Bespoke Brunch Reads: 12/6/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Ancient History

A great wave: the Storegga tsunami and the end of Doggerland? by James Walker, Vincent Gaffney, Simon Fitch, Merle Muru, Andrew Fraser, Martin Bates, and Richard Bates (Cambridge University Press)

A review of the history of Doggerland, the delta region between the modern low countries and UK, which was subject to a catastrophic tsunami over 8,000 years ago. [Link]

‘Sistine Chapel of the ancients’ rock art discovered in remote Amazon forest by Dalya Alberge (The Guardian)

Deep in the Amazonian rain forest of Colombia, paintings on rock faces stretching across almost 8 miles reveal a fascinating insight into the pre-historic Americas. [Link]

Breakthroughs

How a Couple’s Quest to Cure Cancer Led to the West’s First Covid-19 Vaccine by Bojan Pancevski (WSJ)

A husband-and-wife team of German scientists whose parents migrated from Turkey were the core of a vaccine development team that turned around the eventual Pfizer product in a period of mere days. [Link; paywall]

Alphabet’s DeepMind achieves historic new milestone in AI-based protein structure prediction by Darrell Etherington (TechCrunch)

This week, Alphabet’s subsidiary DeepMind reported that it had developed a major leap in predicting protein folding, which could lead to much faster biological research and drug development. [Link]

Cultured meat has been approved for consumers for the first time by Niall Firth (MIT Technology Review)

A San Francisco-based start-up has been given preliminary approval to sell its lab-grown meat chicken nuggets in Singapore. While the initial product is very expensive and also relies on plant proteins, the move towards commercialization gives a peak into the potential for synthetic meat, a holy grail for vegans and climate activists alike. [Link; soft paywall]

Why Is Apple’s M1 Chip So Fast? By Erik Engheim (Debugger)

The chip Apple has developed in-house for its latest line of Mac computers represents a truly epic leap in terms of both technical approach and competitive landscape. [Link]

The Times They Are A-Changin’

Peak Oil Is Suddenly Upon Us by Tom Randall and Hayley Warren (Bloomberg)

COVID has brought forward an almost unthinkable reality: maximum oil demand. A look at what that might mean for the future of the global economy. [Link; soft paywall]

House passes historic bill to decriminalize cannabis by Alicia Victoria Lozano (NBC)

In a vote that mostly broke down on party lines (Democrats mostly in favor, Republicans mostly opposed) the House passed a historic bill that would remove pot from the Controlled Substances Act. [Link; auto-playing video]

How The Tumult of 2020 Will Shape the Future of Ride Sharing (Wired)

A podcast discussing the very strange ride for ridesharing giants which have been brought low by the pandemic…but offered some new opportunities as well. [Link; soft paywall]

Disaster

Huge Puerto Rico radio telescope, already damaged, collapses by Dánica Coto (PhysOrg)

The massive radio telescope dish of the Arecibo Observatory in Puerto Rico has collapsed, with the receiver assembly collapsing after a cable snapped back in August. [Link]

Death by PowerPoint: the slide that killed seven people (McDreeamie-Musings)

One potential reason for the Columbia shuttle disaster which killed its crew in 2003 was a poorly-designed slide in PowerPoint that was used to create a risk assessment. [Link]

Bad Calls

One country tells Apple to put a wall charger in iPhone 12 box by Trevor Mogg (digitaltrends)

Apple has been told by a Brazilian state regulator to include a wall charging unit compatible with the USB-C cords it includes with its new iPhone 12 or face a fine. [Link]

David Einhorn Has Made a Lot of Bad Bets — And One Very Good One by Katherine Burton (Bloomberg)

Since 2015, Greenlight Capital has lost 34%, with a slew of bad investments weighing returns. This year, the fund is flat thanks to a 15% gain for a homebuilder that the fund owns half of. [Link; soft paywall]

Policy

In Blue States and Red, Pandemic Upends Public Services and Jobs by Patricia Cohen (NYT)

