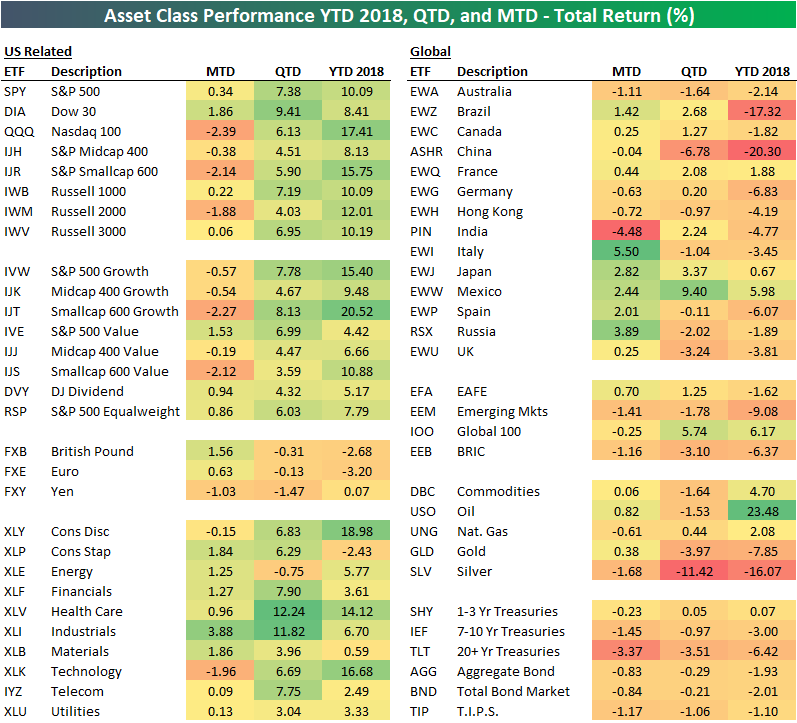

Asset Class Performance MTD, QTD, and YTD 2018

Below is an updated look at the performance of various asset classes using key ETFs tracked in our Trend Analyzer tool. For each ETF, we show its total return month-to-date, quarter-to-date, and year-to-date.

While September has been an up month so far for the S&P 500 (SPY), we’ve seen some rotation out of the strategies that were working in 2018 prior to the start of the month. You’ll notice that areas like the Nasdaq 100, the Technology and Consumer Discretionary sectors, and small-caps are all down in September, but they’re also the areas that are still up the most year-to-date. Conversely, the Dow 30 (DIA) has been the weakest of the three big US indices (Dow, S&P 500, and Nasdaq 100) in 2018, but it’s doing the best of the three in September.

Outside of the US, we’ve seen big moves higher for Italy (EWI), Japan (EWJ), Mexico (EWW), Spain (EWP), and Russia (RSX), while India (PIN) and Australia (EWA) have both fallen. Brazil (EWZ) and China (ASHR) remain as the worst international performers on a year-to-date basis.

The commodities ETF (DBC) is pretty much flat on the month along with oil (USO) and gold (GLD), while Treasury ETFs are down across the board. The 20+ Year Treasury ETF (TLT) has been one of the worst performing asset classes in September with a drop of 3.37%.

