2018 Dogs of the Dow

Below is a check-up on the performance of the “Dogs of the Dow” strategy so far in 2018. For those unfamiliar with the strategy, it’s a simple portfolio allocation and re-balance at the start of each year into the 10 highest yielding stocks in the Dow Jones Industrial Average.

As shown in the table, the 2018 Dogs are currently up an average of 4.77% YTD on a total return basis compared to a total return of 5.11% for the 20 non-Dogs. Coming into the month, the non-Dogs were outperforming the Dogs by a much wider margin, however. With investors shifting out of cyclicals and into more defensive names, the lower-yielding non-Dogs have fallen 4.61% in October, while the Dogs are down just 0.61%. If it weren’t for IBM’s 13.91% drop this month due to another bad earnings report, the Dogs would actually be up 87 basis points MTD.

Merck (MRK) and Pfizer (PFE) have been the best performing Dogs of the Dow this year with total returns of more than 25%. Apple (AAPL) and Microsoft (MSFT) have been the best performing non-Dogs with gains of more than 30%.

If we were to re-balance the strategy now, Merck (MRK) would be removed and JP Morgan (JPM) would enter the Dogs. Note that IBM is now the highest yielding stock in the Dow at 4.82%!

Chart of the Day: Homebuilders Keep Falling, Now Down 38% From Highs

Watches and Casinos Point to Global Slowing

The US economy has maintained its robust growth this year but the broader global economy cannot boast the same health. Among many others, indicators like Japanese exports, Swiss exports, and German industrial orders are all either in retreat or decelerating at a significant pace.

On top of these more mainstream releases, there are some more obscure indicators that we like to track as well. These data points have a history of accurately reflecting the cyclical behavior of the global economy. For starters, commodity prices through the Bloomberg Commodity Spot index is up 4.5% YoY (3m average). This is one of its slowest paces since 2016 when energy bottomed. An additional indicator comes out of a casino-heavy resort town in China named Macau. Macau gaming revenue growth has also slowed to its slowest pace since late 2016. This indicates tighter spending by Chinese consumers at the high end of the spectrum. Another indicator is the value of Swiss watch exports. The YoY growth rates for these luxury items are closely linked to the global economic cycle. Swiss watch exports have fallen by 7.7% since peaking in June. One final variable is world trade value in USD. This data point is released at a pretty significant lag, but still shows much of the same story. Fortunately, the global economy is still experiencing growth, but the pace has become increasingly subdued.

Down 15%+ in 15 Days

October is still only a little more than 15 trading days old, but there are already 31 stocks in the S&P 500 that are down over 15% on the month. The table below lists each of those 31 names, and while it’s not uncommon to see volatile stocks from the Technology or Consumer Discretionary sectors topping the list of worst performers during a market decline, not a single one of the ten worst performers so far this month comes from either sector. As shown in the table, the sectors represented in the list of ten worst performers are Industrials, Health Care, and Materials, and the stocks are all down well over 20% already this month!

The worst performing Technology stock on the list is Advanced Micro (AMD), which is down just under 20%, while Newell (NWL) is the worst performing stock from the Consumer Discretionary sector with a decline of 16.4%. Looking at this overall list of names, it’s cyclical stocks which dominate with eight stocks from the Industrials sector alone. Meanwhile, no stocks from the Consumer Staples, Financials, Real Estate, or Utilities sectors made the list. So much weakness in a number of large-cap cyclical stocks has been a big reason why the ratio of cyclicals to defensives has pulled back so far over the last month.

This Week’s Economic Indicators – 10/22/18

Economic data released last week was pretty mixed. Major industrial releases including Empire and Philly Manufacturing as well as Industrial Production all came in better than expected. Housing, on the other hand, continued to leave a lot to be desired. Starts/permits and existing home sales missed, but fortunately, the NAHB sentiment index came in much more positive. Employment data from JOLTS and jobless claims all reaffirmed a very tight labor market.

Turning to this week, economic data will be back-end loaded. Things will start off quiet with only Chicago National Activity and Richmond Fed Manufacturing Indices released today and Tuesday. Things begin to pick up on Wednesday when Mortgage Applications and the FHFA House Price Index will both be released. More housing data will be released later in the day Wednesday with new home sales, which is forecast to see a huge decline. Markit PMIs will also come out Wednesday morning. The Fed Beige Book will round out the day Wednesday afternoon.