Plunging tax receipts are forcing state and local governments to cut back, extending the economic pain of the COVID recession. [Link; soft paywall]

Bros

Bro Culture, Fitness, Chivalry, and American Identity by Patrick Wyman (Substack)

A deep investigation into bro culture, from the gym floor to the coffee grinder. Wyman ties his narrative into the medieval past as well as the contemporary reality of American bros. [Link]

Hungarian MEP admits he was at lockdown ‘orgy’ by Maïa De La Baume (Politico)

Brussels policy broke up a lockdown party this week with explosive results: a Hungarian MEP closely allied to Hungarian Viktor Orbán was in attendance at a gay orgy. This wouldn’t be remarkable if it wasn’t for the Orbán government’s long track record of LGBTQ suppression. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – A Good Month in Four Days

If you were expecting a bit of a pullback to start December after November’s big gains, it didn’t come this week. While November’s performance for the US and global equities was the equivalent of a good year, December’s MTD returns already would be considered a great month! Major US equity indices are all up 2% already, and the small-cap Russell 2000 is up close to 4%. Every sector with the exception of Utilities is also up on the month, but Energy is by far the biggest winner with a gain of over 10%. Even after that gain, though, it is still down nearly 30% on the year. In international markets, we’ve also seen big gains with countries like Brazil, Mexico, Spain, Russia, and the UK all up over 5%. Lastly, as one might expect given the big gains in equities, bonds are all lower on the month with the most weakness at the long end of the curve.

This week’s Bespoke Report is a bit shorter than normal as we have also started to publish various sections of our annual Bespoke Report Market Outlook. To view this week’s Bespoke Report as well as our Annual Outlook report as it’s published, take advantage of our 2021 Annual Outlook Special.

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

2021 Outlook – Credit

Our 2021 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2021.

The 2021 Bespoke Report contains sections like Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2021 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Housing” section of the 2021 Bespoke Report, focusing on the wild ride taken by credit markets over the course of 2020 and the outlook for 2021. We review the long-term history of corporate debt yields and spreads to benchmark interest rates, as well as looking at what the current backdrop implies for equity markets. We finish with a preview of what might become the biggest focus for credit markets in 2021.

To view this section immediately and all other sections, become a member with our 2021 Annual Outlook Special!

2021 Outlook – Housing

Our 2021 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2021.

The 2021 Bespoke Report contains sections like Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2021 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Housing” section of the 2021 Bespoke Report, focusing on the recent data and outlook for housing markets and homebuilders. We review affordability, construction data, activity in the existing and new home markets, data and drivers for homebuilder stocks, and finally a review of the impact COVID has had on mortgage delinquencies.

To view this section immediately and all other sections, become a member with our 2021 Annual Outlook Special!

2021 Outlook – Washington

Our 2021 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2021.

The 2021 Bespoke Report contains sections like Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2021 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Washington” section of the 2021 Bespoke Report, which recaps market scenarios under different political compositions in DC as well as some important comparisons between this election and 2016’s.

To view this section immediately and all other sections, become a member with our 2021 Annual Outlook Special!

2021 Outlook – Valuation

Our 2021 Bespoke Report market outlook is the most important piece of research that Bespoke publishes each year. We’ve been publishing our annual outlook piece since the formation of Bespoke in 2007, and it gets better every year! In this year’s edition, we’ll be covering every important topic you can think of that will impact financial markets in 2021.

The 2021 Bespoke Report contains sections like Economic Cycles, The Fed, Sector Technicals and Weightings, Stock Market Sentiment, Stock Market Seasonality, Housing, Commodities, and more. We’ll also be publishing a list of our favorite stocks and asset classes for 2021 and beyond.

We’ll be releasing individual sections of the report to subscribers until the full publication is completed by year-end. Today we have published the “Valuation” section of the 2021 Bespoke Report, which compares current valuations for major indices and sectors to their historical levels at various points in bull and bear markets. We also analyze the earnings yield, price to book ratios, and dividend yields for the S&P 500 relative to history.

