Ambarella (AMBA) Up 9% on Earnings Triple Play

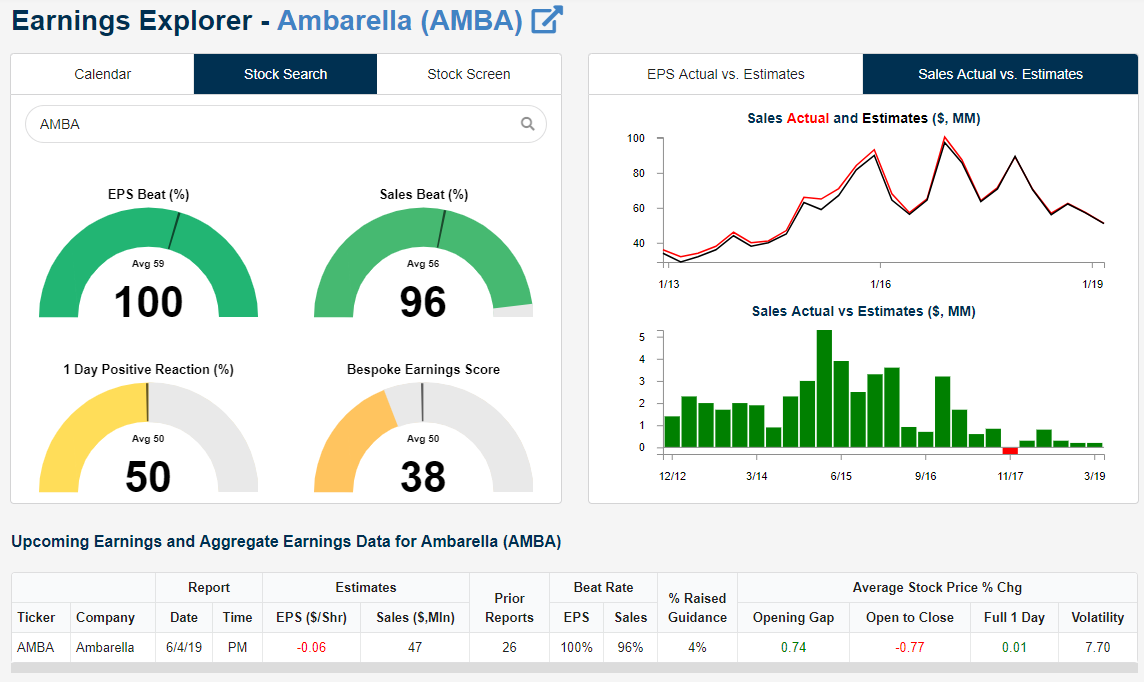

Chip-maker Ambarella (AMBA) is trading up 9% after reporting an earnings triple play after the close of trading last night. An earnings triple play occurs when a stock beats consensus EPS estimates, beats revenue estimates, and raises forward guidance. While EPS beat by 7 cents ($0.01 vs. -$0.07 est.), revenues managed to just barely beat by $180,000 ($47.2 million vs. $47.02 estimates). But…a beat is a beat.

Ambarella is certainly in the sweet spot of the semiconductor space it seems. The company was only founded 15 years ago in 2004, but its low-power/high def chips are key for tech products like video security, advanced driver assistance systems, fully autonomous driving, and robotics.

Bespoke Institutional subscribers have access to our popular Earnings Explorer tool. One of the sections of the tool allows you to search for individual stocks to see historical earnings results for the company. Below is a snapshot of AMBA pulled directly from the Earnings Explorer. As shown, AMBA has historically beaten EPS estimates 100% of the time since it went public in 2012. This quarter’s EPS beat was the company’s 27th in a row! Talk about consistency. In terms of sales, the company has a 96% beat rate, which means it has only missed sales estimates once in twenty-seven quarterly reports.

