The Closer — Powell On The Hill — 2/27/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we dissect testimony from Fed Chair Powell on Capitol Hill today. We also review a big swathe of economic data released today related to manufacturing and trade.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Consumer Confidence Hits a 17-Year High

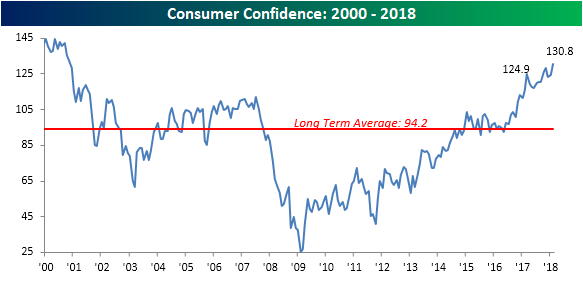

Tuesday morning’s report on Consumer Confidence for February handily topped already positive expectations, as the headline index came in at 130.8 (versus expectations for 126.0), which was the highest level since November 2000. While Consumer Confidence had a hard time getting above its long-term average for much of the current expansion, it has now been above that level of 94.2 for 21 straight months.

One area of the economy where consumers are very confident is in employment. More and more lately, the percentage of consumers who consider jobs as being ‘plentiful’ has been on the rise. In February’s report, it came in just under 40%, which was the highest level since April 2001. It only makes sense that consumers who are confident also think jobs are easy to get.

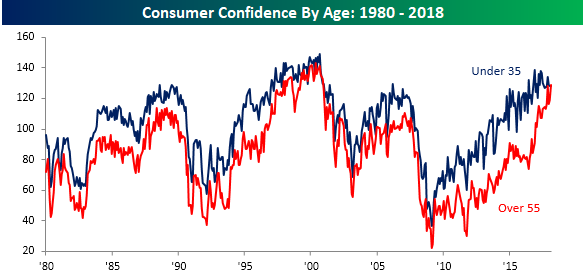

One of the more interesting trends in confidence since the November 2016 election is the shifting demographics of confidence levels. In a nutshell, younger consumers (under 35) have seen little in the way of a confidence boost since President Trump was elected, while older consumers (over 55) have seen confidence surge. After the generational divide between the two age groups widened considerably during the early to mid part of the expansion, confidence levels are now roughly equal.

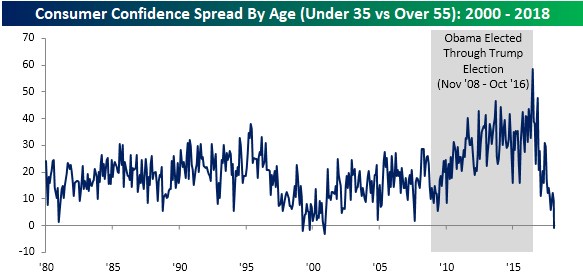

Looking at how the spread between the two has changed over time, you can actually see that as of the most recent report, confidence among older consumers is now higher than it is for younger consumers. This type of confidence inversion is so rare in fact that it has only occurred three other times since 1980, and all of them came in 1999 and 2000. Another interesting trend to notice is that throughout the terms of President Obama, the confidence gap between younger and older consumers steadily rose. Right after President Trump was elected, however, that gap was quickly erased. You know where to find the President’s base!

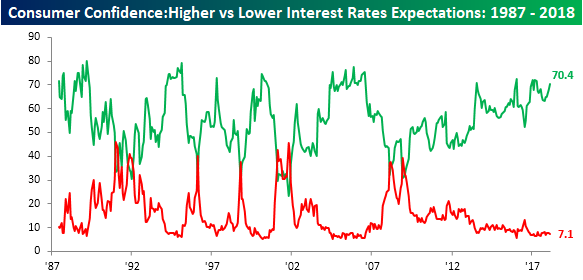

While politics has a lot to do with the shift in confidence among different age groups, another factor is interest rates. President Obama’s tenure also coincided with a period when interest rates were generally at or very close to zero. The impact of low-interest rates has nearly the exact opposite impact on older Americans (who generally have more savings) than it does on younger Americans (who usually have more debt). When you think about it that way, it makes a lot more sense that confidence among older Americans started to improve right after interest rates bottomed.

As far as sentiment towards the direction of interest rates, more than two-thirds (70.4%) of consumers expect interest rates to rise, while just 7.1% expect rates to fall. This view among consumers has generally been in place for the last several years. While it’s tempting to look at such a lopsided split between the two and want to take the other side, when rates are at or near zero, there is really nowhere to go but up!

