B.I.G. Tips – Sector Performance Following Initial Inversion of Yield Curve

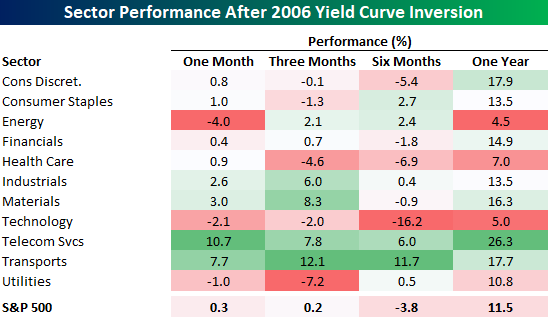

In our latest B.I.G Tips report, we detail and summarize sector performance following periods where the yield curve first inverts after two-years or more of not being inverted. One of the periods we looked at was the most recent period prior to last week, which was back in 2006. The 2006 inversion was followed by mixed market returns. One month later, the S&P 500 was essentially flat with Telecom Services and Transports leading the way higher as Energy and Utilities both declined. Three and six months later, the S&P 500 saw similarly mixed returns, but one year later, the S&P 500 was up over 11% and every sector was up at least 4.5%. The party ended shortly thereafter, however, as the Global Financial Crisis took hold in late 2007 through early 2009.

To gain access to the full report which contains more of the same analysis for each of the periods where we saw similar inversions after at least two years without an inversion, please start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

Fixed Income Weekly – 3/27/19

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we review the shocking rally in short-term rates over the last few weeks.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Chart of the Day: Smart Money Shifts Negative?

B.I.G. Tips: Recession Odds

What are the odds of a recession coming at some point in the next three years?

In order to more precisely quantify recession risks, we took four economic indicators related to the labor market (the Conference Board’s Current Situation indicator, the Jobs Hard to Get—Jobs Plentiful spread, the unemployment rate, and the 6m rate of change in each month’s initial jobless claims average) and four rates market indicators (the 3m5y curve, the 3m10y curve, the 5y30y curve, and the real Fed Funds rate) and ran probit regressions against the binary condition “did a recession start at some point over the next X years.”

A probit regression is very similar to linear regression, but instead of continuous variables, the regression is run against a binary data point. The result is a probability of a binary outcome based on continuous inputs; given a certain set of data points, what are the odds we enter recession? We note that for the real Fed Funds and unemployment rates, we use February data for March; all other variables are either March or March-to-date.

To read our findings, start a two-week free trial to Bespoke Premium or Bespoke Institutional. Then come back to this post.

Bespoke’s Global Macro Dashboard — 3/27/19

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

Morning Lineup – More Inversion

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

The global frenzy for yield continues this morning as Mario Draghi made dovish comments suggesting more easing measures likely to come from the ECB in response to recent weakness in the economic headlines. US Treasuries are rallying again this morning, sending the yield on the 10-year to 2.38% and pushing the yield curve further into inverted territory at negative 6 basis points on the 10y/3m curve. In corporate news, Southwest Airlines (LUV) lowered guidance citing the grounding of the 737 MAX and adverse weather conditions. On a more positive note, both KB Homes (KBH) and Lennar (LEN) are trading up over 2.5% after reporting earnings.

Please click the link below to read today’s Bespoke Morning Lineup.

The chart below is from the second page of our Morning Lineup and shows where S&P 500 sectors are trading with respect to their trading ranges. For each sector, the circle represents where it is now, while the tail indicates where the sector was trading a week ago. In the chart, light red or green shading represents overbought or oversold readings (>1 standard deviation above or below 50-DMA), while dark red and dark green shading indicate extreme overbought or oversold readings (>2 standard deviations above or below 50-DMA).

