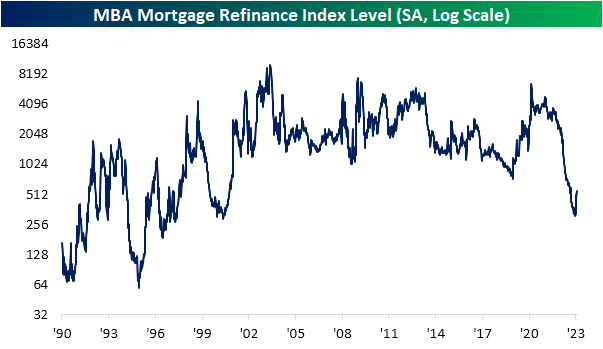

Refis Rise

Mortgage rates have come off of recent lows with the 30-year national average from Bankrate.com currently at 6.53%. While rates are not making new lows, those are much more attractive levels than last fall when they peaked well above 7%. On a rolling 3-month basis, the decline in mortgage rates continues to rank as some of the largest since the late 1990s (after the largest increase since the 1990s).

Given the alleviation on the rates front, purchase applications have been rebounding. The Mortgage Bankers Association’s weekly purchase application index is currently 19.2% above the post-pandemic low put in place in the first week of the year.

When rates were rising rapidly, massively stifling demand last year, refinance applications had taken a much larger hit than purchase applications. At the worst levels during the holidays, refinance applications reached the lowest level since May 2000. Since the start of the year, though, refinance applications have surged. Although there is still plenty of lost ground still to make up as applications continue to run below the past two decades’ range, the 68% month-over-month increase in applications has been the largest jump since March 2020 when applications doubled. Of all weekly readings since 1990, the current one-month increase ranks in the top 5% of all month-over-month moves on record. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke Briefs — Debt Ceiling

Fixed Income Weekly: 2/8/23

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report, we discuss what the short-term interest rate market is pricing.

Our Fixed Income Weekly helps investors stay on top of fixed-income markets and gain new perspectives on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Bespoke’s Morning Lineup – 2/8/23 – All Quiet

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I have civilized my own subjects; I have conquered other nations; yet I have not been able to civilize or to conquer myself” – Peter the Great

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

They say that you should never short a dull market, but that’s what seems to be the case this morning as futures are trading modestly lower despite a very quiet macro backdrop both here and abroad. Earnings season remains in full swing and a number of stocks are seeing big moves, but none of them are impacting much more than their respective shares let alone the broader market.

It’s hard to call the day-to-day performance of the equity market this year anything but impressive. Despite last Friday’s strong employment report and a continued hawkish (although no longer hawkish with a capital H) rhetoric from FOMC officials, the S&P 500 has managed to keep its rally intact. Just yesterday, it closed right near its YTD high from last Thursday. At the index level, every major US index ETF is currently at ‘overbought’ levels (greater than one standard deviation above its 50-day moving average) and all of them are in the green YTD with all but one (Dow Jones-DIA) up at least 8%.

Where things stand this year is a far cry from a year ago. At this point last year, all but one index ETF (DIA) was trading at oversold levels, they were all down YTD, and all but one (DIA) was down over 5% YTD.

Comparing the performance of these index ETFs this year versus last year provides an even clearer picture of the complete reversal. Indices that were down the most last year at this point like the Nasdaq 100 and the Russell 2000 are among this year’s biggest winners. Meanwhile, indices that experienced the least ‘damage’ at this point in 2022, like the Dow, have lagged so far this year. Another example? Of the 14 index ETFs we track in our Trend Analyzer, the seven ETFs that were down less than 7% YTD in 2022 are the only ones up less than 10% YTD in 2023.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

