Bespoke’s Morning Lineup – 10/28/22 – Stalling Out

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We have never said that we’re perfect. We’ve said that we seek that. But we sometimes fall short.” – Tim Cook

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We’re seeing another day this morning where Nasdaq futures are much weaker than the broader market. The culprit this morning is Amazon.com (AMZN) which is trading down over 13% after dropping as much as 20% in after-hours trading. The Nasdaq is indicated to open down over 1% while the S&P 500 is down by about half that. Treasury yields are higher this morning, and the 10-year yield briefly traded back above 4% before falling following the latest batch of economic data. Another factor contributing to the weakness in the tech sector is a report that the Biden Administration is considering adding additional restrictions on technology exports to China.

It’s been a busy morning of economic data and the Employment Cost Index (+1.2%), Personal Income (+0.4%), and PCE Prices (+0.3%) were all in line with forecasts. Personal Spending (+0.6%) was higher than expected, and at 10 AM we’ll get Pending Home Sales and Michigan Confidence.

What a month it has been for the Energy sector. Since its recent low in late September, the S&P 500 Energy sector has rallied about 30% and is currently within 4% of its early June high. Looking at a longer-term chart of the sector shows that it has consistently found support at the trendline that extends back to the higher low it made in late 2020. The fact that it managed to bounce at that support during the last leg lower was impressive given that it followed what was a lower high for the sector in late August.

With its gain of over 60% YTD, Energy has trounced the market on a YTD basis, and while the sector has yet to take out its high from June, its performance gap with the S&P 500 did manage to make a new high yesterday as it’s now outperforming the S&P 500 by 80 percentage points YTD.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Meta: Mega Cap No More, 50-DMA Fumble, GDP, Durable Goods – 10/27/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight with a look at Meta Platform’s (META) fall from grace as well as the S&P 500’s rejection of its 50-day moving average (page 1). We follow up with a look at the first release of Q3 GDP (page 2) followed by a review of durable good orders (page 3). Afterward, we provide an update of our 5 Fed manufacturing composite with the addition of the Kansas City Fed (page 4) before closing out with a review of the latest 7 year note auction (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 10/27/22

The Bespoke 50 Growth Stocks — 10/27/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were eight changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Chart of the Day: Dow Strength

Bespoke’s Morning Lineup — 10/27/22

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You should welcome a bear market, since it puts stocks back on sale.” – Jason Zweig

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s a very mixed picture for equity futures this morning with the Dow indicated up pretty sharply while the Nasdaq is down by a similar magnitude driven in large part by shares of Meta Platforms (META) which is down over 20% and struggling to hang on to triple-digits. The ECB just announced its policy decision and hiked rates by 75 bps (as expected). Here in the US, we have a busy morning of economic data, plus big earnings reports from Amazon.com (AMZN) and Apple (AAPL) after the close.

The US Dollar index peaked about a month ago, and its move lower has coincided with the bounce that we’ve seen in US equity indices. The same trend has played out over a shorter one-week time frame as well, which you can see in the Trend Analyzer snapshot below. Over the last five days, the US Dollar Bullish ETN has fallen 2.8% and broken below its 50-day moving average. At the same time, every other area of financial markets has moved higher within its trading range.

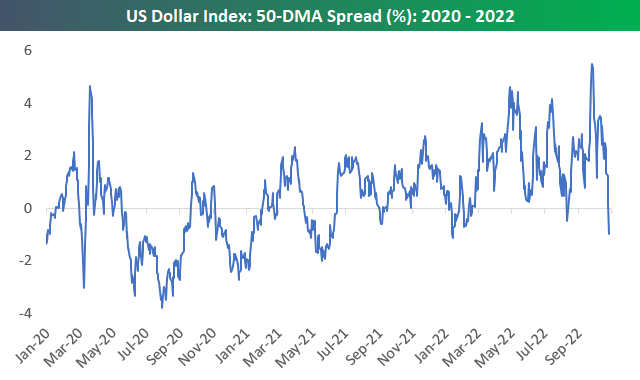

Yesterday, the US Dollar Index broke below its 50-DMA for the first time since August, and it traded the farthest below its 50-DMA since early January. As shown below, the August break did not last long, as the Dollar’s uptrend resumed almost immediately.

This morning the Dollar is back up, and a resumption of its uptrend will almost assuredly coincide with a resumption of the equity market’s downtrend. We’ll certainly be keeping an eye on FX today.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – FAAMG Flatline, Record Crude Exports, GDPNow, New Home Sales – 10/26/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out tonight with a look at the historic underperformance of the FAAMG stocks as well as the outperformance of heavily shorted stocks (page 1). We then dive into the latest EIA data highlighting the record crude export number (page 2). We then review the latest trade balance data and its implications for GDP (page 3). Afterward, we recap new home sales (pages 4 and 5) before finishing with a look at the 5 year note sale held this afternoon (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 10/26/22

Chart of the Day – Another Curve Bites the Dust

Bespoke’s Morning Lineup — 10/26/22

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Solving big problems is easier than solving little problems.” – Google Co-Founder Larry Page

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Bulls have finally seen some green over the last couple of weeks. In fact, the S&P 500 has gained 1%+ on six of the last nine trading days. Below is a log chart of the S&P 500 since 1952 (when the 5-day trading week began) with red dots showing prior times the index has gained 1%+ on six of the prior nine trading days (the first occurrence in at least three months). As you can see, it is not common, and aside from the occurrence in March of this year, prior periods where this happened saw massive gains over the next six and twelve months.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.