High Short Interest Revival

As we detailed in last night’s Closer, whatever name that it might be given—meme stocks, yolo trades, or “stonks”—there has been a trend recently in which there has been strong performance of highly volatile names loved by the most risk tolerant retail investor. That is roughly a year and a half to the day of the meme stock mania where highly shorted names saw massive short squeezes driven by the retail community.

Since the mid-June lows, highly shorted names have again been outperforming. Below we show the chart of an index covering the 100 most highly shorted stocks going back to early 2020. The vast majority of 2020 gains have been erased, however, this index has also risen 46% since its June 16th low (the same date as the broader market’s low). On a relative basis, the most heavily shorted stocks have been outperforming the Russell 3,000 in that time resulting in the relative strength line to break out of the downtrend that has been in place since the peak of the meme stock mania in late January of last year. That being said, the index itself has much further to go in order to break out of its downtrend off of that high in price.

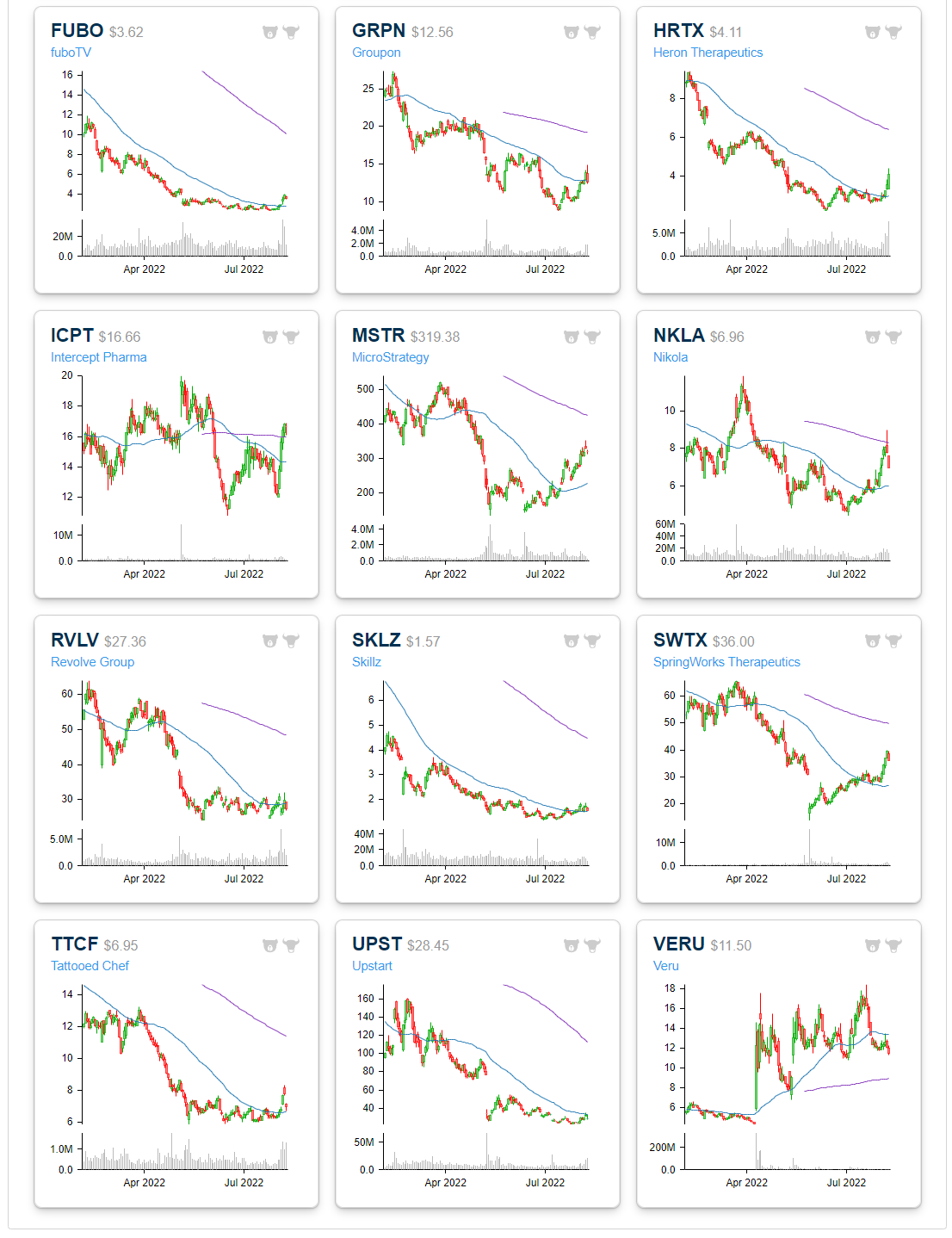

Below we show the stocks within the Russell 3,000 that currently have the highest levels of short interest as of the end of July. The only stock with more than 50% of its float sold short is Torrid Holdings (CURV). The next highest is a company that frequently finds itself high up on the list of highly shorted stocks: Dillard’s (DDS). While those readings are elevated, they are well below what had been the most heavily shorted stock a month and a half ago. As of the mid-June update, Redbox (RDBX) had an extremely elevated reading on short interest that was closing in on 100%. Today that reading has collapsed back down to a still elevated but less extreme 41.5%. We would also note, however, that RDBX is a messy story at the moment in the midst of an acquisition (confirmed to go through in the past 24 hours) with the potential to save the company from bankruptcy.

Other notables on the list of most heavily shorted stocks include grill-maker Weber (WEBR), Bed Bath & Beyond (BBBY), Upstart (UPST), Big 5 Sporting Goods (BGFV), Beyond Meat (BYND), Groupon (GRPN), and Nikola (NKLA). Click here to learn more about Bespoke’s premium stock market research service.

