Morning Lineup – Tell Us Something We Don’t Know

ADP Private Payrolls for February were just released and came in slightly weaker than expected at 183K versus estimates for a reading of 190K. Futures are indicated modestly lower but are near their overnight highs, while oil is down and the dollar is on pace for its 6th straight positive day. Read all about everything driving the markets in today’s Morning Lineup.

Bespoke Morning Lineup – 3/6/19

One of the events getting some headlines this morning is the fact that the OECD has lowered global growth forecasts for both 2019 and 2020. Reasons behind the downgrade include trade disputes and uncertainty over Brexit. Is this really newsworthy? After all, it’s not as if any of these headwinds are anything new. The fact is that economic data around the world has been underwhelming for some time now. Check out the chart below of the Citi Economic Surprise Index for G10 economies. At a level of -34.10, it is currently just off what were its worst levels since 2012.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer — Markets Pause, Global Credit Growth Slows, New Home Sales Bounce — 3/5/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, on a quiet day in macro data, we make note of the broken uptrends given the recent pause in stocks and high yield credit. We then take a look at the lack of movement in the VIX and breadth in Europe. Turning to macro data, we analyze the Bank of International Settlements (BIS) quarterly credit data which showed significant slowing. We finish with a look at today’s New Home Sales report which beat estimates giving a bit more of an optimistic tone to housing.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke’s Matrix of Economic Indicators: 3/5/19

Our Matrix of Economic Indicators is the perfect summary analysis of the US economy. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Bespoke’s Consumer Pulse Report — February 2019

