The Closer: End of Week Charts — 7/26/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

B.I.G. Tips – Earnings Ideas

Nearly 600 stocks have reported earnings over the last two weeks, and 67% of them have beaten consensus analyst EPS estimates. In our newest B.I.G. Tips report, we break down a number of important earnings indicators and feature a number of individual stocks with bullish chart patterns following their recent earnings releases.

To read this report and see which stocks we like most coming out of earnings, start a two-week free trial to Bespoke Premium!

Next Week’s Economic Indicators – 7/26/19

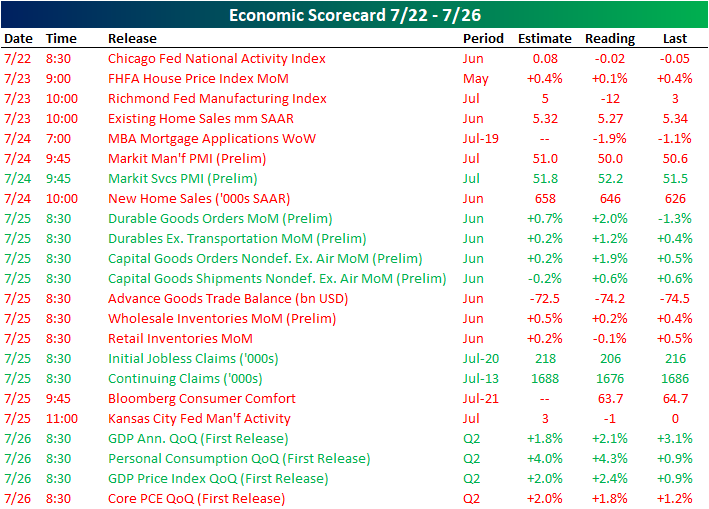

The Chicago Fed’s National Activity Index kicked off this week’s busy macroeconomic data slate on a disappointing note with a still negative reading that was below forecasts. Weak data continued to come in on Tuesday with FHFA home price growth slowing to 0.1% and the Richmond Fed Manufacturing index reaching a multi-year low. Existing Home Sales also came in weaker. Preliminary Markit PMIs released on Wednesday came in below estimates and weaker than the previous month while the services portion saw the opposite results. The release of preliminary Durable Goods and Capital Goods on Thursday came in much stronger than both expectations and the May release. Meanwhile, weekly labor data once again came in at a multi-month low. We ended the week with stronger than expected GDP data, but it still showed the economy slowed versus the first quarter. Overall, economic data didn’t have the greatest of weeks with over half of the indicators released weakening or coming in below estimates.

