B.I.G. Tips – Down Big Friday, Up Big Monday

ETF Trends: Fixed Income, Currencies, and Commodities – 9/12/16

Emerging markets were hit hard in the wake of the big selloff last week, with currencies and local equities moving lower. The Philippines, with outspoken political leadership, is suffering from a lack of investor confidence while Mexico has also gotten slammed over the past week. In the best performers table, oil and other Energy commodities are strongest ETF gainers of the past week while Japanese yen, Hong Konh, and the Biotechs have also performed well versus five days ago.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

S&P 500 Sector Breadth Levels

Underlying breadth obviously took a hit after Friday’s big sell-off, and below is an updated look at where one popular breadth measure currently stands. For the S&P 500 as a whole, 33.8% of stocks are currently trading above their 50-day moving averages. Seven of ten sectors have readings lower than that, however. No stocks in the Telecom or Utilities sectors are currently above their 50-days, while just 5.6% of Consumer Staples stocks are above their 50-days. Health Care has a reading of just 14.3%, Consumer Discretionary is at 24.4%, and Industrials is at 26.9%.

The three sectors with stronger-than-market readings are Energy, Technology and Financials. The fact that Tech and Financials have strong readings is a positive because they’re the two biggest sectors of the market. Market bulls would like to see more participation from the rest of the market, however.

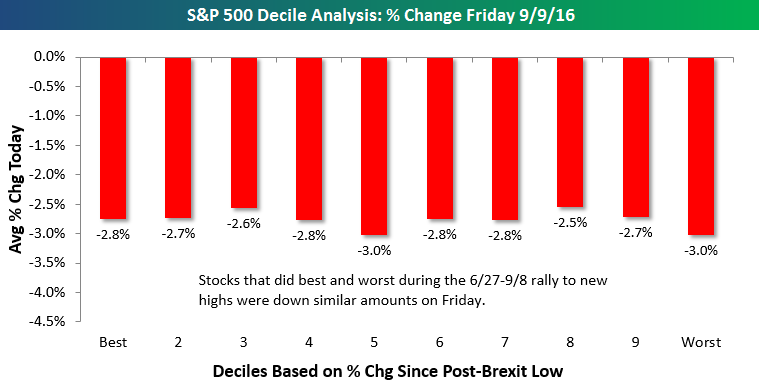

An Equal Opportunity Sell-Off

The S&P 500 fell more than 2% on Friday, and no areas of the market were spared. We broke the S&P 500 into deciles (10 groups of 50 stocks each) based on how stocks performed from the 6/27 post-Brexit low through last Thursday’s close because we initially thought that stocks that did best during that rally might be down the most on Friday. That wasn’t the case, though. When we calculated the average Friday performance of the stocks in each decile, we found that declines were evenly distributed regardless of performance during the post-Brexit rally.

Decile one on the left side of the chart below contains the 50 stocks in the S&P 500 that rallied the most from 6/27 through 9/8. Decile two contains the 50 next best performers, and so on and so forth until you get to decile ten, which contains the 50 stocks in the S&P that did the worst during the 6/27-9/8 rally. The numbers shown represent the average performance on Friday of the 50 stocks in each decile.

Normally during big sell-offs after rallies, you’ll see the stocks that have recently been the biggest winners get hit the hardest. The stocks that went up the least during the rally will typically hold up better during the decline. That wasn’t the case at all on Friday, though. As you can see, every decile’s average stock was down between 2.5% and 3%, and it was actually decile 10 (50 worst stocks during the 6/27-9/8 rally) that saw the biggest average decline (tied with decile five).

GET FREE ACCESS TO ALL OF BESPOKE’S RESEARCH FOR 14 DAYS

(No Credit Card Necessary)

Chart of the Day — Friday Sell Offs

It was bound to happen at some point. After 43 trading days without one, the S&P 500 finally had a 1% one-day move on Friday, and boy did it ever. Also, true to form and as we noted in our Chart of the Day from August 31st, once we finally got one, it was down. The fact that it has been so long since we have seen a big decline coupled with it coming on a Friday only compounded investor concerns heading into the weekend. A 2% decline in the market is bad enough, but when you have to stew over it for the entire weekend, it only makes things worse. Those fears were on display early this morning, as US equity futures traded sharply lower. While they’re still down as of 9 AM ET, they have significantly cut their losses.

It was bound to happen at some point. After 43 trading days without one, the S&P 500 finally had a 1% one-day move on Friday, and boy did it ever. Also, true to form and as we noted in our Chart of the Day from August 31st, once we finally got one, it was down. The fact that it has been so long since we have seen a big decline coupled with it coming on a Friday only compounded investor concerns heading into the weekend. A 2% decline in the market is bad enough, but when you have to stew over it for the entire weekend, it only makes things worse. Those fears were on display early this morning, as US equity futures traded sharply lower. While they’re still down as of 9 AM ET, they have significantly cut their losses.