Thursday will be the busiest day this week with trade balance data, wholesale and retail inventories, durable goods, and jobless claims all coming out at 8:30 AM. As new home sales are expected to see a major decline the day before, existing home sales are estimated to come in unchanged from last month. Finally, the fourth input of our Five Fed Manufacturing Composite Index comes in with the Kansas City Fed’s Manufacturing Index; the last index (Dallas Fed) will come out the following week.

Preliminary GDP data will finish off the week on Friday. GDP and Personal Consumption are forecasted to fall alongside the GDP Price Index and Core PCE.

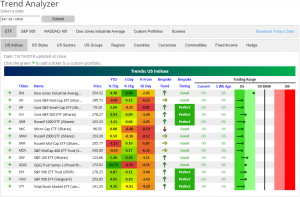

Trend Analyzer – 10/22/18 – Changing Trends

Our Trend Analyzer continues to show weakness for equities after another volatile week last week. Every one of the major US Index ETFs remain oversold. While this is mostly the same as the start of last week, these ETFs are not as extremely oversold as they were. Even though this is a good sign, the Mid-Cap ETFs—IJH, IWR, and MDY—are still sitting lower YTD.

It’s important to note that on a 6-month time frame, five of the members of this group have recently broken their uptrends. Four are trending sideways and the Micro-Cap (IWC) is now in a downtrend. As it currently stands IWC is still positive for the year, but if this downtrend continues, it may not be long before it more closely resembles one of the mid-caps. This simply reflects the greater trend that we have seen over the past month of rotation out of smaller sized companies.

Morning Lineup – Chinese Stocks Surge

China’s biggest stock rally in more than two years has US stocks looking to open higher, and the real strength is in the Nasdaq, where futures are indicating a gain of 0.7%. Economic data is relatively light today, and while there hasn’t been much in the way of earnings reports yet today, the pace will really pick up in the days ahead.

The big gain for Chinese equities overnight is definitely a welcome bullish move from an area of the world that currently keeps investors up at night, but looking back over the last ten years, we would note that 4% moves in Chinese equities haven’t typically come during periods of market strength. The red dots in the chart below show all occurrences of one-day moves of 4% or more for the Shanghai Composite since the start of 2008. While there were exceptions, most of the 32 prior instances came during the downward moves in 2008 and then in 2015.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 10/21/18

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Labor Markets

Strong Economy Draws Women into U.S. Labor Force by Harriet Tory (WSJ)

After peaking north of 77% back at the start of the 2000s, the female prime-age LFPR has started to climb again, more in-line with other global economies than the uncharacteristic declines in the 15 years ending 2015. [Link; paywall]

J.B. Hunt Says 10% Raises Are the Antidote to the Truck-Driver Shortage by Sarah Foster (Bloomberg)

Who would have thought that the anecdote to a worker shortage was to pay a higher price for labor? J.B. Hunt is doing ground-breaking work, apparently! [Link; soft paywall]

Gambling

Mega Millions drawing yields no winners, jackpot swells to $1.6B (AP/NYP)

With no tickets claiming the massive draw on Friday, the multi-state Mega Millions lottery jackpot rose to $1.6bn; the next draw will be on Tuesday. [Link]

2018 Week 7 (Bespoke)

Part of our ongoing series picking NFL games against the spread; so far our picks are 44-38 on the year or 53.7%, which isn’t bad but hopefully will improve with Week 7 action. [Link]

Real Estate

This Small Bank Could Signal Trouble for the Biggest Ones by Stephen Gandel (Bloomberg)

Significant markdowns in the CRE lending portfolio of rapidly-growing Bank OZK (formerly Bank of the Ozarks) suggests the riskier parts of the commercial real estate market could be in trouble. Bank OZK may be familiar; we’d previously mentioned (link) their rapid, aggressive growth strategy in a market that they hadn’t previously been very involved in. [Link; soft paywall]

How Manhattan Became a Rich Ghost Town by Derek Thompson (The Atlantic)

Over 20% of Manhattan real estate is either vacant or set to become vacant, with tens of thousands of retail jobs disappearing in recent years. Surging incomes and real estate prices have made the city a victim of its own success. [Link]

Tech

How Autonomous Vehicles Will Reshape Our World by Samuel I. Schwartz (WSJ)

We’ve previously thrown cold water on the idea that autonomous vehicles will be rapidly introduced and adopted (link) but they are coming eventually. When they do, they will rapidly remake our physical world and economy. [Link; paywall]

Jony Ive on the Apple Watch and Big Tech’s responsibilities by Nicholas Folkes (FT)

