B.I.G. Tips – Stock Market Confidence Crashes

Chart of the Day: Dollar No Concern For Macy’s

B.I.G. Tips – CAT March Slows

Bespoke Stock Scores — 4/24/18

US Index ETFs in a Neutral State of Mind

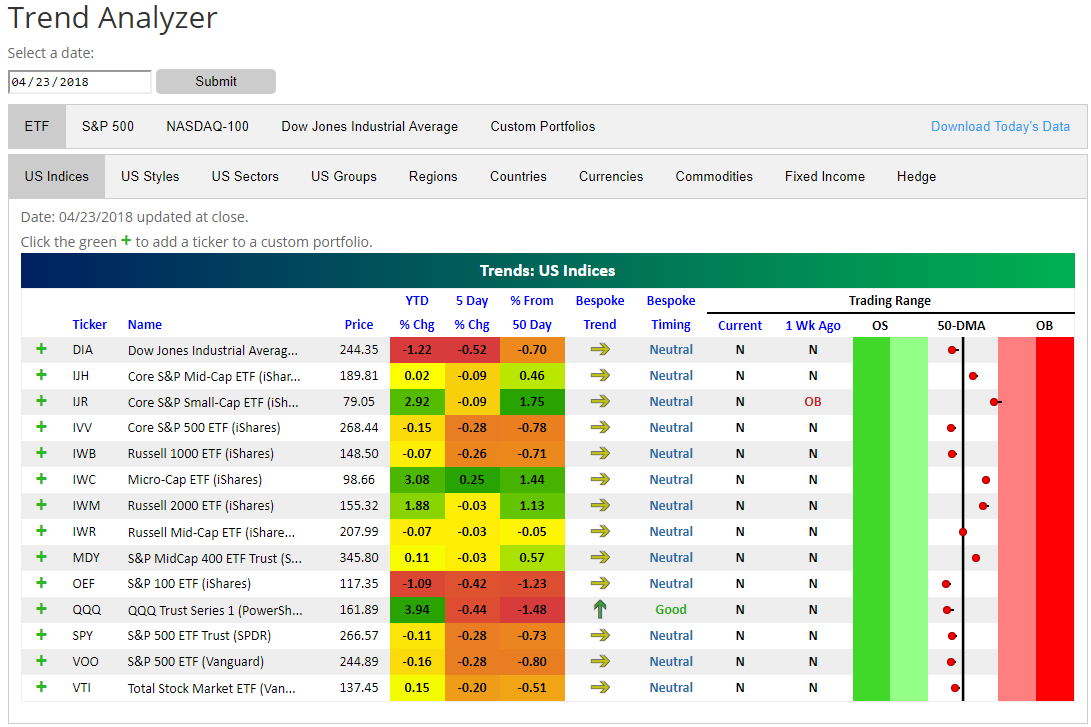

In browsing through our Trend Analyzer tool as we do each day, we noticed that US index ETFs are in a surprisingly neutral state of mind. After all of the volatility over the past few months, every single one of the index ETFs that we track in our Trend Analyzer are trading in neutral territory, which means they’re all within one standard deviation above or below their 50-day moving averages.

You can see the index ETFs in the snapshot of our Trend Analyzer below. (You can view it for yourself at our Trend Analyzer tool as well.) In the “trading range” section on the right side of the tool, the dots represent where the different ETFs are currently trading relative to their 50-day moving averages. As shown, none of the ETFs are trading in overbought or oversold territory, and last week at this time, only one ETF was in overbought territory.

At this point, the large-cap index ETFs are below their 50-day moving averages, while the mid-cap and small-cap ETFs are mostly above their 50-DMAs.

Proceed to our Trend Analyzer now for a further explanation of the tool and how we like to use it. The “US Indices” tab is available to the public, but to access the rest of the tool and set up custom portfolios, you’ll need to start a two-week free trial to Bespoke Premium.

The Closer — Expensive Earnings Yield, US Data Round Up, FX Stories — 4/23/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at new US Census estimates for the growth of the population. We also update our tracking of Canadian monthly GDP and recap some minor data releases from the US today: the Chicago Fed’s National Activity Index, Markit’s flash Manufacturing PMI, and existing home sales.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Dollar Spikes