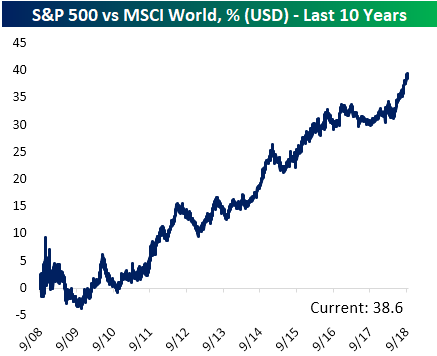

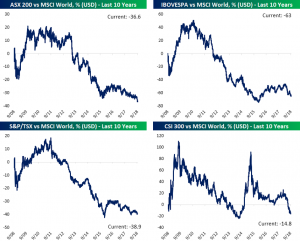

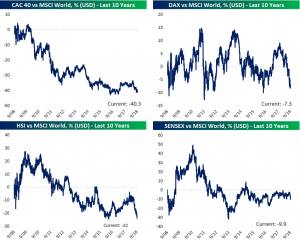

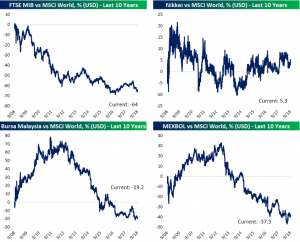

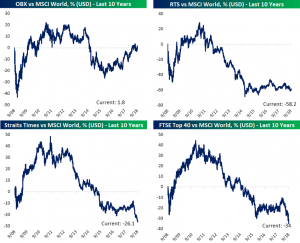

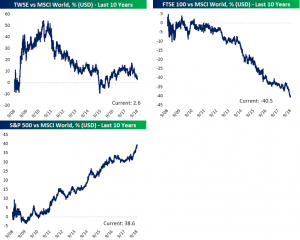

US vs. Rest of World: Relative Strength Charts

Our weekly Global Macro Dashboard is a useful tool for macro or international investors looking for regional and/or country coverage. You can read more about the report here if you’d like to take a look.

In the report, we provide 10-year relative strength charts of each country’s stock market versus the MSCI World index. This tells you how well each individual country’s stock market is performing versus the rest of the world.

US outperformance versus the rest of the world has been a major theme of 2018, and our country relative strength charts do a great job of highlighting this theme.

First, take a look below at the relative strength chart of the US (S&P 500) versus the MSCI World index. The US has been outperforming international equities for the entire bull market, but it has really ramped up its outperformance over the last few months.

Of the 22 additional countries that we feature in our Global Macro Dashboard, you won’t find another relative strength chart that looks even remotely similar to the US. Nearly every country continues to see its relative performance versus the MSCI World index trend lower and lower. The US continues to be the place to be when it comes to stocks.

