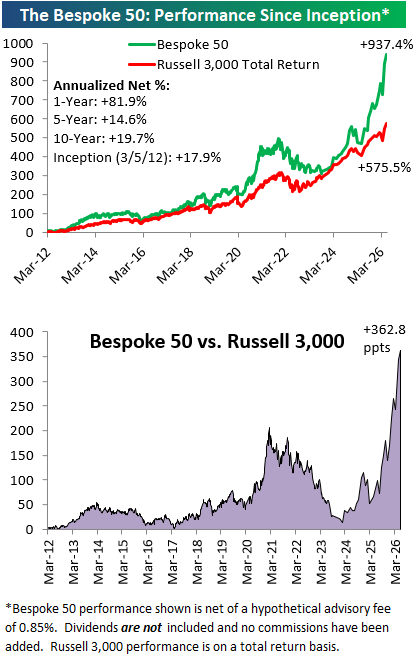

The Bespoke 50 Growth Stocks – 5/28/26

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There were eight changes to the list this month.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 5/28/26 – Breadth Divergences

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The distance between insanity and genius is measured only by success” – Ian Fleming

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

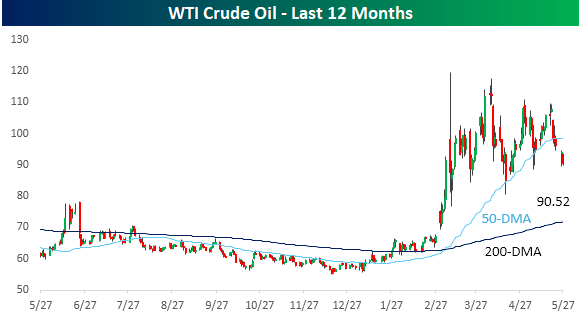

Markets are taking a breather this morning as the US and Iran trade missile and drone strikes. The S&P 500 looks poised to open 0.2% lower, while the Nasdaq is down 0.33%. After a brief excursion below $90, WTI crude oil is back above $90, gold is down over 1%, and the 10-year yield is up 3 bps to 4.51%.

Asian stocks were mostly lower overnight, with the Nikkei down 0.5% and Hong Kong falling 1.3%. The Shanghai Composite bucked the trend, finishing with a marginal gain, but even South Korea finished the session lower, falling 0.5%. South Korea down? Outside of the rising tensions between the US and Iran, there was no obvious catalyst for the declines in the region.

In Europe, events in the Middle East have also weighed on equities. The STOXX 600 is down close to 1%. Led lower by the UK, while Italy bucks the trend with a gain. Hawkish comments from the ECB’s Chief Economist also haven’t helped.

In the US today, there’s a monster slate of data on the calendar with Personal Income, Personal Spending, PCE, Jobless Claims, Durable Goods, and GDP all at 8:30, followed by New Homes Sales at 10 AM, as well as Energy inventories at 10:30 and 12:00.

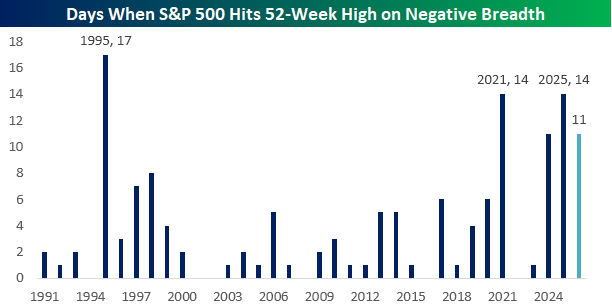

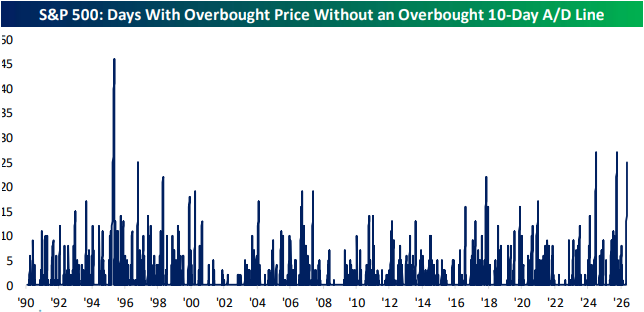

Yesterday was another one of those days when the S&P 500 hit a 52-week high, but breadth was negative. So far this year, these types of daily divergences have occurred 11 times, and if that brings back memories of the late 1990s, it shouldn’t.