In today’s Chart of the Day, which was sent to paid subscribers, we look at prior 2%+ declines on a Friday and show how the S&P 500 performed on the following trading day and over the following week. See today’s Chart of the Day by starting a 14-day free trial to Bespoke’s premium research below.

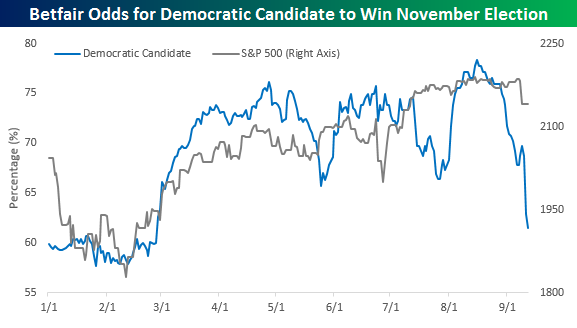

Presidential Election Odds and the Market

Following yesterday’s medical episode involving Hillary Clinton in New York City and the subsequent disclosure that she is dealing with pneumonia, the betting markets saw large moves with respect to the odds of each party winning the election in November. As shown in the first chart below, the odds for Mrs. Clinton to win (which were already well off their peak levels following the DNC Convention) are now down to 61.5. At that level, the odds for the Democratic candidate to win in November are down nearly 17 percentage points from their highs and at their lowest levels since late February.

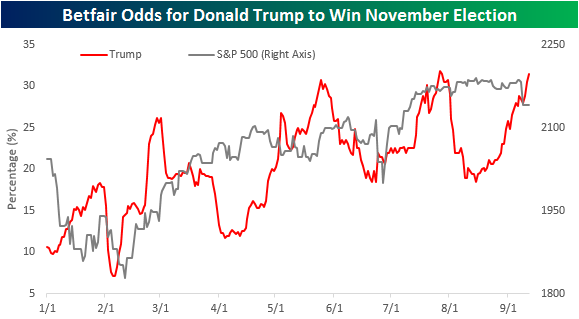

While the odds for Mrs. Clinton and the Democratic Party have declined, the odds for Donald Trump to win have been on the rise. As shown in the chart below, the odds for Mr. Trump are back above 30% and near their highest levels of his candidacy. Mr. Trump’s odds reached similar levels back in late May and July before falling back down again, so it will be interesting to see if he can maintain his momentum this time around, or whether his odds will once again dip. Only time will tell.

Whatever your views are towards the two candidates or how each of them will impact financial markets, the reality is that for the last several months, Mrs. Clinton and the Democratic Party have been the odds on favorites to win in November. If Mr. Trump’s odds prove to be more than temporary and continue to increase as they have in the last few weeks, it will mark a major shift in the prevailing trend that we have seen since Mr. Trump became the odds-on favorite on the Republican side. Good or bad, that is likely to impact financial markets, which have been pricing in a Democratic victory for the last several months.

Bespoke Brunch Reads: 9/11/16

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Sports

A World Cup without Pakistan? by Tim Wigmore (ESPN Cricinfo)

India versus Pakistan is one of the most widely-watched sports events in the world, with a billion viewers tuning in. But the 2017 World Cup (which is almost entirely designed to insure the match takes place) risks no such meeting. A fascinating view of the cricket world, which most Americans barely know exists. [Link]

How to feed a college football team: Start at 4 a.m., and never stop cooking by Roman Stubs (WaPo)

The epic logistics tale (and tail) required to keep a college football team fed is traced in this fascinating insider’s view of the Maryland Terrapins’ team kitchen. [Link; paywall]

Shipping

Hanjin’s Ghost Ships Seek Havens With Food and Water Starting to Dwindle by Sohee Kim and Kyunghee Park (Bloomberg)

A default and bankruptcy has improbably and tragically stranded dozens of ships (and their crews) at sea, unable to dock for fear that port fees will not be paid. [Link target=”_blank”; auto-playing video]

Hanjin’s Stranded Ships Contain One Absurdist Filmmaker by Erica E. Phillips (WSJ)

In an almost perfect twist, one of Hanjin’s ships is currently carrying an absurdist filmmaker, who has been gifted an impossibly fitting situation for her art form. [Link; paywall]

Smashed Fortunes by Biman Mukherji (WSJ)

The global bust in shipping plus volatile steel prices have made the labor-intensive, thin-margined business of shipbreaking centered in Alang, India a painful one to be in. [Link; paywall]

