Bespoke’s Morning Lineup – Ten for Ten

As of this writing, ten companies have reported earnings this morning and all ten have exceeded bottom-line forecasts, so that’s encouraging. As far as revenues are concerned, the results haven’t been as positive with only six companies exceeding top-line forecasts. The biggest winner so far this morning is Goldman Sachs (GS), which is up over 1% after crushing forecasts. On the downside, Domino’s (DPZ) is having a rough morning with a loss of 5% after revenues came up short of forecasts.

In economic news, Import and Export Prices both saw larger than expected declines, while Retail Sales came in stronger than expected. Futures, which had reversed earlier losses remain positive after the report.

Read today’s Morning Lineup to get caught up on news and stock-specific events ahead of the trading day and a further discussion of overnight events including an analysis of the latest ZEW Sentiment Surveys.

Bespoke Morning Lineup – 7/16/19

Yesterday, we mentioned that there had been a modest expansion in new highs among S&P 500 stocks as over 13% of stocks in the index hit 52-week highs even as the S&P 500 was flat all day. That reading exceeded the sub-10% levels that we saw on much stronger days last Thursday and Friday.

In going through the charts of the large and mid-cap stocks hitting new highs yesterday, one trend that stood out is that many of them are very extended and probably due for some sort of pullback or at least a pause. This morning, though, we wanted to highlight some of those stocks that made new highs that aren’t as extended (relatively speaking) and are attempting to break out of short to intermediate-term trading ranges. The six names highlighted below are part of a custom portfolio we created highlighting 20 names that fit these criteria. To view the entire portfolio, make sure you are logged in to the site and then click here or on the image below.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer – VIX Low Into Earnings, Empire Not OK, Cass, Brazil – 7/15/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, with this week marking the start of earnings season, we show S&P 500 performance given the levels on the VIX. We also take a look at the rally in EM credit and OEM auto stocks. We then go over some of the details in today’s Empire Manufacturing report that were weaker than the headline number would lead on. After reviewing Cass Transportation Indices, which showed some alleviation to their weakening trend, we finish with a rundown on the economic conditions in Brazil.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

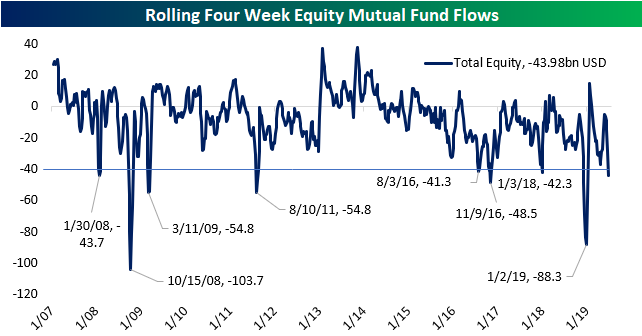

Mutual Fund Flush

Our weekly Bespoke Report newsletter is one of the most popular reports included as part of the Bespoke research offering. Each week, we provide a comprehensive rundown of the week’s events and our analysis of where the market is headed next. If you haven’t done so before, sign up for a free trial to see for yourself. You won’t be disappointed! In last week’s Bespoke Report, we looked at various measures of investor sentiment including flows into and out of equity mutual funds. The table below provides a summary of mutual fund flows through the latest reporting period last week showing actual flows on the left and how those flows rank relative to history on the right. With the stock market breaking out of its range to new all-time highs, you would expect flows into equity mutual funds to be surging, and while there has been a surge in mutual fund flows, the direction has been out of as opposed to into stocks.

In the latest week, equity mutual funds saw nearly $17 billion in outflows, bringing the four-week total of outflows to just under $44 bln. On a percentile basis, those total outflows rank below the 2nd percentile relative to all prior one-week periods in the last decade and below the 3rd percentile relative to all other four-week periods. Not only has there been an exodus out of equity mutual funds, but the declines have been broad-based across domestic and global funds.