As shown in the chart below, we’re not even fully five months into the year, but this year already ranks tied for fourth in the number of days when the S&P 500 closed at a 52-week high but breadth was negative. The only years with more occurrences were 1995 (17), 2021, and 2025, with 14. If you look at the late 1990s, though, in 1998 it happened only eight times all year, in 1999 there were only four occurrences, and in 2000, it only happened twice.

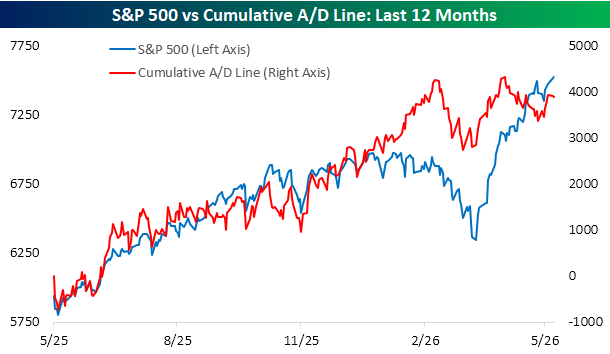

Regarding breadth, the S&P 500’s cumulative advance/decline line continues to diverge from price. On 4/20, the cumulative A/D line made a marginal new high, but ever since then, it’s been biased to the downside, even as the S&P 500 has rallied close to 6%.

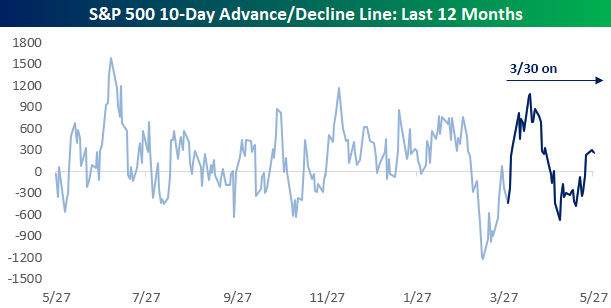

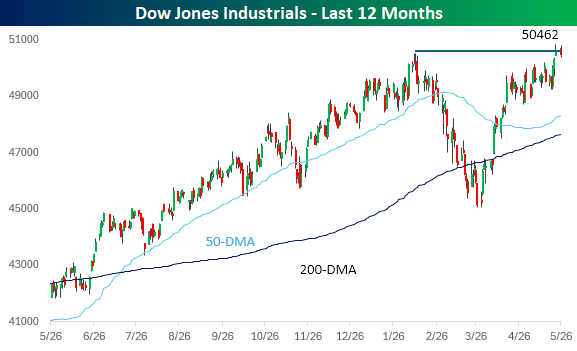

At least there have been some signs that breadth is modestly improving. The chart below shows the S&P 500’s 10-day A/D line over the last year, with the period from 3/30 shown in dark blue. While breadth was positive in the early days of the rally, from late April through just before Memorial Day weekend, it was negative before moving modestly back into positive territory this week. Breadth could still use a lot of improvement, but you have to start somewhere!

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Overbought Without Breath, Regional Prices Rise, AI – 5/27/26

Log-in here if you’re a member with access to the Closer.

- The S&P 500 has been overbought for 31 days in a row, but the 10-day A/D line hasn’t experienced an overbought reading since April 21st.

- Regional manufacturing surveys had the strongest showing for price indices since the spring of 2022.