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

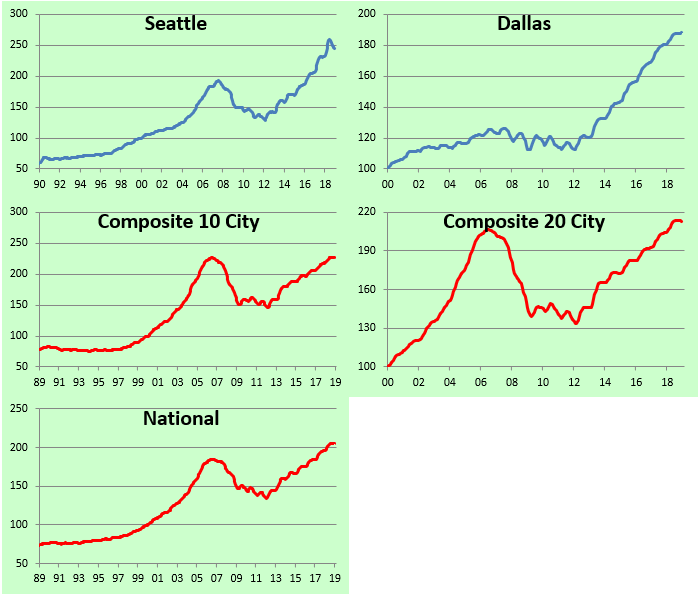

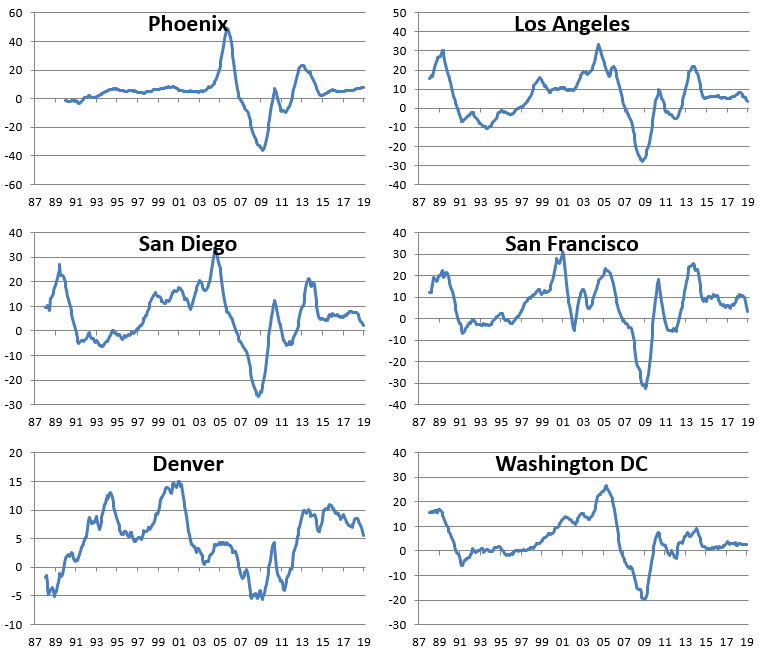

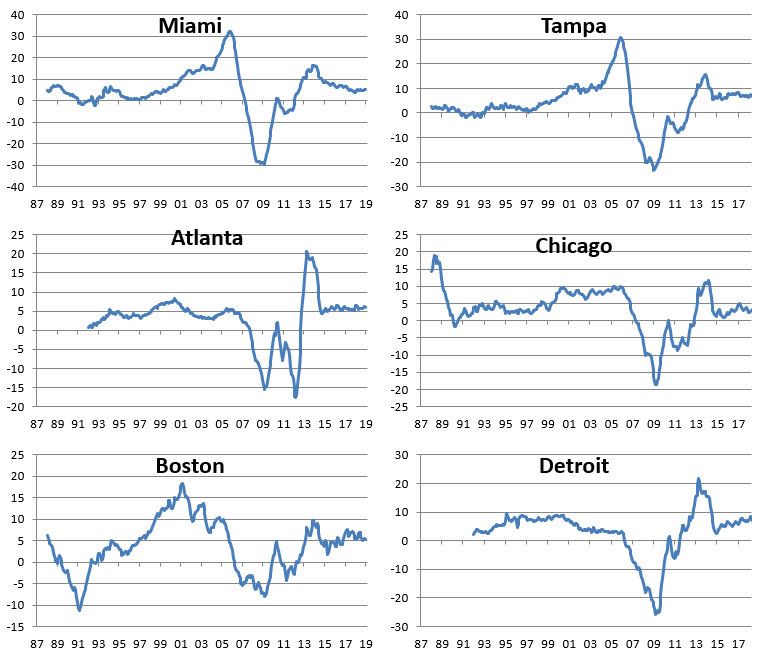

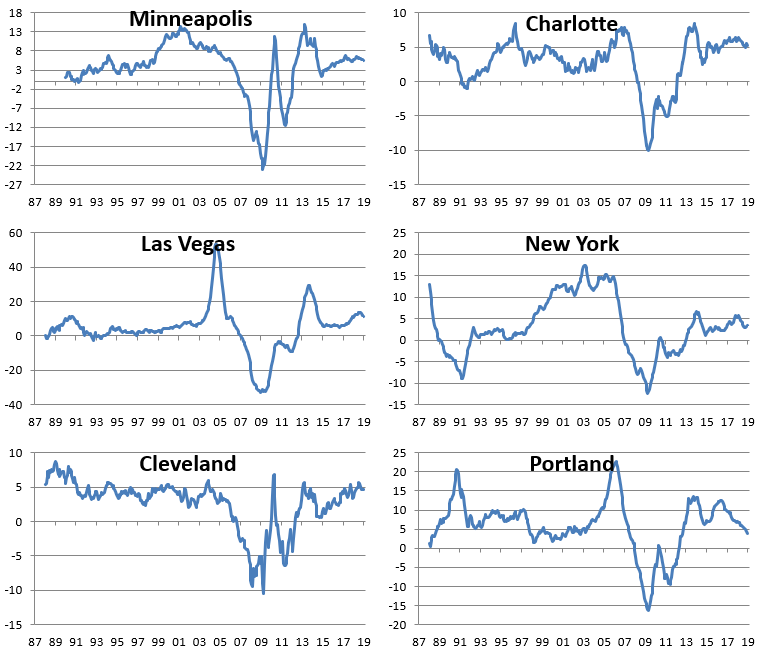

2018 Home Price Trends for Major US Cities/Regions

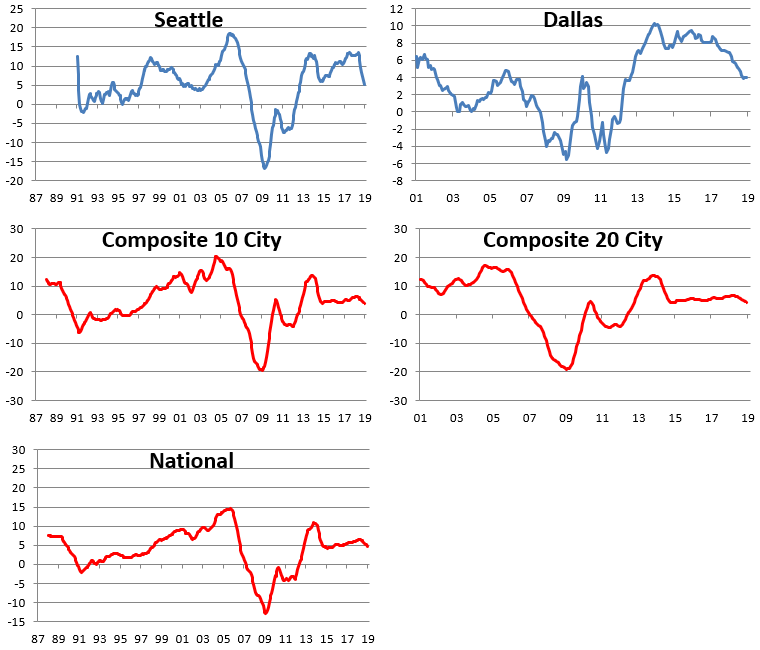

The most recent Case Shiller home price data for the 20 cities tracked was released last week, and below we have updated a number of charts and tables that we’ve published on a regular basis over the years. The first table shows the month-over-month and year-over-year change in home price values across the country. After years of seeing all green in this table, we’ve seen a string of month-over-month declines recently. The composite 10-city and 20-city indices both fell 23 basis points in December, while the “National” index saw home prices dip 14 basis points.

San Francisco saw the biggest month-over-month decline at -1.43%, followed by Chicago (-0.70%), San Diego (-0.69%), and Seattle (-0.63%). Seven of twenty cities saw small month-over-month gains, led by New York and Las Vegas at +0.17%.