The fact that outflows have been so large just as the S&P 500 is hitting new all-time highs is unique, to say the least. The chart below shows the rolling four-week total of fund flows going back to the start of 2007. During that time, there have only been eight other periods where the magnitude of outflows from equity mutual funds has been more than $40 billion (as it is now). If you look at the dates of each of those occurrences, more often than not they were during periods of elevated volatility during a market decline rather than in unison with an all-time high in the equity market.

Chart of the Day: Lenders Cheap, Yields High

B.I.G. Tips – 20%+ YTD

The S&P 500 came into the new trading week up 20.22% year-to-date, which is the biggest gain at this point in the year since 1998. This year’s gain is the 9th strongest move at this point in the year in the S&P’s history dating back to 1928. It’s also just the 9th time the index has been up 20%+ at this point in the year. (Keep in mind that the S&P fell 19.8% from its high point to low point in Q4 2018, so while this year’s move has been impressive, the index is not all that far above its 2018 highs.)

Below is a look at all years that the S&P 500 has been up 20%+ at this point in the year (133 trading days). For each year, we show how the index performed over the next month, three months, and through the rest of the year.

To continue reading this report and see how the S&P 500 performed in prior years that saw 20%+ gains through mid-July, start a two-week free trial to Bespoke Premium!

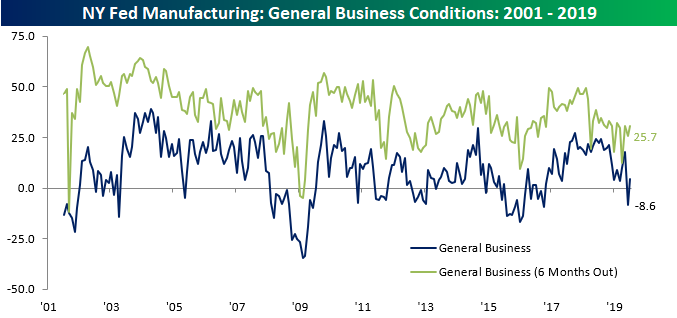

Empire Index Moves Back to Growth

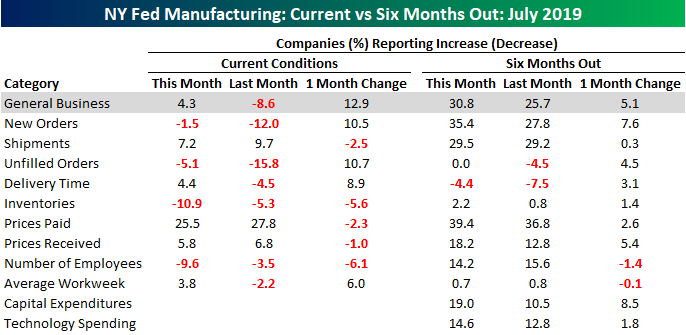

After threats of tariffs on Mexican imports sent sentiment in the Empire Manufacturing Index plunging in June, things bounced back a bit in July as the headline index moved back above zero and surpassed consensus expectations. While economists were forecasting the headline index to rise up to 2.0 from last month’s reading of -8.6, the actual reading came in slightly stronger at 4.3. Expectations for six-months from now improved by a smaller margin, but they also never fell as much.

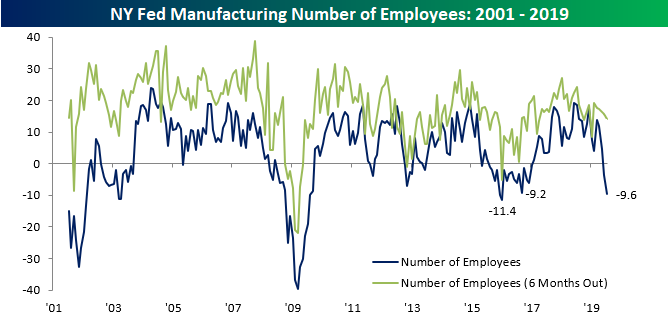

While the headline index bounced back pretty significantly in July, breadth among the components wasn’t particularly strong as just four showed m/m increases compared to five declines. On the upside, the biggest gains were in Unfilled Orders and New Orders, while the largest decline was in Number of Employees. In terms of expectations, breadth was much stronger as the only two components showing declines were Number of Employees and Average Workweek. Plans for both Cap-Ex and Technology Spending both increased.