- Special questions from regional Federal Reserve bank surveys indicated rising prices and decelerating AI adoption among responding firms.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Chart of the Day – Memory Stocks Make a Memory

Q1 2026 Earnings Conference Call Recaps: Modine (MOD)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Modine (MOD) Q4 2026 earnings call.

![]()

Modine Manufacturing (MOD) makes thermal management equipment, most importantly the chillers, cooling units, and air handlers that keep data centers from overheating. It has become one of the most direct ways to invest in AI infrastructure buildout. This was a landmark quarter as MOD made a $4 billion long-term agreement with an existing data center customer to supply chillers from 2027 through 2029, with no more than $2 billion in any single year. Management raised its fiscal 2027 data center growth forecast to 60% to 80% and reaffirmed a 50% to 70% CAGR for fiscal 2028, implying a data center business approaching $3 billion or more. The company also closed the year with record order intake for the second straight quarter. Component shortages hit late in Q4 and will weigh on Q1 production, though management says it won’t affect the full year. Tariffs are a headwind but manageable, with cost recovery mechanisms in place and a typical 3 to 6 month lag. The pending spin-off of its legacy vehicle thermal business into Gentherm remains on track to close by year’s end. MOD reported a triple play; however, shares are down over 6.5% on the day…

Continue reading our Conference Call Recap for MOD by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q1 2026 Earnings Conference Call Recaps: DICK’S Sporting Goods (DKS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers DICK’S Sporting Goods (DKS) Q1 2026 earnings call.

![]()

DICK’S Sporting Goods (DKS) is the largest sporting goods retailer in the US, selling everything from cleats and golf clubs to trading cards and licensed gear. Its acquisition of Foot Locker last year made it a global sports retail powerhouse, and its results offer one of the clearest reads on how the American sports consumer is spending. The core DICK’S business put up a 6% comp on top of a 4.5% comp last year, with no signs of trade-down across income levels and 1.5 million new customers added in the quarter alone. On the Foot Locker side, the turnaround is ahead of schedule. The US Foot Locker banner comped up 6.4%, and the Fast Break refresh, which basically declutters the shoe wall and brings apparel back, is delivering double-digit comps across its first 100 locations. The one soft spot was gross margin, dinged by higher fuel costs, startup costs from a new distribution center, and the fast-growing but lower-margin trading cards business. Despite better-than-expected results, shares opened more than 3% lower on 5/27…

Continue reading our Conference Call Recap for DKS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

The Triple Play Report: 5/27/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Better Late Than Never

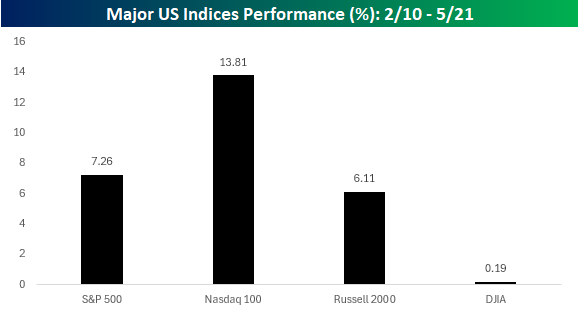

Last week, the Dow finally caught up to the rest of the major US indices in surpassing its pre-Iran war highs. Since that move to new highs, the oldest US index has been moving sideways for the last couple of days.

A look at the performance of major US indices from 2/10 through 5/21 – the period the Dow went between highs – illustrates how much the index has lagged its peer indices. While the DJIA rallied just 0.19% during that span, every other major US index was up at least 6%, with the Nasdaq 100 blowing them all out of the water, gaining nearly 14%.

