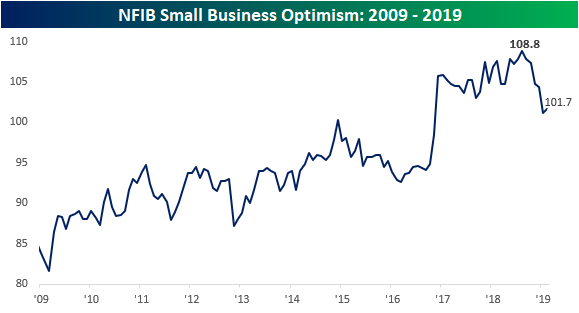

Small Business Rebounds Less Than Expected

After the steepest five month decline since the Financial Crisis and the longest monthly losing streak since 1998, NFIB Small Business Confidence rebounded in February, although by a less than anticipated degree. While economists were expecting the headline index to bounce from 101.2 up to 102.5, the actual increase was much smaller at just 101.7. As shown in the chart below, while the index was higher this month, it hasn’t put anything more than a small dent into the decline we saw from the high back in August of last year.

From a longer term perspective, the recent decline from the August 2018 high is definitely severe relative to prior declines. What we noted following last month’s report and is worth reiterating again is that prior periods where we have seen a quick and fast drop in small business sentiment haven’t been particularly good at timing downturns in the business cycle. While recessions typically are accompanied by a sharp downturn in business sentiment, there have also been plenty of other periods (1984, 1993, and 2005) where we saw sharp declines in small business sentiment but were nowhere near the onset of a recession.

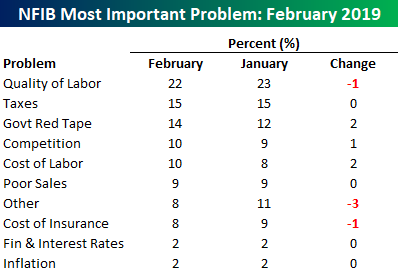

Finally, when it comes to issues facing small businesses, finding qualified employees continues to be the biggest problem they face, and there are some signs that they are starting to pay up in order to find those with the right qualifications. In this month’s survey, the percentage of businesses citing Labor Costs as the biggest problem increased from 8% to 10%.

Morning Lineup – Brexit and Boeing

Today’s Morning Lineup is brought to you by the letter “B” as Brexit and Boeing are the major drivers of headlines this morning. Regarding Brexit, while things looked promising ahead of today’s vote after last night’s deal between PM May and EU President Juncker, reality has set in overnight, and the prospects of the deal passing a vote in Parliament aren’t looking entirely promising at this point. Meanwhile, Australia and Singapore joined the growing list of countries grounding flights of the 737 Max, and just now Malaysia announced the same. While the FAA deemed the 737 Max airworthy overnight, it also sent a mixed message mandating Boeing to push certain changes to the 737’s flight control system by ‘no later’ than April.

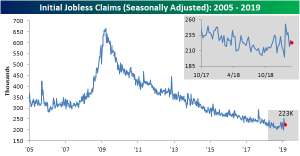

In economic news, the NFIB Small Business Optimism Survey increased versus January but came in lighter than expected, while CPI was right in line with forecasts at both the headline and core levels.

Please click the link below to read today’s Bespoke Morning Lineup.

Bespoke Morning Lineup – 3/12/19

Software has been a key group for the market over the last year, and yesterday’s rally took the S&P 500 Software group back within 1% of an all-time high. On Friday, the index bounced right at what was former resistance levels which was an encouraging sign. This group is dominated by Microsoft (MSFT) but is also comprised of Oracle (ORCL) Adobe (ADBE), and salesforce.com (CRM). Watch this group in the coming days to see if it can lead the broader market higher.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Technicals, Big Mondays, and Analyst Sentiment — 3/11/19

Log-in here if you’re a member with access to the Closer.

