Chart of the Day: Don’t Throw GPK Out With The Trash

Bespoke’s Morning Lineup – 12/11/25 – Passing the Baton

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In today’s regulatory environment, it’s virtually impossible to violate rules.” – Bernard Madoff

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

17 years ago today, all hell was already breaking loose in financial markets as the banking sector had imploded three months earlier. Lehman’s bankruptcy accelerated a chain of failures and near-failures in some of the country’s most well-established banks. As if the market needed any more bombs hurled at it, along came the “Breaking News” interruptions on the news channels of a Ponzi scheme surrounding a man named Bernie Madoff. We’ve come a long way in the last 17 years, and after yesterday’s Fed meeting, the S&P 500 is back right near record highs and has rallied nearly 10-fold after accounting for dividends.

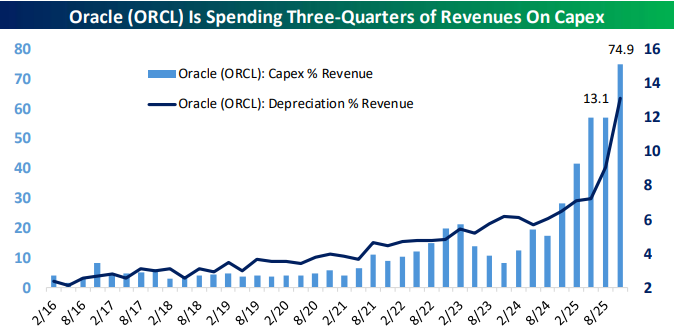

This morning, equity futures are taking a breather. Oracle (ORCL) earnings after the close last put renewed doubt on the AI trade, and the stock is down 13% as investors question whether the company can fund its ambitious capex plans. If that magnitude of decline, it would be the stock’s largest downside gap in reaction to earnings since at least 2001. Make sure to read our detailed discussion of ORCL earnings and investor concerns regarding the stock and the AI trade in the commentary section of today’s report.

After trading down close to 1% overnight, though, S&P 500 futures have rebounded and are now down just 0.3% while the Nasdaq is down 0.5%. Treasury yields are down another 3 basis points (bps) to 4.13%, and crude oil is down below $58 per barrel, falling over 1%. Gold is fractionally higher, but Bitcoin and other crypto assets have reversed all of their gains from the prior 24 hours.

In Asia, stocks traded mostly lower, with the Nikkei down 0.9% and South Korea down 0.6% as ORCL’s earnings dragged on the region. In Europe, though, we’re seeing modest gains across the board with the STOXX 600 trading 0.2% higher.

In the US, the only economic data release on the calendar this morning was jobless claims. Initial claims came in higher than expected at 236K (versus 220K), erasing all of last week’s surprising decline. Meanwhile, continuing claims showed a sharp decline, falling to 1.838 million, or 100K less than expected. The continuing claims number is lagged a week, so the sharp drop in initial claims last week was likely a holiday quirk.

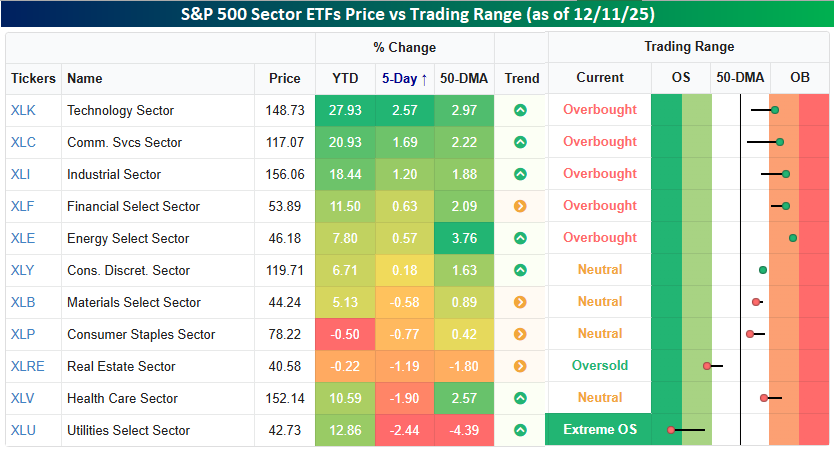

The S&P 500 closed within fractions of a new high yesterday, and the same sectors that have driven the market this year are the ones that have driven the rally over the last week. As shown in the snapshot below, Technology, Communication Services, and Industrials are the only two sectors up over 1% in the last five trading days, and they’re also the three best-performing sectors this year.

