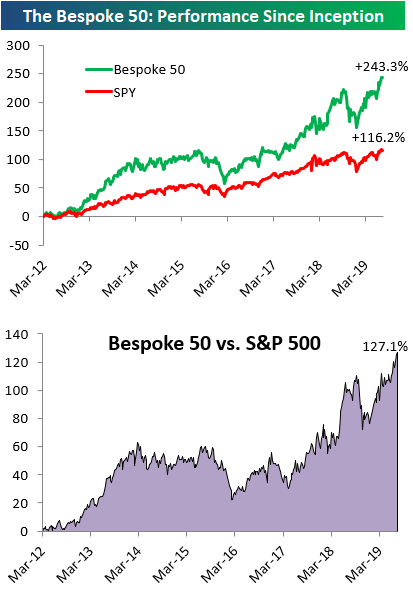

The Bespoke 50 Top Growth Stocks

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 127.1 percentage points. Through today, the “Bespoke 50” is up 243.3% since inception versus the S&P 500’s gain of 116.2%. Always remember, though, that past performance is no guarantee of future returns. To view our “Bespoke 50” list of top growth stocks, please start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

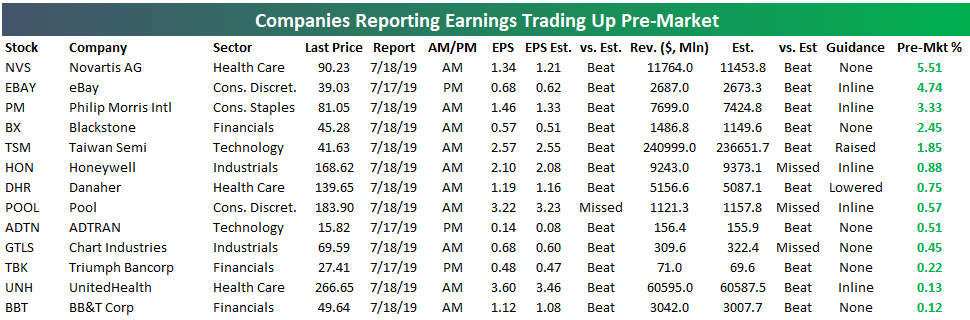

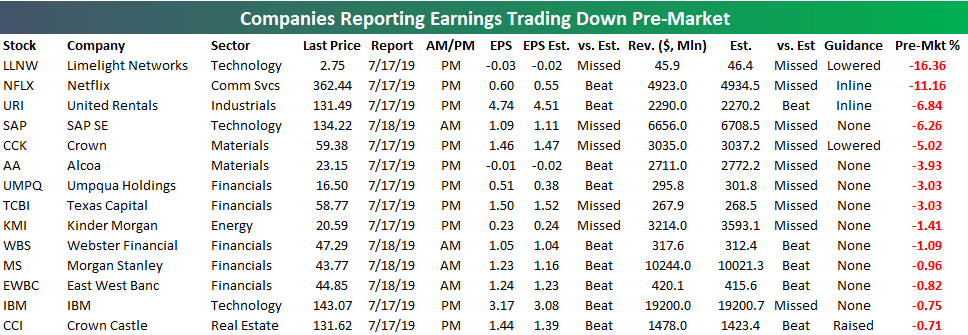

Pre-Market Earnings Movers: NFLX Down Big; NVS, EBAY, PM Trading Higher

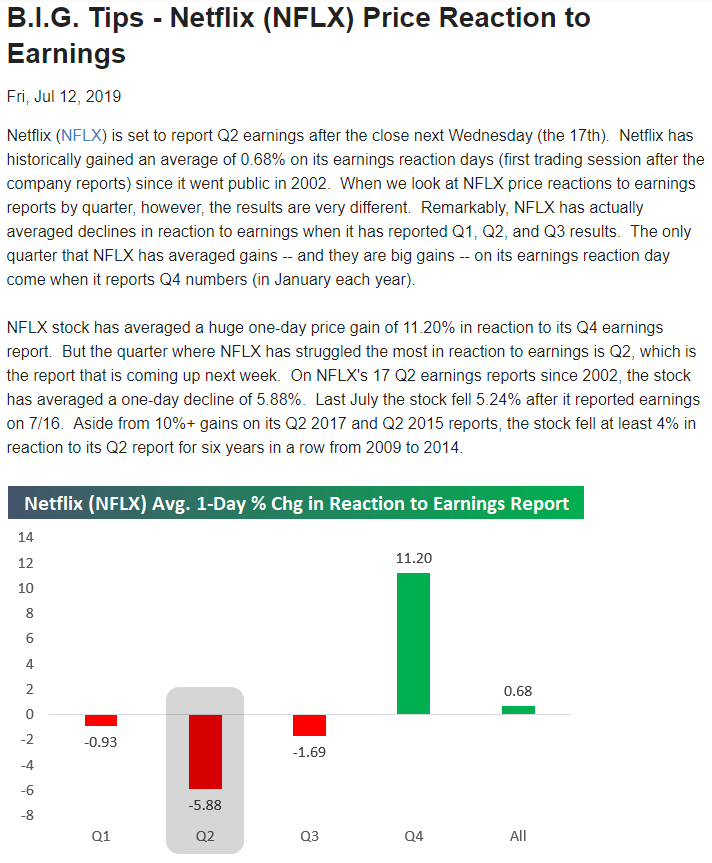

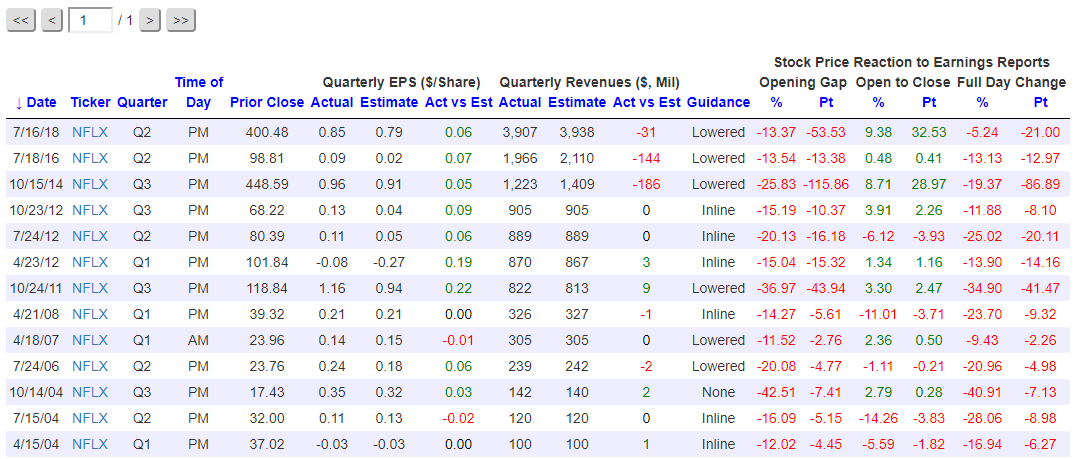

Netflix (NFLX) is trading down sharply in pre-market trading after reporting Q2 earnings after the close yesterday. (Here’s a snapshot of a report we sent subscribers last week noting that Q2 earnings are typically weak for NFLX.) The stock is set to open lower by 11% when markets open for trading this morning. Big gaps up or down of 10%+ are nothing new for NFLX. Since the company went public, this will be the 14th time that NFLX has gapped down 10%+ in reaction to earnings. When looking at how the stock might trade from the open to the close today following its gap lower, note that in the past the stock has traded higher from the open to the close 8 out of 13 times. As shown below, this same reaction happened a year ago when NFLX reported its Q2 2018 numbers. The stock opened down 13.37% on July 17th last year, but traders that bought at the open that day saw a huge gain of 9.38% from the open to the close.

{kind=link}

A total of 46 stocks have reported earnings since the close yesterday. Of those 46 stocks, 67% posted better than expected EPS, while just 56% posted better than expected sales.

Below we show the stocks that reported earnings since yesterday’s close that are trading up in the pre-market. Novartis (NVS) is set to open higher by 5.5% after beating on both the top and bottom line. eBay (EBAY) is set to open up the second most this AM with an expected gap higher of 4.74%. Philip Morris International (PM) is trading up 3.33% pre-market following big beats on EPS and revenues. If PM opens up more than 3%, it will be its biggest gap up on earnings since its April 2015 report when it opened up more than 5%. Other notables on the list of earnings winners ahead of the open include Blackstone (BX), Honeywell (HON), and Danahar (DHR). (Note that this is a snapshot of where stocks were trading pre-market at 8:30 AM ET, so prices could still change quite a bit before the 9:30 AM ET open.)

