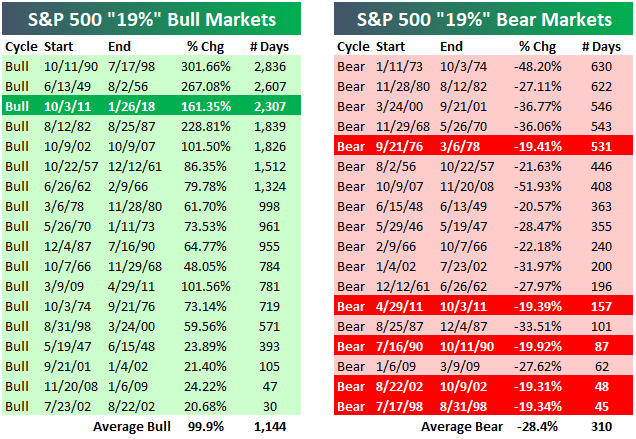

Historical Bull and Bear Markets of the S&P 500

There’s been plenty of chatter lately about the current bull market becoming the “longest on record.” Below is an updated look at the length of the current bull market compared to past bull markets for the S&P 500.

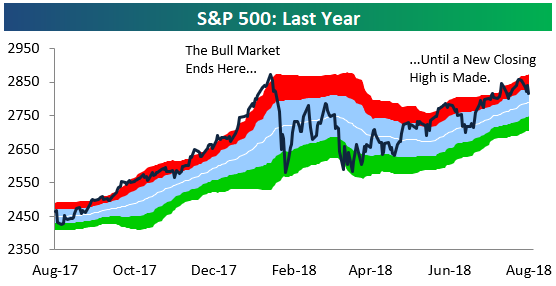

First things first, though. Until the S&P 500 closes at a new high, January 26th, 2018 represents the end point of the current bull market because that’s the date of the S&P’s highest closing point of the bull market. Thus, the length of the current bull market has been stopped at 3,245 days since January 26th (3/9/09-1/26/18). A bull market is most commonly defined as a 20%+ rally that was preceded by a 20%+ decline. If the S&P never closes above its January 26th closing level, and instead it goes on to fall 20% from that level, a new bear market will have begun with a start date of January 26th, 2018. Since we don’t know whether the S&P will go into a new bear market before it closes above its 1/26 high, or vice versa, we can’t extend the length of the current bull market past the 1/26 high point.

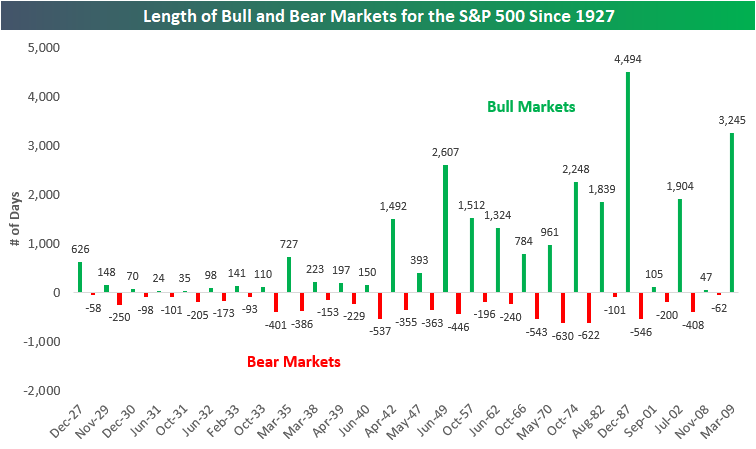

Based on the most commonly used definition of bull and bear markets (20% rallies and declines using closing prices), below is a chart showing the length (in calendar days) of bull and bear markets for the S&P 500 since 1927. We’ve shaded bull markets in green and made them positive, while we’ve shaded bear markets in red and made them negative.

The current bull market that has lasted 3,245 days is the second longest on record behind the 4,494-day bull market that ran from late 1987 through early 2000. Yes, the S&P 500 went from late 1987 to early 2000 without experiencing a single decline of 20% or more on a closing basis.

