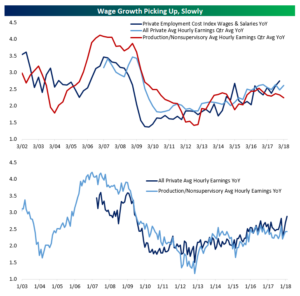

Wages Picking Up

Today we’ll have three quick blog posts discussing some data from this month’s nonfarm payrolls report. In this first post, we’ll focus on wages. As shown in the chart below, YoY growth of average hourly earnings for all private employees is at its strongest pace since the aftermath of the recession. YoY growth for last month was also revised up to +2.7%. As shown below, though, production and non-supervisory average hourly earnings growth (pay for non-managerial earners) is not accelerating as dramatically. We should also note that earlier this week the employment cost index for Q4 showed the strongest YoY wage and salary growth in the post-recession period. The ECI adjusts for the composition of the labor force, so if anything the relatively strong pace of growth we’ve seen in wages recently could be understated.

For more of Bespoke’s economic/macro analysis, start a 14-day free Bespoke Institutional trial today.

January 2018 Headlines

The Closer — Productivity, Auto Sales, 60/40 — 2/1/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at US productivity, grim US auto sales (including some brutal numbers from Ford and Fiat-Chrysler), and update our tracking of the pain this week’s price action has wrecked on balanced stock/bond portfolios.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke’s Sector Snapshot — 2/1/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

Below is one of the many charts included in this week’s Sector Snapshot, which highlights the 10-day advance/decline line for the S&P 500. Even though the S&P’s price level is still overbought, the index’s 10-day advance/decline line (an important breadth measure) has moved back into neutral territory.

To learn more about the 10-day A/D line and see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

Bespoke Consumer Pulse Report — February 2018

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and the results from this month’s survey were certainly enlightening. Along with a few under-the-radar shifts in consumer sentiment towards the economy that we found, we also continue to see extremely high levels of bullish investor sentiment. Start a 30-day free trial to see just how extreme the investor sentiment numbers have gotten.

Chart of the Day: Productivity Plateau

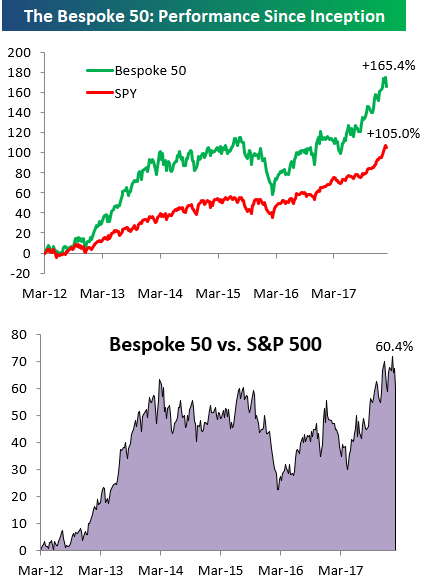

the Bespoke 50 — 2/1/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 60.4 percentage points. Through today, the “Bespoke 50” is up 165.4% since inception versus the S&P 500’s gain of 105.0%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

