Brunch Reads – 4/12/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Poyekhali!: With the Artemis 2 astronauts splashing down on Friday after returning from their trip around the moon, we find this look back at history especially relevant. On April 12, 1961, Yuri Gagarin became the first person to travel into space aboard Vostok 1. Launched by the Soviet Union, Gagarin exclaimed “Poyekhali!” which means “Let’s go!” and completed a single orbit of Earth in 108 minutes, reaching speeds of more than 17,000 mph.

The mission proved that humans could survive and function in space, marking a major milestone in the Space Race. Gagarin’s successful flight made him an international figure overnight and accelerated efforts by the United States to send astronauts into orbit. His achievement remains one of the most important moments in the history of space exploration.

Health & Wellness

Pharma of the Future (Northwestern Magazine)

Researchers are developing implantable “living pharmacies” that use engineered cells inside the body to produce and deliver drugs on demand, potentially improving adherence and allowing treatments to be adjusted in real time. By combining biology with electronics, these devices could treat conditions like cancer, diabetes, and sleep disorders while opening the door to more personalized and automated care. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – 4/10/26 – Chaotic Headlines And What Matters Most

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. Hormuz remained closed this week but markets are working very hard to look past that fact given the huge surge in stocks and drop in energy futures. We go through the week’s chaotic headlines in detail, but keep our eye on other equity market drivers as well: economic data in the US and abroad, risk premiums (and return potential) offered by US stocks and bonds, the very strong performance of emerging markets, and the inflation outlook including the critical question of whether inflation expectations will remain anchored amidst this latest shock to consumer prices.

Daily Sector Snapshot — 4/10/26

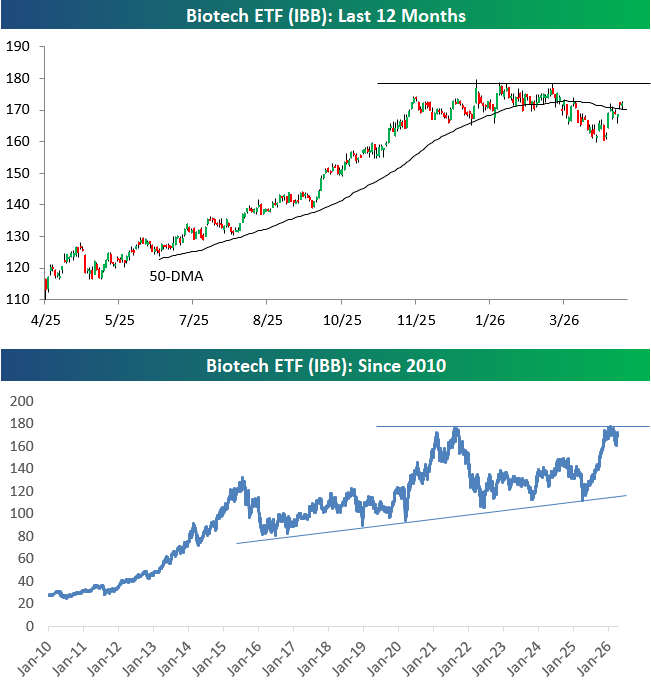

Can Forgotten Biotech Break Out?

After a 50%+ run from lows last April through highs in mid-January, the Biotech group has been trending sideways over the last few months.

Biotech hasn’t garnered much attention lately, with all the coverage of the Iran War and the AI Doom trade that’s been taking down software stocks even as AI infrastructure stocks continue to surge.

Below is a look at the iShares Biotech ETF (IBB), both recently (last 12 months) and over the long-term (since 2010). What we see is a group trading sideways right now at a key inflection point.

In the short-term, IBB has just managed to re-take its 50-day moving average, but it needs to break out to new highs to resume the uptrend that was in place last year.

Looking longer term, IBB’s rally in the last year ran out of steam at the same level it stopped at back in late 2021 before the broader market entered a nasty bear market.