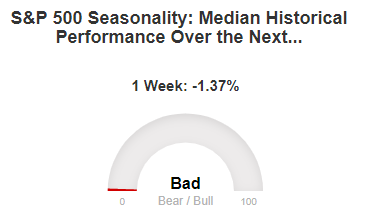

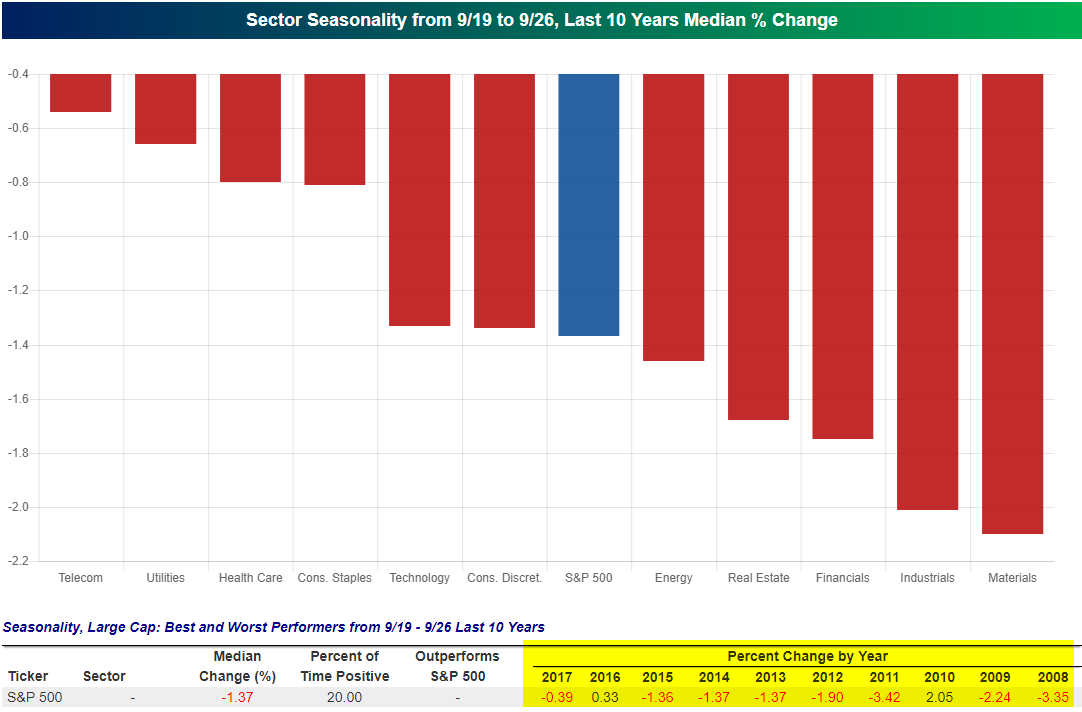

The Worst Week of the Year

Our Stock Seasonality tool (available to Bespoke Premium and Bespoke Institutional members) lets users see how various indices, sectors, stocks, and ETFs typically trade throughout the calendar year. When the tool is opened, it automatically populates the S&P 500’s median change over the next week, month, and three months.

When we opened up the Stock Seasonality tool today, we were greeted with the gauge below showing absolutely brutal seasonal trends for the next trading week. Indeed, from September 19th through September 26th over the last 10 years, the S&P 500 has seen a median decline of 1.37%. As the gauge shows, that’s as bad as it gets compared to all other one-week periods throughout the year.

Below is another snapshot that you’ll find when opening our Stock Seasonality tool that shows median sector performance over the next trading week. Over the last ten years, every S&P 500 sector has seen a median decline, with Materials and Industrials falling the most at more than 2%.

For the S&P 500 as a whole, the index has only gained from 9/19 to 9/26 twice over the last ten years (2016, 2010), which is pretty bearish considering the index has been in a raging bull market since 2009.

Start a two-week free trial to Bespoke Premium to try out our Stock Seasonality tool today!

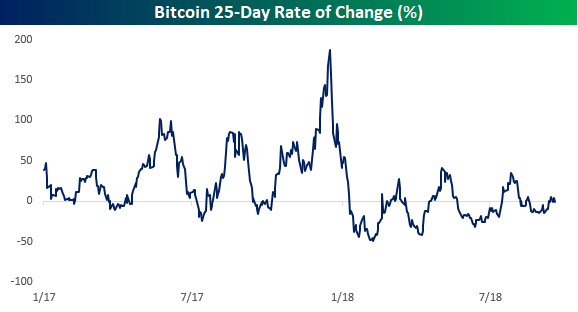

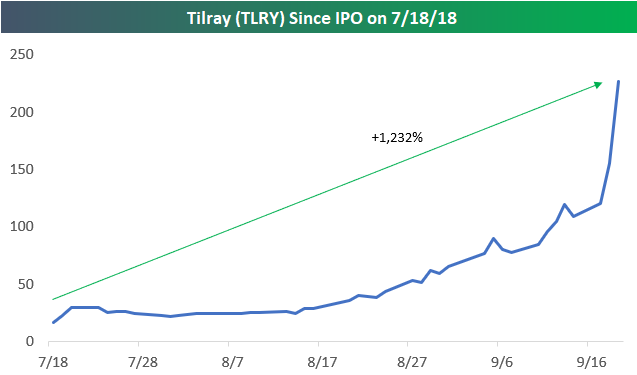

Bitcoin, Meet Tilray (TLRY)

As mentioned in a post earlier, shares of cannabis drug maker Tilray (TLRY) have gone absolutely bananas in the short time it has been public. In the 47 trading days since its IPO, the stock is already up over 1,200%. In order to help put the stock’s surge in perspective, we wanted to compare its recent performance to the performance of bitcoin during its monster surge in 2017. For starters, consider this: during all of 2017, bitcoin rallied just over 1,400%. TLRY has done nearly that in two months!

