Chart of the Day – Big Turnaround in Small Business Sentiment

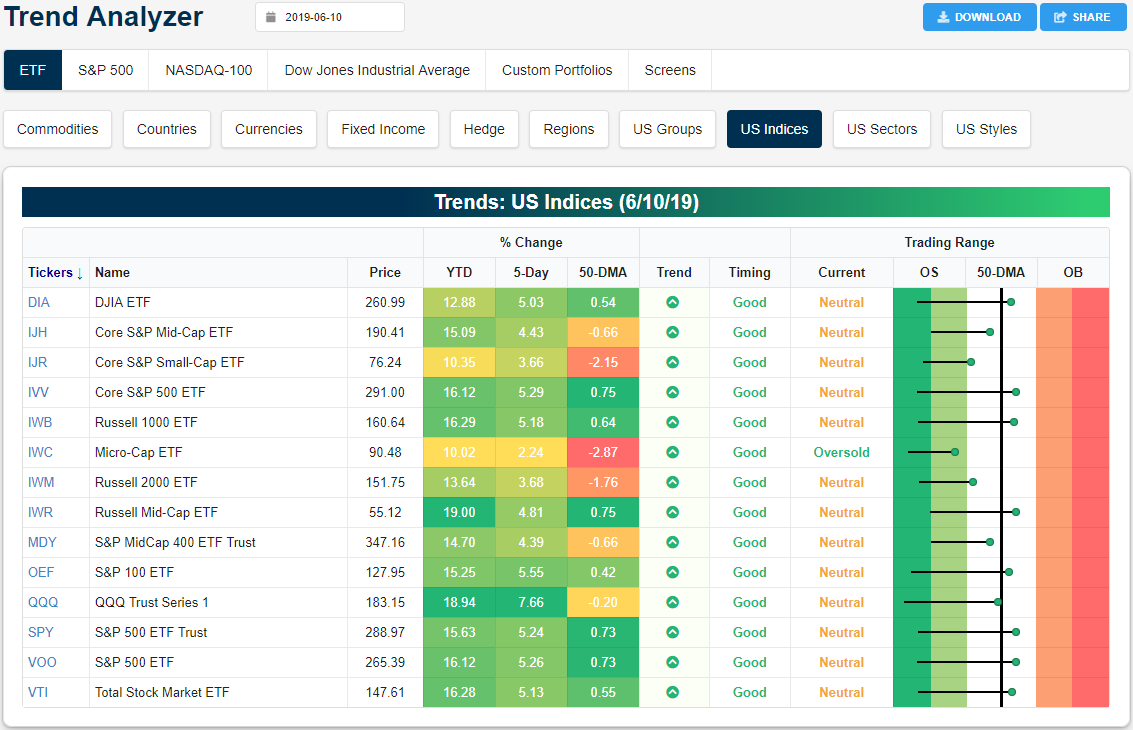

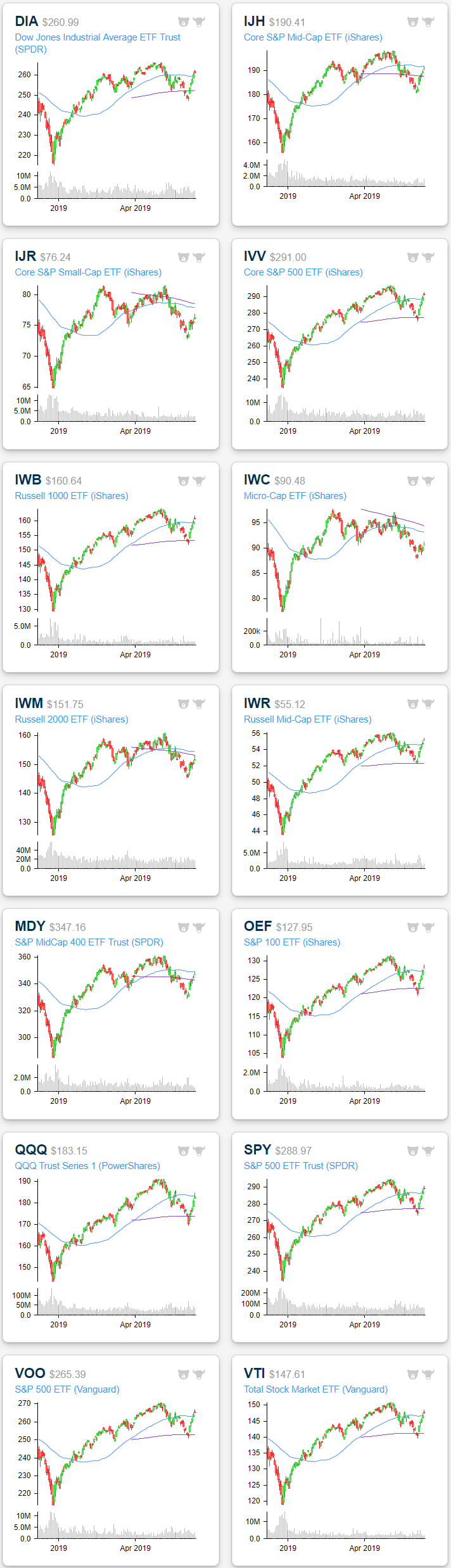

Trend Analyzer – 6/11/19 – Back Above the 50-Day

Equities are looking to keep the streak of gains going today which over the past week has brought all of the major index ETFs—except for the Micro-Cap ETF (IWC)—out of extremely oversold territory and into neutral. As shown in the Trading Range section of our Trend Analyzer tool, the long tails to the left indicate the rapid moves from oversold levels for all of these indices. The move has been strong enough to lift more than half of the ETFs above their 50-DMAs. Large caps especially have moved the highest above this moving average. Small-caps, on the other hand, have continued to lag the rest of the market. The aforementioned IWC has seen the smallest gains of only 2.24% in the past week and is still 2.87% below its 50-DMA. Conversely, the Nasdaq (QQQ) has rocketed the most, rising 7.66% in the past five days. And still, QQQ remains under the 50-day!

Looking at the charts of the these ETFs, while they have mostly broken through resistance at the moving averages, yesterday’s session did show signs of exhaustion as they sold off from the intraday highs as some like the Dow (DIA) or Core S&P 500 (IVV) even continued to fall below the opening price (resembling the shooting star pattern). While this may be a bit of a sign of hesitation in the current rally, these ETFs have also recently broken out of their short term downtrends. In other words, the technical picture of the major indices has improved even if the rip higher from the past week takes a breather. Start a two-week free trial to Bespoke Institutional to access our interactive Trend Analyzer, Chart Scanner, and much more.

Construction Openings Surge

