Morning Lineup – Rising Tide on Both Sides of the Atlantic

Please click the link below to read today’s Bespoke Morning Lineup.

Bespoke Morning Lineup – 3/19/19

With the S&P 500 down just over 3% from its all-time high and tomorrow marking the six-month anniversary since the last time the index closed at an all-time high, the current period is just the fifth time since the March 2009 low that the index has gone six months or more without closing at post-financial crisis high. It also marks just the sixth time that the index has gone more than 100 trading days without hitting a new high.

In the chart below, we highlight the S&P 500’s path since the March 2009 lows and show each of the 100+ trading day droughts without a new high in red. The current period, which will extend to 122 trading days today, has been unique as it came just 19 trading days after a 145 trading day drought that spanned late January to August of 2018. When the S&P 500 finally broke out to new highs last August, bulls were probably not expecting such a ‘lame’ breakout as the difference between the September high and the high from earlier in January was barely more than 2%. The only period that was similar was from 2011 through 2012 where a 206 trading day streak without a new high and a 108-day streak were separated by just 22 trading days and a rally of less than 4%.

Those two examples just mentioned are where the S&P 500 saw the smallest rallies following a drought of 100+ trading days without a new high. The other three periods, however, were a lot more palatable for bulls as the S&P 500 rallied an additional 12% through May 2011 after breaking the 135-day drought in November 2010, an additional 50% through May 2015 after breaking the 108-day drought in September 2012, and an additional 33% through January 2018 after breaking the 285 trading day drought in July 2016.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Resistance in the Rearview — 3/18/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, with the 2,816 resistance level now behind us we evaluate how much higher the S&P 500 can run given catalysts like overbought/oversold levels, the VIX, and valuations. Next, we look at last week’s release of Chinese credit creation which came in at the slowest pace in years. We then provide a quick update on Brexit before finishing with one of the few US data points today: Cass Freight Volumes and Costs

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Financials Looking Attractive

As we briefly noted in last week’s Sector Snapshot, the Financial sector has been making a series of higher highs and higher lows, making it attractive from a technical perspective. Additionally, it is just barely overbought as of today, and it also has the lowest P/E ratio of all sectors. While the sector ETF (XLF) is still working its way to new highs after recently pulling back in the first weeks of March, a number of stocks within the sector are breaking out to new 2019 highs or above levels last seen before the late 2018 sell-off. Taken from our Chart Scanner, we show the charts of some of these stocks below.

Across the sector, there are several opportunities with a variety of financials from FinTech to Banks. To highlight a few, American International (AIG) has tested resistance near $44 multiple times since falling off a cliff last October. Though not there yet, a push above these levels could pose as a bullish sign for the stock. Discover Financial Services (DFS) and FactSet (FDS) both have similar patterns since the market found a bottom on Christmas Eve. Both stocks have gone on extremely strong runs so far in 2019 and after recently pulling back, the stocks have caught their breath and are once again pushing higher. While FactSet is reaching 52-week highs, DFS still has room to run to highs from 2018. The big banks are also looking constructive. Whereas Citigroup (C), Goldman Sachs (GS), and JP Morgan (JPM) have all been more or less meandering sideways for the past few weeks, today they have managed to distinctively break out above their recent ranges. In the case of Citi and JPM, both have found support at the 50-DMA before moving higher. Even stocks that have been in long term downtrends like KeyCorp (KEY) or Invesco (IVZ) have seen such strength that the downtrends have been broken. To add to the attractive technical setup, these stocks both have come back to retest this downtrend line having since bounced off and moving higher.

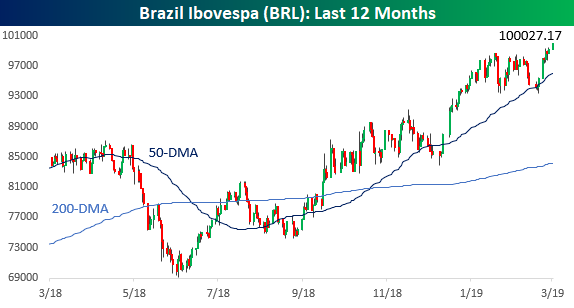

Record High But Still Down Over 40%

We’re not sure if they’re throwing around “Ibovespa 100K” hats on the floor of the Sao Paulo stock exchange, but Brazil’s benchmark Ibovespa equity index just topped the 100,000 level for the first time in its history. The latest breakout in Brazilian stocks comes after a two-month period of sideways trading that followed a gain of over 40% from the lows last Summer.

The rally in Brazilian stocks and the new high in the Ibovespa are impressive, but at the same time a bit misleading. Brazilian equities may be at record highs, but for a US investor invested in Brazil, things don’t look nearly as impressive. The chart below shows the Ibovespa index going back to 2006 priced in US dollars. From the perspective of a US investor, Brazilian stocks are still up over 40% from their lows last Summer, but even after that move they are still down 41% from their highs way back in May 2008.