As mentioned above, the Number of Employees index saw the largest decline this month and at its current level of -9.6, this component is not far from its lowest levels since the end of the last recession. The only period we saw a weaker reading was right in the midst of the late 2015/early 2016 oil-induced slowdown. Employment has been a bright spot for the US economy, but this data point is negative. Going forward, it will be important to watch the other regional FOMC indices for signs of confirmation. Start a two-week free trial to Bespoke Institutional to access our Economic Indicator Database and other interactive tools.

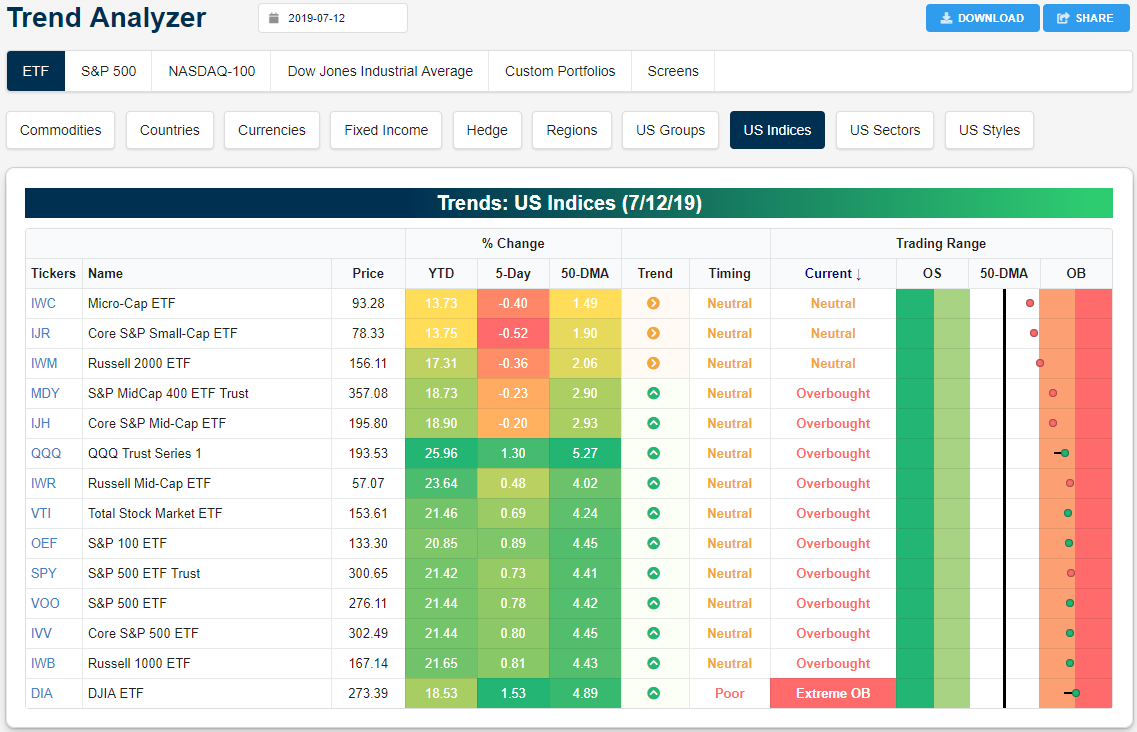

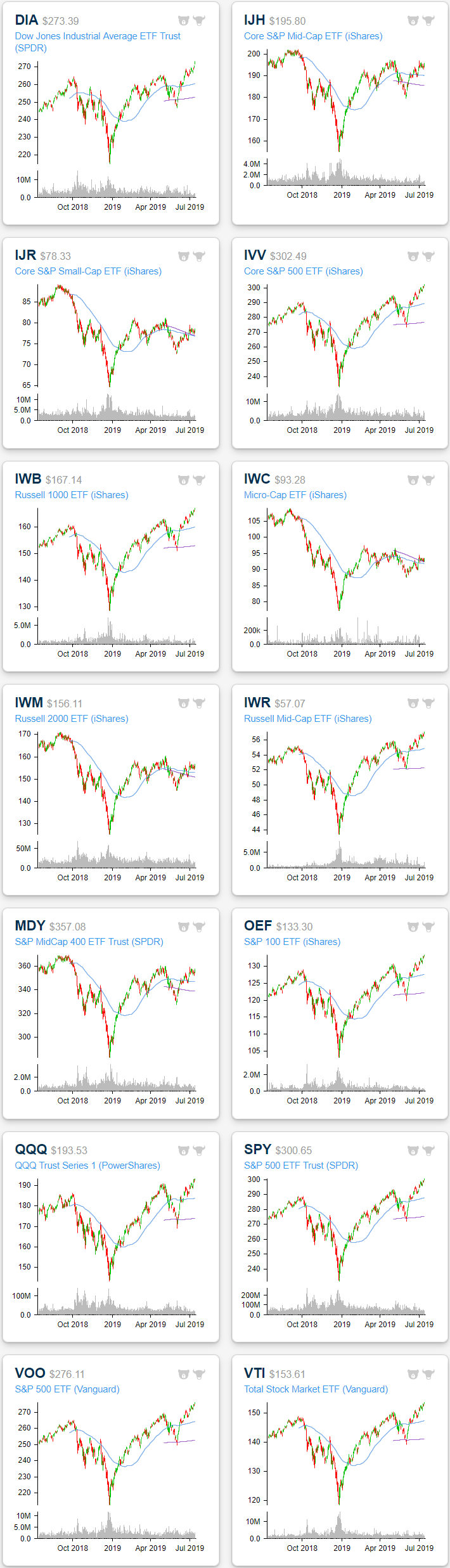

Trend Analyzer – 7/15/19 – Small Caps Sitting Out New Highs

Large-cap indices rallied into the end of the week to finish at all-time highs. The Nasdaq 100 (QQQ) surged 1.3% in the past five days, and QQQ has now risen the most of any of the major index ETFs in 2019. Meanwhile, the Dow (DIA), which is the worst-performing large-cap index YTD, received a boost from UnitedHealth (UNH) and finished as the best performing major index ETF last week with a gain of 1.53%. This not only sent the index above the 27,000 milestone, but also brought it up to extremely overbought levels. DIA is currently the only major index ETF at extreme overbought levels, although ten others are also overbought and approaching extreme levels. Small caps, on the other hand, all remain neutral with further declines last week. Mid-caps shared in these losses but to a lesser extent.

Small and mid-caps have continued to lag their large-cap peers and last week’s break out to new all-time highs for the likes of the Dow (DIA) and S&P 500 (SPY) has made this lag even more evident in the charts. The DIA, QQQ, S&P 500 (SPY & VOO), Core S&P 500 (IVV), Russell 1000 (IWB), S&P 100 (OEF), and Total Stock Market ETF (VTI) are now all in uncharted waters as they have broken out to new all-time highs. As we mentioned in Friday’s Bespoke Report, while the Dow and S&P 500 breakout was more clear cut, QQQ’s was a bit less convincing. Similarly, small and mid-caps—except for the Russell Mid-Cap (IWR)—all sit firmly below their prior highs from late last year. While they have made some higher highs earlier this year, they have still sat in consolidation and continue to move sideways rather than distinctively higher. Start a two-week free trial to Bespoke Institutional to access our interactive Trend Analyzer, Chart Scanner, and much more.

