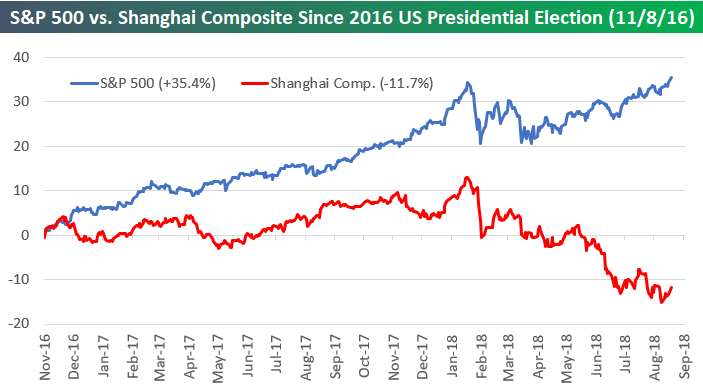

US vs. Chinese Stocks

This is a topic that has been discussed often recently, but it’s worth highlighting it again — US equities have been crushing Chinese equities. Below we show the performance of the S&P 500 versus the Shanghai Composite since President Trump was elected in November 2016. As of yesterday, the S&P was up 35.4%, while the Shanghai Composite was down 11.7%.

While the US has led China throughout Trump’s entire term thus far, we’ve seen significant divergence since the US/China trade battle really began to heat up earlier this year. As US equities have rallied over the last few months, Chinese equities have fallen lower and lower.

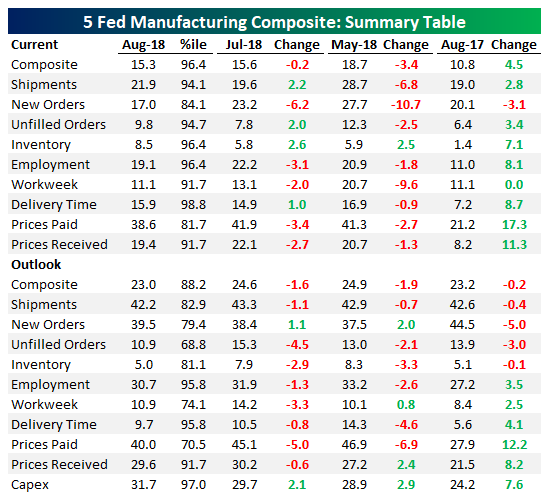

5 Fed Manufacturing Index Softer In August

Each month, we aggregate the 5 regional Fed manufacturing activity indices into one gauge that assesses activity around the country. The sample includes manufacturers in the NY, Philadelphia, Richmond, Kansas City, and Dallas Fed districts. As shown in the table below there were a couple of improvements in the current assessment of various categories of activity, with Shipments, Unfilled Orders, Inventory, and Delivery Time all rising versus July. While August wasn’t a horrible result, only one category (Inventory) is up in the last three months. Expectations were much weaker sequentially, with only two categories (New Orders and Capex) rising sequentially. Finally, we note that while indices are declining broadly, most categories are still at very high levels as shown by the percentile column.

Below we show charts of selected industries from above along with the composite of all series. As shown, the composite is definitely pulling back with New Orders especially weak.

The Closer — Cuts Priced, NAFTA Noise, FX Positioning — 8/27/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we assess the implications of the very strong gap up in the wake of all-time highs set yesterday. We also review market pricing of Fed cuts in out years, NAFTA news today (as well as some data from Mexico), and finally take a further look at positioning in the FX futures market.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