Chart of the Day: Monday Market Mania in China

Homebuilder Sentiment Unchanged

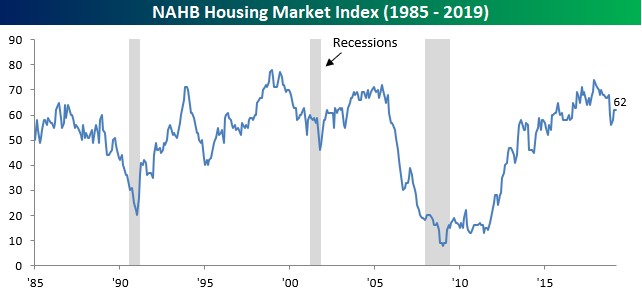

Economic data kicked off the week on a mixed note Monday as Homebuilder Sentiment for the month of March was unchanged versus February, even as expectations were for a small improvement. According to the National Association of Homebuilders (NAHB), the general sentiment index was unchanged at 62 versus consensus forecasts for an increase to 63. While sentiment has been stable after improving in December and January, it remains well off of its highs from late 2017.

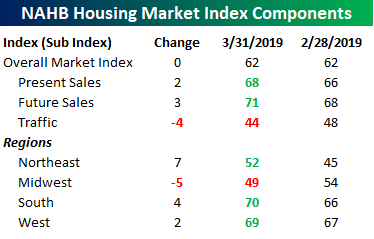

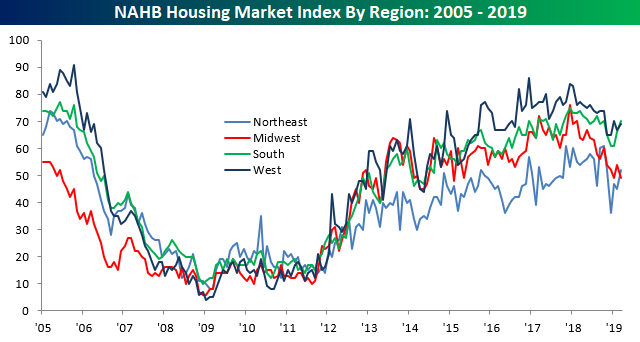

Breaking out the details of the report, most of the report’s subcomponents saw m/m increases. While Traffic was down, both Present and Future Sales showed improvement. On a regional basis, sentiment in the Midwest was down pretty sharply falling from 54 to 49 (indicative of contraction), but homebuilders in every other region of the country were more optimistic. Interestingly, while sentiment in the Northeast was consistently the weakest from 2012 through mid-2018, more recently, the Midwest has been giving the Northeast a run for its money. The Northeast has actually seen a nice pickup in sentiment off of multi-year lows seen a few months ago.

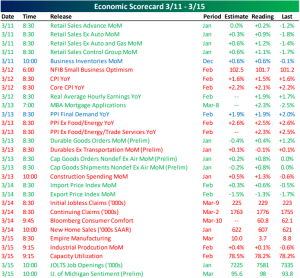

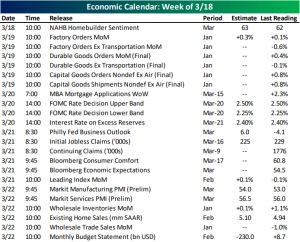

This Week’s Economic Indicators – 3/18/19

Last week was fairly busy in economic data with 31 releases spaced throughout the week; most of which came in weaker. Monday’s Retail Sales report for January offered some relief (but also confusion) from the awful December print. While January’s readings showed growth, the already bad readings from December were revised even lower. CPI data on Tuesday showed lower increases than January and came in lower than expected with the headline and core measures rising only 1.5% and 2.1%, respectively. Further in inflation data, on Tuesday Core PPI also missed estimates, though, it was in line with expectations. Friday was a rough day for industrial data as Industrial Production missed estimates, and Empire Manufacturing fell even as expectations called for an increase.

Turning to this week, it will be slightly less busy with only 23 releases compared to last week’s 31. Leading off was NAHB Homebuilder Sentiment which missed expectations coming in unchanged from last month. After Factory Orders tomorrow, there will be an FOMC rate decision on Wednesday, though, no one is expecting a change in rates. Thursday and Friday will have some big releases with the Philly Fed’s Business Outlook, Leading Indicators, preliminary Markit Manufacturing and Service PMIs, and the Budget Statement.