Looking for Action? S&P 1500 Most Volatile Stocks

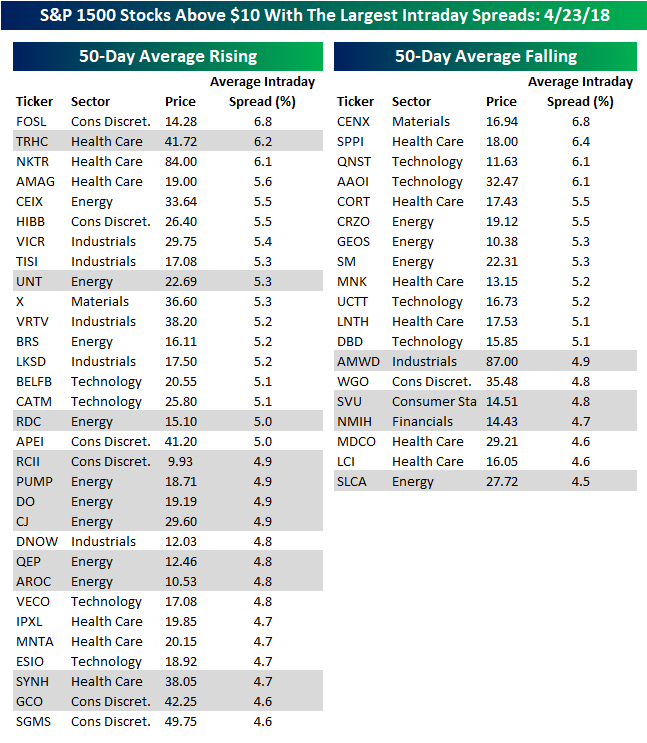

For traders with a short-term time horizon looking for big moves, we have updated our list of the S&P 1500 stocks trading above $10 that have the largest intraday high-low ranges (based on the average percent spread between the intraday high and low over the last 50 days). The stocks are grouped based on whether they have a rising or falling 50-day moving average (DMA), and 15 names highlighted in gray are new to the list this month.

In terms of sector representation, stocks on the list come from eight of the eleven S&P sectors. The only three sectors not represented are Real Estate, Telecom Services, and Utilities. Of the sectors on the list, Energy (13) and Health Care (12) take up the lion’s share of names listed with a total of 25.

As far as individual stocks are concerned, the highest priced stock on the list is American Woodmark (AMWD), which is trading at $87. With an average daily range of 4.9%, the stock typically sees an intraday swing of over $4 per share. While AMWD trades in the $80s, most of the stocks on our list are much lower priced. In fact, the average price of the 25 stocks listed is just slightly more than $25 per share.

Over time, the longer the market continues to trade in a sideways range as it has for the last several weeks, the more balanced the list of stocks in uptrends and downtrends will become. As it stands now, though, the number of stocks in uptrends (rising 50-DMA) outnumbers the number in downtrends (falling 50-DMA) by a comfortable margin of 31-19.

Bottom Line Beat Rates Strong, But Top Line A Different Story

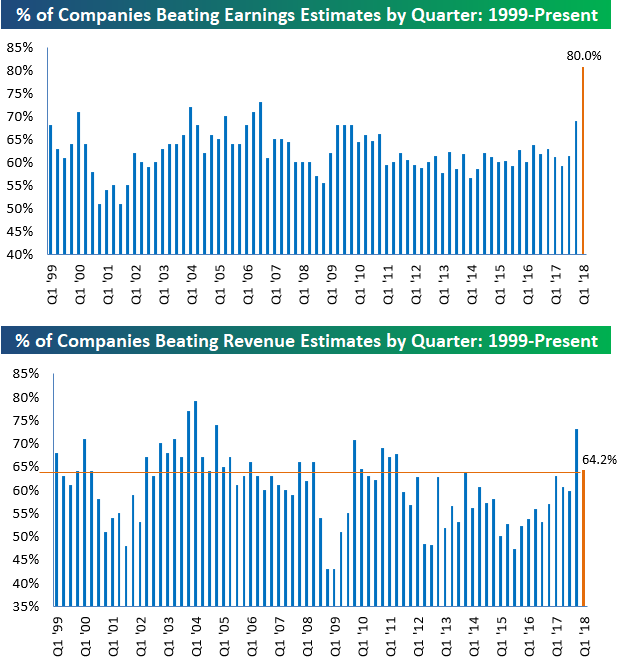

In last Friday’s Bespoke Report newsletter, we provided our first rundown of this season’s earnings results. While only 10-15% of companies have reported so far, it’s still enough to give us an early read on how companies performed in Q1. Below are two charts we thought we’d share more broadly with Think B.I.G. readers. In the first chart, we show the percentage of companies that have beaten consensus analyst EPS estimates on a quarterly basis going back to 1999. So far this season, 80% of companies that have reported have beaten EPS estimates. If that reading were to stand — and note that we don’t expect it to stand — it would be the strongest earnings beat rate seen in at least 19 years. Needless to say, companies have been beating EPS estimates at a historic clip so far this season.

In the second chart below, we show the percentage of companies that have exceeded consensus top-line revenue estimates on a quarterly basis. In terms of revenues, the beat rate looks much different this season compared to earnings. Only 64.2% of companies have beaten revenue estimates, which is nearly 16 percentage points below the EPS beat rate. If we had to choose, we’d prefer the top-line beat rate to be stronger than the bottom-line beat rate, because sales are harder for companies to manipulate. Last earnings season we actually saw a stronger revenue beat rate than earnings beat rate, but the opposite has been the case so far this season.