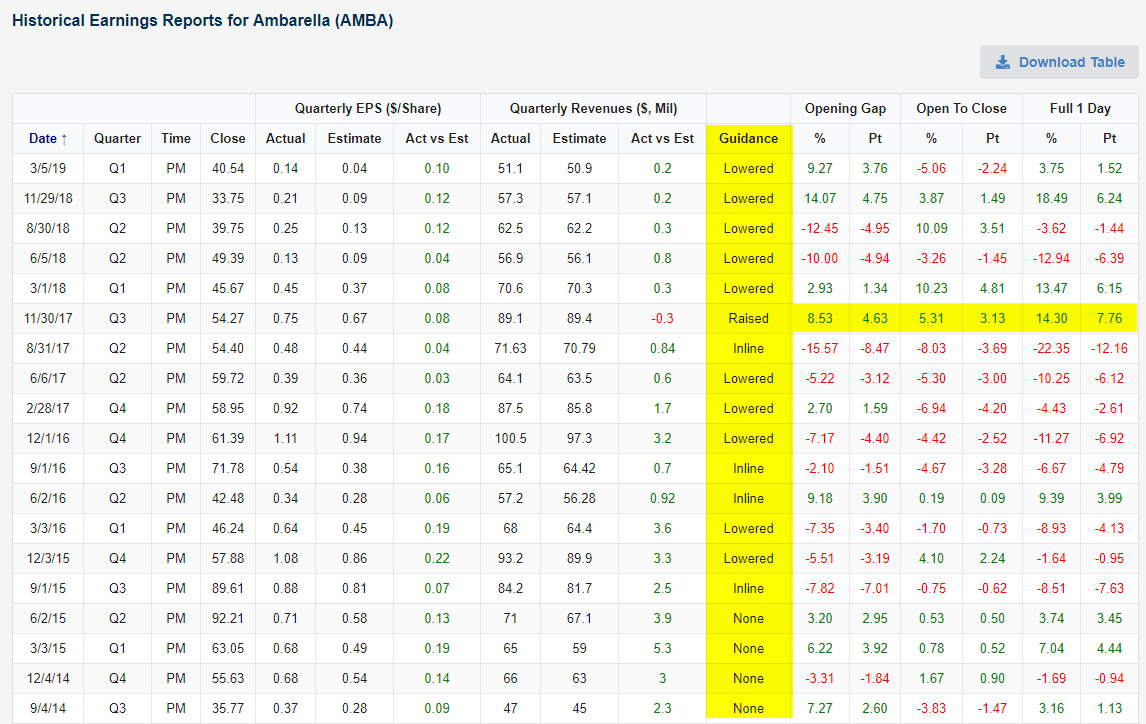

While AMBA has no problem beating EPS and sales estimates, it lowers guidance quite often. In just the last ten quarters, AMBA has lowered guidance eight times. Prior to this quarter, AMBA had lowered guidance for five quarters in a row. That’s what makes this quarter’s report so impressive. Instead of lowering guidance as the company usually does, it raised guidance this time around. This is only the second time that the company has raised guidance on a quarterly report since it went public. As highlighted in the table below, the last time AMBA raised guidance on November 30th, 2017, it opened higher by 8.5% and then continued to trade higher by another 5.3% from the open to the close. Its full-day change that day was +14.3%. Again, AMBA is set to gap higher at the open this morning by about 9%. Will the same trend of intraday buying that happened the last time AMBA raised guidance occur once again today? We’ll find out soon enough. Start a two-week free trial to Bespoke Institutional to unlock our Earnings Explorer tool and much more.

Morning Lineup – ADP.U.

The bulls are out again this morning, but an ADP Private Payrolls that simply stinks has dampened the mood. While economists were expecting the headline reading to come in at 185K, the actual reading was just 27K. That was the weakest monthly print since March 2010 and the third weakest report relative to expectations since at least 2006.

Outside of the US, the World Bank lowered its global growth forecast down by 0.3 percentage points to 2.6% and said that risks to the global economy are firmly on the downside. On a similar note, the IMF lowered its growth forecasts for China slightly just as the May Services PMI for that country came in lower than expected. In Europe, Services PMI data was slightly better than expected coming in at a level of 52.9 compared to expectations of 52.5. Even if the economic outlook is cloudy, investors have been encouraged by the belief that the Fed is ready to act if needed. Whether the market and FOMC are both on the same page with regards to what “needed” means, though, is up for debate, but more data like this morning’s ADP report will likely move the FOMC closer to acting.

Please click the link below to read today’s Bespoke Morning Lineup for our take on what the rates markets are pricing, a recap of services sector PMIs, and just as important the latest data on Semiconductor sales.