Putting the short-term and long-term together, if Biotech manages to break out to new highs at some point this year, it would clear a significant resistance hurdle and open the door up for another big leg higher.

If new highs can’t be made soon, the double tops from earlier this year and late 2021 will loom large in the minds of traders.

Sign up for Bespoke’s Think BIG mailing list to receive an interesting market stat like this in your inbox a few times per week. Click here or on the image below to sign up. An email is all we need!

Bespoke’s Morning Lineup – 4/10/26

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The market is a pendulum that forever swings between unsustainable optimism and unjustified pessimism.” – Jason Zweig

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

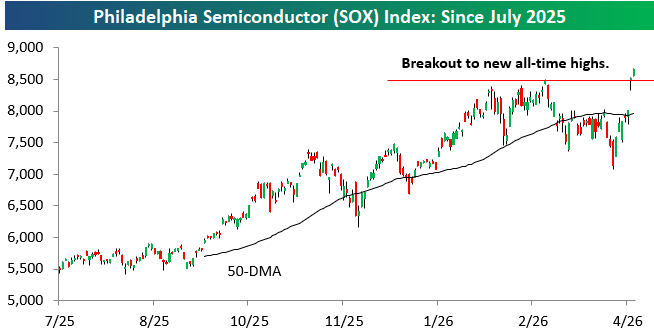

While the S&P 500 still sits 2.8% below all-time highs, both the Dow Transports and Philadelphia Semiconductor index — two groups seen as “leading” indicators — hit new all-time highs yesterday. The charts below show the breakouts to new highs for these two closely-followed areas of the market.

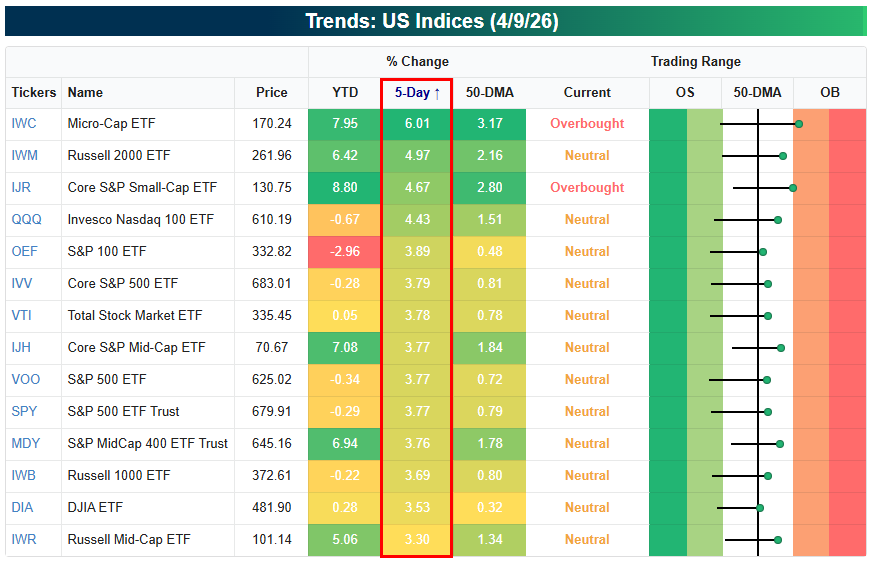

US equity futures are trading slightly higher this morning as we look to close out the week with five days of gains (and extend the daily win streak to eight dating back to last Tuesday).

Below is a look at the swing we’ve seen from oversold levels last week to back above the 50-DMA for most key US index ETFs:

While we’ve seen a nice bounce, price charts for ETFs like SPY, QQQ, and IWM still have work to do to break out of the choppy action seen for many months now.