On a year-over-year basis, every city still posted home price gains, but those gains are getting smaller and smaller as the months progress.

The chart below shows how much each city has seen home prices gain off of their housing crash lows that were put in sometime between 2010 and 2012 for most cities. San Francisco is up 128% off of its lows, while Las Vegas and Detroit are both up more than 100% as well. The National index is up 53% off of its low, while New York home prices have bounced the least at just 25%.

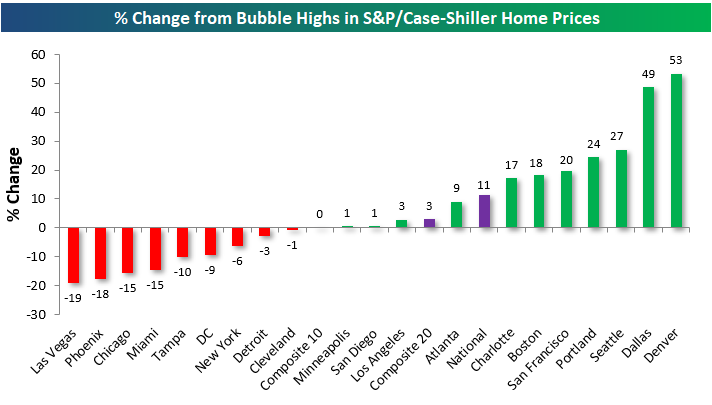

The next chart shows where home prices stand for each city relative to their peak during the housing bubble of the mid-2000s. The National index is up 11% from its prior all-time high that was made in July 2006. Denver prices have soared the most above their prior highs at +53%, followed by Dallas at +43%. On the flip side, Las Vegas is still the furthest below its housing bubble highs from the mid-2000s at -19%. Phoenix, Chicago, Miami, and Tampa are all still 10%+ below their prior highs as well.