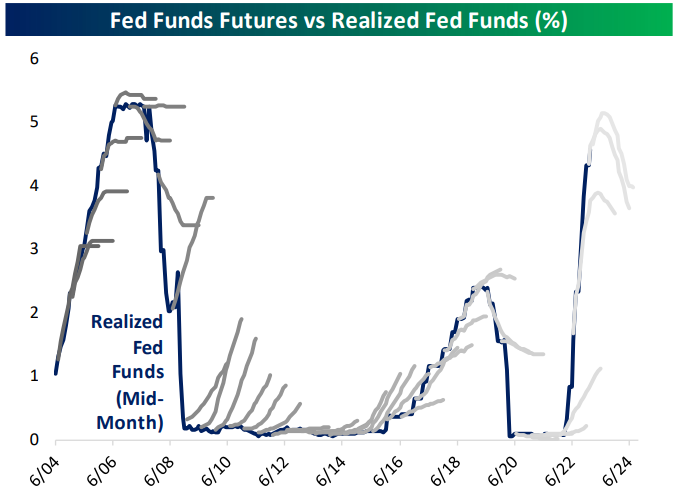

The Closer – Powell Raises the Terminal Rate – 2/7/23

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with earnings recaps (page 1) followed by a look at stock correlations and volatility (page 2) and the contango in crude, copper, and natural gas (page 3). We then review the latest consumer credit and trade balance figures (page 4) before switching to a look at the latest readings on supply chain stress (pages 5 – 7). We close out with a recap of the historically bad 3 year note auction (page 8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 2/7/23

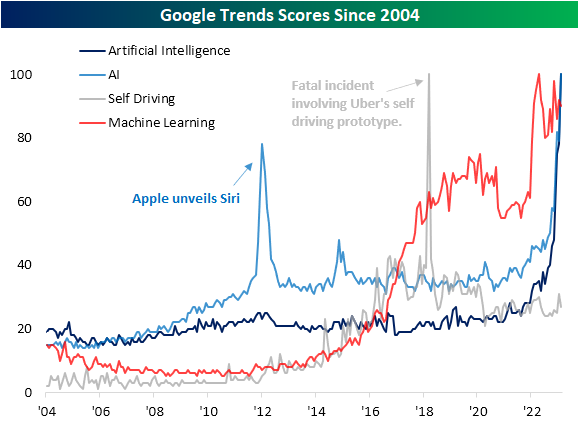

People All Over AI

In today’s Morning Lineup post, we compared Chat GPT’s rapid emergence into the mainstream to the rise of a number of other products. While Artificial Intelligence, or AI, has been a buzzword for some time now, this year it certainly has been in the spotlight more than in the past. Given the popularity of Chat GPT, some mega-caps like Alphabet (GOOGL) and Baidu (BIDU) have jumped in on the opportunity to announce their own versions. To quantify how in focus AI has become, below we show the Google Trends scores for a handful of related terms. Readings of 100 would indicate the peak in searches for a given topic globally.

Searches for “Artificial Intelligence” or its abbreviation have reached a new record while the field of “Machine Learning” has similarly seen searches rip higher and remain elevated in the past year. One interesting area which has not seen searches rise much is in regards to the automotive industry. Searches for “self-driving” have not picked up much within the range of the past few years. That is also well below the record from March 2018 when searches spiked due to a fatal incident involving Uber’s self-driving car. That being said, it is worth noting that even before the Chat GPT craze, these searches had been moving higher quite rapidly.