Yesterday, the BLS released its April Job Openings and Labor Turnover Survey (JOLTS). The JOLTS report allows for a deeper look at the labor market beyond the plethora of statistics included with the monthly Employment Situation Report (which is best known for its Non-Farm Payrolls number). Overall, the JOLTS report showed robust openings levels, cycle highs for quit rates, strong gross hiring, and very slow layoff rates — a generally positive set of indicators for the US labor market.

The most interesting data point in the survey came from job openings at the industry level. Opening levels in the construction industry surged 11% MoM and 40% in two months to a record level. Typically, openings levels are a leading indicator for employment numbers in the construction industry, as shown in the first chart below. The uptick in openings could represent a pending surge in construction hiring (and therefore, activity).

On the other hand, construction openings haven’t consistently led residential construction activity (as measured by housing starts — 2nd chart below), proving a lagging indicator during the last cycle and a coincident one for most of this one.

The same is true for construction spending numbers, which captures residential spending correlated to starts and the nonresidential sector. The surge in construction openings actually looks a bit like the mid-2000s, with modest declines in spending off peak levels taking place as openings continue to surge. While the recent explosion in openings is interesting, it’s hard to be sure whether it’s a positive or negative sign for the construction industry. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Morning Lineup – Small Business Sentiment Back on Track

After five straight months of declines from an all-time high back in August, it appears as though small business sentiment has gotten back on track. This morning’s release of the NFIB Index of Small Business Sentiment showed a larger than expected increase as the headline index came in at a level of 105.0 compared to estimates for a reading of 102.0. While the index is still off its record high of 108.8 from last August, it has risen for four straight months now, which is tied for the longest streak of increases since the four months that followed the 2016 election.