Below is a look at price charts for most of the heavily shorted stocks listed in the table above. While many of these names are up huge since mid-June, the gains hardly register on six-month charts because they got hit so hard in the first half of the year. Bespoke subscribers can create Custom Portfolios on our website like the one below to easily monitor baskets of stocks and ETFs. Start a two-week trial to test out the service today!

B.I.G. Tips – Dollar Moves into Unfamiliar Territory

Fixed Income Weekly: 8/10/22

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we look at the explosive market reaction to CPI this morning.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Chart of the Day: Semi’s Summer Slump

Bespoke’s Morning Lineup – 8/10/22 – The Day is Here…Whether You Can Afford it or Not

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Having a little inflation is like being a little pregnant.” – Leon Henderson

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s been a quiet morning for markets so far, but enjoy the calm before the storm while it lasts. The release of July CPI comes in the next few minutes (or has already been released depending on when you read this), and in the immediate aftermath of the release at least, markets are likely to experience a surge in volatility. How long that volatility lasts will be directly correlated to how much the headline and core aspects of the report deviate from expectations.

Over in Europe, the major equity benchmarks have seen little movement versus yesterday’s close, and if the releases of CPI for both Germany and Italy are any indication (both reports came in right in line with consensus forecasts), maybe there won’t be too many fireworks today. We can always hope!

Today’s Morning Lineup discusses earnings and market news out of Europe and the Americas, overnight economic data, and much more.

Last month, the June CPI surged 1.3% m/m which was the largest increase in headline CPI since September 2005. With the July report expected to come in at just 0.2%, it would represent the smallest m/m increase since January 2021. If the July headline CPI does match expectations, it would be just the fourth time since 1960 that the rate of increase in the m/m reading dropped by a full percentage point or more. The only other three periods where this occurred were September 1973 (-1.4 ppt), October 2005 (-1.2 ppt), and October 2008 (-1.0 ppt). In two of these three periods, the economy was either right on the cusp of or in a recession while the third period was after Hurricane Katrina when gasoline prices in the US temporarily went bananas.