The S&P 500 managed to re-take its 200-day moving average today after just one day below it, and this sets the stage for a fourth test of resistance at 2,818 in the coming days/weeks. In tonight’s Closer sent to Bespoke Institutional clients, we take a look at Monday gains of 1%+ for the S&P 500 over the last ten years and whether the upside momentum to start the week typically continues for the remainder of the week. We also provide a big update on analyst Buy, Sell, and Hold ratings and how analyst sentiment has changed since the S&P peaked nearly six months ago on September 21st.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Market Shakes off Boeing

Trend Analyzer – 3/11/19 – YTD Gains Take A Hit

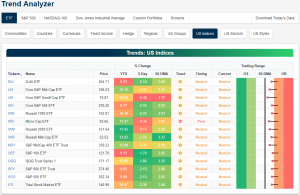

Whereas we began last week with every major index ETF firmly overbought—albeit less than the previous weeks—today, every one of these ETFs are sitting in neutral territory. This comes as each of these have seen significant declines since last Monday’s open. Small caps got hit the hardest with the Core S&P Small-Cap (IJR) falling the most at 4.49%. The other small caps, Micro-Cap (IWC) and Russell 2000 (IWM), also saw declines exceeding 4%. Also worth mentioning, with these declines, IWC has yet to have moved out of its downtrend despite every one of its peers now trending sideways. Meanwhile, the large-cap S&P 100 (OEF) fell only 1.76% last week. With this recent sell-off putting the 2019 rally on hold, it has also dragged down YTD gains. Previously, each major index ETF had seen double-digit returns on a year to date basis, but now, there are only nine exceeding 10%.

Morning Lineup – Boeing Bites Both Ways

As great as things were for the DJIA when Boeing (BA), with its high price and weighting in the index, was on the way up, today the DJIA is feeling the pain of what happens when a high priced (weighted) stock in the index declines. With shares of Boeing set to open down over 10% this morning, its decline is set to have a negative impact of around 250 points (or 1%) at the open. Outside of BA, US equities are generally indicated higher following the lead of both positive starts to the week in Asia and Europe.

Please click the link below to read today’s Bespoke Morning Lineup.

Bespoke Morning Lineup – 3/11/19

As mentioned in today’s Morning Lineup, both China and European equities bounced this morning right at short term support from a brief late February consolidation. The S&P 500, meanwhile, finished off last week below its 200-DMA for the second straight day. While in a bit of a tougher hole than its international counterparts, the S&P 500 is also right at a potential support area from a period of consolidation in early February. Friday’s rebound off the early lows was a positive sign, and if equities can follow through today, it might just be enough to finally break out of the congestion area around the 2,800 level.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 3/10/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Mercenaries

Coinbase Cuts Ties With Hacking Team Following Spyware Backlash by Nour Al Ali (Bloomberg)

A recent purchase of a security company by cryptocurrency giant Coinbase is coming under fire after revelations that staff included in the acquisition had been involved in selling spyware to oppressive regimes. [Link; soft paywall]

WWF Funds Guards Who Have Tortured And Killed People by Tom Warren and Katie J. M. Baker (BuzzFeed)

In part of its war on poachers, the World Wide Fund is allegedly paying mercenaries to protect wildlife. Those same guards have allegedly engaged in torture and murder. [Link]

Ouch

A Hedge Fund Steps Into Nigeria’s $9 Billion Corporate Dispute by Joe Light (Bloomberg)

A tiny natural gas company was offered concessions in Nigeria, but the deal fell through. Now, a hedge fund is seeking to collect, to the tune of 2.5% of the country’s GDP. [Link; soft paywall]

The American With the Toughest Job in Finance: Saving Deutsche Bank by Jenny Strasburg (WSJ)

Private equity giant Cerberus has been called in to help Deutsche Bank navigate the collapse of its business and explore a potential sale. [Link; paywall]

Chinese Stocks Plunge and It All Started With a Single Downgrade (Bloomberg)

This week the onshore Chinese equity market collapsed in part thanks to an aggressive sell call on People’s Insurance Company of China, in a move many think was sparked by regulator approval of the bearishness. [Link; auto-playing video, soft paywall]

Economics

Who’s Really to Blame for America’s Trade Deficit by Matthew C. Klein (Barron’s)

What drives the trade balance? Klein argues convincingly that foreign economic choices are washing up on US shores just as much as domestic economic policy has driven trade balances. [Link; paywall]

Kelton And Krugman On IS-LM And MMT by Jo Mitchell (Critical Macro)