While Netflix (NFLX) is the most notable loser on earnings this morning, Limelight Networks (LLNW) is actually set to open down even more with an expected gap of -16.36%. LLNW reported a reverse earnings triple play by missing EPS estimates, missing revenue estimates, and lowering guidance.

United Rentals (URI), SAP, Crown (CCK), and Alcoa (AA) are other notable stocks set to open down this morning following earnings reports. Need earnings info for stocks you care about most? Start using our Earnings Explorer tool now with a two-week free trial to Bespoke Institutional.

Bespoke’s Morning Lineup – Stocks and Bonds Still Neck and Neck

The earnings flow is now in full swing and Netflix (NFLX) is the early leader for the title of the biggest flop as the stock is down over 10% after missing subscriber growth forecasts. In other earnings news, of the roughly 50 companies that have reported since the close yesterday, two-thirds have exceeded EPS forecasts while slightly more than half have managed to top revenues estimates. This morning’s economic slate kicks off at 8:30 with Jobless Claims and the Philly Fed report while Leading Indicators will be released at 10:00 am.

Read today’s Morning Lineup to get caught up on news and stock-specific events ahead of the trading day and a further discussion of recent earnings reports from around the world.

Bespoke Morning Lineup – 7/18/19

It may sound hard to believe given the recent gains in the equity market, but over the last 12-months, the S&P 500 and long-term Treasuries have had nearly identical returns. The chart below os from page two of our Morning Lineup and shows the relative strength of the S&P 500 versus the US Long Term Treasury future. When the line is rising, it indicates that stocks are outperforming bonds, while a falling line indicates periods where bonds outperformed stocks. With the line currently right at 0.0 through yesterday’s close, after the last twelve months, it has been a dead heat between the two.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer – Media Outperforms, International Data, Beige Book, Housing Starts – 7/17/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick things off with a look at media stocks which have been outperforming in both the US and across the pond in Europe. We also show the top 20 stocks in the S&P 500 so far this year. Next, show economic data out of Canada and France including the strength in the two countries’ manufacturing sectors. We then recap today’s release of the Fed’s Beige Book before finishing with looks at this morning’s housing starts and EIA data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Fixed Income Weekly – 7/17/19

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we review the resumed decline in global developed market yields and curve flattening.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

