July 2017 Headlines

Bespoke’s Global Macro Report — 8/2/17

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

Click here to start a no-obligation two-week free trial to Bespoke Institutional!

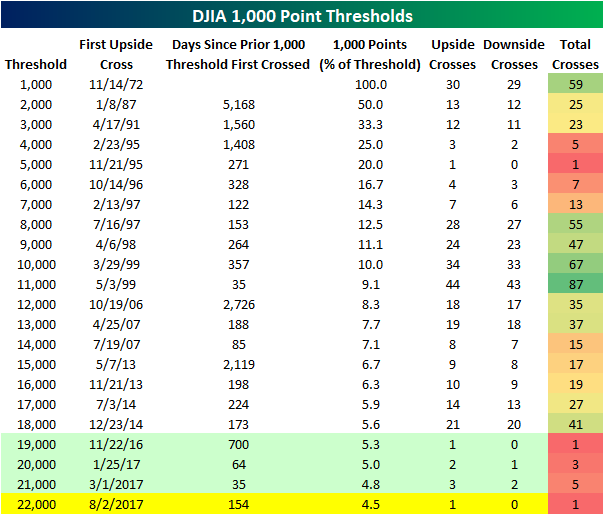

19K, 20K, 21K, 22K…

The thousand point thresholds are dropping like flies these days. With the caveat that a thousand points becomes an increasingly small percentage of the overall index as prices rise, the DJIA just crossed its fourth 1,000 point threshold since Trump’s election last November. The table below shows the date that the DJIA has first crossed each 1,000 point threshold on a closing basis since it first closed above 1,000 back on 11/14/72. For each threshold, we show the date the DJIA first closed above that threshold, how many days transpired between that cross and the prior 1,000 point threshold, the percentage that each thousand point threshold represents of the index’s price, and then how many upside and downside crosses the DJIA has had with each level.

Since the election, the DJIA has now crossed four thousand point thresholds, and with each one, there has been very little in the way of looking back. For instance, once the DJIA crossed 19,000 it never closed back below that level. For 20,000, once it crossed that level, it only closed below it again once, while 21,000 only saw two subsequent closes. In looking for comparable periods, the current period is somewhat similar to the late 1990s, when the DJIA also crossed several 1,000 point thresholds in very short order. In the current period, these levels have been coming and going a lot faster, but again, it’s also important to remember that they represent a much smaller percentage of the overall index’s value than the levels that were crossed in the 1990s. Finally, while it may seem as though the move from 21K to 22K was quick, at 154 calendar days (if that level holds between now and the closing bell), it was nearly five times longer than the time that elapsed between 20K and 21K (35 days) and two and a half times longer than the time it took to go from 19K to 20K.

Chart of the Day – What if Apple Wasn’t Apple?

The Closer — Flier On Dollars, Americas Data — 8/1/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at the outlook for the dollar (starting to improve) as well as a review of a variety of US and Brazilian data released today.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See today’s post-market Closer and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research platform!

Bespokecast Episode 15 — Karthik Sankaran — Now Available on iTunes, GooglePlay, Stitcher and More

We’re happy to announce that the newest episode of Bespokecast is now available to the general public both here and via the various podcast platforms. Be sure to subscribe to Bespokecast on your preferred podcast app to gain access to our full collection of episodes. We’d also love for you to provide a review as well!

We’re happy to announce that the newest episode of Bespokecast is now available to the general public both here and via the various podcast platforms. Be sure to subscribe to Bespokecast on your preferred podcast app to gain access to our full collection of episodes. We’d also love for you to provide a review as well!

In our newest conversation on Bespokecast, we sit down with Karthik Sankaran of Eurasia Group. Karthik is Director of Global Strategy for Eurasia Group, a role that requires him to integrate global economics, financial markets, and politics. His understanding of history, theory, and practice of the different disciplines he uses gives a fascinating perspective on current events and what happens next. In our conversation, we discuss his career path, global financial imbalances (and their political roots), the Eurozone’s “immune system”, Angloskepticism, where to get the best Chinese food in New York City, and what it’s like to speak five languages in a world increasingly concentrated on English. We hope you enjoy the conversation! You can catch more of Karthik’s thoughts on Twitter here.

To listen to our newest episode or subscribe to the podcast via iTunes, GooglePlay, OvercastFM, or Stitcher, please click the button or links below.