An interview with Apple’s chief designer, in the FT’s famed lunch format. Plenty of discussion of high society sprinkled in (also the classic FT style) makes for an entertaining read despite some dark overtones from the man who has shaped Apples devices for years. [Link; paywall]

China

China’s Factory Heartland Braces for Trump’s Big Tariff Hit (Bloomberg)

Exporters aren’t terribly worried about 10% charges, but the possibility of 25% tariffs on Chinese goods looms for companies that send the vast majority of their goods to the United States. [Link; soft paywall, auto-playing video]

With Growth Sagging, China Shifts Back to Socialism by Benn Steil and Benjamin Della (Council on Foreign Relations)

With growth flagging and trade war looming, Chinese strategy has shifted back to squeezing private business in order to support state owned enterprises. [Link]

Government & Taxes

The Cum Ex Files (Cum Ex Files)

A massive investigation of fraudulently obtained tax refunds (for taxes which had never been paid in the first place) in Germany; a very long but incredibly useful read on the genesis and persistence of stolen money from the German state. [Link]

Governments Should Be Run More Like Businesses by Matthew C. Klein (Barron’s)

Forget trying to aim for a balanced budget, it’s the asset and liability accounting of governments that need to be updated to the most basic private sector practice, in the eyes of Matthew Klein. [Link; paywall]

Why a Private Landowner Is Fighting to Keep the Homeless on His Property by Mitch Smith (NYT)

An Akron property owner wanted to give homeless neighbors a place to pitch a tent, but the city has ordered the organized, self-regulating encampment torn down for zoning violations. [Link; soft paywall]

Personal Exploits

Daniel Sickles by George Pearkes (Thread Reader)

A biography of one of the most dubious characters of the Union Army, New York City’s Daniel Sickles. Machine politics, an underage bride, getting away with murder, Gettysburg, a Medal of Honor, and a leg in a box mailed to a museum; quite a story from Bespoke’s Macro Strategist and occasional history dabbler. [Link]

Original Big Bird, Caroll Spinney, Leaves ‘Sesame Street’ After Nearly 50 Years by Dave Itzkoff (NYT)

The man who has played Big Bird on Sesame Street since 1969 is retiring after almost 5 decades bringing joy to children across the country and around the world. [Link; soft paywall]

Industry Analysis

Lithium miners’ dispute reveals water worries in Chile’s Atacama desert by Dave Sherwood (Reuters)

Mineral-rich brine from the Atacama salt flats in Chile is the most available source of lithium in the world, and one of the operators in the area may be over-drawing its allocation of the valuable and rare resource. [Link]

How 2 Upstart Retailers Want to Reinvent the Traditional Department Store by Michelle Cheng (Inc)

A new concept features rotating online brands, event space, and restaurants to being a new model to the department store retail space. [Link]

Stocks

Goldman says the sell-off is just about over and tells investors to get back into growth stocks by Jeff Cox (CNBC)

GS equity strategist David Kostin thought the bottom was in for growth stocks back on Monday, a call that looked good for about 24 hours but has some room for skepticism later in the week. [Link]

U.S. SEC mulls consultation on easing quarterly reporting rules by Katanga Johnson (Yahoo!/Reuters)

Slower reporting cycles may be in the pipeline for smaller firms, though the SEC notes larger firms aren’t going to avoid quarterly filings anytime soon. [Link]

Weird News

Divers swim through 90 feet of raw sewage to unclog giant, hairy ‘fatberg’ by Joshua Rhett Miller (NYP)

A clog featuring thousands of baby wipes, a baseball (?) and a large piece of metal (???) was causing trouble for pumps in Charleston, SC. Divers ended up swimming through 90 feet of raw sewage to extract the mess. [Link]

Read Bespoke’s most actionable market research by starting a two-week free trial today! Get started here.

Have a great Sunday!

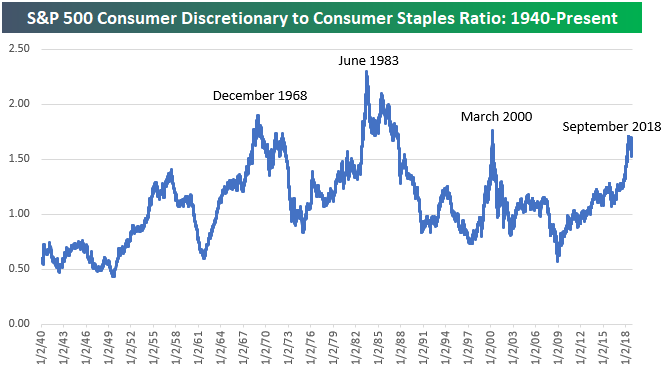

Have Cyclical/Defensive Ratios Peaked?