As mentioned above, the ADP Private Payrolls report just came in weaker than expected, missing consensus expectations by over 150K. Using our Economic Indicator Database, we found that this month’s report was the weakest relative to expectations since January 2009 and just the third time since 2006 that the report has missed expectations by more than 100K.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Equities Bounce Back Across Sectors

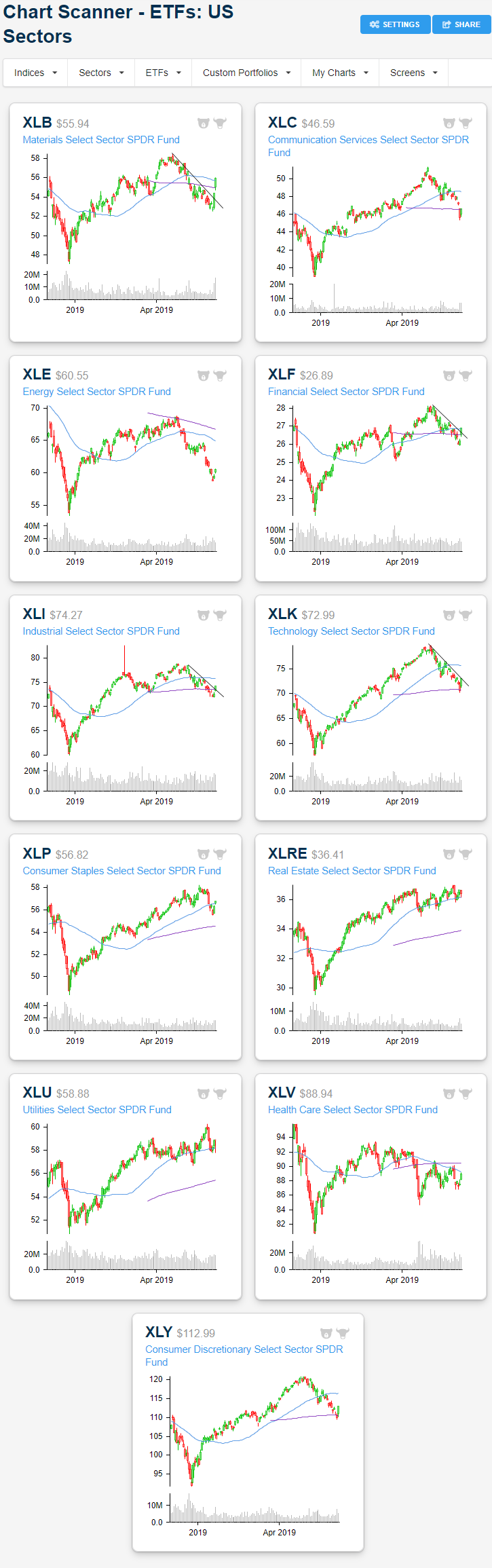

Equities roared back to life in Tuesday’s session as the major indices regained all of Monday’s losses and then some with the S&P 500 seeing its second strongest day of the year. Breadth was pretty strong among sectors as all but one, Real Estate (XLRE), finished the day higher. The Technology Sector (XLK) rose the most, surging 3.34%. This is only one day after a rout of tech giants (like Alphabet (GOOGL) and Apple (AAPL) in response to government investigations) dragged on XLK to finish the day just below the 200-DMA. Names like Facebook (FB) similarly dragged on the Communication Services sector (XLC) for the same reasons, but these losses were mostly made up for on Tuesday. Semis were a major factor in Tuesday’s tech rally as names like Advanced Micro Devices (AMD) and Nvidia (NVDA) rose as much as 7%. Materials (XLB) were the second best performing sector of the day as breadth in the sector was very strong with DowDuPont (DD) being the only S&P 500 Materials stock to be lower at Tuesday’s close. After gapping up to just above the 200-DMA, XLB rose further taking out the 50-DMA and finishing the day 2.81% higher. In addition to taking out the moving averages, XLB also broke out of its recent short term downtrend in dramatic fashion. Industrials (XLI) similarly saw a break out of its downtrend. Other cyclicals, the Financial Sector (XLF) and Consumer Discretionary (XLY), also performed well with both rising 2.71%. XLF’s chart has a similar pattern to XLB with Tuesday’s opening price sitting at the 200-DMA and finishing above the 50-DMA while also breaking out of its downtrend.