Werner CEO Leathers: TL rates getting back to “equilibrium” after slump by John Schulz (Logistics Management)

An excellent write-up covering the current state of American trucking; mentioned are capacity, capex, rates, and demand. [Link]

History Repeats

Option Pricing Methods in the Late 19th Century by George Dotssis (Essex Finance Centre)

Early options traders demonstrated a remarkable intuitive understanding of options theories which were only formalized by academics in the last half century or so. [Link; 31 page PDF]

Robot Macroeconomics: What can theory and several centuries of economic history teach us? by John Lewis (BoE Bank Underground)

An excellent example of what basic economic theory, not to mention well-documented economic history, teaches us about the outlook for employment when capital (possibly robots in the future) supplants labor. [Link]

Labor Market Responses

Alphabet and Chipotle Are Bringing Burrito Delivery Drones to Campus by Alan Levin (Bloomberg)

Drones carrying Chipotle burrito payloads will soon drop off chow to hungry students at Virginia Tech, in an exciting new (and FAA approved) experiment. [Link; auto-playing video]

McDonald’s Free Housing Lays Bare East Europe’s Labor Crunch by Zoltan Simon (Bloomberg)

With workers in very short supply, the Golden Arches has become a purveyor of bunks as well as Big Macs and Coke. [Link]

Hedge Funds

Private Equity Is the New Hedge Fund by Lisa Abramowicz (Bloomberg)

With institutional capital no less hungry for returns amidst disappointing hedge fund performance, less liquid private equity is getting more attention. [Link]

This Hedge Fund Made 2,100% From World’s Most Extreme Market Mania (Bloomberg News)

A look inside the operations of one of the most successful speculators to trade the recent extreme volatility in Chinese commodity futures. [Link]

Startup Economy

A Cleaning Start-Up Wielding Mops, Buckets and 700 Data Points by Eilene Zimmerman (NYT)

Data collection has started to make an impact for a tech-fueled competitor in the highly fractured cleaning services market (worth $51 billion and with tens of thousands of firms). [Link; paywall]

When your boss is an algorithm by Sarah O’Connor (FT)

Depending on your point of view, apps which intermediate passengers and drivers or hungry people and food delivery workers are either a blessing or a curse. [Link; paywall]

US Labor

Video killed the radio star by Erik Hurst (Chicago Booth School of Business Review)

Are video games the reason there are millions of Americans “missing” from the post-recession labor market? [Link]

Hunt for Holiday Workers Heats Up, Giving Wages a Boost by Laura Stevens and Loretta Chao (WSJ)

With fewer and fewer Americans looking for work, filling seasonal positions which surging pre-Christmas sales volumes require is becoming more difficult for many companies. [Link; paywall]

Politics

In Germany, Tax Cuts Go From Taboo to Potential Political Tool by Andrea Thomas (WSJ)

As absurd as it may sound from an American’s perspective, German voters would much rather see infrastructure spending than a reduced tax burden. [Link; paywall]

Why Trudeau Is Like Trump by Stephen Marche (Bloomberg)

While their politics, temperament, and tone could not be more different, Canadian Prime Minister Trudeau and GOP candidate Trump share a remarkable proficiency with social media. [Link]

‘What Is Aleppo?’ Gary Johnson Asks, in an Interview Stumble by Alan Rappeport (NYT)

We don’t link to this story for the rather boring gaffe which will quickly be forgotten by Libertarian candidate Gary Johnson; frankly, nobody cares. What’s truly amusing is the correction, in which the Times notes it also got the significance of Aleppo, Syria wrong in the very article calling attention to Johnson’s lack of knowledge. Irony lives! [Link; paywall]

Pop Culture

The Oral History of the Comedy Central Roast By Julie Seabaugh (Paste Magazine)

A fantastic rundown of the hilarious and irreverent and frankly very American tradition of televised roast for our most reviled – and attention-getting – celebrities. [Link]

The Minivan Is Back, and It’s Kind of Cool by Kyle Stock (Bloomberg)

Once a (perhaps unfairly) derided symbol of suburban drudgery, minivan sales are accelerating thanks to new models and a mini-boom in births. [Link]

New Species

‘Superbug’ scourge spreads as U.S. fails to track rising human toll by Ryan McNeill, Deborah J. Nelson and Yasmeen Abutaleb (Reuters)

Wide prescription of anti-biotics has resulted in numerous strains of resistant bacteria, and health authorities (not to mention the health care industry) are dropping the ball in preventing their spread. [Link]

The Last 100 Days: A-parasitic-hairworm-named-Obama edition by Olivier Knox (Yahoo!)