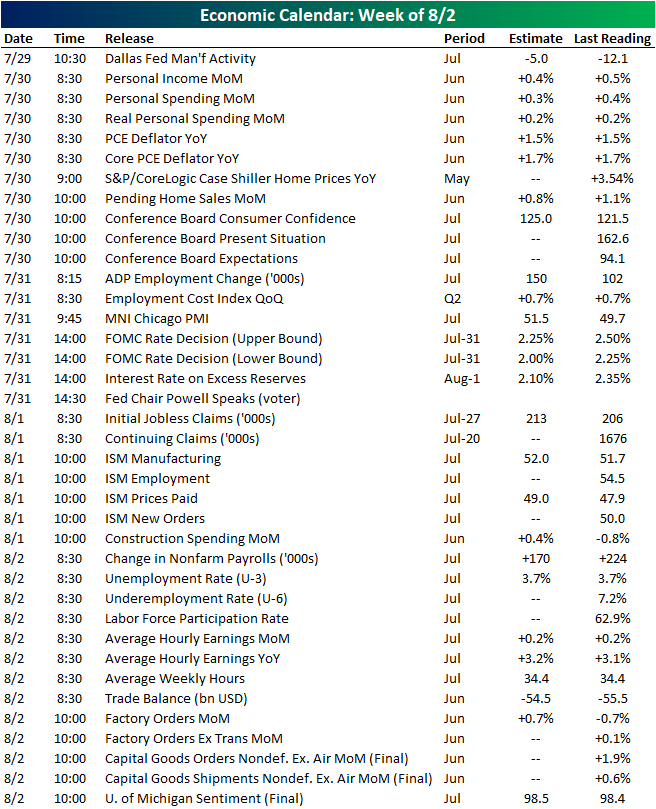

Next week is a busy one when it comes to macroeconomic developments. The week starts off quiet with only the Dallas Fed’s Manufacturing Activity Index out on Monday. It is expected to rebound to -5 off its multiyear low of -12.1 from its June release. Things pick up on Tuesday with the release of personal income and spending data which are forecast to fall 0.1%. PCE data, Pending Home Sales, and consumer confidence will also be out that day. Ahead of Friday’s Nonfarm Payrolls report, which is expected to show 170K added jobs in July, on Wednesday ADP will release their own employment data. Also on Wednesday, there will be an FOMC rate decision followed by a presser by Fed Chair Powell. Markets are anticipating a 25 bps cut in this meeting. After digesting the results of this meeting, on Thursday ISM will release their manufacturing report for July. In addition to the NFP report, the release of the June trade balance, factory orders, and the University of Michigan’s sentiment data will all round out the week on Friday. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – Strong Earnings; GDP on Tap

Ahead of US GDP today earnings headlines are flying, rates are slightly lower, and commodities are mixed. With huge names in tech (GOOGL, INTC, TWTR), quick service food (SBUX, MCD) and health care (ABBV) reporting very good numbers since the close yesterday, the market is poised to gap up over a quarter percent despite relatively weak AMZNnumbers. European earnings are also relatively strong once again.

Continue reading in today’s Morning Lineup.

Bespoke Morning Lineup – 7/26/19

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer – Inside Day Reversal, QE Dipsey-Doodle, Looking To GDP – 7/25/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, Given today’s inside day reversal, we show performance following other times this pattern has been observed following all-time highs. We also review the market reaction to confusing policy news out of Europe. We follow up with a discussion of what tomorrow’s GDP release could look like given recent data like the Census Advance Economic Indicators and Durable Goods. We finish with an update of our Five Fed Manufacturing composite with the addition of the Kansas City Fed’s index.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke’s Sector Snapshot — Strong Earnings Reactions

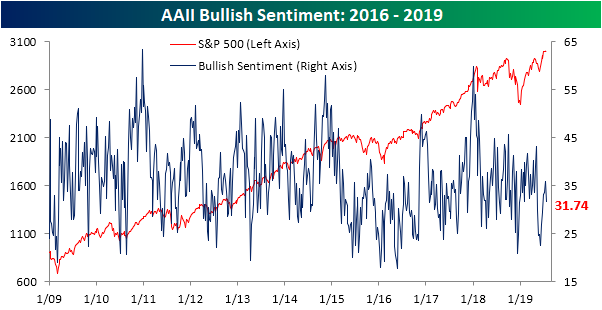

Sentiment Steps Back

After collapsing below 25% at the start of June, bullish sentiment had rebounded for six consecutive weeks, but this week’s release of the AAII survey snapped that streak. The percentage of bullish investors dropped to 31.74% from 35.93% last week. This comes despite the major indices once again reaching all-time highs yesterday (which admittedly would have little effect on the survey due to timing) and earnings season kicking off to a solid start with rising beat rates and guidance spreads. While this was the biggest drop in bullish sentiment since May, it has not brought the indicator to any sort of extreme low, but it has now been below its historical average for 11 consecutive weeks. While that may sound like a long streak, in the history of the survey—going back to 1987—there have been 19 other such streaks; six of which continued on for twice as long.

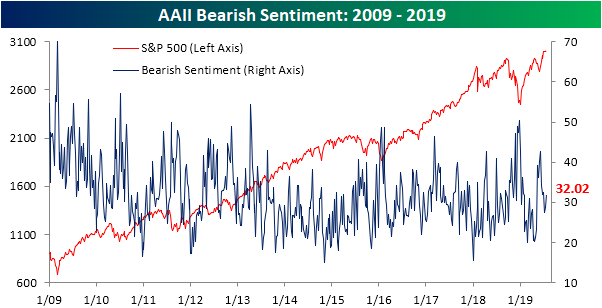

Whereas bullish sentiment fell, bearish sentiment picked up. Bears now outnumber bulls with 32.02% of investors reporting as bearish versus last week’s 28.64%. This is the first time that bears have outnumbered bulls since late June when a streak of nine straight weeks of this came to an end. Bearish sentiment has also now moved back above the historic average of 30.33% after staying below for two weeks. Before that, bearish sentiment was above average for 8 straight weeks.