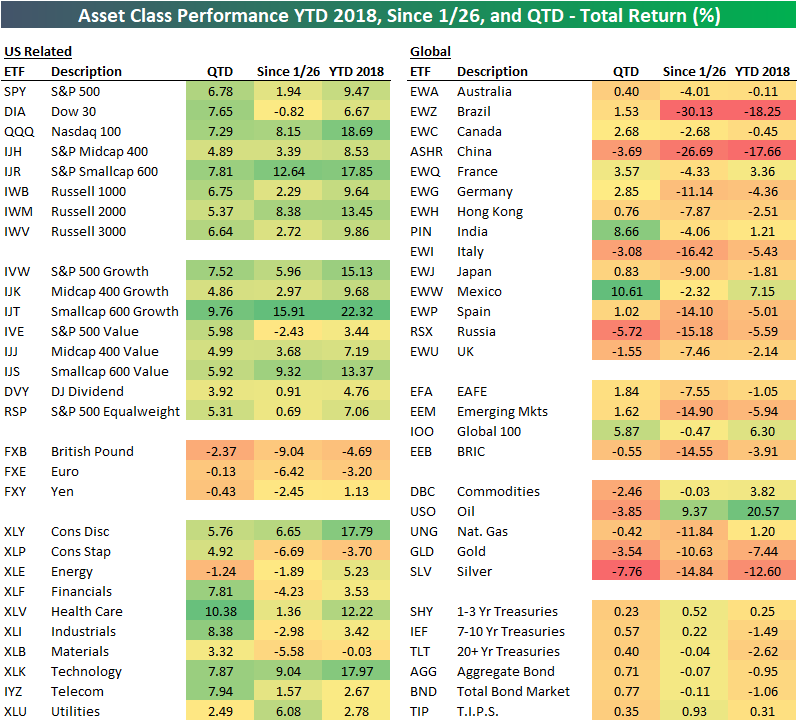

Bespoke’s Asset Class Performance Matrix: 2018 YTD and More

Below is an updated look at our asset class performance matrix. With the S&P 500 finally taking out its January 26th all-time closing high, the matrix allows you to see how other areas of the financial world have performed since that date as well. Note that performance numbers are total return, which is why the S&P 500 is up 1.94% since 1/26 even though it has just barely moved above that level in price.

While the S&P has just crossed above its January highs, the Dow is still slightly down. The tech-heavy Nasdaq 100, however, is up huge at +8.15%. Smallcaps (IJR, IWM) are up even more with gains of 10%+.

Looking at S&P 500 sectors, five are up since 1/26 and five are down. Technology (XLK) is up the most, followed by Consumer Discretionary (XLY) and Utilities (XLU), while Consumer Staples (XLP), Materials (XLB), and Financials (XLF) are down the most.

Outside of the US, equity market performance has been horrendous since January 26th. Brazil (EWZ) and China (ASHR) are both down 25%+, and not one single country ETF in our matrix is in the green. Commodities are also in the red with the exception of oil (USO), while Treasury ETFs are essentially flat.

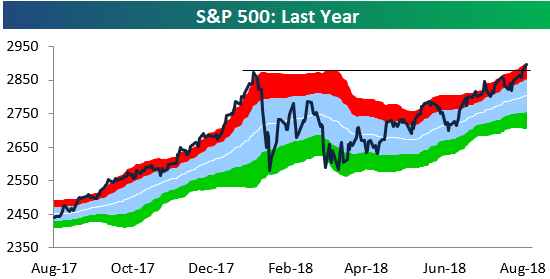

S&P 500 Breakout; Sector Trading Range Charts

After finally closing at a new all-time high on Friday, the S&P 500 continued its push into uncharted waters with a solid gain of 80 basis points today. You can see the breakout to new highs pretty clearly in our trading range chart of the S&P 500 below.

