The Bespoke 50 Top Growth Stocks

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 108.3 percentage points. Through today, the “Bespoke 50” is up 221.5% since inception versus the S&P 500’s gain of 113.2%. Always remember, though, that past performance is no guarantee of future returns. To view our “Bespoke 50” list of top growth stocks, please start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day: How Bad Is Breadth?

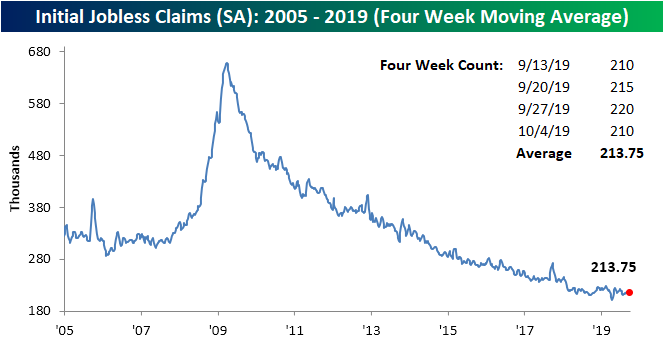

Claims Stay In Their Lane

Headed into this week, initial jobless claims had been on the rise for three weeks in a row. This streak has come to an end as claims fell to 210K. Expectations were calling for this week to be unchanged from last week’s revised 220K. This decline has brought claims back to the lower end of the past year’s range and the lowest since September 12th. The record streaks at or below 300K and 250K also continue this week, growing to 240 and 105 consecutive weeks, respectively.

Although the weekly data saw a fairly large decrease with its 10K drop, the four-week moving average actually rose for its second week in a row. The moving average, which helps to smooth out the week to week fluctuations, now sits at 213.75K. While it did rise, the degree of the increase was once again small. The moving average is up just 1K from last week, and that is actually one of the larger moves in recent weeks as the prior three weeks only saw movements of 0.25K.

Given this, the moving average has remained in its tight range recently. Over the past three months, there has been only one week (August 30th when the average was 216.75K) when the average was not in the range of 212K and 215K. That sort of tight range over the past quarter is something that has not been observed in the past couple of years. In fact, the spread of just 4.75K between the past 3 months’ high and low is the joint smallest range since late August 2017. Furthermore, that is the second tightest range of the current cycle with the only smaller 3-month range being the week prior to the aforementioned week in August 2017 when the range was just 4K. In other words, claims are still at healthy levels but have also not picked a direction of improvement or worsening.

Claims in non-seasonally adjusted terms also rose by just 1K this week to 173K. While that is a small week-over-week change, relative to last year claims dropped by over 20K. This week’s NSA data was also well below the average for the current week of the year since 2000 of 300.56K. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke Morning Lineup – 10/10/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Epic Flows From Equities, Fed Minutes, JOLTS-A-Palooza, EIA – 10/9/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at the massive flow from equity mutual funds into fixed-income funds. We then review the consolidation of FANG stocks and today’s Fed minutes. Turning to economic data, we take a deep dive into the details of today’s JOLTS data before finishing with weekly EIA data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Dividend Stock Spotlight: The Dividend Aristocrats (NOBL)

The Dividend Aristocrats (ETF: NOBL) is an index made up of 57 S&P 500 stocks that have long histories of increasing their dividend payments to shareholders. In fact, each of these companies has raised their dividend for 25 consecutive years or more; some have even been growing their dividends twice as long. After a sharp rally at the end of August through mid-September which brought the index up to all-time highs, the group fell back below its prior highs at the start of the month. Having fallen further since then, NOBL now sits at the bottom of its long term uptrend.