In other news, foreign equity markets are in rally mode once again despite relatively weak economic readings. In the US, PPI will be released shortly, but as the President already tweeted, “The United States has VERY LOW INFLATION, a beautiful thing!” Please read today’s Morning Lineup for our latest take on events from overnight and this morning.

As markets have started to recover, the yield curve is still inverted (as it has been for the last three weeks), but it has become less so over the last six trading days. As shown in the chart below, the curve has steepened from a low of negative 25 bps on June 3rd to 9 bps this morning. That’s the largest six-day steepening since October.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer – Fed Pricing, JOLTS – 6/10/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we show what the two year Treasury note is pricing in terms of the policy rate over the next two years and how this plays into multiple scenarios. We also look at how equities performed the last time markets were pricing in cuts this aggressively. We then look at this morning’s JOLTS report which still showed strong demand for labor.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

B.I.G. Tips – Fed Easing Cycles

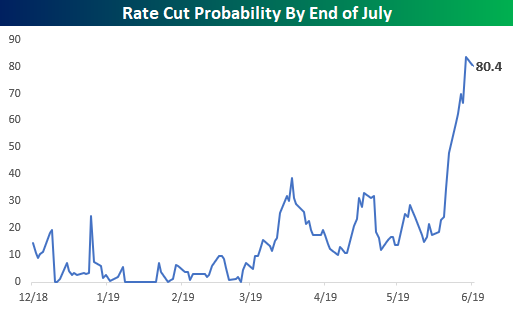

After the last ten to twenty years of market ups and downs, it takes a lot to surprise experienced investors. One recent trend that qualifies, though, is the rapid and aggressive pricing of Fed rate cuts in the coming months. The futures market is pricing in over an 80% chance that the FOMC will cut rates between now and the end of July. This comes even as there has been an absence of any overwhelmingly supportive or consistent commentary from Fed officials suggesting that rate cuts are imminent.

With rate cuts likely on the horizon, it’s time to look back at prior rate-cutting cycles from the FOMC to see how equities performed leading up to and after the first cut in an easing cycle. To do this, we looked at all prior periods in the last thirty years where the FOMC cut rates at least three times after a series of hikes. While we could have gone back further in our analysis, the last thirty years essentially covers the period since Greenspan became the Fed chair, and it also wasn’t even until 1994 that the FOMC actually announced what the interest rate policy was on the day of their meetings. Therefore, the further you go back in time the less relevance there is to circumstances today. Interestingly enough, at 1,272 calendar days and counting, the current rate hike cycle has been the longest of the last 30 years. Our latest B.I.G. Tips report provides an insightful look at the stock market’s performance during prior rate cut cycles. To see the report, sign up for a monthly Bespoke Premium membership now!