Wherever the CPI report comes in this morning, one thing we can say is that weaker than expected reports have been hard to come by in the post-COVID world. Last month’s report was the tenth straight month that headline CPI was either higher than or in line with expectations. That is the longest streak of months without a lower-than-expected report since at least 1999. Not only that, but the current streak started just a month after what at the time had been the longest streak just ended. In other words, over the last 20 months, we have seen the two longest streaks without a lower-than-expected CPI report over at least the last 20 years.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Stonks are Back, Productivity Collapse, Home Inventory Surge – 8/9/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, after a brief recap of tonight’s earnings reports, we also show the resurgence of the meme stock trade (page 1). We follow up with the latest productivity and costs data for Q2 (pages 2 and 3). Afterward, we dive into the latest housing inventory data from Realtor.com showing a surge in active listings (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 8/9/22

Bespoke Stock Scores — 8/9/22

B.I.G. Tips – Q2 Earnings Triple Plays

Today we published our newest Earnings Triple Plays report. This season we identified 34 earnings triple plays that may be worth taking a closer look at.

What is a triple play? When a stock reports quarterly earnings, it registers a “triple play” when it beats analyst EPS estimates, beats analyst revenue estimates, and raises forward guidance. We coined the term back in the mid-2000s, and you can read more about it at Investopedia.com. We consider triple plays to be the cream of the crop of earnings season, and we’re constantly finding new long-term opportunities from this basket of names each quarter. You can track the newest earnings triple plays on a daily basis at our Triple Plays page if you’re a Bespoke Premium or Bespoke Institutional member. To read our newest report and see the triple plays that we think look the best right now, start a two-week trial to Bespoke Premium!

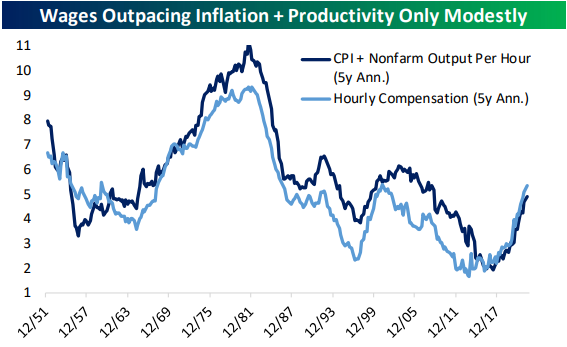

Inflation Still Top Of Mind for Small Business

While fewer respondents to this month’s NFIB small business survey reported that they observed higher prices, inflation continues to be a front and center concern. The percentage of respondents reporting inflation as their biggest problem has risen further to another record high of 37%. That completely erased June’s drop down to 34%.

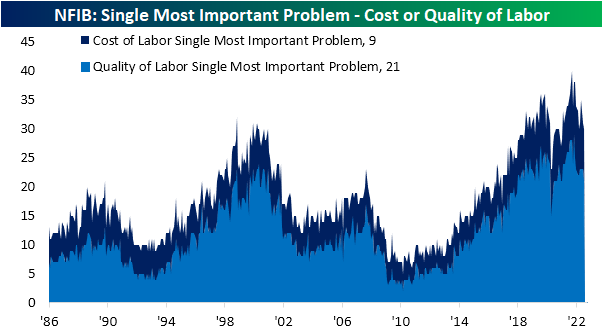

While broad inflation is currently the most pressing problem, other inflation-related measures also rose in July. The percentage of firms reporting cost of labor as their single most important problem rose to 9%, although that is still below the record high reading of 13% at the end of last year.

While we often combine that reading with the percentage of responses reporting quality of labor as the biggest issue as a gauge of labor market health, the latter problem dropped 2 percentage points to net out the rise in cost of labor. On a combined basis, these two concerns are now tied with March at 30% for the lowest level since January 2021 (28%).

One other combined reading that we often check in on is the percentage of respondents reporting government requirements or taxes as their biggest issues. Over the past few decades, Republican administrations have usually coincided with lower readings whereas Democrat administrations would see a higher reading. With inflation concerns surging this year, a historically low share of businesses are concerned about government action. The combined reading fell to another record low of 16% in July with the entirety of that drop on account of a 3 percentage point decline in government requirements and red tape. Click here to learn more about Bespoke’s premium stock market research service.