Looking at the chart, can you tell which one isn’t like the others? While the S&P 500 and most sectors remain at short-term overbought levels, Financials have been hit hard and is not only the only sector trading below its 50-DMA, but it is also the only oversold sector. Keep in mind also, that this reading comes after yesterday’s rally where the sector handily outperformed the S&P 500 gaining over 1%. If there is one sector where the pain of an inverted yield curve was immediately felt, it was in the Financials!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Doji City, Recession Odds, California Crushed — 3/26/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a note on the S&P 500’s price action after two straight days with a doji candlestick pattern. Turning to rates, we discuss where the 10-year Treasury yield should be given its relationship to crude oil, and the prospects of the 2-year after today’s impressive auction. Following up on today’s Chart of the Day, we provide some probit regressions to show the odds of a recession in the next few years given a number of variables. Next, with the addition of the Dallas and Richmond Feds’ indices, we provide an updated look at our Five Fed Manufacturing Composite which is now showing some improvements. We finish with today’s housing starts release which missed by a wide margin (though permits were stronger) partially thanks to weather conditions on the west coast.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

No Congestion for Gas Prices

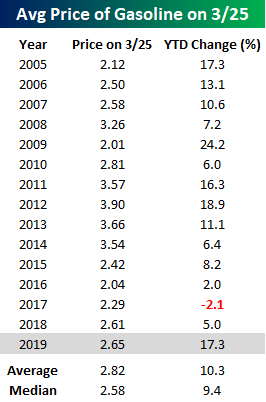

The road higher for gas prices has been as clear as can be of late as prices have been on a tear. According to AAA, the national average price of a gallon of gas has risen 17.3% YTD through 3/25. That’s a full seven percentage points above the average YTD gain for this time of year and the largest YTD increase through 3/25 since 2012. Even after the gains, though, the average price is only four cents higher now than it was a year ago. What’s ironic about this year’s gains in prices is that they are coming at a time when inflation is just about the last worry on anyone’s mind.

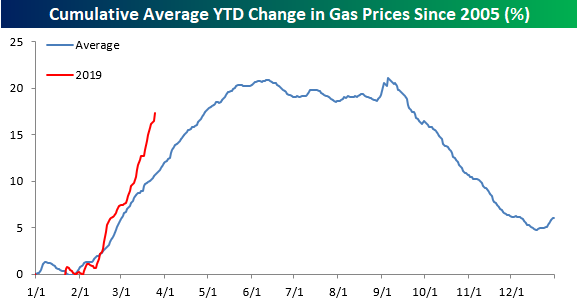

The chart below compares the change in gas prices this year to an annual composite chart of prices going back to 2005. While prices are higher this year, and the move has been much larger than normal, we would note that prices typically rise at this time of year. They also typically continue to rise right up until Memorial Day when the summer driving season kicks off. For most of the summer, prices then plateau and then start to rapidly decline heading into year-end.

One reason behind the much larger than average increase in gas prices this year is that lately, prices have barely gone down- not even for a day here and there. Check out the chart below. Over the last 42 calendar days, the national average price of gasoline hasn’t declined once. Going back to 2004, there have only been two other streaks that are longer (2009 and 2011), and if prices don’t decline today or tomorrow, the current streak will move into a tie for second.

Maximum Frustration

Make up your mind already! That’s the way traders are feeling towards the market these days. Whether you are a bull or bear, it’s hard not to be frustrated with how the equity market trades lately with its complete lack of decisiveness. After repeated attempts at breaking through 2,800 in the fourth quarter, the S&P 500 attempted to break through that level once again in late February but stalled right at resistance. Then, in the first full week of March, it seemed as though another roll-over was in store as the S&P 500 saw five straight days of declines taking the index back below its 200-DMA (light red shaded box in chart). Negative sentiment peaked on Friday, March 8th when the much weaker than expected Non-Farm Payrolls report set the stage for a negative open to close out the week.

The weak open on 3/8 proved to be the low point of that sell-off, and in the following week the S&P 500 regained all of its prior losses and traded right back up to the former resistance line. At the close the following Friday (3/15), the S&P 500 even marginally eclipsed that resistance line (provided you had a magnifying glass to see it). The strength from that week followed right through to the next week as the S&P 500 looked to have finally and convincingly broken through that pesky resistance level of 2,816 (green shaded box), confirming that the ‘breakdown’ from the first week of March was a fakeout.

Or was it the rally that was the fakeout? Ever since last Wednesday’s FOMC meeting where the central bank took on a surprisingly dovish tone, equities have once again had trouble. Whether it was last Friday’s sell-off that took the S&P 500 back below the former resistance line or Tuesday’s rally which has now seen its early gains more than halved, it seems as though the market can’t make up its mind one way or the other as the S&P 500 sits right on the resistance line at 2,816 as we type! In the span of less than a month, we have seen two moves (one up and one down) that technicals suggested was the start of a move, and both proved to be false alarms.