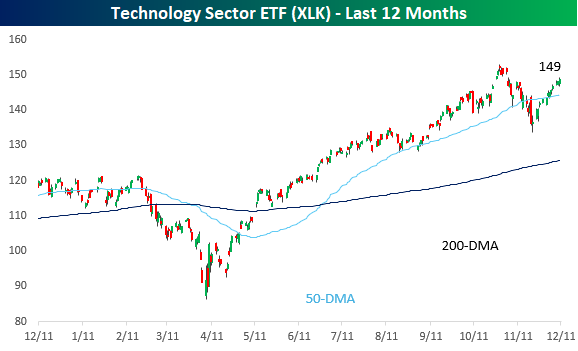

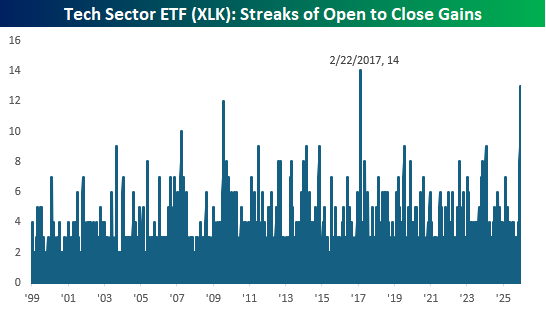

While the S&P 500 closed within whiskers of a new high and tech has led the rally, the Technology sector still has a ways to go before hitting a new high, as yesterday’s close was more than 2% below the late-October high. What stands out about the chart, though, is how much green there has been in the candles since the November low.

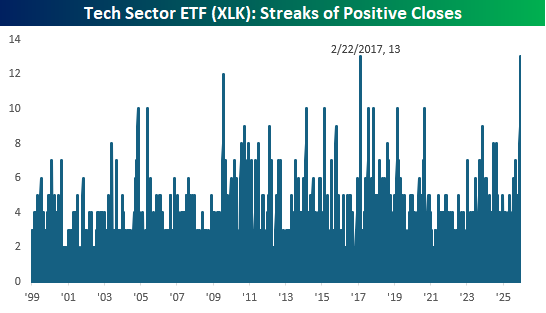

In fact, with 13 straight days of gains and 13 straight days of positive returns from the open to close, the Technology sector ETF (XLK) is knocking on the door of history. The 13 days in a row of daily gains are tied for the longest in the ETF’s history, dating back to 1999. The only other streak as long ended in February 2017. Similarly, the streak of open-to-close rallies is just one shy of the 14-day streak that also ended in February 2017.

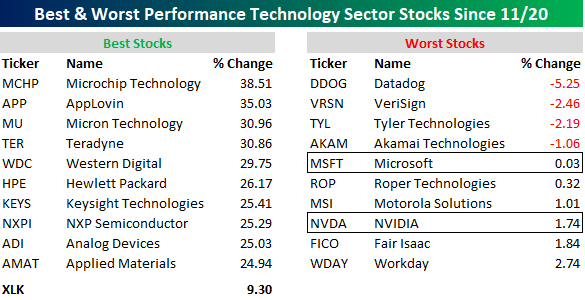

What surprised us most about the Technology sector’s recent run is the stocks that have been driving the bus. Nine Technology sector stocks are up over 25% since the close on 11/20, and the majority are semiconductor stocks. One semi-stock not on the list of winners, though, is Nvidia (NVDA). While it’s not down since 11/20, NVDA’s 1.74% gain ranks as the eighth-worst performance in the sector. Also on the list of laggards is Microsoft (MSFT), which is barely higher since 11/20 (+0.03%). These two stocks collectively account for about 25% of the entire Technology sector, but as they have tread water over the last two weeks, the sector they dominate has still rallied over 9%. Is the baton being passed?