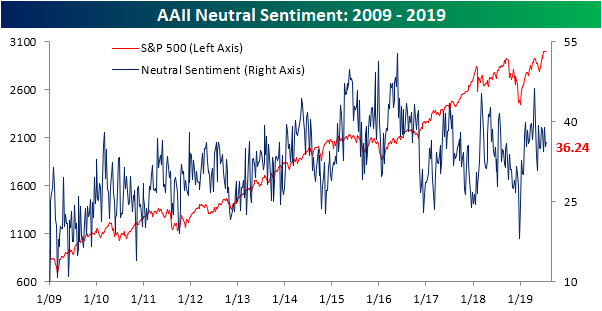

Although bears outnumber bulls, neutral is still the predominant sentiment level at 36.24%. For a solid chunk of this year—16 of 30 weeks—those reporting as neutral have outnumbered both bulls and bears. That is already more than the entirety of 2018 (14 weeks) and is closing in on that count for 2017 (18 weeks). Neutral sentiment continues to stay in a fairly tight range as it has for most of the year. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: European Earners Outperforming

B.I.G. Tips – Checkup on Breadth at New Highs

Throughout the bull market and especially since early 2018 when volatility in the market started to pick up, one factor consistently working in the market’s favor has been breadth, specifically the S&P 500’s cumulative A/D line. Each time the S&P 500 has made a new high, breadth has confirmed the move, and in each of the rallies coming out of corrections, breadth has consistently lead price. With the S&P 500 making another new closing high yesterday, in our latest B.I.G. Tips report we looked at current breadth levels for not only the S&P 500 but also each of the major sectors.

To continue reading this report, start a two-week free trial to Bespoke Premium!

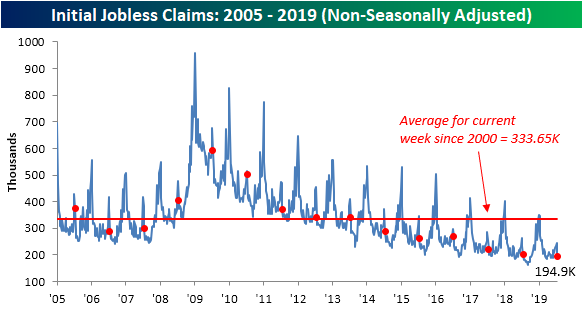

Claims Keep Moving Lower

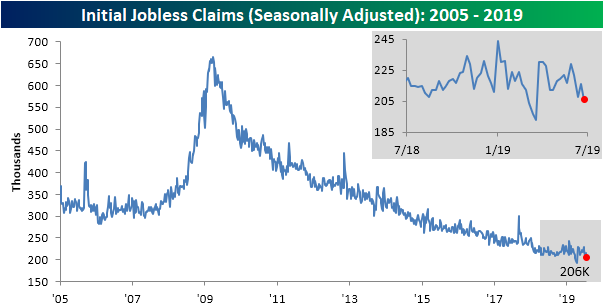

Two weeks after seasonally adjusted initial jobless claims came in at the lowest level in 3 months (208K), this week’s claims data continued to edge even lower dropping to 206K. This 206K number is now only 13K above the multi-decade low of 193K from the April 12th release. Expectations were actually calling for a small increase to 217K from last week’s 216K. This week’s drop also gave some headroom to the record streaks below 250K and 300K which grew to 94 and 229 weeks, respectively. Overall, this was a healthy print for claims as it held up near the lower end of the past year’s range and helped to reaffirm a trend lower of the past several weeks.

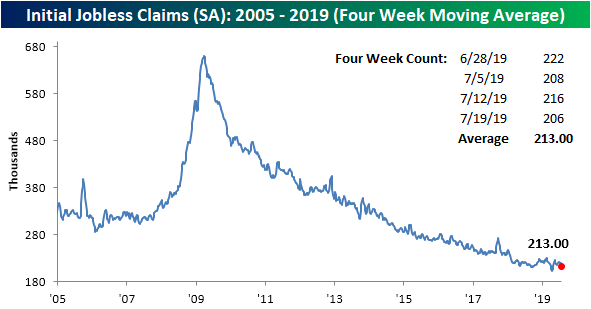

The four-week moving average, which helps to smooth out some of the week-to-week fluctuations, dropped to 213K from 218.75K last week. Similar to the seasonally adjusted weekly number, the moving average is also near the multi-decade lows from April (201.5K). Assuming next week sees another healthy print like we have over the past few weeks and with the recent high of 222K rolling off, the average could continue to grind lower.

On a non-seasonally adjusted basis, claims came in at 194.9K. This was a sizeable drop of 48.7K from last week’s number. This could be expected though as last week has typically been a seasonal peak for this time of the year. Regardless of seasonality, this drop to 194.9K is still a healthy print as this week’s reading is well below the average for the current week since 2000 and the lowest for the current week of the year of this cycle. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.