Start a two-week free trial to Bespoke Premium for access to all of our in-depth earnings season analysis.

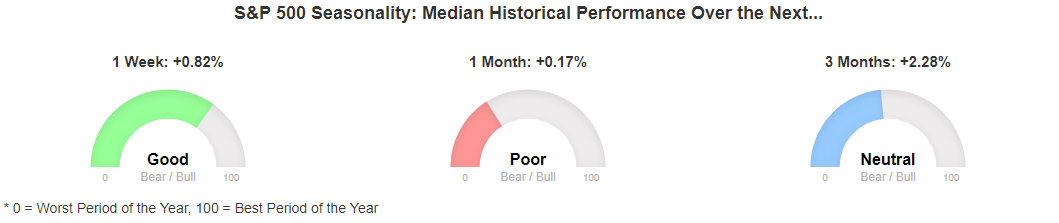

Something for Everyone in Upcoming Seasonal Trends

Our interactive Stock Seasonality Tool (available to Bespoke Premium and Bespoke Institutional members) allows investors to quickly analyze and track seasonal tendencies for any asset class. It’s an incredibly useful tool that we added for clients earlier this year. Looking at the Seasonality Tool earlier today, we noticed that depending on your time frame, there’s a little something for everyone.

The graphic below shows the S&P 500’s median one-week, one-month, and three-month returns (from today’s closing level) based on the last ten years of data. In the short term, the S&P 500’s median performance in the one-week period from the close on 4/23 through month end has been an impressive +0.82%, which is better than average compared to other one-week periods over the last ten years. While median returns in the very short-term have been good, the S&P 500’s median one-month return from the close on 4/23 has been a paltry 0.17%, which ranks as poor relative to all other one-month periods over the last ten years. Finally, looking out over the next three months, the S&P 500 has seen a median gain of 2.28%. That sounds respectable enough, but when you consider the fact that most of that time has been during a bull market, 2.28% only ranks as neutral relative to median three-month returns for all other periods throughout the year.

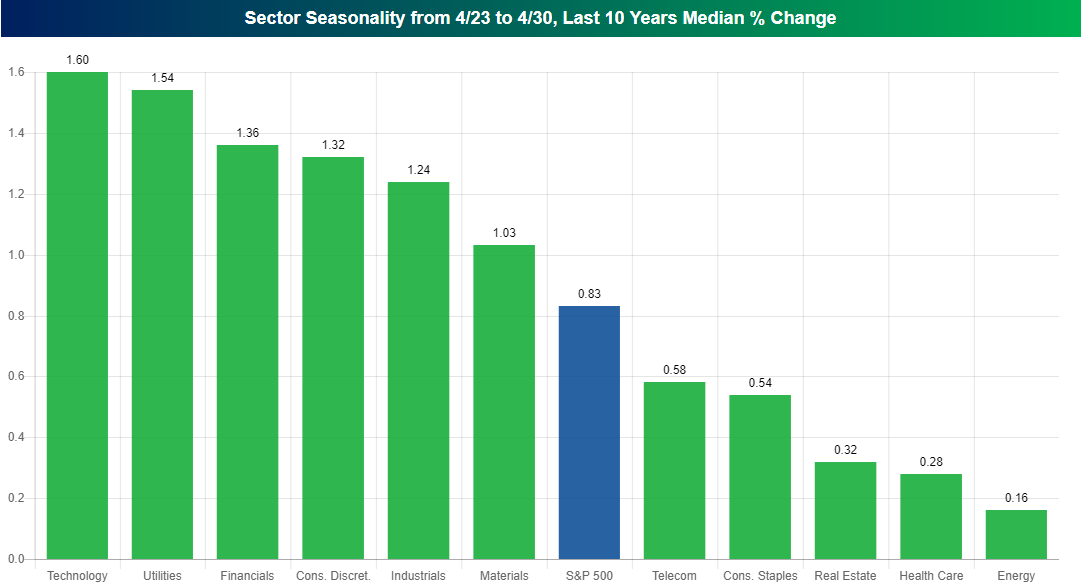

Looking more closely at just the next week, the chart below is also from our Stock Seasonality Tool, and it shows the median performance of S&P 500 sectors over the upcoming week. Leading the way higher, Technology has historically seen a median gain of 1.6% during the last week of April, but another five sectors (Utilities, Financials, Cons Discretionary, Industrials, and Materials) have seen median gains of more than 1%. While no sectors have seen declines on a median basis, Energy (+0.16%) and Health Care (+0.28%) have been the biggest laggards.

Again, both the chart below and the graphic above our from our Stock Seasonality Tool (available to Bespoke Premium and Bespoke Institutional members) and can be customized by time frame as well as different market cap sizes, asset classes, etc. Not only that, but you can also track seasonal trends for the stocks or ETFs in any custom portfolios you have created. Give it a try!