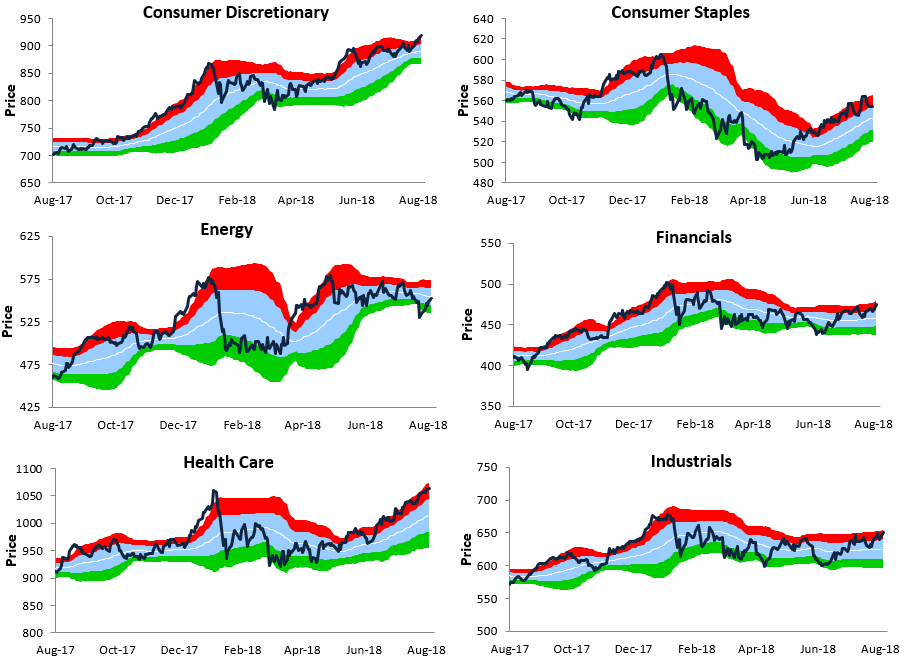

While the S&P (and most major US indices) has indeed broken out to new highs, not every area of the equity market has joined the fun. In fact, only three of the major sectors have traded to new highs along with the S&P — Consumer Discretionary, Health Care, and Technology. Below we show trading range charts for ten S&P sectors (Real Estate not included). In each chart, the white line represents the 50-day moving average, while the red and green areas represent overbought and oversold territory.

While Tech, Consumer Discretionary, and Health Care have broken out, none of the other sectors are really even that close to breaking out. Financials and Industrials are the next likely to test prior highs, but they still have a way to go.

Economic Surprises Improving In The Eurozone, Deteriorating In The US

Recently, the Citi Economic Surprise Index for the Eurozone has started to improve while the Citi Economic Surprise Index for the US has slipped into negative territory. As shown in the first chart below, we show the relative surge in Eurozone data surprise versus the US. Historically, that’s had a relatively mixed message for relative equity performance. As shown in the chart below, forward returns are at times correlated and at times uncorrelated to the relative performance of Eurozone versus US equities. But the bottom line is that longer-run, relative economic surprise index performance is basically uncorrelated to forward performance; we show the long-run lack of correlation in the bottom chart below.

Fed Speakers Dial Back Hawkishness

The Fed is currently engaged in an internal discussion about what to do once interest rates reach “neutral”; that is, the rate at which the economy is neither accelerated nor braked by the overnight interest rate. Where that “neutral” rate lies is part of the debate, but the market has basically priced an end to the current hiking cycle and start of a cutting cycle in about 18 months to 2 years. As that conversation has evolved, the FOMC has shifted into more dovish territory after speaking relatively hawkishly from late April to late June.

We keep track of what the Fed is saying with regular updates to our Fedspeak Monitor, a running summary of what FOMC members say publicly. This is a qualitative assessment, so of course it might differ somewhat from others’ views on how hawkish or dovish a given speech is. Using each speech’s rating, we can keep track over time how hawkish or dovish the FOMC is. The result is shown in the chart below, which tends to track the 3-month change in the 10 year yield pretty well over time. If you’d like access to our Fedspeak Monitor in real time, start a two-week free trial to Bespoke Institutional today.