To view this section immediately and all other sections, become a member with our 2021 Annual Outlook Special!

Bespoke’s Morning Lineup – 12/4/20 – Positive Tone into Jobs Report

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“I buy when other people are selling.” – J. Paul Getty

It’s safe to assume then that Mr. Getty hasn’t been buying much lately. Futures are higher again this morning putting the S&P 500 on pace for its fourth positive week in the last five, but in order to get there, we’ll have to get through the November jobs report. There have been some concerns about the health of the jobs market lately, but secondary indicators we track have been holding up relatively well.

Be sure to check out today’s Morning Lineup for updates on the latest market news and events, a discussion of the latest OPEC talks, factory orders in Germany, an update on the latest national and international COVID trends, and much more.

We’ve illustrated the positive breadth in the market in a number of different ways lately, but here’s another. For the last few days now, all 24 of the S&P 500’s Industry Groups have been trading above their 200-DMA. Looking back at the last five years, that doesn’t happen all that often. The last time there was such a high reading was at the start of the year on January 2nd. While the year may be on pace to finish right where it started in terms of breadth, it was far from a straight line as this reading went from 100% down to 0% and back to 100%. You can’t get any wider of a range than that!

Bearing Down Into The Holidays

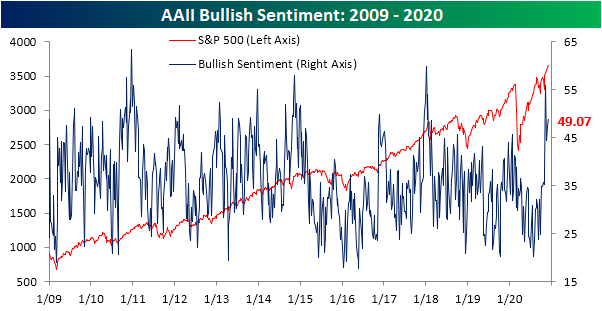

The S&P 500 has pressed to more all-time highs, and as a result, sentiment has turned even more bullish. In this week’s AAII sentiment survey, nearly half of the respondents (49.07%) reported a bullish. That is up for a second week in a row and remains at some of the highest levels of the past few years, though, it is more moderate than the reading from the first week after the election when over 55% reported as bullish.

While bullish sentiment is still off its recent highs, bearish sentiment has continued to press to new lows. 22.66% of respondents reported as bearish this week. That is down from 27.47% last week and is the lowest reading for bearish sentiment since the final couple of weeks of last year and the first week of 2020.

Given this, the bull-bear spread remains widely in favor of bulls, but off of its highs from a few weeks ago. Just like bullish sentiment, it is still at some of the highest levels of the past few years. Outside of the early November high, the bull-bear spread is at the highest level since February 2018.

Neutral sentiment is perhaps the most normal of the sentiment categories. While bullish and bearish sentiment readings are several percentage points away from their historical averages, at 28.25% neutral sentiment is only 3.19 percentage points below its historical average. Click here to view Bespoke’s premium membership options for our best research available.