Bespoke Stock Scores: 8/1/17

Chart of the Day: July 2017 Decile Performance

ETF Trends: US Sectors & Groups – 8/1/17

Coffee is a big winner in this week’s edition of our ETF Trends report, seeing gains almost twice as large as our 2nd best performing ETF, GDXJ. US Oil continues its strong performance that started about a week ago, up over 3%. Also reemerging this week is a trend we saw about 2 weeks ago, the outperformance of a host of central European countries, led by Poland, Norway, Belgium, and Austria. On the losing side, Natural Gas continues to tank, down almost 6%, along with other notables Biotech, Transports, and Health Care providers. Natural Gas is now down nearly 10% over the last 10 days.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

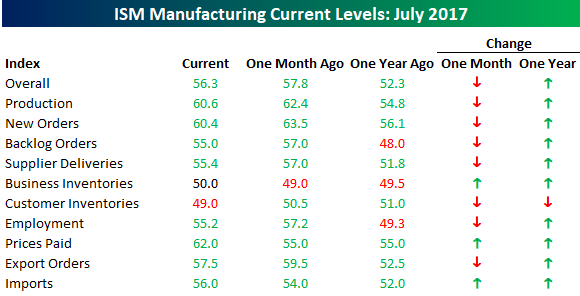

Weaker Than Expected Strong ISM Manufacturing Report

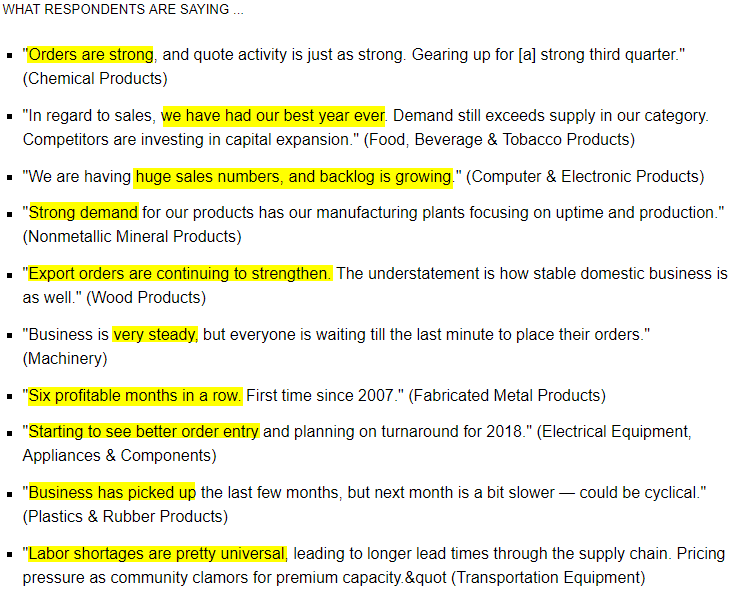

The headlines will say that today’s ISM Manufacturing report was weaker than expected, continuing a trend we have seen in the data for some months now, but the reality is that today’s report was still very strong. Just look at the commentary associated with today’s report. Whenever you see adjectives like strong, best, huge, and steady dominate, it’s a sign of strength, and this month’s commentary was littered with them. There was literally not one mention of a weaker manufacturing environment!

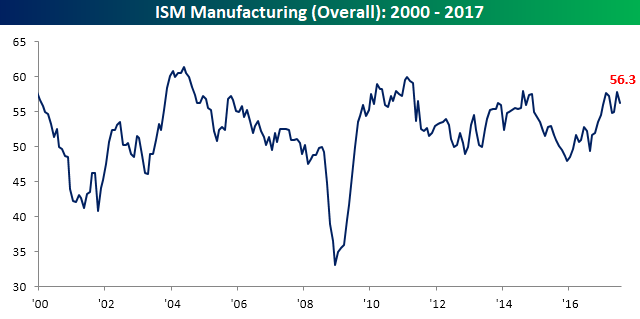

As shown in the chart below, the headline index in this month’s report dropped from a multi-year high of 57.8 to a still strong reading of 56.3. Even at current levels, though, the index is near its highest levels of the expansion.

Taking a quick look at the internals of the report, they were mostly similar to the headline index, as declines were relatively muted and mostly coming from their highest (or near highest) levels of the expansion. The only categories which showed m/m increases were Prices Paid and Import Orders. While the increase in Prices Paid makes sense given the weaker dollar, a pickup in import orders doesn’t usually go hand in hand with a weak dollar. On a y/y basis, most components of the ISM are up considerably from their levels one year ago. The only category to see a decline was Customer Inventories.

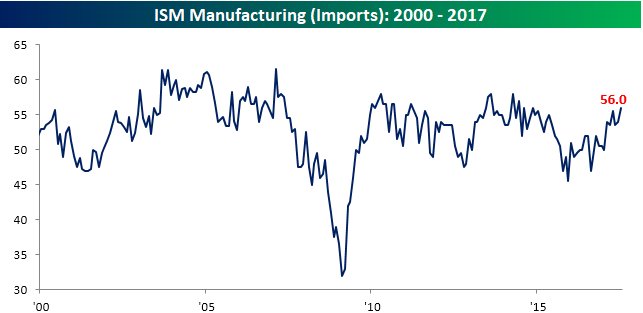

As mentioned above, Import Orders was one of only two categories that ticked higher this month even as the dollar weakened. What makes this month’s increase in the Import Orders category even more significant is that it’s the highest reading in more than three years!

Finally, each month ISM also asks respondents which commodities are up in price, down in price, and which are in short supply. In this month’s survey, respondents noted shortages in eight different commodities, which is extremely high by historical standards. Going back to 2000, there has never been a month where more commodities were in short supply, and the last time there were eight was back in October 2005.