

If today’s declines hold, it will also mark the 11th time in the last 100 trading days that ORCL declined at least 5% in a single session. Even during the Financial Crisis, when it seemed as though stocks were crashing every day, the highest this reading ever got for ORCL was ten. That said, it’s nowhere near the levels (at least not yet) that it got during the bursting of the dot-com bubble in early 2000 through 2002. Hopefully for bulls, Oracle’s recent weakness isn’t living up to its namesake and offering a warning for the rest of the market.

Bespoke’s Morning Lineup – 12/17/25 – 10, 9, 8…

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I can’t believe it, but it looks as though television has betrayed me.” – Bart Simpson, Episode 1, The Simpsons

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If you think the seven-month winning streak in the Nasdaq has been impressive, think of this: today marks the 36th anniversary of the first episode of The Simpsons, when the longshot Santa’s Little Helper first cancelled Christmas for the Simpson family by losing his race at the dog track and then saved it when he was kicked to the curb and adopted by the Simpson family. Everyone who watched that first episode has aged quite a bit, but Homer, Marge, Lisa, Bart, and Maggie haven’t aged a bit, and Barney Gumble is still drunk down at Moe’s!

After a busy day for data yesterday, the calendar goes dark again this morning, but there is some Fedspeak to fill the void. Fed Governor Waller is speaking now in New York, and then NY Fed President Williams will speak just after 9 AM. Williams bailed out the bulls late last month, and the way markets have been trading over the last couple of weeks, they could use some market-friendly comments from him this morning. After these two morning speeches, the only other Fed speaker on the calendar is Atlanta Fed President Bostic at 12:30 Eastern.

Futures suggest a positive open for the market this morning, with the S&P 500 and Nasdaq both indicated to open about 0.4% higher. Treasury yields are giving back some of yesterday’s declines as the 10-year yield is back to 4.18%, and crude oil and gold are both trading higher. The same can’t be said for the crypto space, though, as Bitcoin and Ether are both down about 1%.

It took until Wednesday, but Asian stocks finally had a positive session with the Nikkei rallying 0.3%, China rallying over 1%, and South Korea’s Kospi rising 1.4%. In Japan, Machinery Orders for October unexpectedly increased 7.0% versus forecasts for a decline of 1.8%, and November export orders also rose at the fastest pace in nine months (+6.1%).

European stocks got off to more of a mixed start this morning. The STOXX 600 is up 0.3%, but Germany and France are both trading lower as Italy, Spain, and the UK gain. Investors got some good news on the inflation front as November CPI declined 0.3% m/m, which was in line with expectations, but the y/y reading increased slightly less than expected at 2.1% compared to forecasts for an increase of 2.2%. That weaker print all but green-lights a rate cut at tomorrow’s ECB meeting.

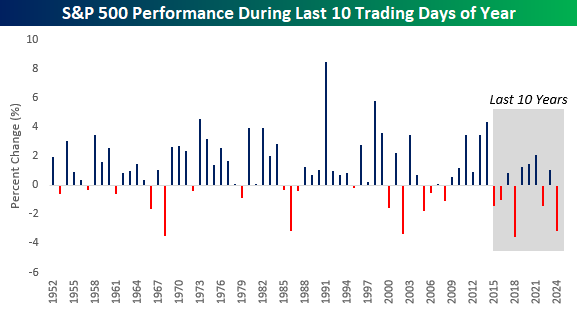

It’s time to let the countdowns begin as there are now just ten trading days left in 2025 (and five until Christmas!). December has historically been a strong month for the S&P 500, and while there has been a lull in the seasonal tailwinds, there’s still time left for them to blow. December has historically been a back-end-loaded month in terms of when the gains occur.

The chart below shows the S&P 500’s performance in the last ten trading days of the year for every year since 1952 (when the five-day trading week in its current form started). Just looking at the chart, it’s easy to see that positive ends to the year outnumber negative ones. It’s also much more common to have a solid gain to end the year than a sharply negative one. While there have only been five years when the S&P 500 declined 3%+ in the last ten trading days of the year, there have been thirteen when it rallied more than 3%, including gains of 8.5% and 5.8% in 1991 and 1998, respectively.

The Closer – Odd Jobs, Retail Sales, Freight – 12/16/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a deep dive into the latest release of payrolls data (pages 1-4). We then pivot into the rest of today’s data releases including retail sales (page 4), ADP and New York Fed Service Indices (page 5), and Cass Freight Indices (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!