Bespoke’s Morning Lineup – Earnings Season Kicks Off and More Fed

Happy earnings season! Citigroup (C) kicked things off this morning with a better than expected report, and the stock is trading up modestly on the news. The pace of earnings reports will be slow today, but things will pick up as the week goes on. While last week was an extremely busy one for Fed speakers, this morning we will also hear from NY Fed President Williams, and then tomorrow will be another busy day with Bostic, Bowman, Kaplan, Powell, and Evans all scheduled to speak. In US economic news, the Empire Manufacturing report for July came in better than expected at 4.3 and up from June’s reading of -8.6.

Read today’s Morning Lineup to get caught up on news and stock-specific events ahead of the trading day and a further discussion of overnight events including the latest round of economic data from China.

Bespoke Morning Lineup – 7/15/19

The US Dollar Index is on pace for its fourth straight day of declines today, and while that kind of trend would normally benefit the stocks of US multinationals, in recent days that hasn’t been the case. As noted in last Friday’s Bespoke Report, last week it was the Domestics that outperformed and propelled the market to new highs. Sure, it’s just a couple of days, but for now, at least, investors in the stock market don’t seem to be convinced that the recent dollar weakness will be long-lasting.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 7/14/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Physical Performance

Unlocking the mystery of superhuman strength by Scott Eden (ESPN)

An investigation of the extreme increases in physical performance human beings are capable of when adrenaline and survival instincts converge during life-or-death situations. [Link]

‘These kids are ticking time bombs’: The threat of youth basketball by Baxter Holmes (ESPN)

Extreme specialization, high workout loads, and little downtime are breaking young bodies before they can perform at an elite level in the NBA. [Link; auto-playing video]

Weird Sports

Redskins’ Norman runs with bulls in Pamplona (ESPN)

Seeing an NFL cornerback leap over a bull is worth the price of admission. Norman is a regular visitor to Pamplona in the offseason, wowing Spanish crowds with his athleticism. [Link; auto-playing video]

The AHL App Melted Down And Demanded $6,000 From A Guy Named Stewart by Laren Theisen (Deadspin)

An all-timer app blow up led to a series of totally ridiculous notifications sent to AHL fans via the hockey league’s app. [Link]

Investing

Fund Blowups Rekindle Doubts About ETF Liquidity in Crisis Times by Rachel Evans and Emily Barrett (Bloomberg)

The latest terror to grip markets is the idea that investors who use ETFs as cash substitutes won’t be able to liquidate in a large price shock. [Link; soft paywall]

Sub-Zero Yields Start Taking Hold in Europe’s Junk-Bond Market by Laura Benitez and Tasos Vossos (Bloomberg)

With benchmark rates deep in negative territory, short-term junk debt is trading at negative yields in Europe as it approaches maturity. [Link; soft paywall]

As Stocks Surge to Records, Nervous Investors Buy Bonds, Too by Daniel Kruger (WSJ)

Bond funds have seen massive inflows as individual investors load up on Treasuries and other low risk securities despite an equity market at record highs. [Link; paywall]

Economic Research

Study: The value of data in Canada: Experimental estimates (StatsCan)

A new analysis by Canada’s statistics agency has identified the scale of nonresidential fixed investment in data products. The agency estimates somewhere between 105bn CAD and 150bn CAD in data alone, with billions more invested in databases and data science. [Link]

From Policy Rates to Market Rates—Untangling the U.S. Dollar Funding Market by Gara Afonso, Fabiola Ravazzolo, and Alessandro Zori (NY Fed)

An extremely helpful background brief on the structure and flow of US money markets, complete with an interactive infographic. [Link]

Confederate Streets and Black-White Labor Market Differentials by Jhacova Williams (Google Docs)

A working paper from Clemson University’s Williams uses a novel identification technique to identify racial animus. Areas that honor Confederate Generals with street names have higher labor market inequality between blacks and whites, robust across a number of controlling factors. [Link; 37 page PDF]

Russia

Revealed: The Explosive Secret Recording That Shows How Russia Tried To Funnel Millions To The “European Trump” by Alberto Nardelli (BuzzFeed News)

Audio recordings reveal that top officials from Italy’s Lega Nord party met with Russian state actors who proposed a funding scheme that would have violated Italian law. [Link]

