The Closer: End of Week Charts — 2/9/18

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. This week, we’ve added a section that helps break down momentum in developed market foreign exchange crosses.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

S&P 500 Quick-View Chart Book: 2/9/18

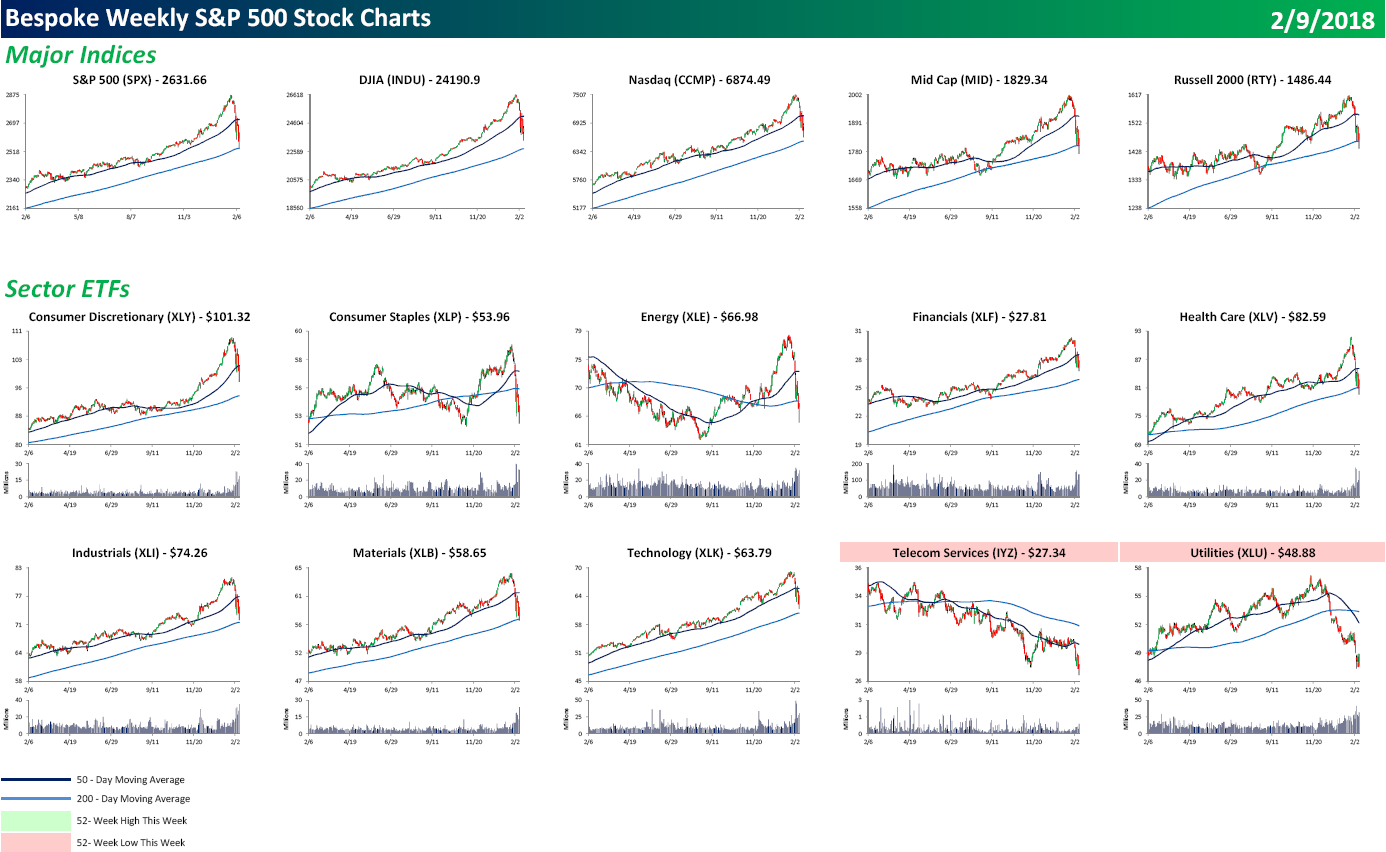

Each weekend as part of our Bespoke Premium and Institutional research service, clients receive our S&P 500 Quick-View Chart Book, which includes one-year price charts of every stock in the S&P 500. You can literally scan through this report in a matter of minutes or hours, but either way, you will come out ahead knowing which stocks, or groups of stocks, are leading and lagging the market. The report is a great resource for both traders and investors alike. Below we show the front page of this week’s report which contains price charts of the major averages and ten major sectors.

Looking through the Chart Book this week, there are a number of broken looking charts, as all the major averages and sectors are below their 50-DMA. Utilities have been especially weak as the sector hit a 52-week low. In terms of individual stocks, 62 members of the S&P 500 hit 52-week lows this week, and they were spread out across just about every sector. In fact, the only two sectors where not a single stock hit a 52-week low were Technology and Telecom Services (which has just three stocks in it). Real Estate was one of the weakest sectors with 19 different components of that sector hitting new lows. It just hasn’t been a good year for interest rate sensitive stocks.