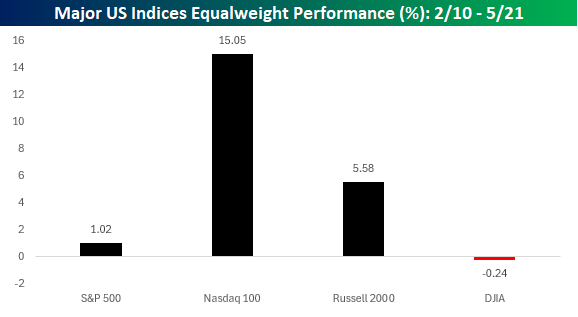

While the Dow has lagged its peer indices, on an equal-weighted basis where each component’s performance is treated equally, the Dow’s underperformance doesn’t look quite as bad, at least relative to the S&P 500. As shown in the chart below, while the 30 Dow components were down an average of 0.24% from 2/10 through 5/21, the average S&P 500 component was up just barely 1%. The average Russell 2000 component, however, was still up close to 6%, while the average performance of the stocks in the Nasdaq 100 is even higher than the index’s performance.

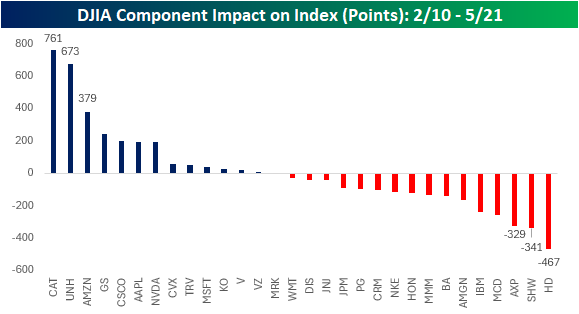

Turning back to the Dow, breadth in the index from 2/10 through 5/21 was skewed to the downside. The chart below shows each component’s impact on the index in terms of points during that period. Caterpillar (CAT) has had the biggest positive impact, responsible for 761 upside points, followed by UnitedHealth (UNH) at 673 points. Trailing way behind in third place, Amazon.com (AMZN) has added 379 points to the index’s performance.

On the downside, Home Depot (HD) and Sherwin-Williams (SHW) have had a combined downside impact of just over 800 points, illustrating housing market weakness. Pointswise, there wasn’t much in the way of train wrecks at the individual stock level, but just a lot more malaise than clear sailing ahead.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

Bespoke’s Morning Lineup – 5/27/26 – Here We Go Again

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Every victory is only the price of admission to a more difficult problem” – Henry Kissinger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

S&P 500 futures are modestly higher (+0.27%), while Nasdaq leads (+0.79%) as memory stocks surge again in pre-market trading. Crude oil is down over 4%, right around $90 per barrel, on hopes (again) of a resolution to the war in Iran and the closure of the Strait of Hormuz. The 10-year yield is down 3 bps to 4.46%, and gold is down another 1.2% to $4,450 per ounce.

It’s a quiet economic calendar this morning, with Richmond Fed the only report on the calendar, while several Fed officials are scheduled to speak. In Asia and Europe, markets were mixed, and the STOXX 600 is currently up 0.2%

As mentioned above, WTI crude briefly dipped below $90 per barrel this morning and now trades just above that level. Prices have been moving in an increasingly narrow range as the markets await a resolution to the war in Iran and the closure of the Strait of Hormuz. US markets have already rallied so much above their pre-war levels, so it’s hard to imagine seeing the US market get a major lift unless prices see a major decline from here. However, if prices continue to drift lower, we would expect to see a broadening of the rally, perhaps even at the expense of the mega caps.

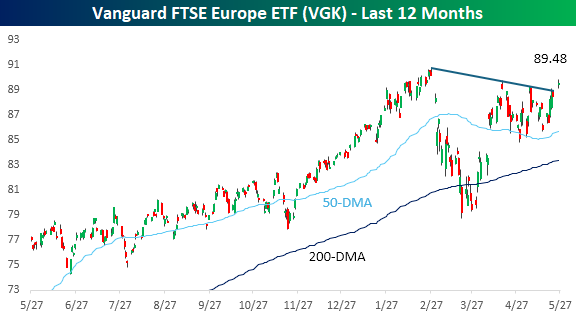

One area of the world more leveraged to oil prices is Europe. As shown below, the FTSE Europe ETF (VGK) has yet to take out its high from earlier in the year, but the drop in oil prices this morning has it getting closer. With this morning’s rally, the ETF is also breaking its downtrend from its earlier peak, leaving one less roadblock to clear on the road to new highs.