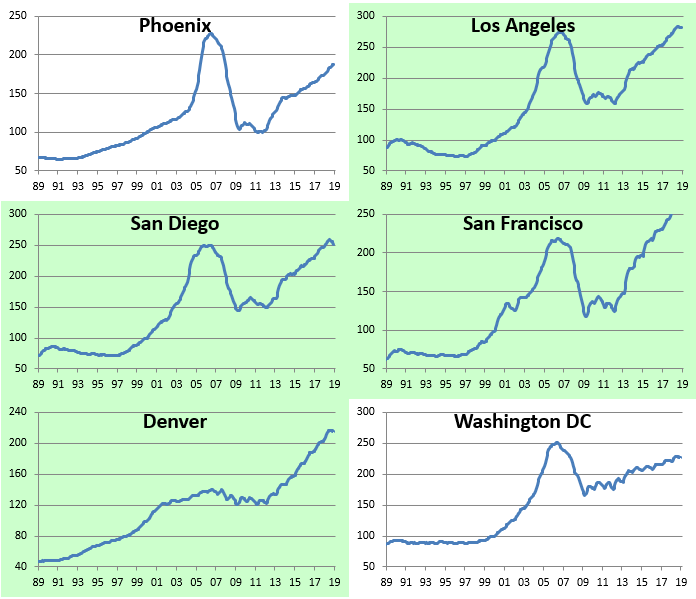

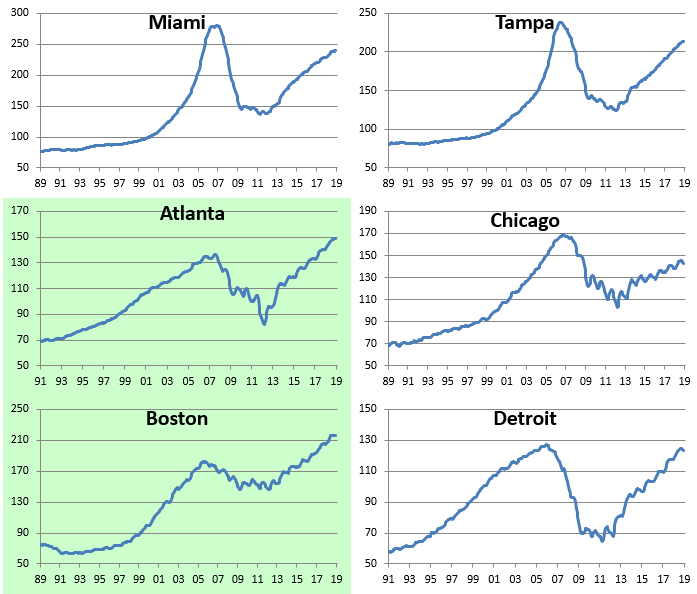

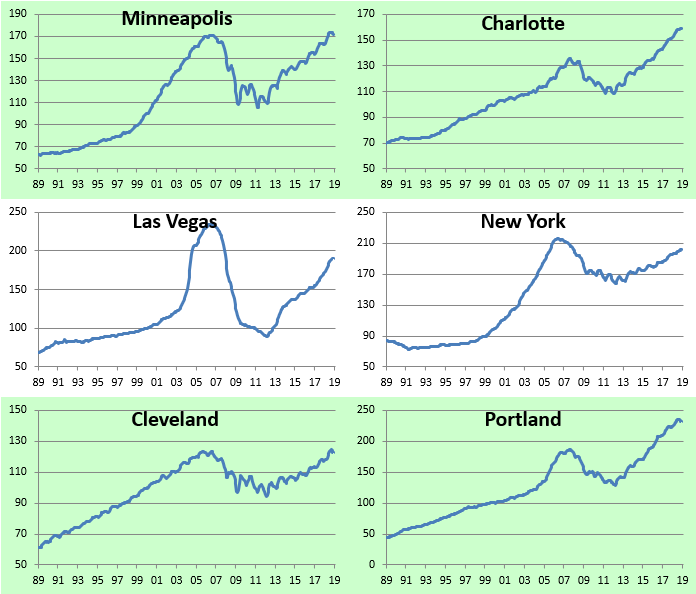

Below we provide charts showing home price levels over the last 30 years for the cities tracked by Case Shiller. Cities highlighted in green have taken out their prior housing bubble highs, while cities not highlighted are still below their prior all-time highs.