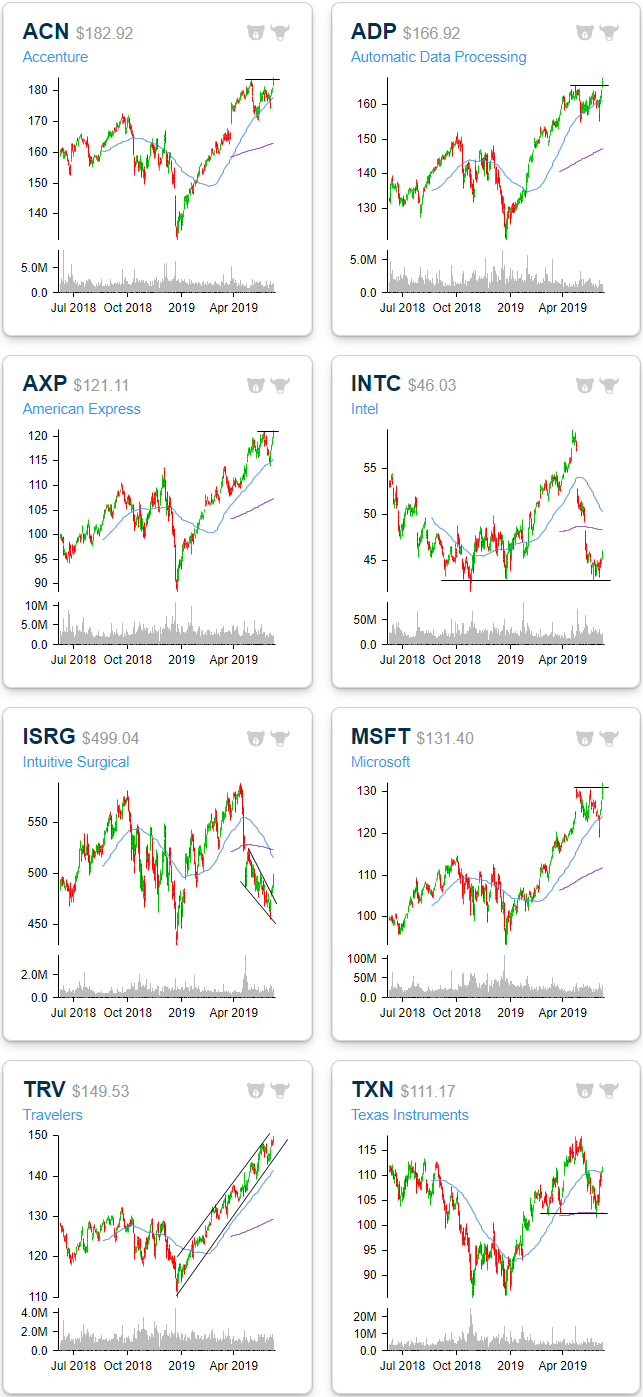

Rally Leads to Breakouts

Below are a handful of charts we wanted to highlight after browsing through our Chart Scanner tool over the weekend.

The strong rally off of oversold levels last week was a tide that lifted just about all boats. This was a sigh of relief for some individual stocks that have been breaking down recently like two of the semis, Intel (INTC) and Texas Instruments (TXN). Since the end of April, tariff talks had been hitting the semiconductor stocks hard. In INTC’s case, this also played a role in lowered guidance in the most recent earnings report on April 25th. These declines brought TXN down to the 200-DMA in addition to lows from earlier in the year and INTC all the way back down to 2018 lows. Both have found support at these levels, though, and last week’s rally was a sizeable bounce off of this support. TXN has even now managed to retake its 50-DMA. Similarly, Intuitive Surgical (ISRG) has been pretty volatile over the past year and since April has been in a short term downtrend and oversold. Last week’s price action helped to break the stock out of this downtrend.

Other stocks have been stronger in the past year and sit in longer-term uptrends. Traveler’s (TRV), for example, has been trading in a steady uptrend all year with last week’s gains bringing it to the upper end of this channel. Others like Accenture (ACN), Automatic Data Processing (ADP), American Express (AXP), and Microsoft (MSFT) have broken out to new highs. This is after all four constructively found support at their 50-DMAs. Start a two-week free trial to Bespoke Institutional to access our interactive Chart Scanner and much more.

Broad Participation During Last Week’s Rally

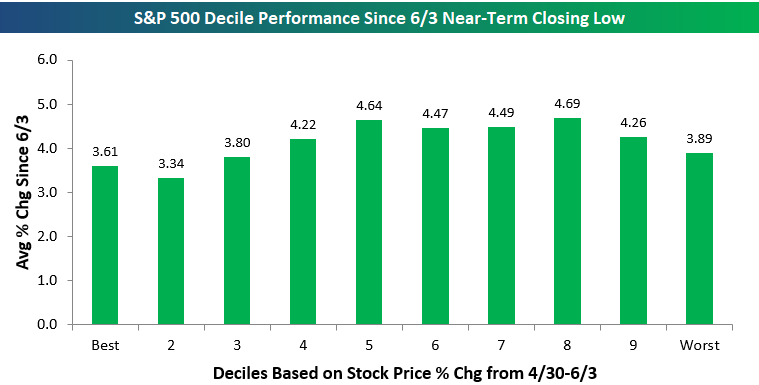

The average stock in the S&P 500 has gained 4.14% since last Monday’s near-term closing low. Usually, when we see such a strong bounce after a period of weakness, we see the stocks that were down the most during the pullback rally back the most during the bounce. That hasn’t been the case this time around, though.