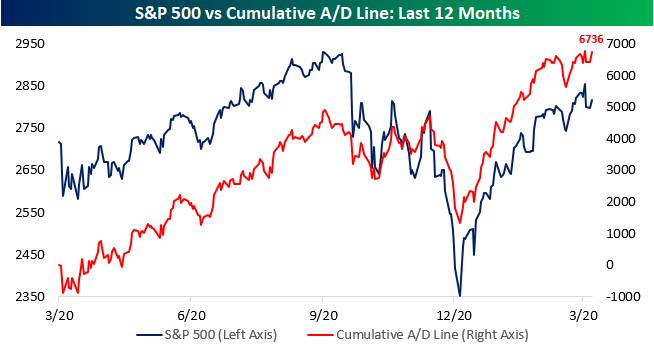

Unfortunately, we aren’t getting much in the way of direction from market internals either. The S&P 500’s cumulative A/D line remains strong, but after hitting new highs earlier today, as equities have sold off, so too has the A/D line putting it back below last week’s highs. The fact that the S&P 500 A/D line continues to hold up right near its record highs is definitely more positive than negative, but we’d much more prefer something a little bit more decisive.

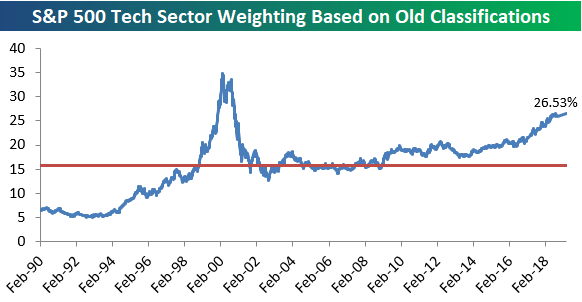

S&P 500 Sector Weightings — Tech Treks Higher

Below is a table we published last September showing the S&P 500 stocks that were impacted by the S&P GICS sector re-classifications. Twenty stocks in the index switched sectors at the time, while the three Telecom stocks remained in what became the new Communication Services sector.

Since a number of the stocks involved in the sector re-classifications were mega-caps, the switch ended up altering sector weightings in the S&P 500 quite a bit. Both Alphabet (GOOGL) and Facebook (FB) came out of the Technology sector and went into the Communication Services sector, which lowered the Tech sector’s market cap by $1.3 billion at the time. Other stocks like Disney (DIS), Netflix (NFLX), and Comcast (CMCSA) moved nearly $500 billion in market cap from the Consumer Discretionary sector to the Communication Services sector.

The sector re-classifications last September came at a time when the Tech sector’s weighting in the S&P 500 had ballooned up to 26% of the index. Not since the Dot Com bubble of the late 90s had Tech’s weighting been that high, so the timing of last year’s sector moves was very convenient. The re-classifications basically clipped 5 percentage points off of Tech’s weighting in the S&P, which made things look a lot less lopsided.

So what would the Tech sector’s weighting look like now if the sector re-classifications had not taken place last September? We answer that question in the chart below. Had the re-classifications not taken place, Tech would currently make up 26.53% of the S&P 500. That would be a new high for the current expansion. And the only time Tech’s weighting has been higher than this level was during a 10-month window between December 1999 and October 2000. That turned out to be quite a disastrous time to be long Tech.

Below is a chart showing current S&P 500 sector weightings based on both the old and new sector classifications. As shown, instead of 26.53% based on the old classifications, Tech has a much more digestible, but still high, 21.14% weighting in the S&P.

Health Care ranks second with a weighting of 14.56%, followed by Financials at 12.64%. Communication Services ranks 4th at 10.24%, and then Consumer Discretionary, Industrials, and Consumer Staples rank 5th through 7th. Energy, Utilities, Real Estate, and Materials combine for a weighting of about 14.5%, which is the same size as the Health Care sector on its own.

These numbers really give you a good sense of which sectors impact movements in the S&P the most, and which ones have basically no impact at all anymore.