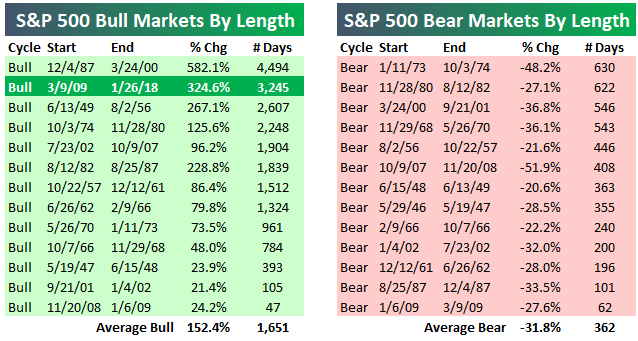

If the S&P 500 went on to make a new closing high today, the current bull market would be at 3,447 days, which would still be more than 1,000 days less than the longest bull market on record. For the current bull to become the longest on record, the S&P 500 would need to move above its 1/26 closing high and then not experience a 20% decline from an all-time high through June 29th, 2021.

Two things stand out the most in the chart below. The first is that bull markets last a lot longer than bear markets. Indeed, the average bull market since 1927 has lasted 981 calendar days, while the average bear market has lasted 296 days. The second is that US bull/bear market cycles became much longer lasting post-WW2.

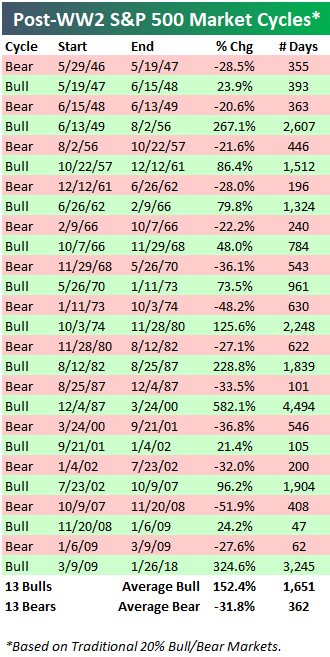

Below is a table showing the 13 post-WW2 market cycles for the S&P 500. The average bull market since WW2 has lasted 1,651 days and seen a gain of 152.4%. The average bear market has lasted 362 days and seen a decline of 31.8%. The current bull market’s gain of 324.6% over 3,245 days is more than double the length and strength of the average bull market.

There is always a lot of debate about the 20% rally/decline definition of a bull market. That’s because there have been multiple 19%+ declines from a closing high that just didn’t quite make it to the 20% threshold for a new bear market. Shouldn’t the 19.92% decline back in 1990 be considered a bear market since the index was just 0.08% away from the 20% threshold? Or shouldn’t the 19.39% decline seen in 2011 be considered a bear as well?

We try to be as consistent as possible with the data, so we’re always going to use some type of percentage threshold to measure bull and bear markets over time instead of trying to be subjective about them. And we would never try to say that one 19%+ decline should be considered a bear market while another 19%+ decline shouldn’t be. So for those that would rather use a 19% threshold for market cycles instead of the standard 20% threshold, below we offer a side-by-side comparison of the two.

As you can see, the 19%+ threshold ends up adding 5 more bull and bear markets to the tally in the post-WW2 era.

As mentioned earlier, the current bull market is the 2nd longest on record using the standard 20% threshold for bull and bear markets.

If we use the 19% threshold, the current bull would rank as the third longest on record instead of the second longest.

At Bespoke, we’ll likely always use the 20% rally/decline threshold as our definition for bull and bear markets. For investors out there that prefer to be subjective about it or include some 19% declines, that’s fine too!

In regards to the current bull market, even if you include the 19% selloff in 2011 as its own bear market, the bottom line is that this bull has still been a really long one.

There are two things to remember, though, for the time being. 1) As mentioned above, the current bull is actually not aging at this point until it takes out its January 26th high. And 2) — more importantly — bull markets don’t die of old age.

