Chart of the Day: AAL The Way Down, But Not Out

The Closer — LIBOR Climbs, Real Rates Rise, Growth Rich To Value (Duh?) — 10/9/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review rising interbank rates but falling spreads on those rates relative to the policy rate. We also discuss how big of a driver real yields have been in the recent UST selloff. Mexican and Brazilian equities have outperformed EM pretty dramatically of late, and the rotation within EM equities shows a new sensitivity to oil prices. We also discuss the extreme outperformance of growth relative to value and the enormous divergence in forward valuations between growth and value stocks.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

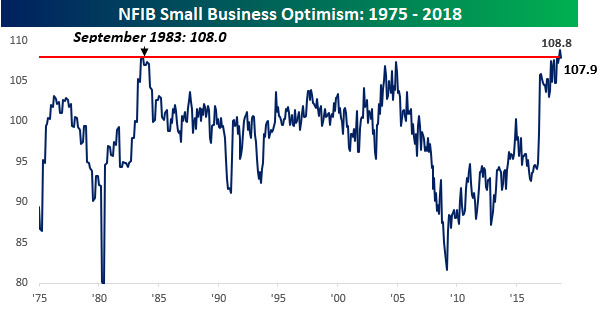

Small Businesses Slightly Less Optimistic

Small business sentiment for the month of September was released earlier this morning, and while the headline index saw a modest decline (108.8 down to 107.9) and came in below consensus forecasts of 108.3, the overall level is still extremely optimistic. One of the more interesting comments in the report was that “The economy is growing faster than our ability to support that growth without inflation or significant productivity gains.” It’s this line of reasoning which is exactly why the FOMC is so vigilant with respect to upward moves in prices.

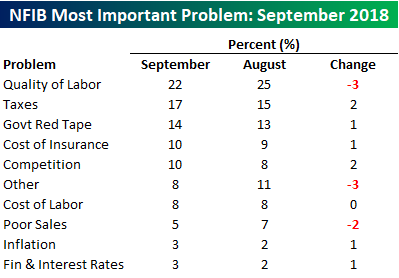

The table below summarizes the issues that small businesses currently cite as their biggest problems. Topping the list once again this month is Quality of Labor. While it could just be a one-month blip, it was a bit encouraging to see that this reading actually dropped from 25% in August to 22% in September. On the upside, the two components that saw the largest increases were Taxes (15 up to 17) and Competition (8 up to 10).

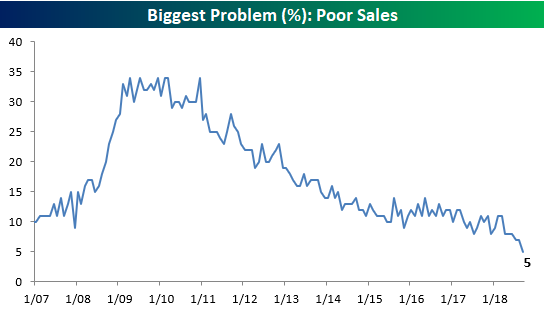

One other issue worth highlighting is the percentage of companies citing Poor Sales as their biggest problem. The percentage of companies citing this issue dropped from an already low level of 7% down to 5%. The last time the percentage was this low for the issue of Poor Sales was in January 1998, and it hasn’t been lower since the early 1980s. That’s a far cry from as recently as eight years ago when the percentage of small businesses citing Poor Sales as their biggest problem was more than six times higher at 34%! When “Poor Sales” are your biggest problem as a small business, your small business is in serious trouble. It will be critical to monitor this reading going forward because it can’t get much lower than this. When “Poor Sales” start to tick higher, it’s highly likely that it will coincide with the end of the current expansion.

Average Small Cap Stock in “Bear Market” Territory

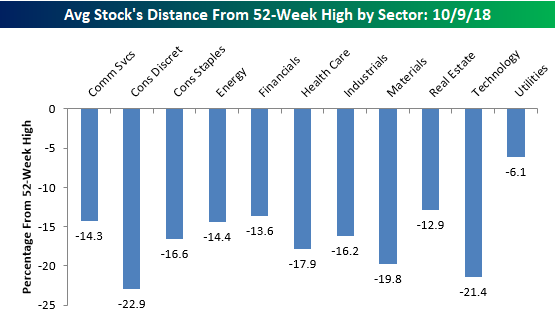

Most people watching have noticed that the recent weakness in equities has been especially tough on the small-cap space, and another illustration of that trend is to look at the distance that stocks are currently trading from their 52-week highs. Within the large-cap S&P 500, the average stock is currently 13.2% below its 52-week high. Moving down the market cap spectrum, though, the numbers get progressively worse. In the S&P 400 mid-cap space, the average spread is 16.9%, while members of the S&P 600 Small Cap index are down an average of 20.7%. Using the standard bear market definition of a 20% decline from a high, the average small-cap stock is in a bear market!