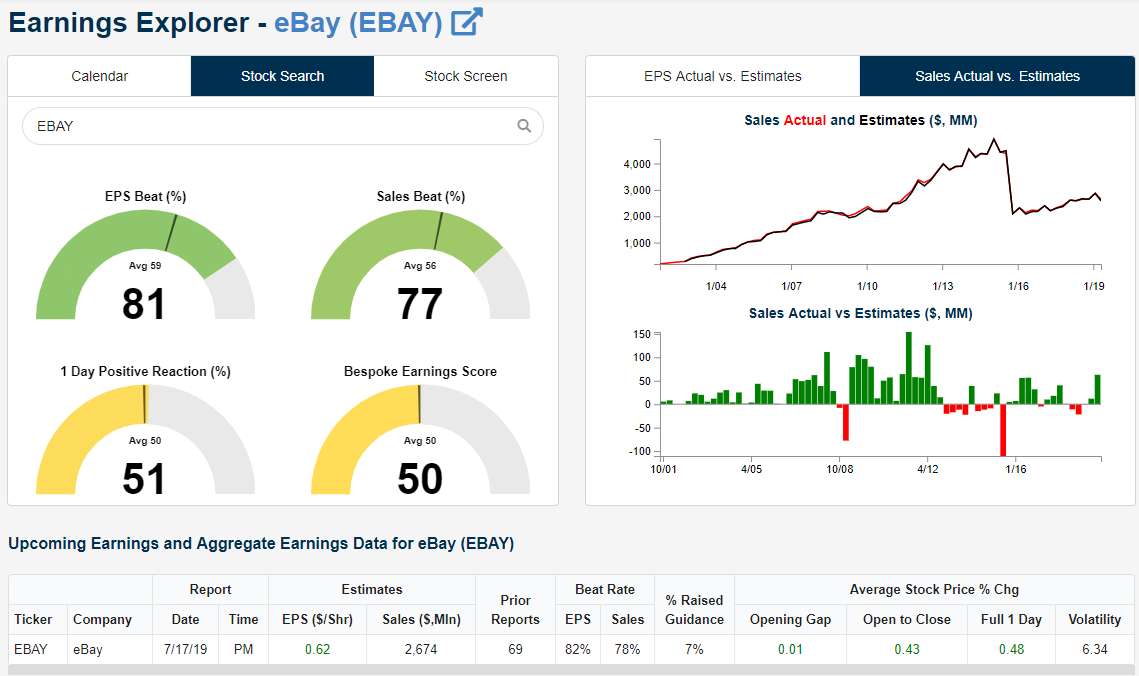

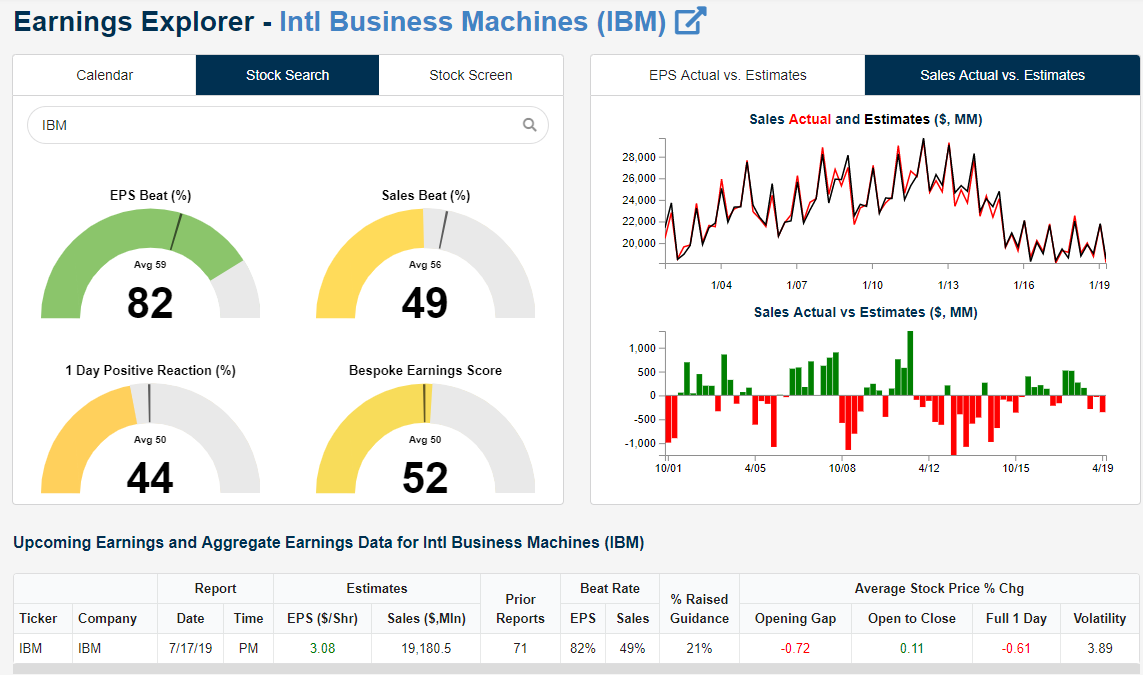

EBAY, IBM Earnings After the Close

Along with Netflix (NFLX), both eBay (EBAY) and IBM are also reporting Q2 earnings after the close of trading this evening. If you’re interested in our analysis of Netflix earnings, start a two-week free trial to Bespoke Premium and read our recent BIG Tips report on the subject. Below are snapshots of both eBay and IBM from our popular Earnings Explorer tool that’s fully available to Bespoke Institutional subscribers.

As shown, eBay has historically beaten consensus analyst EPS estimates 81% of the time, while it has beaten sales estimates slightly less at 77%. In terms of eBay’s stock price reaction to earnings, the stock has gained on the first trading day following quarterly earnings just a notch above half the time. The likelihood that EBAY will rise or fall in price in reaction to earnings has basically been a coin flip throughout the stock’s history. Be sure to check out some of the other stats included in the snapshot of eBay. You can find this same info for nearly every publicly traded US stock in our Earnings Explorer tool.