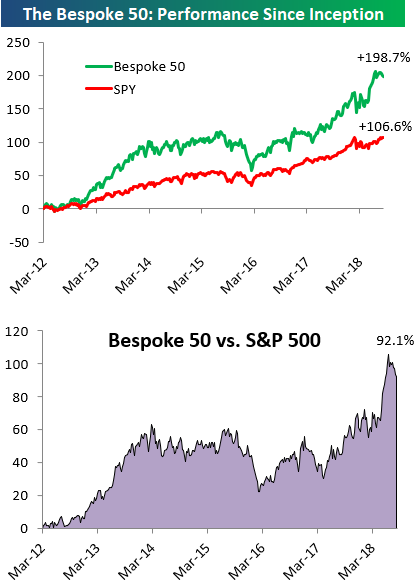

the Bespoke 50 — 8/16/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 92.1 percentage points. Through today, the “Bespoke 50” is up 198.7% since inception versus the S&P 500’s gain of 106.6%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

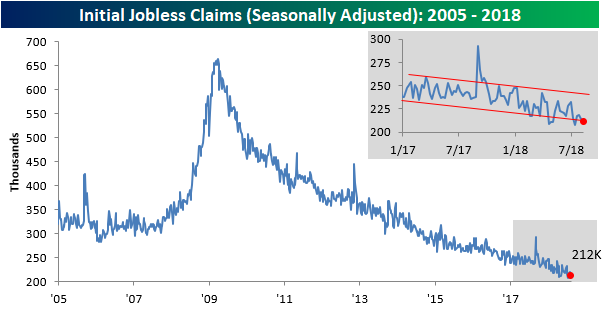

Death, Taxes, and Strong Jobless Claims Reports

Yeah, jobless claims are starting to get that dependable in terms of delivering a strong weekly print. This week’s report was no different as first-time claims came in at 212K versus estimates of 215K. So now it’s time to update the streaks. This week’s report was the record 180th straight week of sub-300K claims, the 45th straight week where claims were at or below 250K (longest streak since 1970), and the 6th straight week that claims were at or below 220K (longest streak since 1969).

Despite the decline in claims this week, the four-week moving average increased to 215.5K, which is 2K above the multi-decade low of 213.5K from mid-May. Unless we get a print below 209K next week, the May low will hold for at least another week.

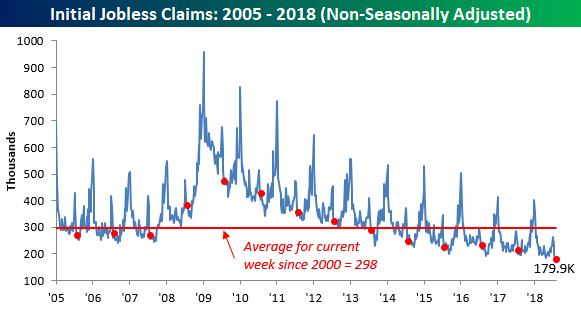

Finally, on a non-seasonally adjusted (NSA) basis, jobless claims dropped to 179.9K. For the current week of the year, this is the lowest reading on record and nearly 120K below the average of 298K dating back to 2000.

Fixed Income Weekly – 8/16/18

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

We take a look at differences between investment grade and high yield credit risk metrics.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Chart of the Day: “The Yield Curve Doesn’t Matter”

The Closer — Staples Breaking Out, Data Deluge, Oil Swoons — 8/15/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at the strong relative performance and breakouts of the Consumer Staples sector versus other sectors and the broad S&P 500. We also review today’s data: industrial production, productivity, and EIA data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

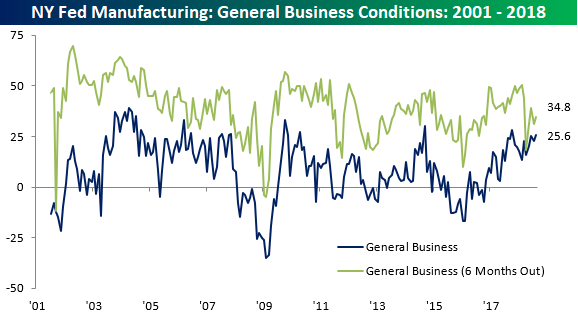

Empire Manufacturing Rebounds

Manufacturing activity in the New York region heated up right with the temperature in August as the Empire Manufacturing survey unexpectedly rose to 25.6 versus estimates for a reading of 20. As shown below, the tracker for General Business conditions hit its highest level since last October. Expectations, however, remain a bit more subdued. While the index for Business Conditions six months from now increased on a m/m basis, it remains well off of its recent highs.