Looking at the spreads between current prices and 52-week highs, stocks in the Consumer Discretionary sector are further from their highs than any other sector (-22.9%), but Technology isn’t far behind at 21.4%. For two sectors that were market leaders, Tech and Discretionary have certainly seen a good deal of profit-taking lately. Outside of these two, other sectors where the ‘average’ stock has seen a pretty sizable pullback from its 52-week high include Materials (-19.8%), Health Care (-17.9%), and Consumer Staples (-16.6%). On the other end of the spectrum, Utilities (-6.1%) is the only sector where stocks are currently down by an average of less than 10% from their 52-week highs.

Chart of the Day: Worst Starts to October for the Nasdaq

Global Equity Sell-Off

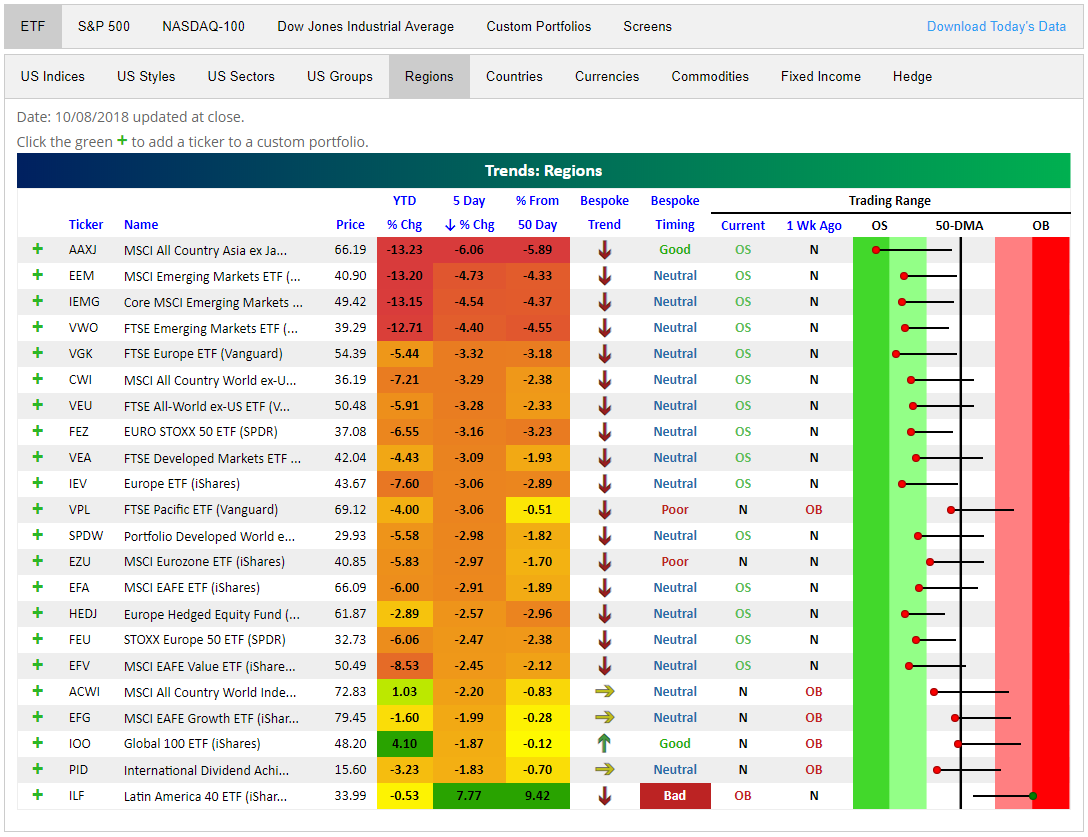

lt’s not exactly news that global markets have been significantly weaker than the US this year. Almost every single international ETF is down year to date; a few of which are down by double digit percentages. Only two have managed to edge out slight gains YTD. The Global 100 (IOO) has seen gains of 4.1% and the MSCI All Country World Index (ACWI) is up 1.03%. Unlike other ETFs in the Regions category of our Trend Analyzer, these two have US exposure that has helped them stay afloat. In the past week though, not even this has been a saving grace; just about every ETF is down well over 1%.

Emerging market ETFs are especially feeling the pain as they have each dropped over 4%. The MSCI All Country Asia excluding Japan (AAXJ) has had the worst performance of all. It has fallen 6.06% in the past 5 days! Looking at the long tails in the Trading Range section of the Trend Analyzer, you can see the large movements below the 50-DMA for most of the ETFs included in this group. This has pushed many deep into oversold territory. All the negativity aside, the Latin America 40 (ILF) has been gaining ground recently with a huge jump up yesterday thanks to Brazilian first round election results. Currently, it is up 7.77% since this time last week. While good, it may be getting overextended. It is the only overbought member of this group sitting 9.42% above its 50-DMA and our Trend Analyzer has given it a bad timing rating based on its extreme overbought reading.