The Closer – FOMC, SEP, ECI – 12/10/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a recap of the Fed day including the SEP update (page 1), the development of bill purchases (page 2), and market reactions (page 3). We then provide an update on the Employment Cost Index and Oracle (ORCL) earnings (page 4) before closing out with a look into the latest sentiment data (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

The Triple Play Report — 12/10/25

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 25 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

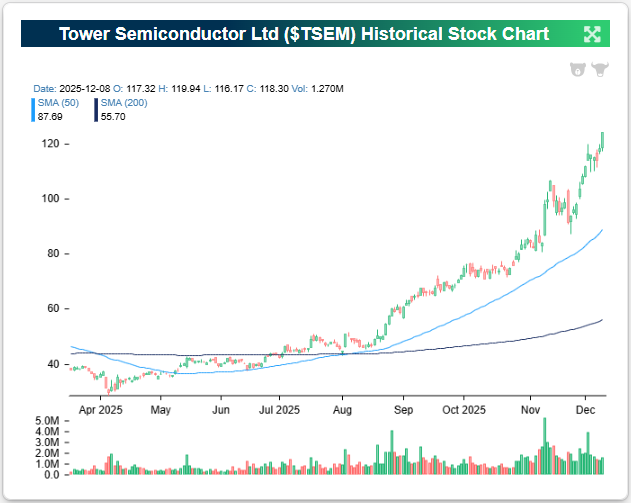

Tower Semiconductor (TSEM) is an example of a company that recently reported an earnings triple play before the opening bell on 11/10. In reaction, TSEM shares rallied 16.7% on the day. That move has helped push the stock up more than 140% YTD!

Here’s how AI describes the company: Tower Semiconductor (TSEM) is a specialized independent foundry that manufactures high-value analog integrated circuits, producing chips for customers who design hardware but do not own their own fabrication facilities. In other words, customers send TSEM blueprints, and it uses its factories to physically build those designs into finished computer chips. Instead of competing on the smallest digital processors, Tower focuses on customizing “specialty” process technologies, such as Silicon Photonics (SiPho), Silicon Germanium (SiGe), and RF-SOI, that excel at managing real-world signals like light, radio waves, and electrical power. You can think of these like the “senses” and “connectors,” rather than the main processors, “brains,” of a computer. These components are critical for optical transceivers in high-speed AI data centers, radio frequency front-ends in 5G smartphones, and power management systems in automotive and consumer electronics. Operating seven manufacturing facilities across Israel, the United States, and Japan, TSEM does not sell devices directly to consumers. Instead, it provides the essential manufacturing service and complex chemical processes needed to create these specific parts, which are then installed inside smartphones, cars, and the massive data centers powering AI.

Tower delivered a strong third quarter with revenue climbing 7% YoY to $396 million and net profit reaching $54 million, while the company raised guidance to a record $440 million for Q4 on the back of huge AI infrastructure demand. The standout performer was the Silicon Photonics segment, which creates optical interconnects for data centers, as revenue here surged 70% to $52 million and is rapidly moving toward ultra-fast 1.6 Terabit speeds that already make up nearly a third of production starts. This demand is so intense that management committed an additional $300 million investment to triple manufacturing capacity for these optical chips by late 2026. Customers are abandoning traditional lasers in favor of Tower’s silicon-based alternative because it offers better performance while requiring only half the number of lasers, making them far cheaper and more efficient.

As we touched on earlier, the stock has staged a historic run; up more than 140% YTD and roughly 325% since the April Tariff Tantrum. The stock is currently trading at its highest level in over 20 years. Wall Street has aggressively re-priced the company from a standard chip manufacturer to a critical piece of the AI supply chain. But this skyrocketing valuation creates a new challenge where expectations are now through the roof. With so much optimism already baked into the price, the company has effectively entered a zone where simply meeting estimates will likely not be enough going forward. To sustain this upward trajectory, TSEM must now likely continually deliver better-than-expected results to justify its massive run.

Looking at the snapshot below from our Earnings Explorer, Tower Semi (TSEM) has found a rhythm with its pace of positive reactions to earnings over the last three and a half years. The stock has risen on 13 of its 14 earnings reaction days since August 2022. EPS and revenue beat rates have been shakier, though. Although not a consistent triple play name, the company has managed a couple recently.

You can read more about TSEM and the 24 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 12/10/25 – Hot Rocks

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I am in a charming state of confusion.” – Ada Lovelace

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

On a Fed day, we’d normally say that wherever the futures are in the pre-market, don’t expect the market to be there after the decision is announced, let alone after Powell talks. Based on recent history, though, volatility on Fed days has been muted. As we noted in today’s Chart of the Day, the S&P 500’s average absolute daily change on the last five Fed days has been among the most muted relative to any other rolling five Fed day period since 1994. So, maybe the muted moves in futures markets are on to something!