Chart of the Day: Big Retreat From Record Bullishness

Bespoke Stock Scores — 2/27/18

The Closer — Savings & Investment — 2/26/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at savings and investment by sector, and update our tracker for the capex outlook.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

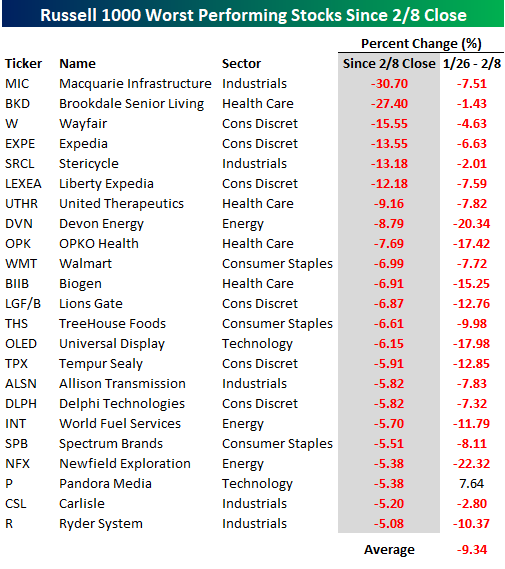

Top Performing Stocks Since February Low

It may be hard to believe, but it has now been a full month since the S&P 500 last closed at a record high. During that span, we have seen one of the quickest 10%+ declines from an all-time high, followed by an impressive rally off the 2/8 lows. During the equity market’s leg down, the average decline of stocks in the Russell 1000 was a drop of 9.7%, and breadth was terrible with 951 of the 975 stocks in the Russell 1000 posting negative returns. The rally on the way up has been a bit weaker in magnitude and breadth, but still strong in its own right. Since the 2/8 closing low, stocks in the Russell 1000 are up an average of 6.0% and all but 98 stocks in the Russell 1000 have seen their share price rise. In the table below, we wanted to highlight both the biggest winners off the lows as well as those stocks that haven’t even been able to rally in a very strong tape.

We’ll start with the winners. Since 2/8, there have been 28 stocks in the Russell 1000 that have rallied more than triple the average 6.0% rally of all stocks. In the table below, we have listed each of those names along with how they performed during the downturn as well. Overall, these stocks saw larger declines than the rest of the market on the way down, but they have more than made up for that weakness on the way up. Fifteen of these stocks have risen more than 20% including US Steel (X), Applied Materials (AMAT), Lam Research (LRCX), and Align Technology (ALGN). In terms of sector representation, investors still can’t get enough of tech stocks as 13 of the 28 names come from that sector. The sector with the next most names is Energy (5). Meanwhile, not a single stock from the Financials, Real Estate, Telecom Services, or Utilities sector made the list.

As mentioned above, just under 100 stocks in the Russell 1000 have declined relative to their 2/8 closing levels, and below we highlight the 23 stocks that have dropped more than 5% during this time. Leading the way lower, Macquarie Infrastructure (MIC) has lost nearly one-third of its value, followed by Brookdale Senior Living (BKD), which has declined 27.4%. Besides these two names, other notable losers include Walmart (WMT) and Biogen (BIIB), which have both dropped nearly 7%. Regarding sector representation, this list is a little more even as no sector represented has more than six names (Consumer Discretionary), while just two stocks from the Technology sector are down more than 5%.

Chart of the Day: Margin Debt Mediocrity

Stock Seasonality: 2/26/18

While we don’t ever suggest that investors should base their trading solely on the calendar, there is evidence that the market and many stocks do indeed follow seasonal patterns. This makes our S&P 500 Stock Seasonality report a useful addition to every investor’s toolbox. Using the last ten years worth of price data, our Stock Seasonality report looks at the average returns for the S&P 500, its eleven sectors, and its 500 individual stocks. In the report, we highlight the five stocks in each sector that have historically been the best and worst performers over the next two weeks. For each stock, we also include information such as average returns, the percent of time each stock or sector is positive/outperforms the S&P 500, and its historical performance over the next two weeks for each of the last ten years. The Stock Seasonality report is published on a weekly basis on Mondays, and it is available to all Bespoke Premium and Bespoke Institutional subscribers.

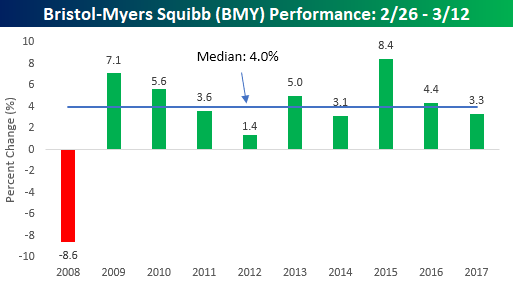

This week’s stock that we have chosen to highlight is Bristol-Myers Squibb (BMY). BMY typically doesn’t trade in as wide a range as other stocks in the market, but in the upcoming two-week period it has been remarkably consistent. BMY hasn’t traded down during the upcoming two-week period since 2008. Overall, the stock’s median gain during this period is a gain of 4.0%.

For active traders, our Stock Seasonality report is an excellent tool to help keep track of the best and worst times of year for the overall market, sectors and individual stocks. To see the report, sign up for a monthly Bespoke Premium membership now!