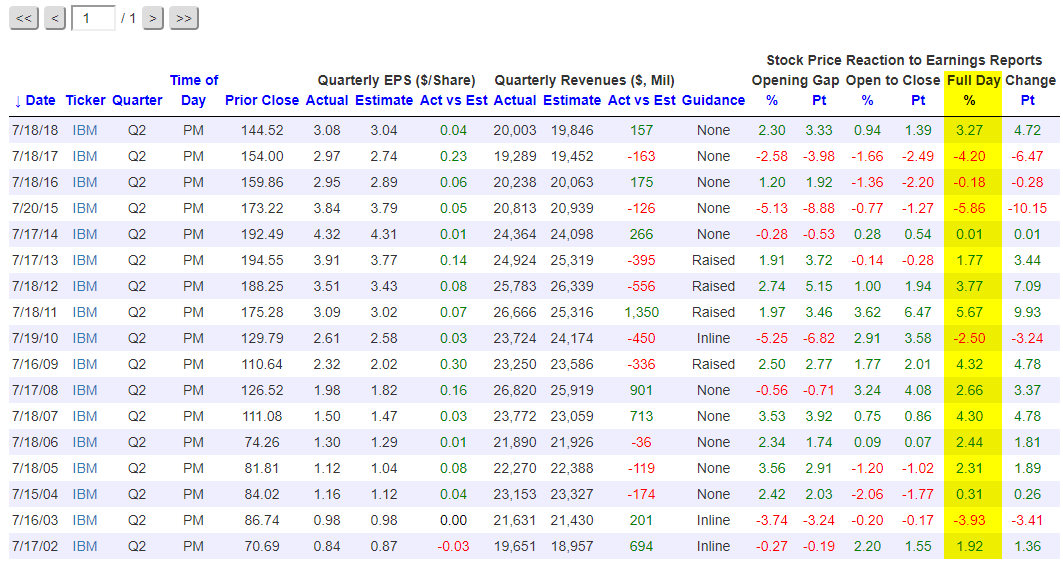

At 82%, IBM has an even stronger EPS beat rate than EBAY, but its sales beat rate is much weaker at just 49%. And IBM’s stock price has only posted gains on its earnings reaction days 44% of the time since 2002. Notice the slowdown in sales that IBM has seen over the last few years in the top right chart below.

When you look up an individual stock in our Earnings Explorer tool, we also provide detailed info for every single quarterly earnings report that each company has posted over the last 17+ years. Users can break the reports up by quarter so that we can look specifically at IBM’s historical Q2 reports for example. Below is a snapshot of IBM’s historical Q2 reports. We’ve highlighted the stock’s one-day price reaction to the earnings reports as well. As shown, when IBM reported earnings last July, the stock gained 3.27%. But the stock fell on its Q2 earnings day in each of the three prior years.

Overall, however, IBM has actually averaged a gain of more than 1% on its Q2 earnings reaction day when you look at all of its reports since 2002.

Need earnings info for stocks you care about most? Start using our Earnings Explorer tool now with a two-week free trial to Bespoke Institutional.