An informed recap of a recent exchange over modern monetary theory in the pages of the New York Times and Bloomberg. [Link]

Regulation

SEC Chief Wants Smaller Investors to Have Better, Faster Stock Data by Gabriel T. Rubin and Alexander Osipovich (WSJ)

A new SEC proposal seeks to level the playing field for smaller investors, who are currently stuck in the slow lane when it comes to stock market pricing. [Link; paywall]

Wall Street Votes to Support Single Bond for Fannie, Freddie by Andrew Ackerman and Ben Eisen (WSJ)

This week SIFMA endorsed a proposal to combine the market for mortgage-backed securities issued but Fannie Mae and Freddie Mac. [Link; paywall]

Presidential Munching

Dining at Mount Vernon by Mary V. Thompson (mountvernon.org)

Every curious what the first President ate? This quick post recaps the recorded history of what was served on the table at Mount Vernon when Washington was shepherding the early republic. [Link]

Payments

Philadelphia Is First U.S. City to Ban Cashless Stores by Scott Calvert (WSJ)

As stores have shifted away from cash (improving wait times), some regulators have stepped in to require cash payments be accepted; that’s an interesting wrinkle of state/local enforcement of the importance of settling “all debts, public or private”. [Link; paywall]

Streaming

AT&T Is Dragging HBO’s Streaming Strategy Out of the Dark Ages by Felix Gillette (Bloomberg)

HBO is on the cutting edge of content production, but its streaming strategy has long lagged behind competitors. That may be changing. [Link; soft paywall]

Health Care

GoFundMe CEO: ‘Gigantic Gaps’ In Health System Showing Up In Crowdfunding by Rachel Bluth (KHN)

An interview with the CEO of GoFundMe reveals the huge discomfort he and the rest of the company feel with regards to the massive waves of fundraising being done to meet health care costs. [Link]

Farewells

Take Them to the River by Phoebe Zerwick (The Bitter Southerner)

The touching inside story of New Orleans krewes which meet, year after year, and often carrying former members’ ashes to the Mississippi for scattering. [Link]

Sports

For Many Girls, Figure Skating Loses Its Edge to Hockey by Anne Marie Chaker (WSJ)

Once steered into figure skating, many young girls are seeing pad appeal, trading sequined dresses for helmets and gloves. [Link; paywall]

Special Effects

Buyer Beware: Hollywood Special Effects Now Permeate Property Listings by Ryan Dezember (WSJ)

In order to drum up interest in listings, home sellers are going as far as removing walls, changing flooring, and adding swimming pools to get buyers interested in their listings. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Closer: End of Week Charts — 3/8/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

The Bespoke Report — The KISS Market

Global equity markets had a rough week, but the US staged a nice intraday rally on Friday after an NFP-driven gap lower. Global economic data has been rough, but there are reasons for optimism. In this week’s Bespoke Report, we talk about earnings, smart money flows, retail flows, economic data, and upticks in US data we’ve seen since last Friday. For the S&P 500, the technical line in the sand is 2,816, while 10 year yields are desperately clinging to 2.61% support that has held for the past few months.

Along with in-depth earnings season coverage, we review what’s been happening in markets around the world from equities to commodities to credit. We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Despite An Uptick, Debt Growth Remains Slow Versus History

Yesterday the Federal Reserve updated quarterly sector debt levels for the US economy in its Z.1 Flow of Funds report. We discussed the full report in greater detail in The Closer last night, but we want to highlight a key observation. Below we show the YoY growth of debt for the United States by major sector. Each sub category sums to the total 4.49% YoY growth in debt.

While debt has been growing – and at a generally accelerating pace – since bottoming out in 2011, it’s been doing so at a pace much slower than anything seen since the 1950s. Even though Q4 2018 saw debt grow at the second-fastest YoY pace of the post-crisis period, only one quarter since 1951 saw debt grow at a slower pace than current. While government debt has grown relatively quickly in the post-crisis period, almost all other sectors have seen much slower contributions to total debt growth than has been typical historically. Corporate debt has been the exception, though even that sector has seen debt growth at the low end of the historical norm. State and local governments, households, and the financial sector have all seen extremely slow debt growth.