To view our entire S&P 500 Chart Book, sign up for a 14-day free trial to our Bespoke Premium research service.

B.I.G. Tips – You Don’t See This Very Often

The chart below comes from the second page of our Morning Lineup report, and it shows the S&P 500’s price relative to its 50-day moving average (DMA) expressed in standard deviations. When the line is in the white areas, the S&P 500 is trading at neutral levels. Readings in the light red (or light green) areas are considered overbought (or oversold), while readings in the dark red (or dark green) are considered extremely overbought (or oversold). Yesterday, we tweeted the chart out calling it El Capitan after the rock formation in Yosemite National Park, but a more apt Yosemite analogy after today may be Yosemite Falls.

The types of move that we have seen over the last two weeks in the S&P 500’s trading range aren’t seen too often. In the span of two weeks, the S&P 500 has gone from an extreme overbought reading to an extreme oversold reading (as of Friday afternoon). While that could change depending on where the S&P 500 settles at the end of the day, at the very least, we have seen the S&P 500 shift from extremely overbought as of 1/26 to an oversold level as of yesterday.

What makes the move that we have seen over the last two weeks even more dramatic is the fact that leading up to it there had been only two other trading days over the last year where the S&P 500 even traded at oversold levels in the past year! Whether you want to call it a slap in the face, a reality check, or something else, investors have been quickly reminded of the fact that equities move in both directions.

Following this move where the rubber band has gone from being stretched in one direction to another, we wondered whether it tends to snap back again or just snap. To that end, we just published a report looking at prior periods in the S&P 500’s history where the index has gone from trading at extreme overbought levels to oversold or extreme oversold levels in the span of two weeks or less.

If you’re interested in the report, you can read it by signing up for a Bespoke Premium membership now!

S&P 500 Corrections

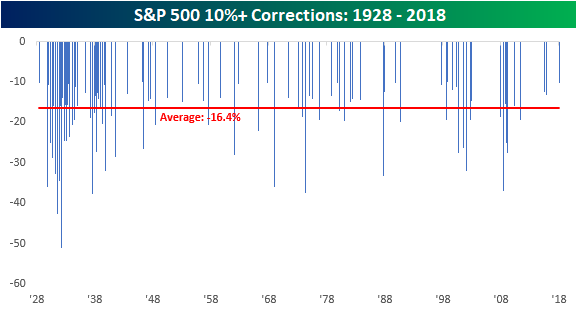

After nearly two years without one, the S&P 500 officially entered correction territory yesterday, falling 10.2% from its 1/26/18 all-time closing high. The current correction represents the 96th decline of 10%+ from a closing high that followed a gain of at least 10%. The chart below shows the magnitude of every prior correction for the S&P 500 since 1928. Not including the current period, the median decline for the S&P 500 in the 95 prior corrections was a decline of 16.4% over the course of 64 days. Keep in mind, though, that these are median levels. There have been a number of corrections (13) that saw declines of less than 11%, while several saw deeper declines of more than 20%. In terms of length, prior corrections have also been all over the map. Some have lasted as little as three days, while others have stretched on for well over a year.

Unfortunately, there is no hard and fast rule when it comes to corrections, and that’s what can make them so terrifying when you go through one. You never know when it will end. Throughout history, market corrections have ‘typically’ occurred a little more than once per year. As mentioned above, there have been 96 corrections since 1928, but if you look at their distribution over time, a good deal of them were clustered around the Great Depression. If we look just at the post-WWII period, there have been 55 corrections in the span of 73 years, reducing their frequency to once about every 16-17 months. In any event, the market was still overdue for a correction heading into the current one, but maybe not by as much as it seemed on the surface.

The Closer — A Correction Comes — 2/8/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we make the case that downside for equities is limited from current levels, based on technicals, the economic back drop, and historical precedent, with each reviewed in turn.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

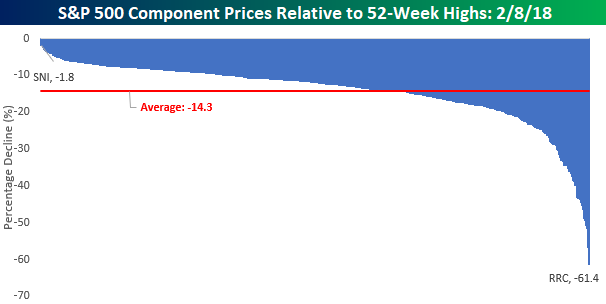

How Much Are Individual Stocks Down From Their 52-Week Highs?

The S&P 500 is currently down about 8.5% from its 52-week high less than two weeks ago, but the average stock in the S&P 500 is now down 14.3% from its respective 52-week high. That may seem like a pretty wide discrepancy, but it’s actually pretty common for the individual stock reading to be much lower than the index itself due to the fact that not all stocks hit 52-week highs at the same time as the index. In fact, you rarely even see a third of stocks hit an all-time high on the same day.