The next set of charts shows the rolling year-over-year change for home prices in each of the 20 cities tracked. You’ll notice that home price appreciation for the National and Composite indices has begun to turn lower, although it’s still important to remember that it’s positive. Cities like Portland, Denver, Seattle, and Dallas have seen some of the steepest drops in home price growth, but again, every city is still in the green on a year-over-year basis for the time being.

Bespoke Stock Scores — 3/5/19

Chart of the Day: Breadth Stays Strong

No Slowdown in Services Sector

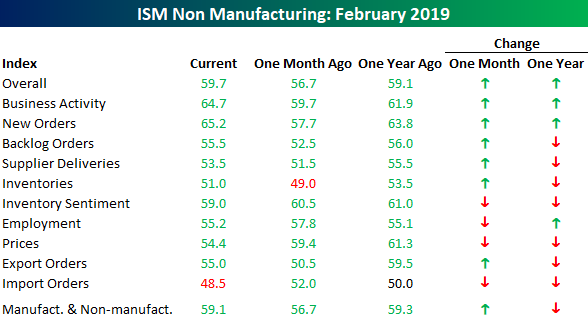

If this is a slowdown, we’ll take it. While economic data clearly slowed in December and January due to a combination of equity market weakness, the government shutdown, and other factors, activity really appears to have bounced back in February. In the case of the ISM Non-Manufacturing report, February not only increased versus January’s reading of 56.7, but it also came in higher than the consensus expectation of 57.4. At 59.7, February’s report was just slightly more than one point below the cycle high of 60.8 from back in September.

On a combined basis and accounting for each sector’s share of the total economy (second chart), the February ISM came in at 59.1 which was nearly two points below the cycle high of 60.7 from back in September. Following the strength of this report, the market is now once again pricing in a higher chance that the FOMC hikes rates between now and next January (8.9%) versus cutting rates (5.6%). Meanwhile, the odds that the FOMC sits on its hands between now and then are at just under 86%. Normally, we would say the odds of the FOMC doing nothing are extremely low, but now that they have the balance sheet to tinker with, a long pause on the Fed Funds rate is certainly a possibility.

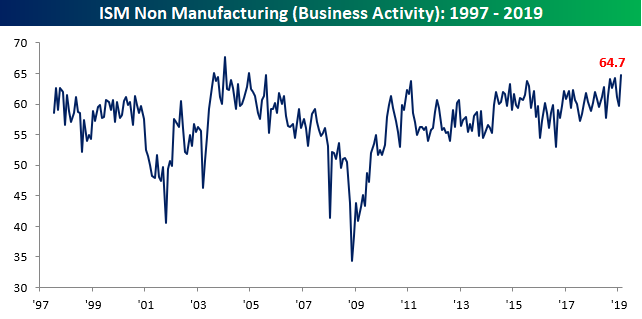

The table below breaks down February’s report by each of its sub-components. On a m/m basis, this month’s report saw solid breadth, although versus where things stood a year ago the pace of growth has been less robust. The real stars of this month’s report, however, were Business Activity and New Orders (two charts below table). Business Activity rose to 64.7, which is the highest reading that component has seen since August 2005! New Orders saw an even more impressive move. While it also reached its highest level since August 2005, the m/m increase of 7.5 points was the third largest on record behind only the 9.6 point jump in April 2009 and the 8 point rise in February 2002. Pretty impressive!

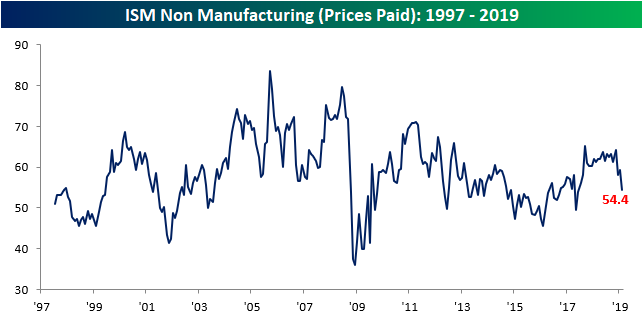

On the downside, Prices Paid saw the largest m/m decline of any component, falling from 59.4 down to 54.4 to its lowest level since June 2017. Behind Prices Paid (lowest chart), the only other components to decline on a m/m basis were Import Orders, Employment (which doesn’t necessarily bode well for Friday’s Payrolls report), and Inventory Sentiment.