Below is a list of the 20 Dividend Aristocrat members with the highest yields. A large portion of the top 20 are Health Care and Consumer Staples stocks (each sector having 5 of the 20) with Industrials also having a sizable contribution (4 stocks) to the highest yielders. Currently, there are three stocks that yield over 5% including Exxon Mobil (XOM), AT&T (T), and AbbVie (ABBV). AbbVie (ABBV) — which was spun off from Abbott Labs in 2013 — tops this list with a yield of 5.8%. Even though the stock has been in a downtrend over the past year, it has still increased its dividend. Multiple other stocks in this group including Franklin Resources (BEN), 3M (MMM), and Johnson and Johnson (JNJ) are also in downtrends. Meanwhile, others such as Coca-Cola (KO) are in uptrends. We created a custom portfolio of all the dividend aristocrats for members so that they can keep tabs on the trends of these stocks. Some other notable high yielders include People’s United Financial (PBCT) and Leggett & Platt (LEG). These two have some of the highest yields in spite of also having the third smallest and smallest market caps, respectively, of all 57 dividend aristocrats. JNJ, on the other hand, has the largest market cap of all aristocrats.

While ABBV (formerly Abbott Labs) has the highest yield of the top 20, it does not have the longest track record of growing its dividend even though it has been doing so for nearly 50 years. Genuine Parts (GPC) actually holds that accolade having raised its dividend for 63 consecutive years. Of the other top 20, 3M (MMM) and Emerson Electric (EMR) are the only other stocks to have done so for 60 years or more. A few others like Johnson and Johnson (JNJ), Federal Realty (FRT), and Coca-Cola (KO) have grown their dividends for better than a half-century. Start a two-week free trial to Bespoke Institutional to access our custom portfolios, Trend Analyzer, Chart Scanner tool, and more.

B.I.G. Tips – Do Nothing Markets

Fixed Income Weekly – 10/9/19

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we review the narrowing yield premium for US bonds relative to the rest of the world.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

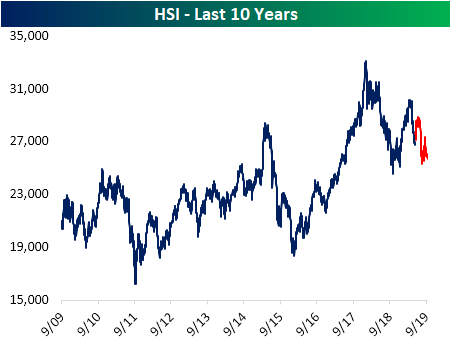

Protests Pummel Hong Kong Data

Through most of the second half of the year, a series of mass protests in opposition to Chinese extradition legislation has been consuming Hong Kong. While smaller-scale protests have been taking place since the early spring, things really began to ramp up in June when hundreds of thousands took to the streets. In the more than three months that have passed since then, some of the effects are beginning to be seen in the country’s economic data that we track in our Global Macro Dashboard. Markets were the quickest to respond as the country’s Hang Seng Index has fallen roughly 5% since the start of June. The HSI is now in a defined downtrend over the past couple of years and recently has been making its way towards support at last year’s lows.

Hong Kong retail sales have tanked since protests began. In the months leading up, retail sales had been contracting year-over-year for four consecutive months. The reading for May came in at -1.4%, but once protests took effect the following month, retail sales collapsed to a -6.7% growth rate. Conditions have only worsened from there as retail sales contracted 23% YoY in August. That is the worst contraction in the history of the data going back to 2006, surpassing the previous low of -20.6% in February 2016.

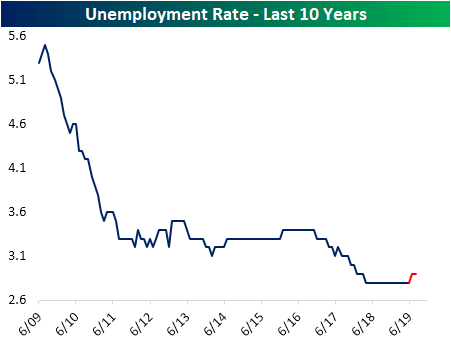

Likely as a result of people taking to the streets rather than showing up to work, the unemployment rate has begun to tick higher over the past few months. For the entire year before the protests began, Hong Kong’s unemployment rate held steady at 2.8%; the lowest level of the past decade. But the July release showed the rate has risen 0.1% to 2.9%. That was the first increase of any kind since the one month blip in July of 2017. Start a two-week free trial to Bespoke Institutional to access our Global Macro Dashboard as well as our Economic Indicators Database and much more.

Bespoke’s Global Macro Dashboard — 10/9/19

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!