Equity Newsletter Exuberance

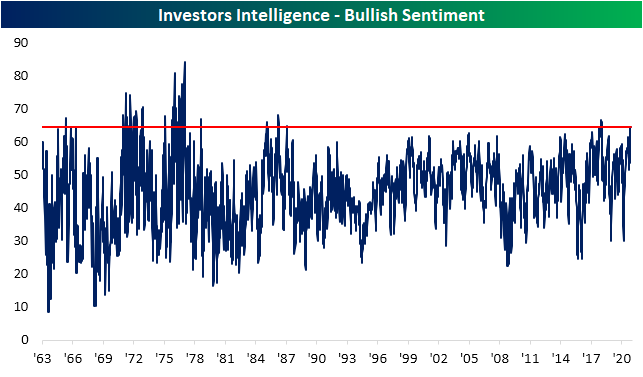

As we discussed in an earlier post, sentiment, as proxied by AAII’s weekly survey, has been overwhelmingly bullish. Other sentiment surveys are echoing the exuberance among investors. The Investors Intelligence survey of equity newsletter writers likewise saw bullish sentiment rise again this week from what were already strong levels. 64.7% of respondents reported as bullish this week. That is in the top 3% of all readings in the history of the survey. The last time this reading on bullish sentiment was this elevated was in January of 2018. Prior to that, you would need to go all the way back to February of 1987 to find a time that a higher share of respondents reported as bullish.

Meanwhile, just 16.7% of the respondents reported as bearish. While not at the same sort of extreme as bullish sentiment (in the bottom 13% of all readings), that is the lowest reading since early September.

In addition to gauging bearish sentiment, the report also measures the percentage of respondents that are “looking for a correction”. This reading ticked slightly higher this week rising from 18.2% up to 18.6%. While slightly higher, that is still in the bottom 20% of all readings across the history of the survey. More recently, though, this was more of an extreme low. Last week’s reading of 18.2% was the lowest reading since December of 2006. Click here to view Bespoke’s premium membership options for our best research available.

Services Slowing

Just like the reading on manufacturing earlier this week, the ISM’s Non-Manufacturing survey showed overall growth in November, albeit at a slower rate. The headline reading for the services index beat expectations (55.9 vs 55.8 expected) but still came in below last month’s level of 56.6. That is a sixth consecutive month of expansionary readings (readings above 50 indicate growth/below 50 indicate contraction) although the reading for November was the lowest of those six months. The same applies to the composite of the manufacturing and services which fell from 56.9 to 56.1.

Looking across each of the individual indices of the report also resembled the manufacturing report. While most components continue to be consistent with further growth, November did see some slowing across a range of indicators.

The improvements in business activity have considerably moderated over the past few months. After a near-record high reading back in July, this index has fallen every month except for in September. At 58, the index is around levels similar to just before the pandemic began earlier this year. A slowdown in orders likely plays a role in this as the index for New Orders similarly sits in the middle of its historical range following a 1.6 point decline to 57.2 in November. While that is still indicative of new orders growth, it would be the slowest growth since August.

Export order growth slowed in November as that index fell to a barely expansionary reading of 50.4. While orders from outside the US were a bit weak, the index for imports rose to 55 which is the strongest level since January of this year (55.1). One important thing to note with these indices, though, is less than half of survey respondents report that they do not use or track imports/exports (only 29% for exports and 37% for imports). In other words, these readings only apply to a smaller sample of responding firms.

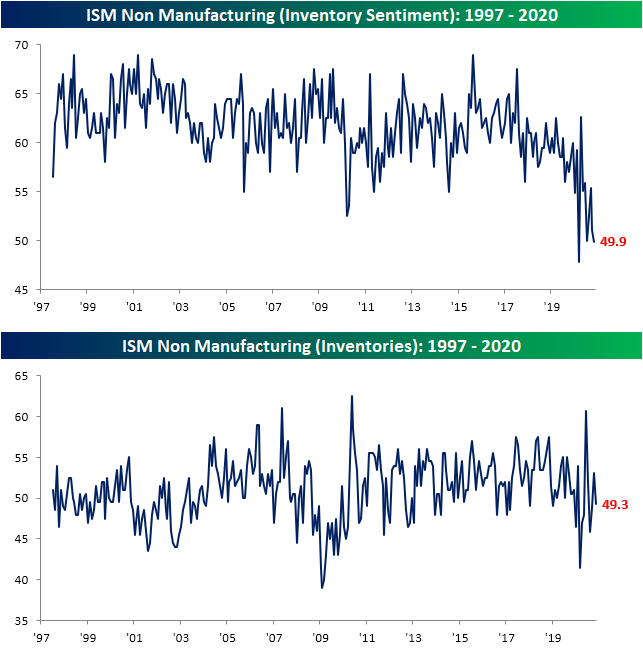

The continued growth in new orders has resulted in smaller inventories. For only the second time in the index’s history (the other instance being March of this year), the index for Inventory Sentiment came in below 50. That indicates a larger share of companies are reporting that inventories are too low rather than too high. As a result, the index for Inventories showed a contractionary reading of 49.3. That is not any sort of extreme reading but again points to declining inventories.