Growth Groups Move to Extreme Oversold

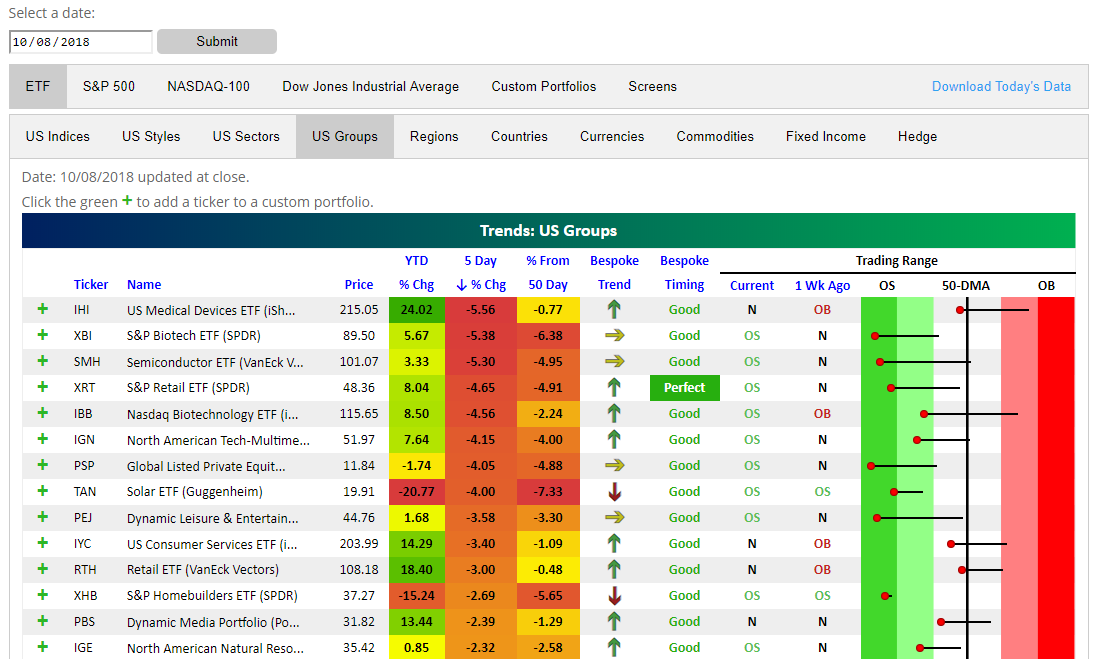

The US has had a rough go of it the past week, which we can explore using our Trend Analyzer. The past few days have seen many indices close lower; namely, the growth groups. Even though many have seen significant gains YTD—US Medical Devices (IHI) is up 24.02% and Retail ETF (RTH) is up 18.4%—in the past week, there has been a rotation out of these names. These groups are plummeting now as the market takes a breather. Even though it is one of the strongest ETFs on the year, IHI has fallen the most over the past 5 days out of all US groups. S&P Biotech (XBI) and the Semiconductor ETF (SMH) are not far behind. All three of these are down over 5% in the past week. Impressive to note though, even falling as much as it did, IHI has not entered its respective oversold territory. Unfortunately, this is not the case with the rest. These large moves since the beginning of October have pushed most growth ETFs deeply oversold.

Investors seem to be rotating into Financials and Energy as well as safe assets like gold and real estate. This comes on the back of rising rates and oil prices over the past week. The S&P Regional Banking (KRE) has had the strongest gains of 2.16% over the past 5 days. Insurance (KIE), Exchanges (IAI), Financial Services (IYG), and Mortgage Real Estate (REM) have each seen gains following news of higher rates. Right behind KRE for the largest gains is Junior Gold Miners (GDXJ) rising 1.75% over the same time. This is one of the worst underperformers on the year as gold has fallen consistently. Gold Miners (GDX) while not seeing as large of gains over the past week is seeing a similar pattern. Fears of what’s around the corner seem to have had investors shift out of growth and into safer assets like gold, while higher rates are making financials more attractive.

Morning Lineup – Growth Shrinks

Futures are trading lower again this morning as rising interest rates and weakness in Europe are keeping a lid on any gains in the US. Worries over earnings are also a concern as we head into earnings season.

Earnings season hasn’t even started, but already we may have one company that will serve as a microcosm for all the concerns that investors have heading into the period. Last night, PPG Industries (PPG) lowered guidance for the quarter citing factors like rising input costs, weaker demand from the auto sector for its paints, softening demand from China due to trade tensions, the stronger dollar hurting foreign demand and weakness in emerging markets. If you were to sum up all of the concerns that investors have that could possibly have a negative impact on company results in Q3, PPG mentioned them!