Chart of the Day: Dollars Over-Owned

Bespoke Brunch Reads Linkfest — 8/26/18

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Labor In The Valley

What is this weird Twitter army of Amazon drones cheerfully defending warehouse work? by Devin Coldewey (TechCrunch)

Amazon appears to be astroturfing a public display of worker satisfaction via either bots or the Twitter accounts of actual workers; the larger story isn’t exactly clear. [Link]

Microsoft Bug Testers Unionized. Then They Were Dismissed by Josh Eidelson and Hassan Kanu (Bloomberg)

While tech companies, especially those based on the West Coast, have a reputation for being liberal or left-wing bastions, their relationship with labor isn’t consistent with that image; this story about Microsoft is a good example. [Link; soft paywall]

Turkey

Framing Turkey’s Financial Vulnerabilites: Some Rhymes with the Asian Crisis, but Not a Repeat by Brad Setser (Council on Foreign Relations)

Setser makes the case that Turkey’s banks are so exposed to foreign exchange denominated debt that the decline in lira has dramatically raised the odds of a funding crisis similar to the Asian Tigers in 1997. On the other hand, the complexity of the Turkish banking and credit system is very different, and Setser discusses in great detail. [Link]

Framing Crashed (5): The Turkish Crisis – the Missing Chapter (Adam Tooze)

Due to its very unique geographic, religious, cultural, financial, and political position as a bridge between the Middle East and Europe, Turkey is a nexus for all sorts of narratives related to near-history. [Link]

Real Estate

Traditional mortgage denial metrics may misrepresent racial and ethnic discrimination by Laurie Goodman and Bing Bai (Urban Institute)

While minorities tend to face higher mortgage applications denial rates than whites, they also typically have lower credit scores and incomes. After adjusting for these credit profiles, an interesting trend emerges: while Hispanic and white borrowers face an elevated denial rate relative to whites when adjusting for credit quality, it’s actually Asian buyers who face the highest “real” denial rates. [Link]

Climate Change Has Already Hit Home Prices, Led by Jersey Shore by Christopher Flavelle (Bloomberg)

A comprehensive study of property values on the New Jersey coast which are exposed to sea level rise shows that climate change’s impacts are already starting to have adverse impacts on home values. [Link; soft paywall, auto-playing video]

Luxury Apartment Sales Plummet in New York City by Josh Barbanel (WSJ)

Sales of apartments priced at $5mm or more fell 31% YoY in the first six months of the year, digesting extremely high prices and the impact of tax reform. [Link; paywall]

Unreal Animals

Company is offering ‘fur-ternity leave’ for new pet owners by Matthew Haag (CNBC/NYT)

A Minneapolis firm is offering its employees the ability to work from home for a week when they get a new dog or cat. [Link]

Animal crackers break out of their cages (CNBC/AP)

For more than a century, Barnum’s Animal Crackers (a Nabisco brand owned by Mondelez) were shown in cages, as animals were kept for circuses were historically. A 2016 request from PETA led to the change. [Link]

Weird History

Before the Civil War, Congress Was a Hotbed of Violence by Anna Diamond (Smithsonian)

Imagine if your Senator was beaten nearly to death with a stick at his desk during discussion of legislation? That was the environment of Congress prior to the Civil War, when outbursts like the Caning of Sumter were frequent and part of the process of making (or, in the case of the South, more frequently preventing) laws. [Link]

History of Rat Control In Alberta (Alberta Agriculture and Forestry)

As rates crept westward across the Prairies in the 1940s and 1950s, Alberta prepared by instituting an intense public awareness campaign and immediately eliminating even the smallest infestations. As a result, it’s just about the only human-populated place on earth without rats. [Link]

Economics

Elizabeth Warren Has Got It All Wrong by Matthew C. Klein (Barron’s)

Senator Warren of Massachusetts wants companies to distribute less cashflow to shareholders via buybacks. She’s misinformed about when and how companies buy back shares, and how that effects their ability to invest. [Link; paywall]

Demographics, Unemployment Rate and Inflation by Bill McBride (Calculated Risk)

Teasing out the relationship between demographics and macroeconomic variables is a significant challenge, but the general consensus is that population growth and inflation are positively correlated. [Link]