Chart of the Day: Still Finishing Strong

Trend Analyzer – 7/17/19 – Healthcare Industries Diverge

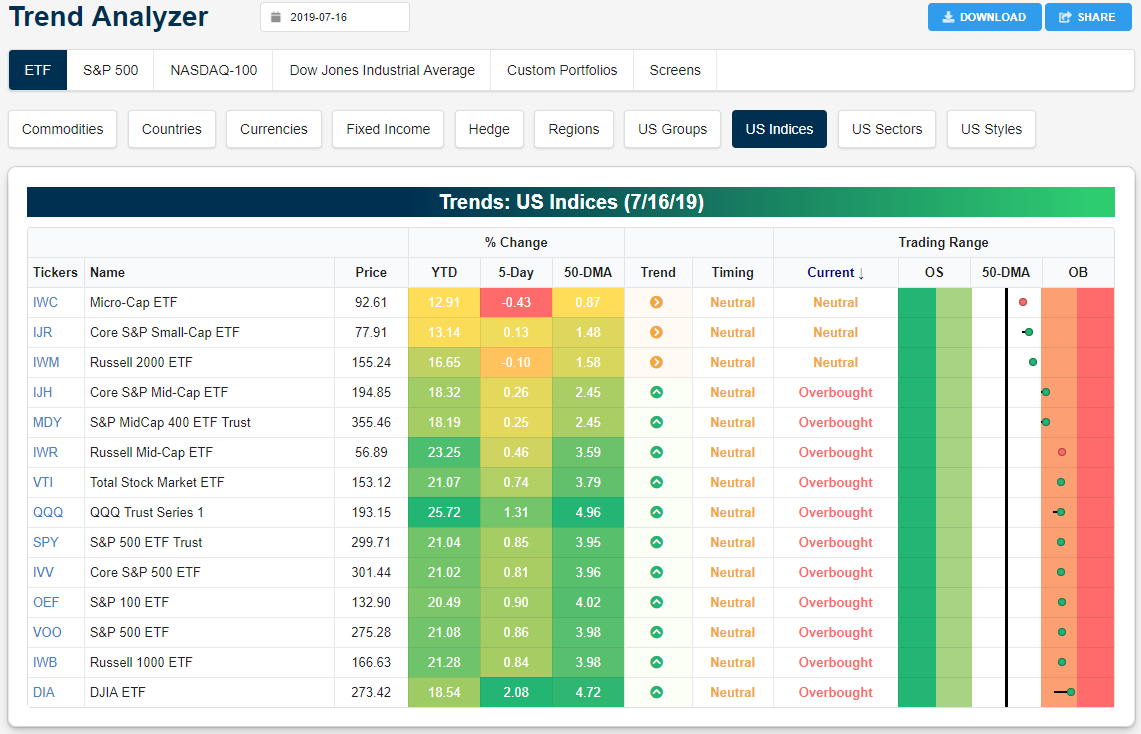

Yesterday’s session did little to create any major changes in the overbought and oversold levels of the major US index ETFs. As shown in our Trend Analyzer tool below, most of the major index ETFs have very small or no tails indicating little movement in respect to each ETF’s trading range over the past week. Large-cap indices continue to outperform small-caps with the Dow (DIA) having risen the most over the past five days. DIA has risen 2.08% while the Nasdaq (QQQ) has been the second-best performer rising 1.31%. With these changes, DIA and QQQ have both moved the most within their respective trading ranges in the past week. DIA, while still the most overbought, is actually in better shape than it was earlier in the week when it was sitting at extremely overbought levels. Meanwhile, the Micro-Cap ETF (IWC) and Russell 2000 (IWM) are both lower over the past few days. Alongside the Core S&P Small-Cap ETF (IJR), these ETFs are also the only ones to be neutral and in sideways trends.