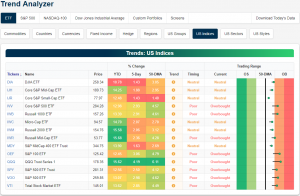

Trend Analyzer – 3/18/19 – Push Towards Overbought

Coming off of last week’s strong gains, the major index ETFs are mostly overbought headed into the new week with eight firmly overbought while the remaining six are still neutral. Those that are overbought are predominantly large caps, though, the Dow (DIA) is actually still neutral and tied with the Core S&P Small Cap ETF (IJR) for the least gains last week at only 1.43%. No doubt this comes as a result of the wild fluctuations in Boeing (BA). While no other small-cap performed as poorly as IJR last week, small and mid-caps have underperformed recently. Despite weaker gains in the past few weeks, since the start of 2019 this group has still treated investors well. While on this topic, the Nasdaq (QQQ), which rose 4.19% last week, has also become one of the best performers year to date. The rapid increase over the past week also leaves the ETF the most extended above its 50-DMA and the most overbought.

On a sector level, the tech-heavy Nasdaq’s rapid rise last week can be credited to the Technology Sector’s (XLK) strength in the past week as the ETF rose 4.56%, making it the most overbought and the furthest above the 50-DMA. Outside of Industrials (XLI) again due to Boeing, every sector has seen a significant push towards overbought levels in the past week. Namely, the Health Care Sector (XLV) has risen from right at the 50-DMA to just under one standard deviation above today.

Morning Lineup – Upward Drift Continues

Not a lot in the way of macro headlines this morning, but US equity futures are modestly higher, although continued weakness in Boeing (BA) is pressuring the DJIA. Chinese equities kicked off the week with another rally of over 2%, sending the CSI 300 to its highest close of the current rally. In the ongoing China-US trade saga, a potential summit between Trump and Xi is looking like it will be pushed back to June.

Please click the link below to read today’s Bespoke Morning Lineup.

Bespoke Morning Lineup – 3/18/19

February trade data for Singapore had good news for optimists on global activity. While both leading indicators and broad gauges of global trade activity have been in pretty persistent decline of late, we note that exports for Singapore (both from its domestic economy, and via broader measures like re-exports and container volumes, both of which are highly sensitive to global trade activity) have not suffered all that much. Certainly, exports are down, and re-exports are off their peak, but container through-put for the biggest Eurasian trade hub has remained very robust, something that would be impossible if total global trade was collapsing.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Bespoke Report – Break Out the Monocle

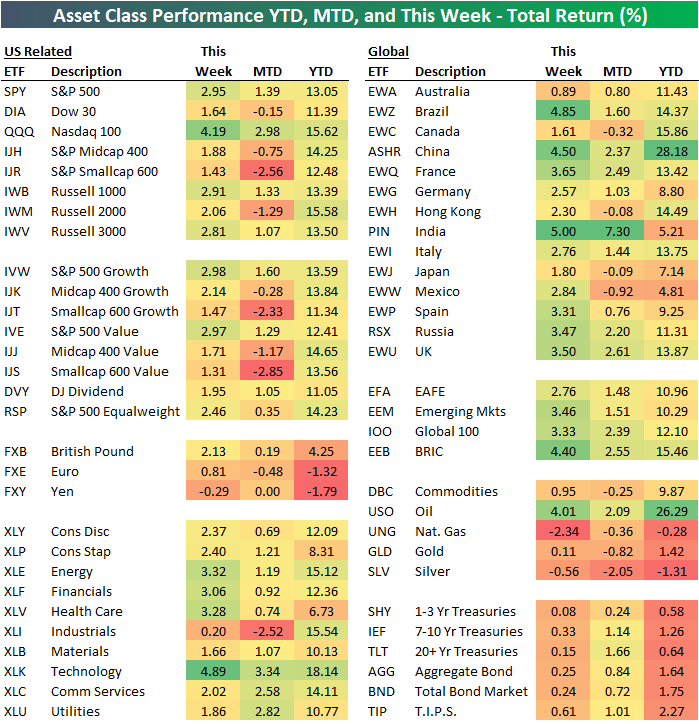

Below is an updated look at our ETF Asset Class Performance Matrix, which shows the total returns of key ETFs across assets classes on both a YTD, MTD basis as well as over the last week. How strong were global equity markets this week? Well of all the equity-related ETFs in the matrix, not a single one finished the week in the red. Even Industrials (XLI), which were dragged down by Boeing (BA), managed to eke out a gain of 0.2%. Among US indices, the Nasdaq 100 blew away the field rallying over 4%, but every other US index ETF was up over 1.4%. International markets were even stronger with India (PIN), Brazil (EWZ), and China (ASHR) all rallying more than 4%. Rounding out the four names from BRIC, Russia (RSX) even rallied 3.5%. In terms of YTD leaders, China and Crude oil are neck and neck for the top spot with gains of 25%+.

Along with a recap of all of this week’s economic data and major market events, we also provide an updated take on our market view. We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!