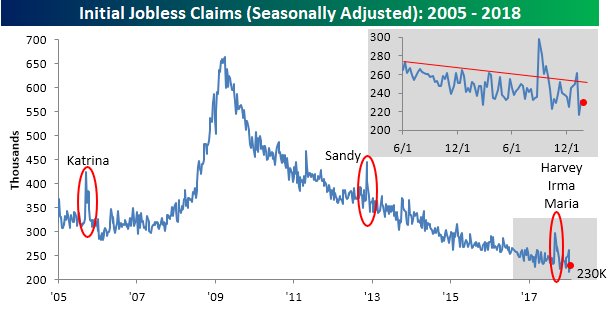

Jobless Claims Drop to 230K

Jobless claims were lower than expected this week and continue to hang around near their lowest levels in decades. While economists were expecting claims to rise from 231K up to 235K, they actually fell slightly to 230K. Throughout the entire economic expansion, jobless claims have only been lower in five different weeks. Furthermore, claims have now been below 300K for 152 straight weeks. If they stay below that level for another ten weeks, it will represent the longest streak of sub-300K readings on record (going back to the late 1960s), and this doesn’t even take population growth into account!

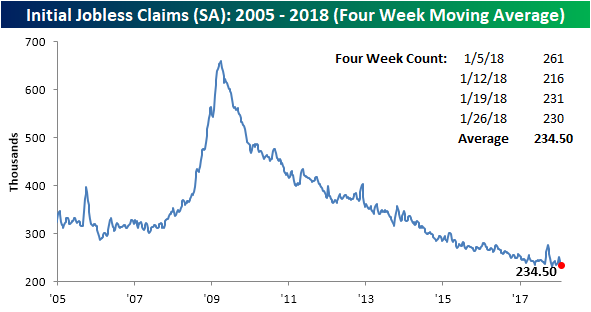

The four-week moving average for jobless claims also declined this week, falling from 239.5K down to 234.5K. That puts this reading within 3.5K of the multi-decade low of 231.25K from early November. Next week, the four-week moving average will drop a reading of 261K from the count, so barring a big increase in claims, we should see this reading make a new cycle-low next week.

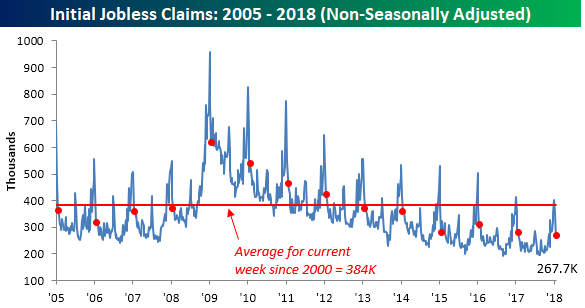

On a non-seasonally adjusted (NSA) basis, jobless claims were just as positive. This week’s level of 267.7K is more than 115K below the average reading for the current week of the year dating back to 2000. To find the same week of the year where NSA claims were lower, you have to go all the way back to 1973.

The Closer — Fed Hold, ECI Acceleration, EIA Data — 1/31/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review the FOMC’s policy decision today, update our tracking of wage growth as indicated by the BLS’s employment cost index, and finally recap weekly petroleum market data and energy market price action.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Record Streak Without a 3%+ Pullback

On Monday the S&P 500 broke a streak of 99 trading days without a 0.60%+ decline. Then yesterday the index broke a streak of 310 trading days without back-to-back declines of 0.50%+ or more.

One streak that is still going, however, is the record length of days it has been without a 3% pullback. It has now been 448 calendar days since the S&P 500 last fell 3% from a closing high.

Below is a chart showing streaks without a 3%+ pullback for the S&P 500 throughout its entire history. Late last year we broke the prior record of 370 days set back in 1995, and since then the S&P hasn’t looked back.

We might be getting close, though. Since last Friday’s high, the S&P is now down 1.7%.

Streaks are made to be broken, and this one will eventually be broken as well. It’s been quite the ride!

Chart of the Day: A Concrete Opportunity

B.I.G. Tips — February 2018 Seasonality

Bespoke Matrix of Economic Indicators: 1/31/18

Fixed Income Weekly – 1/31/18

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s note, we review the interest rates implied by BTC futures curves.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Bespoke’s Global Macro Dashboard — 1/31/18

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

The Closer — Another AMZN Story, Homeownership + Prices Surge, Red Screens — 1/30/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at the latest attention-grabbing Amazon initiative, updated US homeownership and household formation data, a wild day in the markets, and the January print for Conference Board Consumer Confidence.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

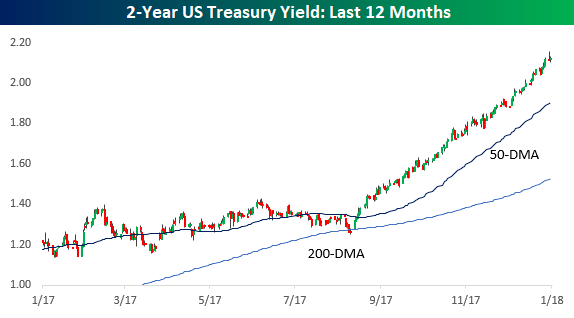

Two-Year Yield on Auto-Pilot

Lately, we’ve been highlighting a number of crazy streaks involving the steadiness of equities in the last several months, but have you seen a chart of the two-year yield lately? While the yield had its share of ups and downs during the first three quarters of 2017, ever since then it has been on auto-pilot to the upside, rising from 1.4% up to over 2%. Looking at this chart, there has been a consistent gap between the current yield and its 50-day moving average to the point where the yield has finished each of the last 98 trading days at least one standard deviation above that level.

Look at the chart above again, because it’s unlikely you will ever see anything like it in a long time, at least if the last 40+ years is any indication. That’s because there has never been a time in the two-year Treasury’s history where it has been more than one-standard deviation above its 50-DMA for this long. Conversely, there has never been a streak where the yield on the two-year was this far below its 50-DMA for this long either.

The chart below shows historical streaks (in trading days) where the two-year US Treasury yield was more than one standard deviation above its 50-DMA or more than one standard deviation below it. In terms of closes above that level, the longest streak prior to the current one was back in 1994 when there were actually two back to back streaks of 70+ trading days. If you don’t remember 1994, it was another period where short-term interest rates steadily rose from just under 4% to just under 8% following a long period of dormancy. That increase in rates culminated with the bankruptcy of Orange County, California in December 1994. On the downside, the longest streak where the yield on the two-year closed more than one standard deviation below its 50-DMA ended in January 1985 during a period where the yield declined from close to 12% to just under 10%.