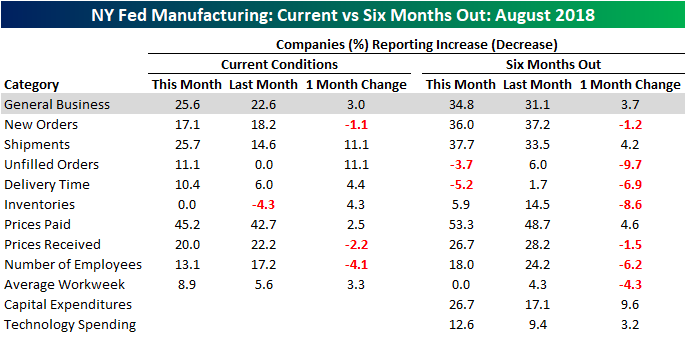

The table below breaks out this month’s report by each of its subcomponents for both current conditions and expectations. Here again, we can see that manufacturers are a lot more optimistic about the present than the future. Of the nine components in the Current Conditions category, just three declined, and none of the drops were exceptionally large. On the upside, Shipments and Unfilled Orders both saw large increases, while Prices Paid saw just a modest increase (Prices Received actually declined).

Looking out over the next six months, most components actually saw declines as Shipments, Prices Paid, Cap Ex, and Tech Spending were the only categories that increased relative to July’s readings.

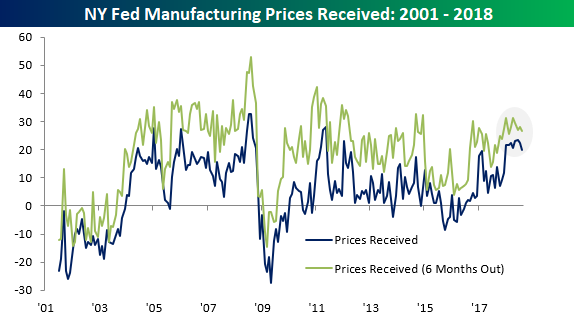

Obviously, inflation readings have become increasingly scrutinized by the market lately, so it’s encouraging to those fearful of inflation accelerating that the recent moves in both Prices Paid and Prices Received haven’t been as one-directional to the upside. In the case of both Prices Paid and Prices Received, the indices for both Current Conditions and Expectations have stalled out in the last few months. While it could be nothing more than a breather, recent declines in commodity prices should help to keep some level of gravity on prices.

Ta-Rough

You can say whatever you want about tariffs and the pros and cons on both sides of the argument, but with respect to the metals and mining companies, keep your ‘pros’ to yourself. The group has been stuck in a downtrend ever since the topic of tariffs first came up, and it’s now basically in full flush mode.

The table below lists the individual components of the group and how they’ve performed over the last six months, a period which roughly coincides with when the Administration brought up the topic of taxing steel imports in early March. During this period, just two out of the twenty members of the group have traded up, and the best of them just happens to be a member of our Model Growth Portfolio! The remaining 18 members of the group are not only down, but they are down big. Eleven of them are down over 10%, and five of those are down over 20%, including Century Aluminum which has been cut in half!

Chart of the Day: Opportunity With Energy Extremely Oversold

B.I.G. Tips – Bricks and Mortar Not Going Down Without a Fight

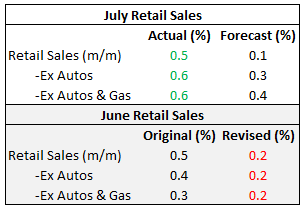

When it comes to the July Retail Sales report, it has historically been one of the better ones relative to expectations. This year was no exception as we saw a strong beat relative to expectations not only on the top line but also when you strip out the impact of Autos and Gas. While July’s data was strong, though, it comes off a lower base as June’s originally reported strong numbers were all revised lower. After taking both the downside revision and July’s strength into account, it ends up being slightly more positive than a wash.

In terms of breadth, the results of this month’s report were positive again with nine components increasing and just four declining. Both the Clothing and Bars and Restaurants sectors showed m/m growth of 1%+. Sporting goods was the only decliner of more than 1%.

Online sales are a category that has been eating the lunch of traditional brick and mortar retail for some time, but in this month’s report, there were some signs starting to emerge that traditional retail isn’t going down without a fight. Even as the above table illustrates, other sectors of the economy showed much more growth than Non-Store retailers this month. In our latest B.I.G. Tips report, we covered all of the major trends surrounding this month’s retail sales report as well as some longer-term trends that may be starting to shift a bit towards the favor of traditional retailers.

This one is a must-read. To see it, sign up for a Bespoke Premium membership now!