Outside of equities, the 10-year yield is up 2 bps and back above 4.2% as part of a global move higher yields. Crude oil prices are also up fractionally but still below $58 per barrel, while the slide in natural gas continues as prices break below $4.50. Metal prices are all over the map as gold prices are slightly lower, while silver rallies over 1% and platinum falls over 1%. In the crypto pace, it’s also a mixed but downwardly biased morning as bitcoin falls 1%.

International markets have also been quiet overnight and this morning ahead of the Fed, as most major benchmarks saw, or are seeing, modest declines. Chinese CPI was weaker than expected, falling 0.1% versus forecasts for an increase of 0.2% while PPI in Japan was right in line with forecasts.

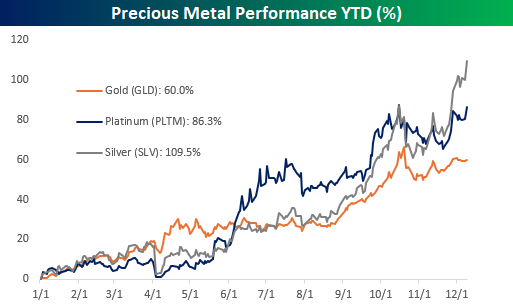

Warren Buffett has famously said of gold that it “gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again, and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.” While other precious metals like platinum and silver have more industrial uses than gold, based on public records, it has been decades since Buffett has been active in them. The primary reason Buffett has generally avoided commodities is that they are essentially a bet on future supply and demand rather than income-generating assets.

While they don’t produce income, precious metals are commodities that have produced massive capital gains this year. Gold (GLD) has rallied 60%, and those gains look modest relative to the 86.3% gain in platinum (PLTM) and the massive 109.5% gain in Silver (SLV).

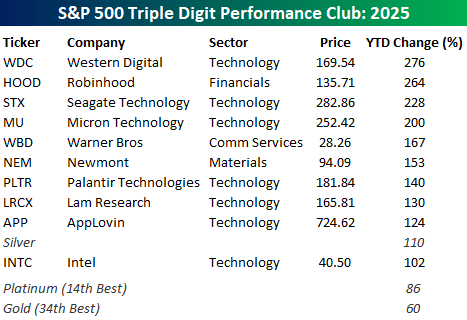

For all three precious metals, the YTD gains would be enough to rank near the top of the list in terms of YTD performance. With its 109.5% gain, SLV would be the tenth-best stock in the S&P 500 this year, ahead of Intel (INTC) and behind AppLovin (APP). Nothing against AppLovin and its prospects over the next several years, but 100 years from now, which do you think has a better chance of still being around in its current form? Silver or AppLovin?

While the gains in Platinum and Gold wouldn’t crack the top ten in terms of performance, the former’s 86.3% gain would rank as number 14 in the S&P 500, while Gold would rank number 34.

Looking at the ten best-performing stocks in the S&P 500 this year, all of them are up by at least 100%, and all but three are from the Technology sector. The top four performing stocks have not only had triple-digit returns, but they’ve also at least tripled! Sticking to the commodities theme, three of those stocks – Western Digital (WDC), Seagate Technology (STX), and Micron (MU) – all make data storage and memory products, which in the universe of the technology sector have for years been considered commodities as well.

Chart of the Day: Last Hour Strength?

The Closer – Cost Woes, PE Enters the S&P, JOLTS – 12/9/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a look into the drop in quality stocks and the rise of private equity names (page 1). We also note the performance of S&P 500 additions (page 2) before shifting into a recap of the JOLTS data (pages 3 and 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Consumer Pulse Report – December 2025

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Chart of the Day – Is the Long End of the Curve Signaling a Mistake?

Bespoke’s Morning Lineup – 12/9/25 – Power Outage

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Lesson Number One: Don’t Underestimate The Other Guy’s Greed!” – Frank Lopez, Scarface

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Bespoke’s Paul Hickey will be on CNBC’s Squawk on the Street today at 10 AM. Make sure to check it out!

Markets remain on snooze with little conviction in either direction this morning, and while investors “waiting for the Fed” has been the excuse, is there really any question over what Powell will say and do tomorrow? Futures are as close to unchanged as you can really get this morning, with the S&P 500 indicated to open up 1 point (0.18%) while the Nasdaq is faring “significantly” worse, down 0.06%. As we wait for the Fed, there is some economic data today. Small Business sentiment hit the tape earlier and came in modestly higher than expected, while JOLTS will hit the tape at 10 AM.