Below is an updated look at the price ratio between the S&P 500 Consumer Discretionary and Consumer Staples sectors. When the line is rising, Discretionary is outperforming Staples, and vice versa when the line is falling.

Prior to late September, the ratio had been skyrocketing as investors plowed into Consumer Discretionary and avoided the low-growth, defensive Consumer Staples sector. Over the last month, however, we’ve seen a big rotation out of Discretionary and into Staples.

With the Staples sector rallying recently and Discretionary falling, the ratio has suffered a big drop. The last time this ratio peaked was back in March 2000 at the end of the Dot Com bull market.

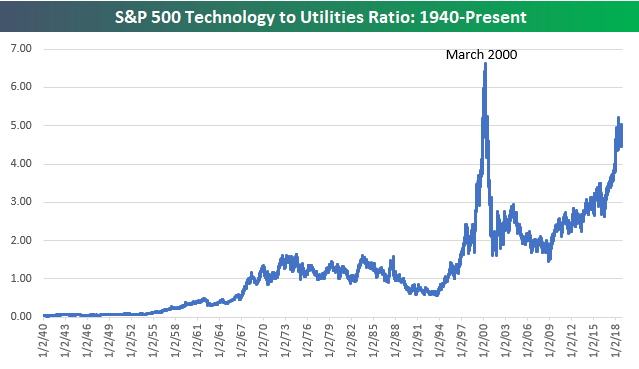

The ratio between Technology and Utilities had also been soaring over the last year or so as the Tech sector took off. While the ratio hasn’t quite gotten to the levels seen at the end of the Dot Com boom in March 2000, it’s still extremely elevated relative to all other periods over the last 65+ years. Back in early 2009, the ratio was at 1.5. It recently crossed above 5 at its peak a few weeks ago. This month we’ve seen Utilities rally and Tech fall sharply, which has caused the ratio between the two to dip a bit. If a peak has been put in, however, it has a long way to fall.

2018 Week 7

Week 6 Results: 7-6, Overall: 44-38 (53.7%)

Outside of financial markets, we’re also sports fans here at Bespoke. With new legal sports betting avenues now available across the US, we figured we’d have some fun and pick each NFL game versus the spread this season (as of Saturday evening). Let’s see how we do…on to Week 7.

We were 7-6 in week 6, bringing our overall record through 6 weeks to 44-38 (53.7%).

2018 NFL Week 7 Bespoke Picks:

Tennessee at LA Chargers (-7): Tennessee +7

New England (-3) at Chicago: Chicago +3

Buffalo at Indianapolis (-7.5): Indianapolis -7.5

Detroit (-3) at Miami: Miami +3

Minnesota (-3.5) at NY Jets: Minnesota -3.5

Carolina at Philadelphia (-4.5): Carolina +4.5

Cleveland at Tampa Bay (-3.5): Cleveland +3.5

Houston at Jacksonville (-4): Houston +4

New Orleans at Baltimore (-2.5): New Orleans +2.5

LA Rams (-9.5) at San Francisco: LA Rams -9.5

Dallas at Washington (Even): Washington Even

Cincinnati at Kansas City (-6): Kansas City -6

NY Giants at Atlanta (-4): NY Giants +4

2018 NFL Week 6 Bespoke Results:

Tampa Bay at Atlanta (-3): Tampa Bay +3 Loss

Pittsburgh at Cincinnati (-1.5): Pittsburgh +1.5 Win

LA Chargers at Cleveland (-1): LA Chargers +1 Win

Seattle (-2.5) at Oakland: Oakland +2.5 Loss

Chicago (-4) at Miami: Miami +4 Win

Arizona at Minnesota (-10): Minnesota -10 Push

Indianapolis at NY Jets (-1): Indianapolis +1 Loss

Carolina (-1) at Washington: Washington +1 Win

Buffalo at Houston (-11): Buffalo +11 Win

LA Rams (-7.5) at Denver: LA Rams -7.5 Loss

Jacksonville (-3) at Dallas: Dallas +3 Win

Baltimore (-2.5) at Tennessee: Tennessee +2.5 Loss

Kansas City at New England (-3.5): Kansas City +3.5 Win

San Francisco at Green Bay (-9.5): Green Bay -9.5 Loss