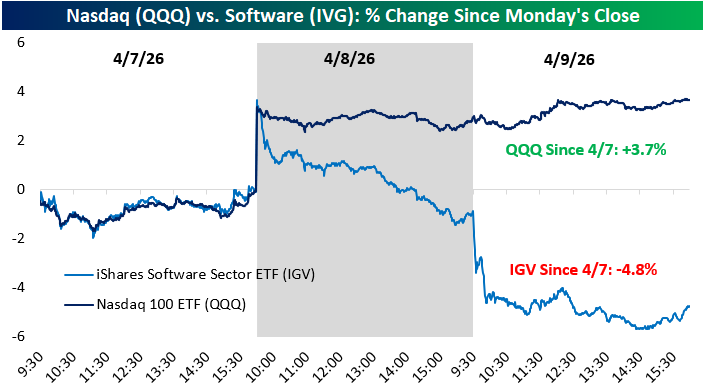

Yesterday was another painful day for the software group, which fell another 3.9% as algos look to exit or short anything at risk of AI obsolescence.

As shown below, IGV is now down 4.8% since Tuesday’s close when the US/Iran ceasefire was announced versus a gain of 3.7% for the broader Nasdaq 100 (QQQ).

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Cybersecurity, NIPA Shifts, PCE – 4/9/26

Log-in here if you’re a member with access to the Closer.

- Despite the recent pullback, Brent crude oil remains on pace for $200/barrel by late May.

- Alongside software stocks, cybersecurity names have also gotten hit hard in the past few months, but there have been a handful of outperformers.

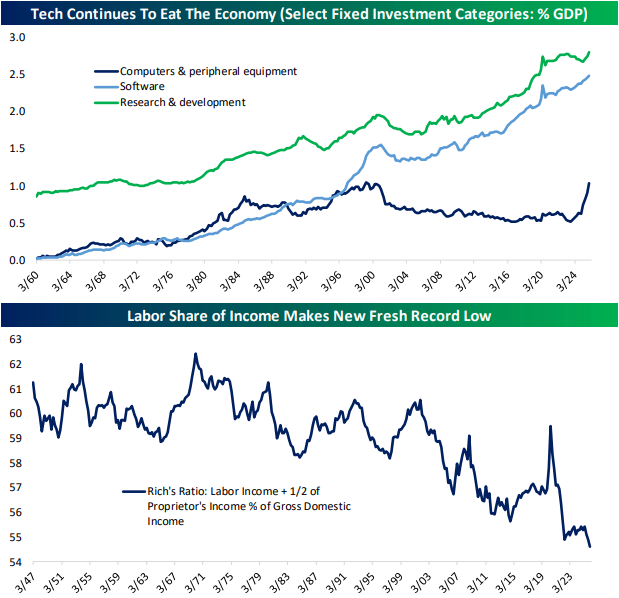

- Tech related categories for investment continue to surge as a share of GDP.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Are the Semis and Transports Leading the Market to New Highs?

For generations of market watchers, the Dow Jones Transportation Index was considered the ultimate leading indicator for the broader market. The idea being that if goods were moving, the economy was humming.

For today’s digital economy, the “leading” torch has been handed to the Semis group, which we labeled “the Transports of the 21st century” years ago.

The logic is the same: semiconductors are the essential inputs that power modern economic activity, from smartphones to data centers to automobiles.

When both of these bellwether indices are breaking out to new all-time highs simultaneously, as they are right now, it’s a signal worth paying attention to.

![]()

What makes the current setup particularly compelling is that the S&P 500 has not yet confirmed the move, still sitting roughly 2.5% below its own all-time high.

Historically, when leading indicators like the Transports and Semis are making new highs while the broader market lags, it has been viewed as a sign that the index is being pulled higher, not pushed.

The charts for Transports and Semis above show clean breakouts, with the 50-day moving average trending solidly higher beneath price. That is the kind of technical foundation that tends to give bulls confidence.

If the S&P 500 closes the gap as well and confirms with its own breakout, the weight of the evidence will be difficult to argue with.

Sign up for Bespoke’s Think BIG mailing list to receive an interesting market stat like this in your inbox a few times per week. Click here or on the image below to sign up. An email is all we need!

Bespoke’s Weekly Sector Snapshot — 4/2/26

Bespoke’s Consumer Pulse Report – April 2026

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.