Bespoke’s Morning Lineup – 2/24/23 – Victory or Death

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I shall never surrender or retreat.” – Sam Houston

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Equity markets are poised to open lower this morning, and the tone has been weakening all morning as futures are right near their lows of the morning. Treasury yields and crude oil are higher, but the moves aren’t really enough to justify the magnitude of the decline in equity futures. Boeing (BA), which is down 3% in the pre-market, helps explain the weakness in Dow futures, but that doesn’t explain the weakness in S&P 500 and Nasdaq futures, which are actually down even more than the Dow.

There’s a lot of economic data to go through this morning. It started with Personal Income and Spending as well as PCE which were just released and will be followed by New Home Sales and Michigan Confidence at 10 AM. In terms of the early data, it wasn’t market-friendly. Personal Income was weaker than expected (0.6% vs 1.0%) while Personal Spending was higher than expected (1.8% vs 1.4%), so consumers are earning less and spending more. Maybe that’s due to higher-than-expected inflation where the headline PCE came in at 0.6% vs 0.5% m/m. Core was even worse relative to expectations coming in at a level of 0.6% versus 0.4% estimates m/m. As you’d expect, equity futures have sold off in reaction to the news while interest rates are higher. with the two-year on pace to close at a new high yield for the cycle.

When looking through the various sector price charts, there were several significant reversals just as they tested (or briefly broke below) some key moving averages. As shown in the charts below, Communication Services, Energy, Consumer Staples, Health Care, and Consumer Discretionary all reversed higher to varying degrees after trading down around their 200-day moving averages (DMA). In addition to those five sectors, Financials, Industrials, and Real Estate all managed to stage similar reversals as their 50-DMAs came into play.

Given this morning’s early weakness and the disappointing economic data, it may look like it was all for nothing. However, if markets can find a way to erase this morning’s weakness and close out the week on a positive note, that lack of surrender will be a difficult trend to ignore.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – GDP Revisions, Bank Checkup, EIA – 2/23/23

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we discuss GDP revisions released today along with a status check on banks, data on petroleum markets. and an earnings review from 10 different stocks that reported after the bell today.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Chart of the Day: US Refined Products Demand Remains Weak

Bespoke’s Morning Lineup – 2/23/23 – A Volatile Rally

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Intuition will tell the thinking mind where to look next.” – Jonas Salk

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It may be the shortest month of the year, but after four straight days of declines for the S&P 500, February is seeming like a long month. This morning, futures are looking to reverse their losing ways, but based on some of the intraday selloffs we’ve seen in recent days, you can’t be too sure of anything. February’s weakness has put a damper on individual investor sentiment as the weekly survey from AAII showed that bullish sentiment plunged from 34.1% down to 21.6%. February hasn’t been a fun month so far, but when you consider the fact that the 10-year yield is up over 40 basis points MTD, it could have been a lot worse than a 2% decline for the S&P 500 and a decline of less than 1% for the Nasdaq.

We just got a slug of economic data with GDP, Personal Consumption, Core PCE, and Jobless Claims. Results relative to expectations were mixed. GDP was revised lower, both initial and continuing jobless claims were lower than expected, while Core PCE was higher than expected at 4.3% vs forecasts for 3.9%. As one might expect given the stronger inflation data, equity futures have seen a modest decline in the immediate aftermath of the report while interest rates are higher.

Even after this month’s weakness, the S&P 500 is still up nearly 4% YTD, but those gains have come with a good deal of volatility. Yesterday was the 35th trading day of the year, and already nearly half of all trading days have seen daily moves of at least 1%. Going back to 1953 which was the first full year of the five-trading day workweek, there have only been five other years where there were as many or more 1% moves in the first five trading days of the year. Of the five prior years where 17 or more of the first 35 trading days were moves of 1% or more, the only year where the S&P 500 was up YTD was 1988 (+7.51%). In all four other years, the S&P 500 was down in the first seven weeks of the year with losses ranging from 3.6% in 2003 to a plunge of 17.7% in 2009.