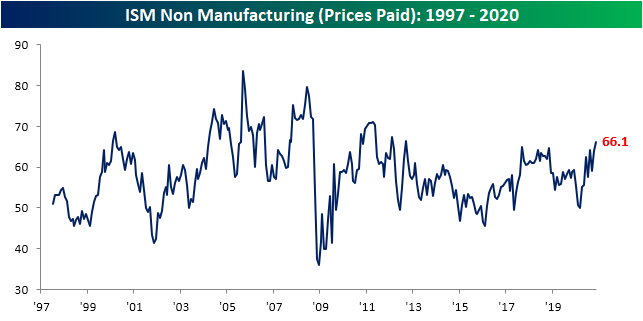

Stronger demand has filtered through to lower inventories which has, in turn, resulted in higher prices. The index for prices paid rose to 66.1 from 63.9 in October. That points to prices growing at their fastest pace since February of 2013.

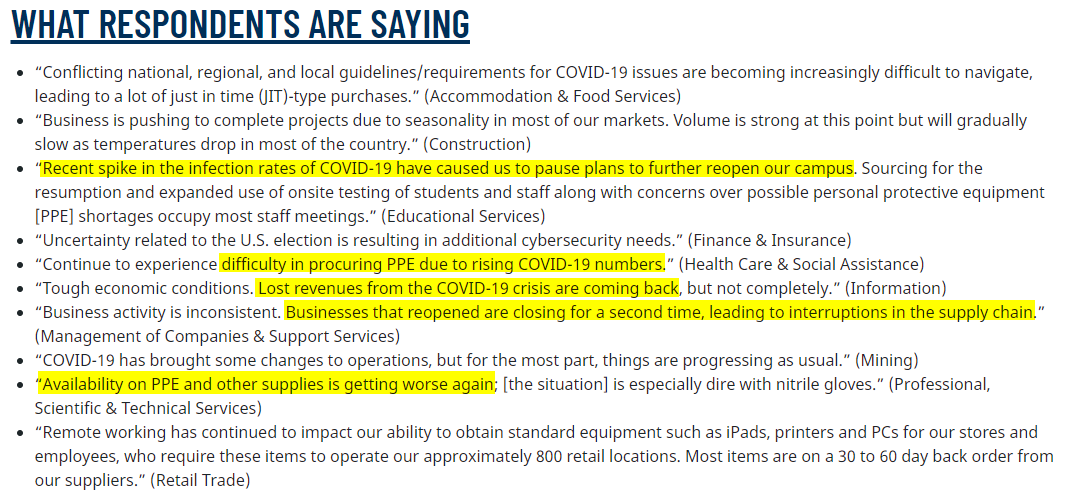

Staying on the topic of prices, with housing flying high, prices for construction contractors and construction supplies like lumber, PVC, and steel have all been on the rise as they remain in short supply. Outside of construction contractors, labor, in general, was cited as in short supply. That is consistent with some commentary concerning employment in Monday’s manufacturing release. But unlike Monday’s report in which the employment component fell to a contractionary reading, the services employment index showed a third straight expansionary reading at 51.5. Additionally, as COVID has made a resurgence in the past few months, PPE and other related products continue to be cited as some of the commodities seeing price increases. For PPE this month saw a 10th month in a row that these products were in short supply with higher prices.

The commentary section reaffirms the COVID ressurgence impact. Quotes from various industries stated how higher infection rates have had negative impacts. Click here to view Bespoke’s premium membership options for our best research available.