While cyclicals were bid up, defensives underperformed. The Consumer Staples sector was the best performing of the defensives as it rose 0.91%. Utilities (XLU) also managed to finish in the green, but it only rose 8.5 bps. Granted, Utilities finished well off of the day’s lows. Intraday, the sector had briefly dipped all the way below the 50-DMA. Finally, as previously mentioned, Real Estate (XLRE) was the only sector to move lower on the day, finishing down 0.55%. Similar to XLU, Real Estate finished off of the day’s lows near the 50-DMA. Start a two-week free trial to Bespoke Institutional to access our interactive Chart Scanner tool and much more.

The Closer – Unsustainable Surge, Fed vs Market, EM Rally, Auto Results – 6/4/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review the internals of today’s surge in equity prices and evaluate how sustainable this rally could be given breadth and price action in credit markets. Next, we provide our analysis of how the disconnect between the market and the Fed in regards to rate cuts in the near future. We then update our Bespoke EMFX Index which has popped higher. We finish with a look at the bounce in automakers and today’s Factory Orders release.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

B.I.G. Tips – Treasury Yields Coming Off Extremes

We’ve just published a B.I.G. Tips report that discusses the recent plunge in 10-year yields and provides a look at how stocks and bonds have followed through in similar periods where the yield in the 10-year reached extremely low levels. To put the recent move in perspective, levels like Monday’s have only been recorded on thirteen prior days in the last 30 years! To read this report and access all of our other reports, start a two-week free trial to Bespoke Premium!

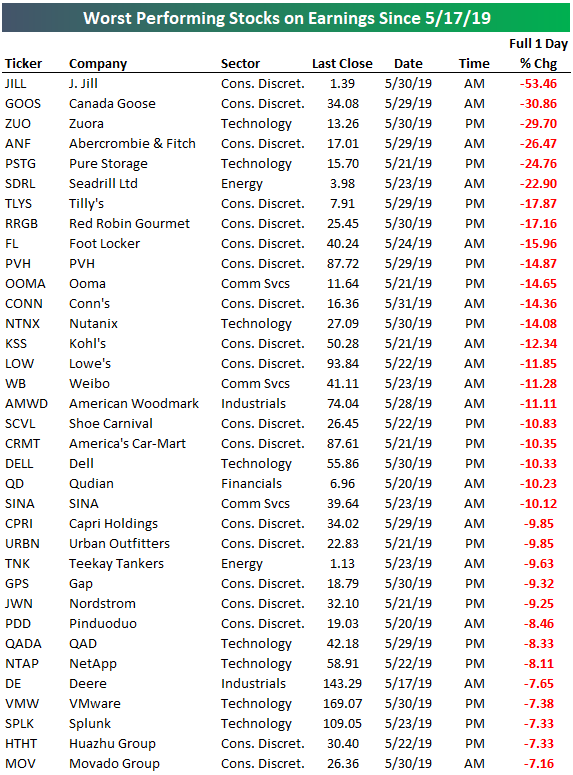

Severe Off-Season Earnings Weakness

Using our Earnings Explorer tool, we did a quick check today on how companies that have reported during this “off-season” have done. There have been 141 earnings reports since May 17th when the first quarter reporting period ended. Of these 141 reports, 71% reported stronger than expected EPS, while 62% reported stronger than expected sales. Only 6% have raised forward guidance while 11% have lowered guidance.

In terms of how company share prices have reacted to their reports this off-season, it has essentially been a bloodbath. The average stock that has reported has fallen 1.31% on its earnings reaction day, which is the first trading day following its earnings report. (For companies that report in the morning, its earnings reaction day is that trading day. For companies that report after the close, its earnings reaction day is the next trading day.)

Our rolling 3-month beat rate charts still show downtrends. While the bottom-line EPS beat rate remains nearly 3 points above its historical average, the top-line sales beat rate has recently dipped slightly below its average.

You can track the performance of individual stocks in reaction to earnings using our Earnings Explorer tool, but below is a list we pulled that shows the worst performing stocks in reaction to earnings since the “off-season” began on May 17th. Twenty-two of the 141 stocks that have reported this off-season have fallen more than 10% on their earnings reaction days. The list is littered with retailers like J. Jill (JILL), Canada Goose (GOOS), Abercrombie & Fitch (ANF), Foot Locker (FL), Kohl’s (KSS), Lowe’s (LOW), Urban Outfitters (URBN), and Nodstrom (JWN). Start a two-week free trial to Bespoke Institutional to unlock our Earnings Explorer tool and much more.