That’s the past. Looking ahead, of the five prior years shown, that volatility to start the year was followed more often than not by gains. In four of the five years shown below, the S&P 500 was higher for the remainder of the year. The only exception was a big one when in 2008, the S&P 500 started the year off with a decline of 8.5% in the first 35 trading days of the year and then went on to drop an additional 32.7% for the remainder of the year.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Fed Minutes, Quantifying EV Battery Needs, Dollar, 5y Auction – 2/22/23

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we talk about earnings covering chips, the shale patch, platform companies, and casual dining. We then discuss today’s Fed minutes, the nascent uptrend in the dollar, and the rapid dislocation of metals markets that support EV battery markets.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

The Bespoke Triple Play Report — 2/22/23

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with above-expectations results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 23 stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Fixed Income Weekly: 2/22/23

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report, we discuss the divergence between crude and breakevens as well as what that implies for the future of both.

Our Fixed Income Weekly helps investors stay on top of fixed-income markets and gain new perspectives on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Chart of the Day – Record Six-Month Decline for Natural Gas

Bespoke’s Morning Lineup – 2/22/23 – Miracles Anyone?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Do you believe in miracles? YES!” – Al Michaels

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

43 years ago today, the US men’s national hockey team shocked the world by defeating the dominant Soviet team in what everyone now knows as the “Miracle on Ice”. Today, faced with stubborn inflation, high-interest rates, lofty valuations, and numerous other concerns, a miracle isn’t the only way out of the current predicament for bulls, but after a sell-off like yesterday’s, it may seem that way. Futures are actually modestly positive in early trade, but hardly in a convincing way. The economic calendar is quiet this morning, but we’ll get the release of the Fed minutes from the previous meeting at 2 PM Eastern.

Yesterday’s plunge in stocks capped off what has been a pretty lousy five days for stocks as the early-year glow in the equity market has lost some of its shine. Every sector in the S&P 500 has traded down over the last five trading days. The least damage has been done in the Consumer Staples and Utilities sectors which are both down less than 2%. Leading the way to the downside, more than half of sectors are down over 3% with Energy leading the way falling over 6.5%. Energy is also one of four sectors down YTD and is the third worst-performing sector YTD.

Sometimes, when you’re watching a game you look at the scoreboard and think, how are we not down even more? The Energy sector has that feeling now. As we noted yesterday, crude oil isn’t far from 52-week lows, and to call the drop in natural gas a free-fall may be an understatement. Earlier this morning, front-month futures briefly dropped below $2 per million BTUs which is a level it hasn’t traded to very often over the last 20+ years. Six months ago, it was close to $10! If someone showed you the charts of oil and natural gas and gave you no other information regarding the state of the economy, the last thing on your mind would be inflation.

Our Morning Lineup keeps readers on top of earnings data, economic news, global headlines, and market internals. We’re biased (of course!), but we think it’s the best and most helpful pre-market report in existence!

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Closer – Rates Surge, Housing Mixed, PMIs Bounce – 2/21/23

Log-in here if you’re a member with access to the Closer.

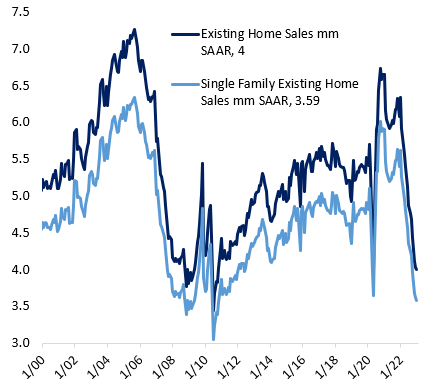

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we review after-the-bell earnings results including companies dealing in crypto, RVs, and housing. We also take a look at moves in interest rates, existing home sales, PMI data, and the latest Treasury auction.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!