Network Defects

Apple and Google Face Growing Revolt Over App Store ‘Tax’ by Mark Bergen and Christopher Palmeri (Bloomberg Quint)

Apple and Google take a big cut from developers who make games or apps that get discovered and installed via the centralized app stores. But now, publishers are pushing back. [Link]

Facebook Fueled Anti-Refugee Attacks in Germany, New Research Suggests by Amanda Taub and Max Fisher (NYT)

A study by University of Warwick researchers suggest that a one standard deviation rise in Facebook use was correlated to a 50% increase in attacks on refugees. [Link; soft paywall]

Social Norms

Sorry, Pal, I Don’t Want to Talk: The Other Reason People Wear AirPods by Rebecca Dolan (WSJ)

Apple AirPods are being worn all day by users who want to avoid conversation or interruption. We’re wondering why it has to be AirPods as opposed to other forms of wireless headphones which generally have the same effect. [Link; paywall]

Venture

Benchmark Capital Stays Lean, Even After $14 Billion Bonanza by Rolfe Winkler (WJS)

Despite a trend that has seen billions of new capital flow into VC firms, one of the original early stage shops is not expanding its annual fund size, keeping things the same size as it has since 2004 despite a 25x performance from its 2011 vintage fund. [Link; paywall]

Sports

Won and done? Sportsbooks banning the smart money by David Purdum (ESPN)

Bookmakers in the UK are increasingly banning successful bettors, a practice that is totally legal and spreading to the US. [Link]

‘Listen To The Kids’: How Atlanta Became The Black Soccer Capital Of America (Bleacher Report)

A walk through the grass roots soccer scene in Atlanta, where immigrant families, hip hop, and an electric MLS squad have combined to create a passionate fan base for the beautiful game in Georgia. [Link]

Have a great Sunday!

The Bespoke Report: “I am the Stock Market King!”

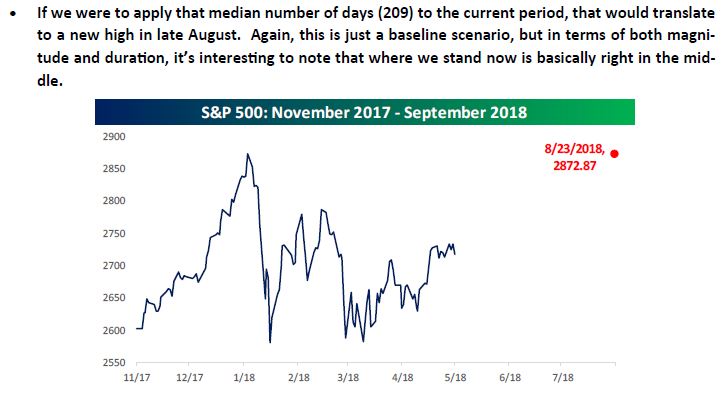

In our Bespoke Report dated 5/25/18, we provided the following chart and comments in our discussion of market corrections modeling that the S&P 500 would close at an all-time high again on 8/23/18. With the S&P 500 finally closing at an all-time high on Friday, we ended up being off by a day, but we’ll take it!

We’ve just published our latest weekly Bespoke Report newsletter, which is available to subscribers across all three of our membership levels. Sign up here to read the report.

To get up to speed on our thoughts regarding the market’s direction going forward, choose any membership option and access this week’s full Bespoke Report newsletter after signing up! You won’t be disappointed. Some of the topics discussed in this week’s report include:

- Comparison between now and 2000

- Housing starts to roll over

- The US economy and the global slowdown

- Decade-low readings in the yield curve

- Some attractive Financial sector stocks

- Market performance leading up to the mid-terms

- High yield breaks through a key level

- Sector breadth

- An exceptionally consistent Spring and Summer

- US vs ROW for the rest of year

- New highs- what now?

- Dividend Model Portfolio Update