On a final note, here we go again. Whenever a new trend emerges in the market, you always find irrelevant companies looking to exploit the wave of euphoria by ‘rebranding’ their businesses to capitalize on the wave of investor interest. In the late 1990s, we saw it with dot-com companies. Then, about 10 years ago, penny stocks started adding crypto to their name in hopes of getting a pop in their share prices.

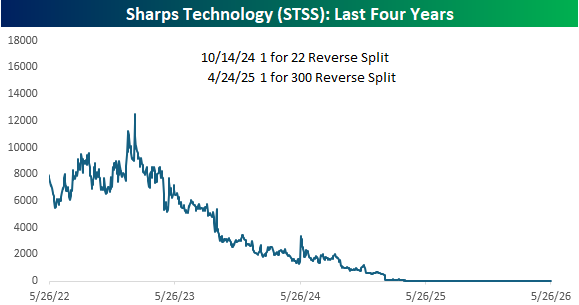

Recently, the “it” rebranding strategy is AI, and the latest example this morning is a company called Sharps Technology (SSTS). For years, Sharps Technology could generously be described as a medical device company in that they made medical syringes. In 2025, the company “pivoted” towards crypto, essentially becoming a Solana treasury company and holding as much as $250 million in the cryptocurrency on its balance sheet.

Judging by the company’s stock price, the pivot to crypto didn’t go as planned, as the price of STSS stock has been in a steady free-fall for several years now. On a reverse-split adjusted basis, the stock has gone from around $16,000 to $1.82 yesterday. It’s been like a memory stock, but only in reverse!

Often, a reverse stock split, even if it’s on a 1-2 basis, is a sign of trouble at a company. STSS has announced two reverse stock splits in the last four years. In October 2024, the company announced a 1 for 22 reverse split, and if that wasn’t bad enough, six months later, it announced a 1 for 300 split. If our math is correct, for every 6,600 shares you had in the summer of 2024, you have one now!

Since the crypto strategy hasn’t quite worked out for Sharps, today the company is going in a new direction and announced a new “vision to build the leading Agentic Finance Platform for the Global South.” The company will change its name to SkyAI and combine its “stablecoin rails with agentic AI to deliver financial access, education, and actionable intelligence to the billions of underbanked users across Africa, Latin America, and Southeast Asia.”

Whenever you see these types of stories, it immediately brings bubble talk into the conversation, and rightfully so. The one silver lining to all of this, at least at this point, is that the announcement has been largely ignored as shares of STSS are up merely six cents in pre-market trading.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Memory & Tokens, AI Chart Check – 5/26/26

Log-in here if you’re a member with access to the Closer.

- DRAM prices and GPU rental rates have continued to rise, powering the AI trade.

- AI related stocks have posted consistent gains recently with many of those names reaching new highs.

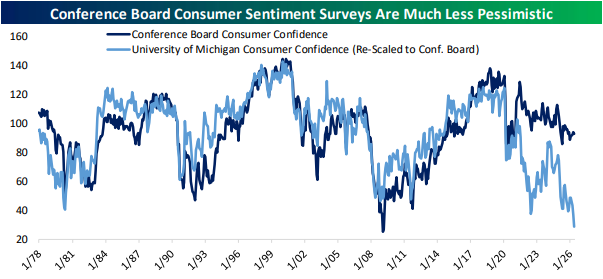

- Separate surveys tracking consumer confidence are showing drastically different results including a record low for UMich and more tempered readings for the Conference Board.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!