Bespoke Stock Scores — 6/4/19

Chart of the Day: Interest Rate Markets In Their Own World

As-of yesterday, the short-term interest rate market was pricing a 59% chance of a rate cut at the FOMC’s July meeting, a 75% chance of two cuts by December, and a 53% chance of three cuts by December. As a result, interest rate contracts and short-term bonds have exploded higher in price with two year yields down over half a percent in a bit less than two months. The explicit bet is that the FOMC will be forced to cut rates in response to rising uncertainty related to trade tensions and a weakening global economy, combined with risks of outright recession. In recent commentary, FOMC members have been much less sure about the negative sides of the outlook. One member of the FOMC (St. Louis Fed President James Bullard, the most dovish member of the committee and a regional bank President who has a history of outlandish lurches in commentary) has said verbatim that a cut may be warranted, but no other FOMC member has said anything close to that. Today, Fed Chair Powell said the FOMC will “act as appropriate to sustain the expansion” and is “closely monitoring” how trade developments impact the economy; that’s a long way from getting markets ready for an imminent cut! So the market is clearly being much more aggressive than the Fed. Why?

Continue reading this Chart of the Day by logging in (if you’re already a member) or starting a two-week free trial to any of our research membership levels.

May 2019 Headlines

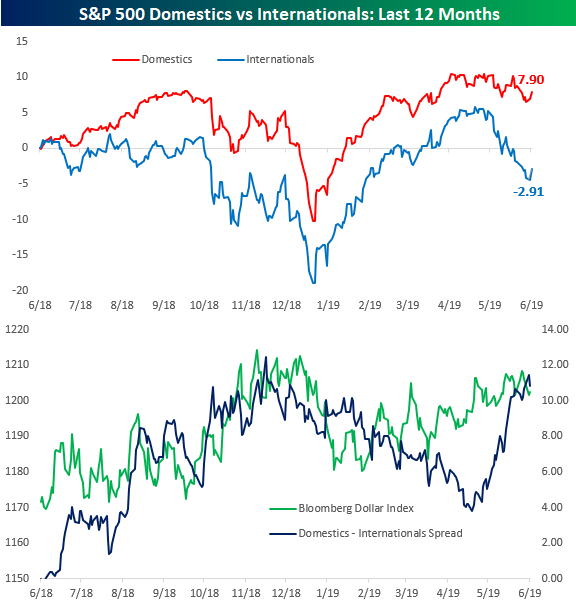

“Internationals” Catch A Break

With the US dollar taking a breather in the last couple of days, our index of Internationals has caught a bid in the early going today as it attempts to stabilize from a drop of just under 10% since late April. For those unfamiliar with our Internationals index, using our International Revenues Database, we classify any S&P 500 company which derives more than 50% of their revenues from outside the United States as part of the Internationals index, while any S&P 500 company which derives more than 90% of their revenues in the United States is part of our Domestics index.

The chart below shows the performance of both indices over the last 12 months, and given the relative weakness of the rest of the world’s economy versus the US, our Domestics index has consistently outperformed the Internationals. Since late May, though, the gap really widened as Internationals fell sharply in response to heightened concerns regarding global trade and possible retaliation from China and other countries in response to US tariffs on imports. Through the early going on Tuesday, the Domestics index is up 7.9% over the last year and down less than 2.5% from its recent high. The Internationals index, meanwhile, is down 2.91% over the last year and nearly 10% from its high less than six weeks ago.

In the second chart, we show a comparison between the Bloomberg US Dollar Index and the performance spread between the Domestics and Internationals indices over the last year. Typically, when the dollar is strong, Domestics outperform the Internationals and vice versa. That’s exactly what we are seeing now, as both the Dollar Index and the outperformance of Domestics relative to Internationals are right near 52-week highs. Going forward, any signs this week from the litany of Fed speakers that they are coming around to the market’s view of cutting rates sooner rather than later would likely pressure the dollar and lead to a boost for the Internationals. We could be seeing some early signs of that today as the Internationals index is bouncing from very oversold levels and trading higher by 1.7% compared to a gain of just 0.8% for the Domestics. Choose one of Bespoke’s three premium subscription options for our most actionable research.