Earnings Slow to a Crawl as Top-Line Beat Rate Continues to Increase

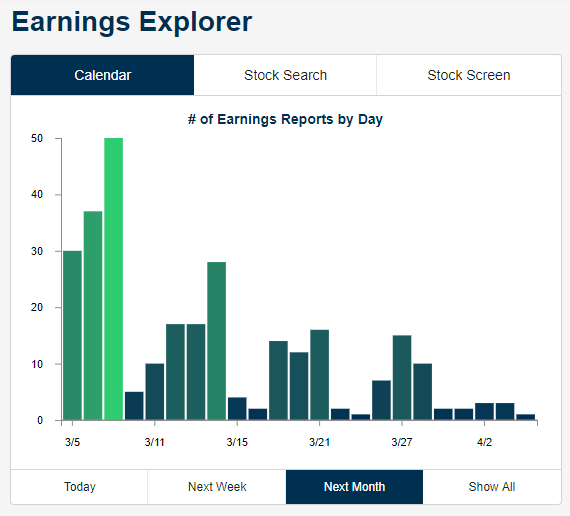

As shown in the chart below from our Earnings Explorer tool, the number of earnings reports slows to a crawl in the weeks ahead. While there are still a lot of companies set to report this week, including a number of big retailers like Kroger (KR), Costco (COST), Dollar Tree (DLTR), Ross Store (ROST), by next week we’ll get only about 20 reports per day. At the end of March and early April, we’ll only see 5-10 reports per day before things pick back up again in mid-April when Q1 reports start to roll in.

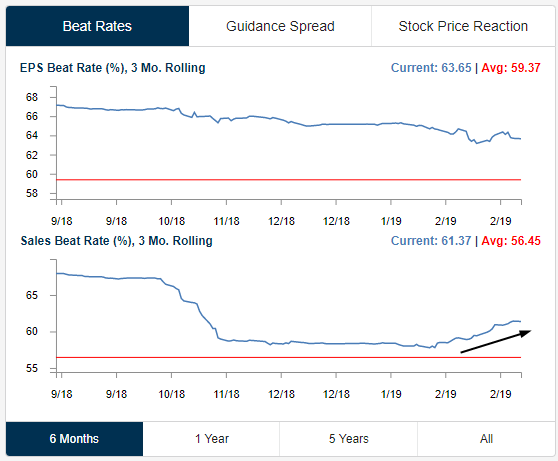

One positive we continue to monitor is the pick-up that we’ve seen in top-line revenue beat rates. Below are two charts from our Earnings Explorer tool — the first shows the 3-month rolling earnings per share beat rate, while the second shows the 3-month rolling revenue beat rate. While bottom-line beat rates continue to trend slightly lower, we have seen a steady increase lately in top-line beats. This means that either the analysts providing revenue estimates got too bearish, or companies have managed to surprise the market with stronger revenues (or a combination of both).

Trend Analyzer – 3/5/19 – Last Three

As we have seen over the past few days, in the midst of some choppy price action, the major index ETFs continue to shed their downtrends. In spite of declines yesterday, there are once again fewer ETFs in downtrends than the prior day. Currently, there are only three that remain in downtrends. Each of these three are small-cap focused ETFs (IJR, IWC, IWM). Ironically, these are also some of the best performing members of the major index ETFs year to date. The Russell 2000 (IWM) and Micro-Cap (IWC) are the top two performers up 17.11% and 16.34% YTD, respectively.

Turning to performance over the past week, things are unfortunately not as positive. There are only two ETFs that have managed to edge out gains: the S&P 100 (OEF) and the Nasdaq (QQQ). All others have seen declines ranging from only a few basis points to 1.65%. These declines have also shifted the overbought/oversold conditions that we have been observing over the past few weeks. Whereas everything has been solidly overbought, and each ETF still has an overbought rating, it is currently much less firmly so.