With ever-more species discovered, many scientists have resorted to a rather unoriginal source for the names bestowed on their finds. [Link]

Mapping The Bad Stuff

The Geography of U.S. Inequality by Quoctrung Bui (NYT Upshot)

A data-driven view of the change in median incomes over time at the state level. Very interesting work, and the geography is counter-intuitive, in our view. [Link; paywall]

Who Falters at Student Loan Payback Time? by Rajashri Chakrabarti, Michael Lovenheim, and Kevin Morris (NY Fed Liberty Street Economics)

A great effort at assessing what type of student is most at risk of going into default on their student loans, and one that should inform policymakers in our view. [Link]

Economic Musings

Dissecting The Fed’s Foreign Repo Pool – The Users (Concentrated Ambiguity)

Foreign central banks have become huge counterparties to the Federal Reserve, placing large USD deposits with the bank via repo transactions. This excellent post dissects which central banks are doing so. [Link]

The Fable of the Ants, or Why the Representative Agent is No Such Thing by Jo Michell (Medium)

An excellent overview of some assumptions which underpin macroeconomic models, and why they may be outdated and incorrect. [Link]

Can trivia help us to be less ignorant of our own ignorance? by Tim Harford (The Undercover Economist)

The Dunning-Krueger effect describes our own serial over-confidence in our own knowledge base. But is the cure found at a weekly meet up with friends over a pint for a little pub quiz? [Link]

Software

Washington Post Unveils ‘Lightning-Fast’ Mobile Website by Jack Marshall (WSJ)

Loading times are touted to fall by over 60% using a new Google technology kit. This matters: 70% of the Post’s traffic comes from mobile. [Link; paywall]

Goldman Sachs Has Started Giving Away Its Most Valuable Software by Justin Baer (WSJ)

SecDB, long a closely guarded competitive advantage, is now being used to power client applications and data queries. [Link; paywall]

China

One Belt, One Road explained by Khalid Hashim (Splash 24/7)

A one-stop shop overview of China’s huge program to transform the infrastructure which links it to the rest of Asia. [Link]

Unrealistic Ambitions

A 24-year-old Chipotle cook is dishing up savvy investing advice to a $40-billion-dollar hedge fund by Rachael Levy (Business Insider)

In a frankly unconventional move, a 24 year old burrito slinger has announced a $1000 activist stake via a personal email to hundreds of hedge funds. [Link]

Exclusive: How Elizabeth Holmes’s House of Cards Came Tumbling Down by Nick Bilton (Vanity Fair)

Once hailed as a demi-messiah, the venture-backed founder of Theranos is now facing investigations, recriminations, and the end of the line. [Link]

Primary Market

Taking stock: Going public in volatile times (ReedSmith)

A deep and engaging read summarizing a survey which questions companies on how they plan to raise capital from the public markets. [Link]

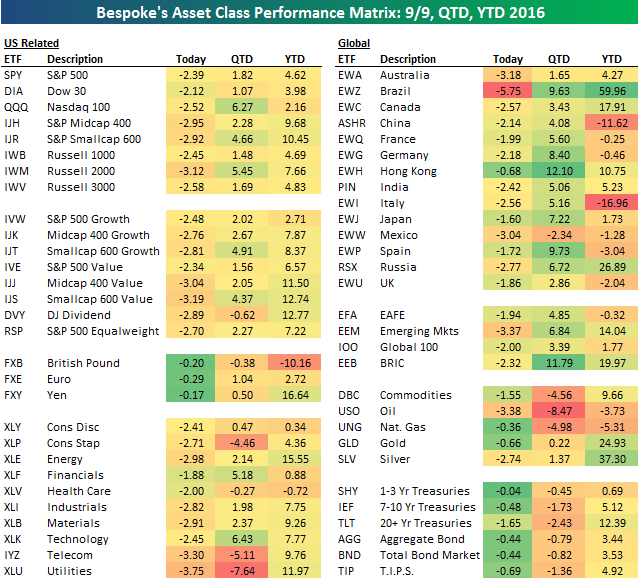

The BESPOKE REPORT — 9/9/16

No asset classes were spared to close out the trading week today. Below is our asset class performance matrix, which highlights the recent performance of ETFs across the financial spectrum.

As you’ll see, every single ETF in the matrix was down today, including all of the currency, commodity and fixed income ETFs. Talk about a brutal day for investors.

We analyze today’s market drop, the Fed, economic indicators, sentiment and more in this week’s Bespoke Report newsletter. You can read the entire report by starting a 14-day free trial to our paid content below.

Have a great weekend!

The Closer 9/9/16 – End of Week Charts

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!