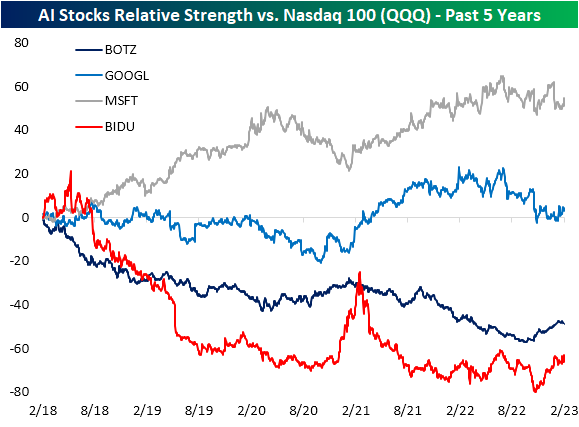

As we discussed earlier, although the broad topic of AI is in vogue, related stocks have not gotten much of a boost in reaction to this news. For those having made announcements regarding AI in recent days like Alphabet (GOOGL), Microsoft (MSFT), and Baidu (BIDU), relative strength versus tech more broadly (proxied by the Nasdaq 100 ETF (QQQ)) has not done anything too notable in terms of long term trends. For MSFT and GOOGL, relative strength has been sideways at best over the past year, and BIDU has been moving higher in recent months, but that follows a few rough years for the stock relative to US tech. The same can be said for a more encapsulating basket of AI-related stocks proxied by the Global X Robotics and Artificial Intelligence ETF (BOTZ). While the relative strength has been trending lower (meaning underperformance versus tech more broadly) the past few months have seen a rebound. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke Stock Scores — 2/7/23

Chart of the Day: Intraday Strength

$2.9 Trillion in Market Cap Added

After seeing the total market cap for the Russell 1,000 fall by $10.9 trillion in 2022, we’ve seen a rebound of $2.9 trillion in market cap so far in 2023. Below is a look at the total change in market cap by sector across the Russell 1,000 so far in 2023 and for all of 2022. The Tech sector saw its market cap fall $4.35 trillion last year, and it has seen its market cap rise by $1.176 trillion to start 2023. Consumer Discretionary’s market cap has risen by $701 billion, followed by Communication Services at $516.9 billion and Financials at $373 billion.

Four sectors have actually seen their market caps fall this year. Health Care’s market cap has fallen the most at -$141 billion, while Energy has fallen $57 billion, Consumer Staples has declined $32.2 billion, and Utilities has fallen $29.9 billion.

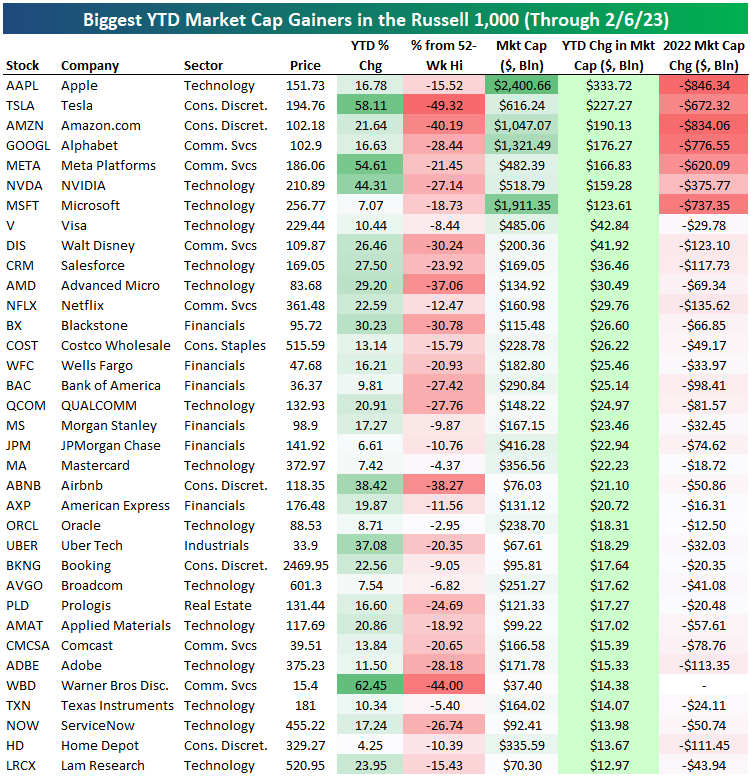

Below is a look at the biggest gainers in market cap so far this year at the individual stock level. Seven stocks have already gained more than $100 billion in market cap this year. Apple (AAPL) has jumped the most at $333.7 billion, followed by Tesla (TSLA) at +$227 billion, Amazon (AMZN) at +$190 billion, Alphabet (GOOGL) at +$176 billion, and Meta (META) at +$166.8 billion.

While the seven biggest gainers to start 2023 have added a combined $1.377 trillion in market cap, they lost a combined $4.86 trillion in market cap in 2022. Click here to start a two-week trial to Bespoke Premium.