Bespoke’s Global Macro Dashboard — 1/23/19

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Trend Analyzer – Pushed Back – 1/23/19

Equities have broadly been able to break above resistance at their 50-DMAs recently, but yesterday’s declines pushed the major index ETFs back downa bit. While each of these ETFs still sit above these levels, they currently have less wiggle room. With the exception of three of these names (IJH, IWM, and IWR), the index ETFs are less than a percentage point from falling back below their respective 50-DMAs. With equities poised to open higher this morning following some solid earnings from the likes of IBM, UTX, and PG, at least for the beginning of trading it looks like things will generally move in the more optimistic direction.

<script>(function($){$.get(‘/display_special.php?type=btn’, function(data) {$(‘.disp_special’).html(data);});})(jQuery);</script>

<div class=”disp_special”></div>

Morning Lineup – Picking Up Where Yesterday’s Close Left Off

Solid earnings news from companies like IBM, UTX, and PG are putting traders in a buying mood this morning sending futures up by about 0.40%. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and commentary.

Bespoke Morning Lineup – 1/23/19

Even after yesterday’s last hour rally of 0.60%, the S&P 500 still managed to finish down over 1% on the day. What makes yesterday’s decline unique, though, is that it came as volume was below average. In other words, there was hardly a rush for the exits. For example, volume in SPY was 13% below its 50-day average, coming in at under 110 million shares. The last time the S&P 500 was down 1%+ and volume was more than 10% below average was almost a year ago in late February 2018. Between then and now, there have been 28 other days where the S&P 500 was down over 1% where volume was higher relative to its 50-day average.

The chart below shows the performance of SPY over the last 15 years, and the red dots indicate each time where the S&P 500 dropped more than 1% on volume that was at least 10% below average. As shown, there haven’t been many of them in recent history. Before the last occurrence in February 2018, you have to go all the way back to early 2016 to find the next most recent occurrences. Before that, there were many occurrences during the financial crisis and the first several years of the bull market, but they were a lot more frequent as the market was rallying than they were during the downturn.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bulls Bailed Out Into the Close

After a great three-week run, US equities kicked off the week on a disappointing note Tuesday. After just barely closing above the 50-day moving average (DMA) last week, bulls were hoping the next milestone for the rally off the Christmas Eve lows would be the downtrend line from the September highs, but the market had other plans. After falling as much as 2% and back below the 50-DMA heading into the final hour of trading, the S&P 500 rallied 0.60% in the final 60 minutes of trading to finish the day down 1.4% but above the 50-DMA. After a strong run like the one we had over the past few weeks, at the very minimum, a pause was expected, and the fact that the S&P 500 was able to once again rally in the final hour of trading is something for the bulls to hang their hats on.

Besides the fact that the S&P 500 showed some life into the close, Tuesday’s sell-off came on extremely low volume which provides some consolation. Whereas market sell-offs are almost always accompanied by an uptick in volume, volume on Tuesday was notably below average. In fact, SPY volume was 13% below average coming in at under 110 million shares. For the sake of reference, the last time the S&P 500 was down 1%+ and volume was more than 10% below average was almost a year ago in late February 2018 and between then and now, there have been 28 other days where the S&P 500 was down over 1% where volume was higher relative to its 50-day average.

Chart of the Day: The Streak Ends At 8

B.I.G. Tips – 12 Month Periods Most Similar to the Last 12 Months

Bespoke Stock Scores — 1/22/19

This Week’s Economic Indicators – 1/22/19

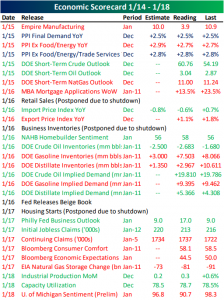

Economic indicators for last week were slightly disappointing as there were more misses than beats. There were no releases on Monday, but Tuesday kicked off with a weak reading from Empire Manufacturing which fell to 3.9 from 10.9. PPI inflation data also came out on Tuesday matching expectations. On Wednesday, the MBA’s mortgage applications came in lower than the prior week but still with a very strong reading. Applications rose 13.5% last week versus 23.5% the prior. Also in housing data on Wednesday was a strong print on homebuilder sentiment as mortgage rates declined in the past month. Import prices fell, albeit less than expected, while export prices came in lower than the previous month. Finally, the last of the major releases Wednesday was the Fed’s Beige Book which had some more pessimistic tones that indicates a slowdown as seen through our Beige Book index. On top of the usual weekly indicators released Thursday, the Philly Fed released their business outlook which saw a strong beat of forecasts and the prior period. On Friday, Industrial Production and Capacity Utilization both beat expectations on Friday, but Michigan Confidence missed by a very wide margin.