The chart below shows the 25-trading day rolling performance of bitcoin throughout 2017 and into 2018. For practically all of 2017, bitcoin’s rolling return remained positive and when it went into negative territory, it rarely dipped very low or stayed there long. On the upside, though, there were multiple periods where the rolling 25-day return topped 100%, and at the height of the mania in late 2017, bitcoin actually rallied close to 200% in just five weeks! Pretty impressive, right?

The chart below is the same one as above, except we have adjusted the y-axis to include the level that corresponds to TLRY’s current five-week return of +691%. Suddenly, bitcoin’s move doesn’t look quite as impressive, does it? In fact, at the peak of the bitcoin mania in 2017, its trailing 25-day return peaked out at 187%. That’s less than a third of TLRY’s gain over the last five weeks. Granted, bitcoin managed to post strong returns for a much longer period than TLRY has so far. In terms of the magnitude of short-term moves, however, bitcoin doesn’t hold a candle to TLRY.

Tilray (TLRY): Canadian Blue Chip?

Canadian-based Tilray (TLRY) is up 1,232% since it IPOd two months ago on July 18th.

Wait, say that again!? Yes, TLRY is up more than 1,200% since going public just two months ago!

What does TLRY do? It’s a cannabis drug-maker, of course.

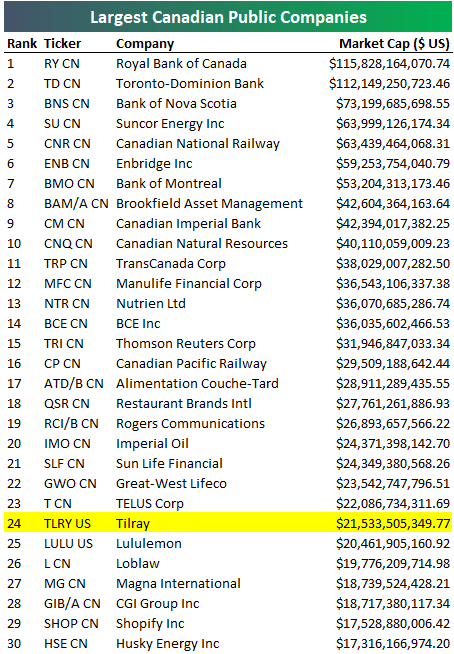

As the cannabis wave has swelled, Tilray’s massive gain over the last two months has left it with a market cap of $21.5 billion (USD). As shown below, this ranks Tilray as the 24th largest publicly traded company based in Canada. At $21.5 billion, TLRY’s market cap is now a billion dollars larger than lululemon (LULU), which is one of the most well known consumer brands based on Canada.

We have no comment on how or when this insane rally will end, except we’re confident that plenty of investors will end up losing their shirts.

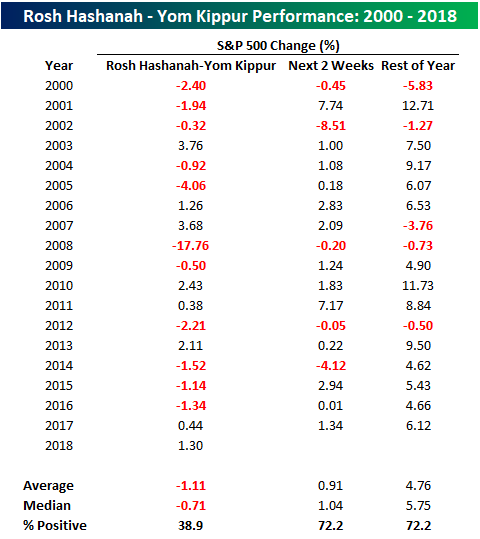

Another Seasonal Trend Fails to Deliver

We pay close attention to historical trends in the market and believe that investors should be aware of them, and in certain cases incorporate them into their process, but we have also always contended that investing based solely on the calendar is not the wisest of investment strategies. This year has been a perfect example. Sell in May and go away? Nope. September swoon? Not quite. The latest seasonal trend not to work this year is the somewhat less well-known, sell Rosh Hashanah, buy Yom Kippur.