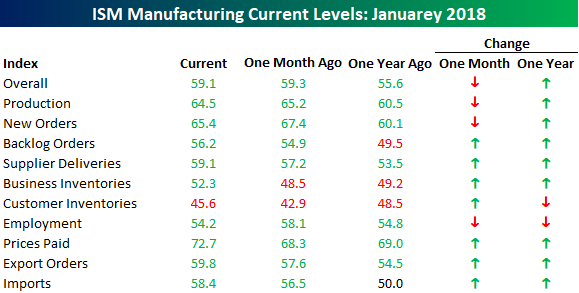

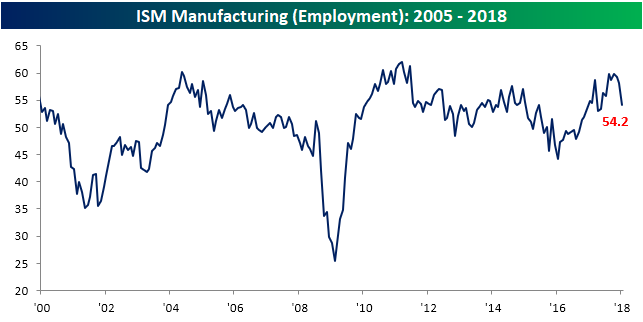

ISM Manufacturing Kicks off January Data on a Positive Note

Manufacturing activity in the US appears to have kicked off the year on a positive note as the ISM Manufacturing report for January saw a slight decline but came in higher than expected. While economists were forecasting a headline print of 58.6, the actual reading came in at 59.1 compared to December’s reading of 59.3. Despite the decline, it was still the fifth highest monthly print of the current expansion.

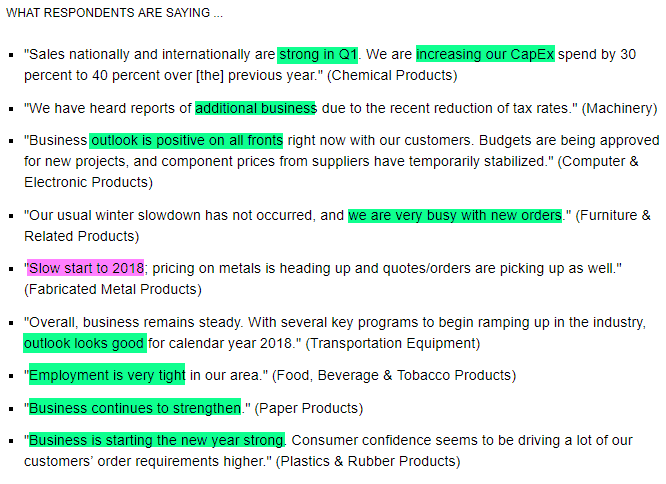

Commentary from respondents was also positive this month. Outside of the Fabricated Metals sector, manufacturers are seeing strong levels of business to start 2018.

The table below breaks down this month’s report by each of the index’s subcomponents relative to last month and last year. Over both time frames, breadth in the report was strong. On a m/m basis, just three of ten subcomponents declined (Production, New Orders, and Employment- chart below), while on y/y basis, Customer Inventories and Employment were the only decliners. On the upside, Prices Paid saw a pretty big increase this month rising to its highest level since May 2011.

Sluggish Truck Sales From Ford

As regular readers are aware, we pay a lot of attention to monthly truck sales. Trucks are not only higher margin, but they are often purchased by small businesses and contractors so they provide a good read on the health of the small business sector. Based on these sales totals for January, small businesses are still expanding, but the pace of sales growth in January slowed after a Monster December. For the month of January, total truck sales came in at 58,937. While that’s a strong number relative to history (5th strongest since 1996), on a y/y basis it represents an increase of only 1.6% even though this past January had one extra selling day compared to January 2017. It’s hard to complain when sales are so close to the high end of their historical range, but it’s something investors have come to expect.

Individual Investors A Bit Less Confident

For all the talk about a supposed correction in the last few days, you wouldn’t know it from the chart of the S&P 500 and bullish sentiment below. If you squint real close, you can see something resembling a small decline for the S&P 500 (red line), but it’s negligible at best. That hasn’t stopped individual investors in the weekly AAII survey from becoming a little bit more cautious, though. In this week’s survey, bullish sentiment declined from 45.5% down to 44.8%. That’s the third weekly decline in the last four weeks, and during that time the bullish ranks have thinned by 15 percentage points. We’ve commented in the past several days that because markets have seen such a steady climb upward, even small declines in equity prices may spook investors and you could argue that the weekly sentiment numbers from AAII are showing just that.

Bearish sentiment, meanwhile, has been moving in the opposite direction. This week’s survey showed an increase in pessimism of nearly five percentage points as bearish sentiment increased from 24.0% up to 28.8%. In the last four weeks, bearish sentiment has now nearly doubled from its second lowest reading of the bull market back in early January.