We broke the S&P 500 into deciles (10 groups of 50 stocks) based on stock performance during the market’s pullback from 4/30-6/3. We then calculated the average performance of the stocks in each decile since 6/3. As shown in the chart below, each decile has seen an average gain between 3.34% and 4.69%. The stocks that held up the best during the pullback are up an average of 3.61% since 6/3, while the stocks that fell the most during the pullback are up an average of 3.89%. We usually see more disparity between these two deciles in this type of market environment. Instead of bidding up the biggest losers during the sell-off, last week’s rally was much more evenly distributed.

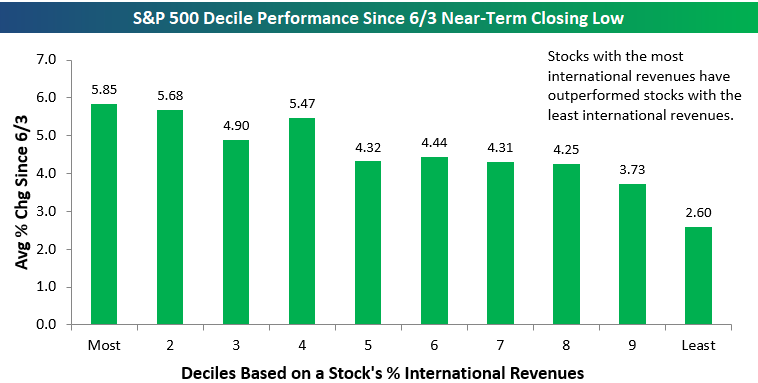

One stock characteristic that did have an impact was international revenue exposure. During the market’s sell-off in May on trade fears, S&P 500 stocks that generate the bulk of their revenues outside of the US were crushed. Stocks with all domestic revenues that are much more insulated from tariffs held up much better in May.

We’ve seen outperformance from stocks with heavy international revenue exposure since last Monday. As shown below, the decile of S&P 500 stocks with the most international revenues has posted an average gain of 5.85%, while decile 2 has posted an average gain of 5.68%. On the flip side, stocks with nearly all domestic revenues are only up 2.6% on average since last Monday.

The “internationals” are still down quite a bit from their Q1 highs, so if trade concerns continue to ease, these stocks stand to benefit the most. Bespoke maintains an “International Revenues” database that allows subscribers to find the geographic revenue breakdown for all stocks in the Russell 1,000 and S&P 500. (Click here to access.) It’s a very useful tool if you’re looking for buying or selling opportunities in the current market environment. Start a two-week free trial to Bespoke Premium to unlock our International Revenues tool!

Chart of the Day: Can Materials Keep Going?

Gauging the Bounce

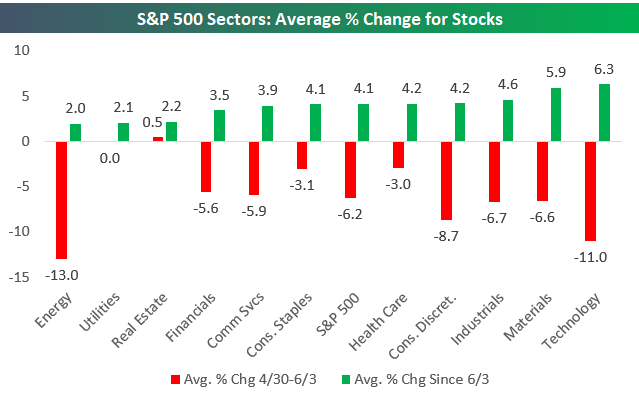

The average S&P 500 stock fell 6.2% from 4/30 (when the index made its last all-time closing high) through last Monday (June 3rd). Since the close last Monday, the average stock in the index has bounced back 4.1%.