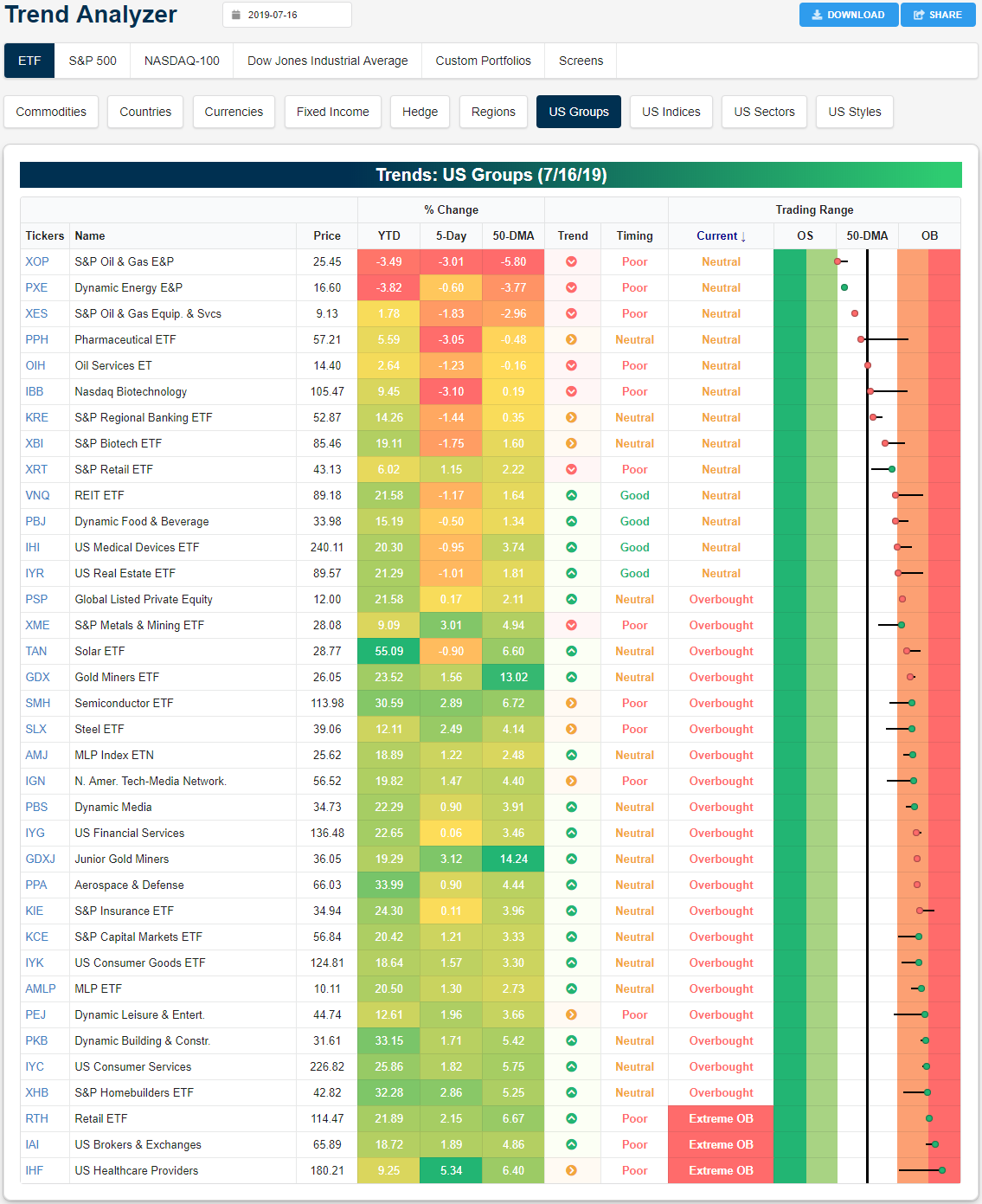

Looking at the various industry groups, there has been an interesting divergence between Healthcare industries over the past few weeks following headlines reporting the Trump administration’s proposal of reforms including an executive order pushing for more transparent pricing in late June. Pharmaceuticals (PPH) and Biotech (IBB) have been taking a beating so far in July after a jump to extremely overbought levels at the start of the month. In the past week, PPH and IBB have fallen 3.05% and 3.1%, respectively. These have been the two worst-performing industry ETFs in the past week and have rapidly pulled back to their 50-DMAs. Meanwhile, US Healthcare Providers (IHF) has been the best-performing industry ETF with a 5.34% gain, thanks to a large gap up last week on more headlines from the White House regarding a rebate plan. This has sent the ETF surging into extremely overbought territory. IHF is not alone at extreme levels though as the Retail ETF (RTH) and Brokers and Exchanges (IAI) also both sit at elevated levels. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Global Macro Dashboard — 7/17/19

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

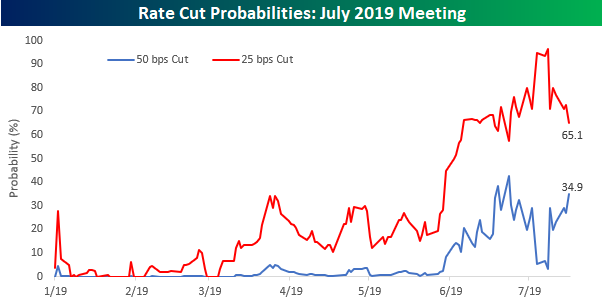

25, 25, 25, Do I have 50?

Remember back on July 5th after the stronger than expected employment report when the probability of a July 50 basis point (bps) rate cut plunged from 29% all the way down to 5%? Of course, you don’t! It was a summer Friday between July 4th and the weekend. The following Monday, though, market expectations for a 50 bps cut continued to fall, even falling below 3% early that week. Ever since that knee-jerk reaction to the employment report, though, probabilities for a 50 bps cut have been back on the rise and are higher now than they were right before the release of the June employment report. At over 34% now, the market is pricing in better than a 1 in 3 chance of a 50 bps cut at the July 31st meeting.

While there have been some weaker than expected data points since the employment report (Industrial Production, Capacity Utilization, Housing Starts, and Building Permits), there have been many more better than expected reports. Small Business Sentiment, Jobless Claims, Empire Manufacturing, Homebuilder Sentiment, Retail Sales, CPI, and PPI are all reports that have come in better than expected since July 5th. While not all the readings have been particularly strong, it’s puzzling to see probabilities of more aggressive easing rise even as the pace of better than expected reports improves. Start a two-week free trial to one of Bespoke’s premium equity market research services.