Overnight in Asia, it was a ho-hum session with the Nikkei up 0.1% while China, South Korea, and India were all down fractionally (less than 0.5%). The RBA left rates unchanged but had a hawkish tone. In Europe, the STOXX is down 0.1%.

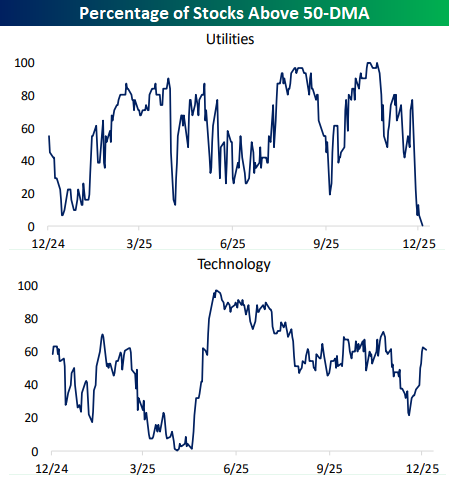

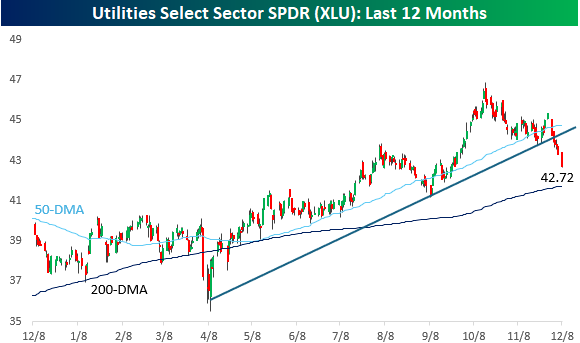

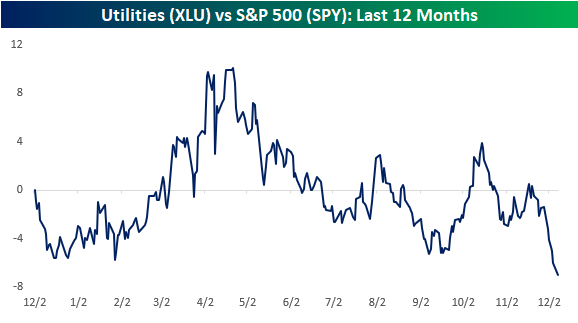

We had a power outage at the Bespoke offices yesterday afternoon, and coincidence or not, have you seen a chart of the Utilities sector recently? After being one of the better performing sectors this year, the sector started to fall on hard times since mid-October, to the point where in late November it broke its uptrend from the April lows. From there, the weakness in the sector picked up in intensity. The fact that longer-term interest rates have been rising hasn’t helped.

The recent weakness in the sector has also brought its relative strength versus the S&P 500 to a new low for the year. After handily outperforming during the tariff-tantrum in the Spring, the sector started performing in line with the broader market. For much of the last six months, its relative strength oscillated above and below the neutral line, but the last two weeks have seen it make a new leg lower.

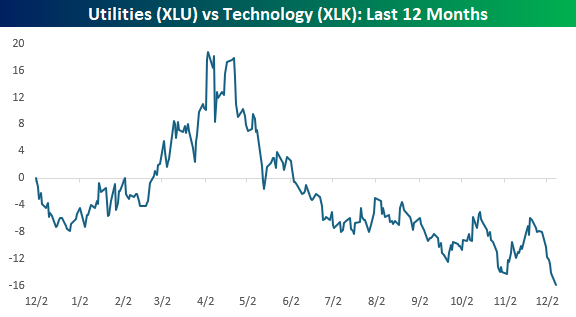

Given the power demands of AI, there have been times in the last few years when Utilities have been considered a technology play, but when you compare the sector’s performance to the Technology sector, it’s not even close. Utilities have been trending lower for the last six months.

The disparity is also apparent when you compare the percentage of stocks in each sector trading above their 50-day moving averages. The Utilities are experiencing a “blackout” in this metric as not a single sector closed above its 50-DMA yesterday. That compares to more than half of stocks in the Technology sector. After some trial and error last night, Con Ed finally got the power back on in our offices last night, now they need to work on getting some power back to the sector!