Below is a look at how stocks within sectors have performed recently. During the pullback from 4/30 to 6/3, Energy stocks fell the most of any sector at -13%. Energy stocks have also bounced back the least since 6/3 with an average gain of just 2%. Technology stocks fell the second most during the pullback with an average decline of 11%, but Tech has bounced back the most since 6/3 with an average gain of 6.3%.

Notably, some sectors have seen average gains since 6/3 that are bigger on an absolute basis than the declines they saw during the pullback. The average Utilities stock was flat from 4/30-6/3, but since then the average stock in the sector has rallied 2.1%. The average Real Estate stock actually gained from 4/30-6/3, and since then the sector has seen an average gain of 2.2%.

Consumer Staples and Health Care both saw average declines of roughly 3% during the 4/30-6/3 pullback, and they have bounced back by an average of just over 4% since 6/3.

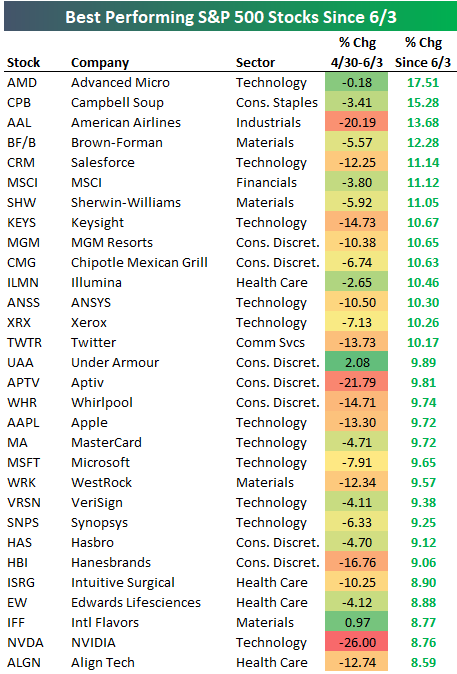

Below is a look at the best performing stocks since the S&P’s recent closing low on 6/3. Advanced Micro (AMD) is up the most of any stock in the S&P with a gain of 17.51%. Campbell Soup (CPB) — a company that couldn’t be much more different than AMD — is up the second most since 6/3 with a gain of 15.28%. American Airlines (AAL), Brown-Forman (BF/B), and Salesforce (CRM) round out the top five with gains of more than 11% each. Other notables on the list of winners include Chipotle (CMG), Twitter (TWTR), Under Armour (UAA), Apple (AAPL), MasterCard (MA), Microsoft (MSFT), and NVIDIA (NVDA). Start a two-week free trial to Bespoke Premium to unlock our premium research and investor tools!

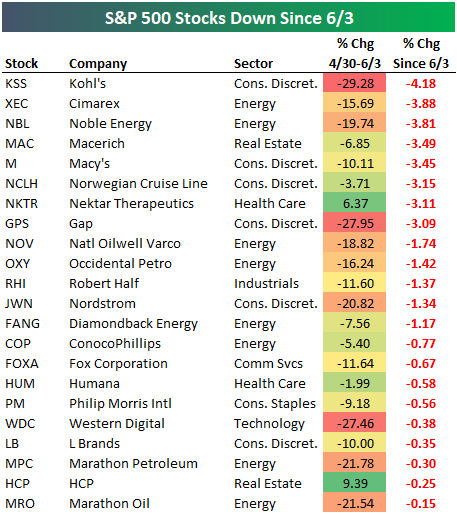

Below is a list of the 22 stocks in the S&P 500 that have the distinction of being down since last Monday. Kohl’s (KSS) is down the most with a decline of 4.18%, followed by Cimarex (XEC), Noble Energy (NBL), and Macerich (MAC). Other notables include retailers like Macy’s (M), Gap (GPS), Nordstrom (JWN), and L Brands (LB).