While the ‘average’ stock is down 14.3%, the vast majority of stocks are down less than the average – 328 to be exact. Of those 328 names, 170 are still down less than 10% from their respective highs. So who is currently the biggest loser in the S&P 500? That title belongs to Range Resources (RRC). At a current price of $13.16, RRC is down over 60% from its 52-week high. Behind RRC, there are three other stocks down over 50%. They are Chesapeake (CHK), General Electric (GE), and Envision Healthcare (EVHC). The demise of GE has certainly been a major fall from grace. While the stock didn’t perform well under the leadership of Jeff Immelt, it hasn’t been any better since he left. In fact, since Immelt officially retired on October 2nd, 2017, GE shares are down more than 40%!

On the upside, shares of Scripps Networks (SNI) have been holding up better than any S&P 500 stock as they are down less than 2% from their 52-week highs.

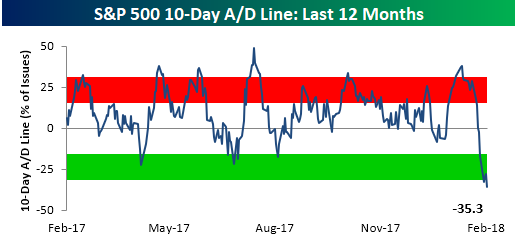

El Capitan!

In our latest update to the 10-day advance/decline (A/D) lines in our Sector Snapshot report for clients, we couldn’t help but think of the rock formation El Capitan in Yosemite National Park. The chart below shows the S&P 500’s 10-day A/D line over the last year. If you are unfamiliar with the term 10-day A/D line, it is simply a rolling 10-day total of the net number of stocks in the S&P 500 rising and falling on a daily basis. When the line is positive it means more stocks are rising than falling, while a falling line means the opposite. Over the course of the last two weeks since the S&P 500’s closing high on 1/26, the 10-Day A/D line has seen an outright collapse, falling to levels not seen at any point in the last year.

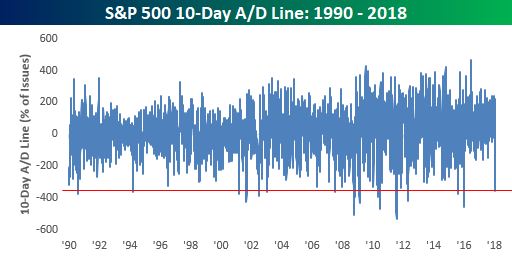

While the big drop in the 10-day A/D line is a big outlier relative to levels from the last year, from a longer-term vantage point, there have been several other periods where the 10-day A/D line was as low or lower. The most recent occurrences came back in early 2016 when the S&P 500 was getting off to its worst start to a year on record. Before that, we saw another extreme reading back in August 2015. Besides these two instances, other periods during the current bull market where the 10-Day A/D line was more negative than it now came in May 2010 (Europe Debt Crisis), August 2011 (US Debt Downgrade), and May 2012 (Greek Debt Crisis).

Bespoke’s Sector Snapshot — 2/8/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

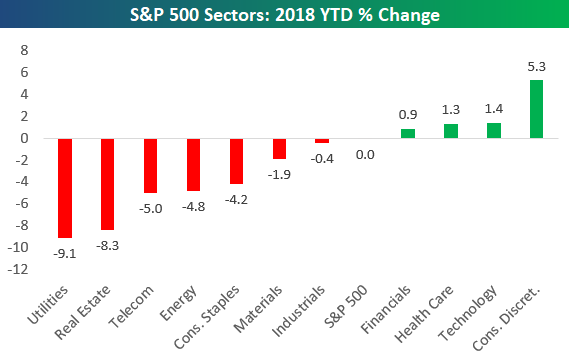

Below is one of the many charts included in this week’s Sector Snapshot, which highlights the year-to-date change of the S&P 500 and its eleven sectors. Just last week nearly every sector was up significantly in 2018. Now there are just four sectors that remain in positive territory, while seven are in the red. Ouch.

To see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

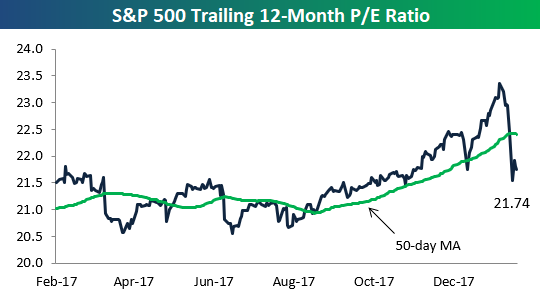

One Benefit of the Selloff — Lower Valuations

Below is a quick snapshot of the S&P 500 run through our trading range chart. After trading overbought for four consecutive months and then going parabolic in January, the S&P has been re-introduced to the concept of “mean reversion.”

One benefit of the mean reversion is that valuations have fallen quite dramatically in the span of less than two weeks. As shown below, the S&P 500’s trailing 12-month P/E ratio had stretched above 23 at the end of January, but it now sits below 22 at 21.74. As long as earnings (the “E” in P/E) remain strong, any price decline in the S&P will cause further declines in the P/E.