Crew of Russian Nuclear Sub Prevented ‘Planetary Catastrophe,’ Officer Says by Henry Meyer and Stepan Kravchenko (Bloomberg)

A fire onboard a Russian submarine nearly created a massive nuclear accident that would have poisoned oceans for generations. [Link; soft paywall, auto-playing video]

Corporate Finance

Buybacks: An Inside View (Sullimar Investment Group)

A $1bn buyback funded with a revolving credit facility saved Delta (DAL) more in dividend payments than it cost in interest payments. [Link]

This Warby Parker Co-Founder’s Next Startup Set Out to Beat a Razor Giant. 6 Years Later, He Sold Harry’s for $1.3 Billion by Tom Foster (Inc.)

Jeff Raider is a co-founder of iconic eyeglass brand Warby Parker as well as the massively successful razor company Harry’s, which was bought out by Schick’s parent company for $1.4bn. [Link; auto-playing video]

Walmart Got a $10 Billion Surprise After Buying Flipkart by Saritha Rai (Bloomberg)

Wal-Mart bought control of India’s leading e-commerce player last year, including an interest in a payments subsidiary which could lead to a $10bn windfall for the American retailer. [Link; soft paywall, auto-playing video]

Long Reads

The Young And The Reckless by Brenden Koerenr (Wired)

An incredible story about a Canadian teenager who ran a business selling level ups on Xbox games that eventually spiraled completely out of control. [Link; soft paywall]

Irony, Thy Name Is Gravy

Boston Market No Longer Has A Boston Location by Cameron Spearance (BisNow)

With 10% of the chain’s locations closing, there are now zero Boston Market locations inside the city of Boston. [Link]

Labor Markets

Amazon’s Latest Experiment: Retraining Its Work Force by Ben Casselman and Adam Satariano (NYT)

The e-commerce giant needs a more intensively trained workforce to operate higher value-add roles, so it’s investing $700mm in re-training a third of its workforce to raise productivity. [Link]

History

Understanding the Burr-Hamilton Duel by Joanne B. Freeman (Gilder Lehrman Institute of American History)

On the 215th anniversary of the most pivotal duel in American history, take some time to get reacquainted with the killing that altered American history. [Link]

The Story of Humans and Neanderthals in Europe Is Being Rewritten by Ed Yong (The Atlantic)

A homo sapiens skull found in a Greek cave is the oldest one discovered outside of Africa, casting doubt on longstanding theories about the spread of our species from its original home. [Link]

Pictures

It Looks Like a Lake Made for Instagram. It’s a Dump for Chemical Waste. by Andrew E. Kramer (NYT)

A brilliant blue lake in Siberia has become a magnet for Russian social media influencers, but its striking color is actually caused by pollution from a nearby power plant; if this isn’t a perfect metaphor for influencer culture, we’re not sure what is. [Link; soft paywall]

What Do People In Solitary Confinement Want To See? by Doreen St. Félix (The NYer)

There is almost nothing more psychologically painful than being cut off from all human contact, as prisoners in solitary confinement are. A new project seeks to connect them with pictures, letting them connect with a world beyond their confinement. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – The Calm Before the Storm

This week’s Bespoke Report newsletter is now available for members.

With little in the way of major economic data and earnings season still a week away, the only major item of this past week was the deluge of Fed officials hitting the tape, including Chairman Powell’s testimony to the House and Senate on Wednesday and Thursday.

With the overall calm and Powell’s soothing words, bulls were in charge and took charge sending the major US large-cap indices to record highs. After numerous attempts to get through the 2,950 level, the S&P 500 finally broke out and hasn’t looked back since. With the S&P 500 up 20% on the year and earnings season coming up on the horizon where does the market stand and have we moved too far to fast?

In this week’s report, we’ll try to shed some light on that question by looking at the recent moves from a variety of angles including market internals, the setup for earnings season, how the economy is faring, and a look at sentiment and prior strong rallies. We cover everything you need to know as an investor in our weekly newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!