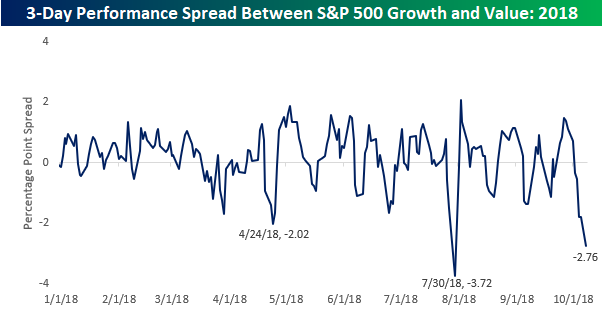

Growth stocks have been taking it on the chin over the last three days, and once again we find ourselves in a situation where they are sharply underperforming value stocks in the short term. Over the last three trading days, the S&P 500 Growth index is underperforming the S&P 500 Value index by over 2.5%. So far this year, this is only the third time that the S&P 500 Growth index has underperformed Value by more than two percentage points over a three trading day period. The last two occurrences were in late April and late July.

This is the third time this year that growth has underperformed value by over 2% in 3 days.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Support, Steepening, Sell Vol, Brazil Beckons — 10/8/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, with economic data nowhere to be seen we focus exclusively on markets with a review of price action (and what it suggests for upcoming returns) in the Stoxx 600, Brazilian real, and VIX futures.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

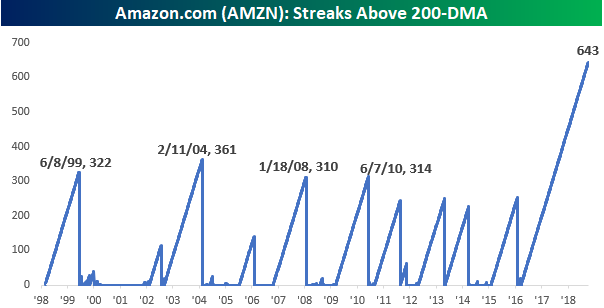

2.5 Years and $570 Billion Ago

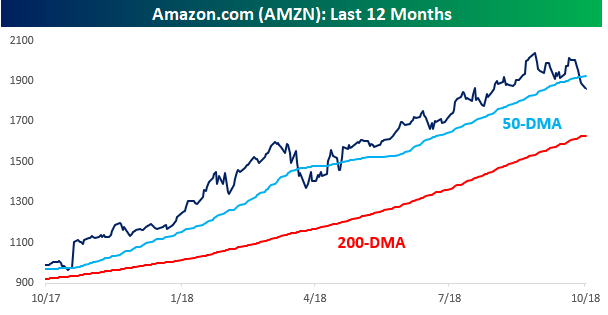

It hasn’t been a good few weeks for Amazon.com (AMZN). After breaching the trillion-dollar market cap level in early September, the stock has been under a fair amount of selling pressure, pulling back about 9% in the span of a month. As a result of this pullback, AMZN recently broke down and closed below its 50-DMA for the first time since late April. While the stock is down 9% from its high, though, it’s still more than 14% above its 200-DMA (1,629).

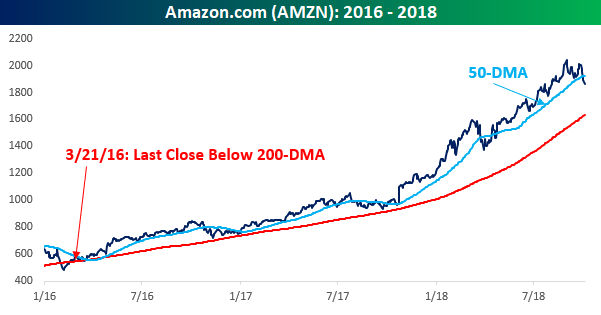

A close below the 200-DMA for AMZN would be something we haven’t seen in quite some time. The last time AMZN closed below its 200-DMA was 643 trading days and $570 billion in market cap ago. That’s right, AMZN hasn’t closed below its 200-DMA in more than two-and-a-half years (March 2016)!

With AMZN still more than 14% above its 200-DMA, its streak of daily closes above the 200-DMA doesn’t appear to be in jeopardy of ending anytime real soon. At 643 trading days and counting, the current streak is already easily the longest in the stock’s history. Since the company’s IPO in the late 1990s, there have only been four prior streaks where AMZN closed above its 200-DMA for more than 300 trading days, and not a single one of those streaks reached the 400 trading day point. In other words, the current streak is more than a year longer than the next closest streak!