In recent history, this seasonal trend based on the holidays of the Jewish New Year and Day of Atonement has actually been pretty consistent. Going back to 2000, the S&P 500 has seen an average decline of 1.11% (median: -0.71%) during the ten-day period with positive returns less than 40% of the time (see table below). What’s more, being out of the market during this period also would have avoided the nearly 18% decline that took place during the Financial Crisis in 2008. While there are a number of theories as to why this trend has worked over time, the most likely probably has to do with the fact that the period always occurs somewhere between early September and early October which has historically been one of the worst times of the year for equities.

While it has worked relatively well in the past, in 2018, the sell Rosh Hashanah, buy Yom Kippur trade hasn’t worked out for anyone following it. Through early afternoon Wednesday (Yom Kippur ends today), the S&P 500 is up 1.3% since the start of Rosh Hashanah, which is its best showing during this period since 2013.

While the period between Rosh Hashanah and Yom Kippur has historically been weak for equities, the two weeks after Yom Kippur have been very positive. Since 2000, the S&P 500 has averaged a gain of 0.91% (median: 1.04%) with positive returns nearly three-quarters of the time. For the remainder of the year, the results are similarly as strong with an average gain of 4.76% (median: 5.75%).

With the S&P 500 bucking the typical trend over the last week and a half, does that mean we can expect the market to do the opposite going forward? It’s possible, but prior history doesn’t suggest it. In fact, in prior years where the S&P 500 traded up during this period, it saw even stronger returns going forward. In the seven years where the S&P 500 was up from Rosh Hashanah through Yom Kippur, it traded up an average of 2.35% (median: 1.83%) in the following two weeks with positive returns all seven times. For the remainder of the year, the S&P 500’s average gain was 6.64% (median: 7.50%) with gains in all but one period (2007).

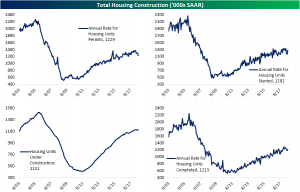

Residential Construction

This morning’s release of US Census residential construction numbers for August came in mixed. Total housing starts reported a 9.2% MoM increase at a seasonally-adjusted annualized rate of 1.282 million, beating the estimate of 1.238 million. Permits, on the other hand, came in far worse. Estimates were for a seasonally-adjusted annualized rate of 1.31 million, but the actual level came in lower at only 1.229 million, a 5.68% MoM decrease. Units under construction and completed both saw month-over-month increases of 0.8% and 2.54%, respectively.

While starts did come in higher overall, a large portion of the gain can be attributed to growth in the West, up double digits for both single and multifamily homes on a MoM basis. That follows an extremely low starts rate in recent months relative to recent permit activity. Conversely, the Northeast is the biggest laggard, especially when it comes to completions and permits. Single family permits, single family starts, total completions, and single family conversions are all down double-digits YoY. While starts, units under construction, and completions have generally been pretty strong around the country, permits have fallen off a cliff. In aggregate, permits are down 5.5% YoY with single family permits only barely clinging to YoY growth.

While the numbers from this report tend to fluctuate, the annual rate for total housing permits are at their lowest point since May 2017. Given that permits are generally more reliable than starts, that’s not a good sign, though it ought to be balanced against the fact that the number of units under construction is at a record level, suggesting that permits are slowing because of supply constraints rather than soft demand.

Fixed Income Weekly – 9/19/18

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

This week we take a look at the very strong trend in 2 year note yields, and the uptick in the 2s5s yield curve.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Chart of the Day: NOC-NOC-NOCing On Breakouts’ Door

Bespoke’s Global Macro Dashboard — 9/19/18

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!