Bespoke Brunch Reads: 2/25/18

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Financial Musings

Private Equity: Overvalued and Overrated? by Daniel Rasmussen (American Affairs)

A case is to be made that the combination of leverage-driven returns, little impact on operating efficiency, and extremely high fees coupled with illiquidity make private equity a wasted allocation. [Link]

The Pricing of FX Forward Contracts: Micro Evidence from Banks’ Dollar Hedging by Puriya Abbassi and Falk Bräuning (SSRN)

Using transaction-level data on FX forwards from 2014-2016 and balance sheet information, the authors find large differences in banks’ hedging costs. The differences are driven by differences in FX funding gaps, the composition of FX funding, and the cost of capital. All-told the result is a direct path for international transmission of shocks to markets. [Link]

Infamous Investors

Berkshire Hathaway Inc. Annual Letter by Warren Buffett (Berkshire Hathaway)

The annual report on how things were for the large conglomerate over the past 12 months. [Link; 16 page PDF]

Risky Crypto Bet Dents Dennis Gartman’s Retirement Account by Lily Katz (Bloomberg)

Widely-followed newsletter author and speculator Dennis Gartman had some pretty terrible trades related to the blockchain play RIOT over the past week. [Link; auto-playing video]

Economics

Why has the US fallen behind the UK in labor force participation? by Ernie Tedeschi (Medium)

An excellent data-driven analysis of changes in the generally similar labor force dynamics in the US and the UK. When adjusting for demographics, health and disability, labor force discouragement, and family care for women are the biggest drivers of recent shifts. [Link]

The distribution of wages and wage inequality by Pedro Portugal, Pedro S. Raposo, and Hugo Reis (Banco de Portugal)

An investigation of why Portugal has seen large structural shifts in its labor market but relatively little change in income inequality over the past quarter century. [Link; 13 page PDF]

The Economy Is Getting Hotter. Is a Productivity Boom Next? by Neil Irwin (NYT)

A long rambling look at the relationship between tight labor markets and productivity, which may be a response to demand just as much as supply. [Link; soft paywall]

Chattanooga

US economy: The growth puzzle by Sam Fleming (FT)

A case-study in what may drive the next leg of productivity growth, through the lens of the East Tennessee industrial hub that’s been a huge success story. [Link; paywall]

The City That Was Saved by the Internet by Jason Koebler (Vice)

One of the reasons Chattanooga has been so successful is the bold steps the city took early on to make sure that businesses had adequate connectivity. [Link]

Olympics

In PyeongChang, maintaining Olympic venues relies on a poor and aging workforce by Chico Harlan and Yoonjung Seo (WaPo)

An army of senior citizens is keeping PyeongChang clean and comfortable during the games, a sign of the broken safety net and impoverished status of the country’s elders. [Link; soft paywall]

German Olympians Drink a Lot of (Nonalcoholic) Beer, and Win a Lot of Gold Medals by Ben Crair and Andrew Keh (NYT)

Gatorade’s got nothing on fizzy hops, which is the recovery drink of course in Germany…sans alcohol, for those at the highest level of competition. [Link; soft paywall]

Surveying Society

He Predicted The 2016 Fake News Crisis. Now He’s Worried About An Information Apocalypse. by Charlie Warzel (BuzzFeed)

A survey of the media landscape with deteriorating trust, fracturing viewership, and vulnerable interpretation that has caused so much trouble over the last few years. [Link]

The Poison We Pick by Andrew Sullivan (NYMag)

One explanation for the surging use of opioids – especially in relatively vulnerable or economically depressed areas – is the simple truth that our society is a miserable place to live for many people. [Link]

It’s Time to End ‘Trending’ by Brian Feldman (NYMag)

The concept of “trending” is one that propagates mistruths, creates online mobs, and aids in the spread of disinformation, with no clear upsides. [Link]

Silicon Valley parents are raising their kids tech-free — and it should be a red flag by Chris Weller (Business Insider)

Many of the people who fuel the tech world’s increasing dissemination of screens into our lives are cautious about allowing their own children access to the same technology. [Link]

Celebrity

What Ever Happened To Brendan Fraser? by Zach Baron (GQ)

An emotional read on what drove one of Hollywood’s leading men out of the limelight, despite box office appeal, marketability, and acting chops. [Link]

In One Tweet, Kylie Jenner Wiped Out $1.3 Billion of Snap’s Market Value by Justina Vasquez (Bloomberg)

A tweet by famed Kardashian family member Kylie Jenner resulted in tumbling shares of Snap, which has been struggling since a redesign and is having a hard time competing with Facebook’s Instagram. [Link]

Consequences

In Vaccines we Trust? The Effects of Anti-vaccine Propaganda on Immunization: Evidence from Pakistan by Monica Martinez-Bravo and Andreas Stegmann (CEMFI)

After the Pakistani public learned a fake vaccination campaign had been used to identify Osama bin Laden’s hideout (ultimately leading to his killing by the US military), vaccination rates plunged in areas that had higher levels of support for Islamist groups. [Link; 44 page PDF]

Read Bespoke’s most actionable market research by starting a two-week free trial today! Get started here.

Have a great Sunday!