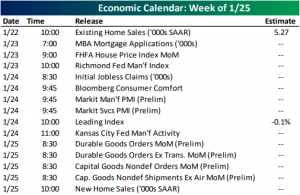

This week will be quieter with a shorter trading week after markets were closed yesterday in observance of MLK Jr. Day. As a result of the holiday, there were no releases yesterday. Today’s only release was existing home sales which were released earlier this morning and missed forecasts. Tomorrow, we will see yet another housing indicator with the FHFA’s House Price Index. The Richmond Fed’s Manufacturing Index will be released a little later on that morning. Thursday will be the busiest day of the week with preliminary Markit PMIs, the Kansas City Fed’s Manufacturing Index, and the Index of Leading Indicators—which is expected to show a slowdown in activity. We will round out the week with preliminary Durable Goods Orders and New Home Sales assuming the government reopens prior to the releases.

With the government still shut down, a few of the releases scheduled in the coming days are dependent on the Federal government reopening its doors. Last week further added to the growing list as Retail Sales Business Inventories, Treasury Flows, and both Housing Starts and Building Permits were all delayed. The table below shows all of the releases missed along with their originally intended release date. All of these releases are out of the Census and Treasury departments where funding has been curtailed. Meanwhile, the releases we have seen recently have come out of non-government agencies or departments that have still have funding secured for the time being.

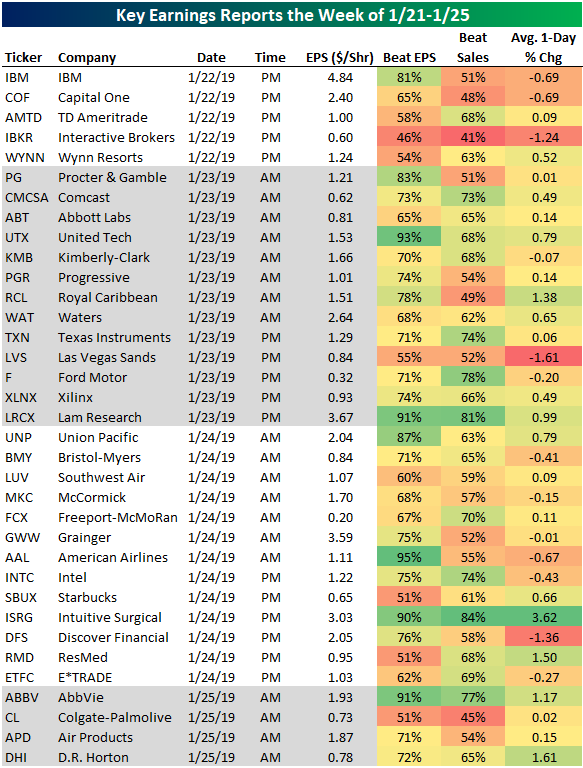

Key Earnings Reports This Week — IBM, WYNN, PG, UTX, LVS, TXN, INTC, SBUX, ISRG

Below is a table showing the key earnings reports we’ll be watching this week. IBM, Capital One (COF), and Wynn Resorts (WYNN) are three of the big reports tonight after the close, while we’ll hear from Procter & Gamble (PG), United Tech (UTX), Texas Instruments (TXN), and Ford Motor (F) on Wednesday. Intel (INTC) and Starbucks (SBUX) will be the most closely watched reports on Thursday, while Friday morning is relatively slow with Colgate-Palmolive (CL), AbbVie (ABBV), and D.R. Horton (DHI) on tap.

Of the stocks listed in the table, United Tech (UTX) and American Airlines (AAL) have the strongest earnings per share beat rates at 93%+. Intuitive Surgical (ISRG) has the strongest revenue beat rate at 84%, and ISRG has also historically responded the most positively to earnings with an average one-day change of +3.62% on its past reports. Las Vegas Sands (LVS) has the worst historical reaction to earnings with an average one-day decline of 1.61%. You can read more about the current earnings season in our most recent Bespoke Report newsletter, which is available with a two-week free trial to any membership level.

Morning Lineup – Sluggish Start

After an extended weekend, bulls are coming into the shortened trading week feeling a little sluggish as futures are indicating a moderately lower open. Weak data out of China, lower global growth forecasts from the IMF and a continued stalemate in DC are all factors contributing to the weakness. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and commentary.

Bespoke Morning Lineup – 1/22/19

The pace of earnings news is going to really pick up this week and one thing investors will be looking at closely is the revenue beat rate. It’s still early in the reporting period, but so far more than half of the companies reporting have missed estimates on their top line readings. If this pace doesn’t pick up in the weeks ahead, it could be a long February.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.