Triple Play Acquiring Triple Play

Exact Sciences (EXAS) announced plans today to acquire another health care company, Genomic Health (GHDX). The two announced that the agreement would combine Exact Sciences with Genomic Health for $72 per share in cash and stock. That acquisition news is not the only thing the two have in common though. Both companies also reported EPS before the open today, and they were both triple plays.

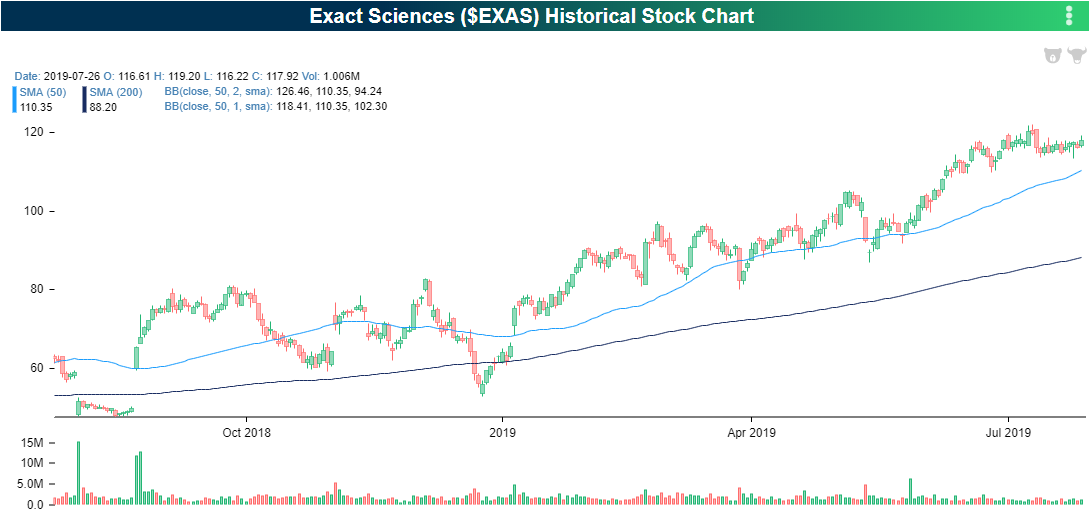

Exact Sciences (EXAS) is a cancer diagnostics company specializing in the detection of colorectal cancer with their signature product Cologuard. This was the company’s fifth triple play with the last one occurring in October 2018. The company is seeing much larger cash flows this year as it grew revenues an astounding 94.3% YoY to $199.87 million versus expectations of $182.18. This was also the 16th straight quarter with sequentially higher revenues. The company is still operating at a loss, though, with EPS at -$0.30, but that was above estimated losses of $0.56 per share. The company has still yet to post a profit for any quarter over the past 34 reports in our Earnings Explorer as costs/expenses have been growing at a high rate, similar to revenues. For example, in this most recent report, total expenses grew 67.5% YoY. Despite the triple play, EXAS is down sharply today, trading more than 10% lower due to the GHDX acquisition. The stock has been in an uptrend over the past year, so this decline brings it below the 50-DMA and near the lower end of this uptrend channel.

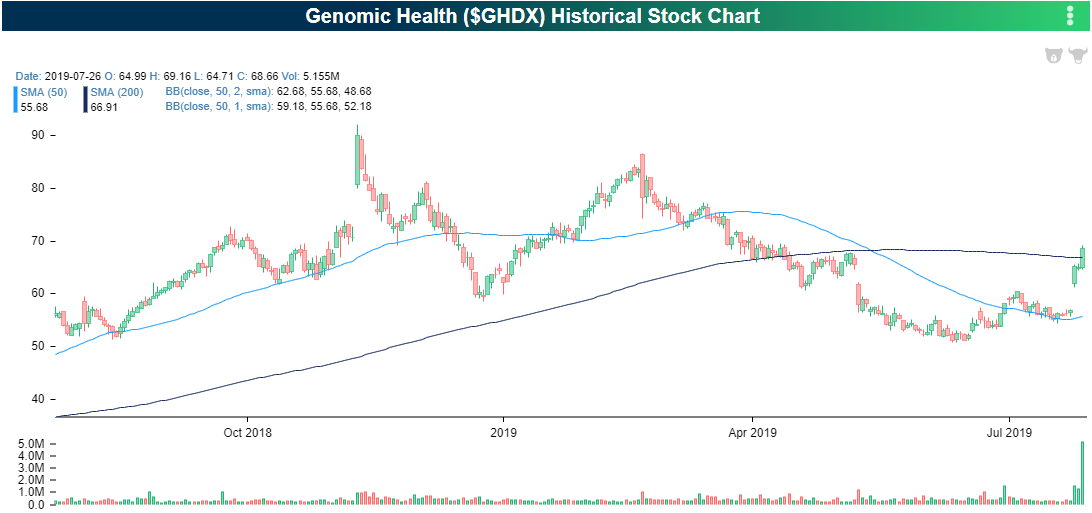

Genomic Health (GHDX) was originally scheduled to release earnings on Thursday (August 1st), but with the merger announcement, they moved up their report. Like Exact Sciences, Genomic Health also specializes in cancer diagnostics. In this earnings report, GHDX reported EPS of $0.42 versus estimates of $0.35. Revenues also came in above estimates at $114.14 million, 19.4% YoY growth. The company reported that each of the key product areas for their main product, Oncotype, saw double-digit growth YoY with the main highlight being a 42.3% growth rate for the prostate test. The stock has risen 3.28% in response today. This is after last week’s massive gains when it was announced the stock would be joining the SmallCap S&P 600 Index. Start a two-week free trial to Bespoke Institutional to access our interactive Earnings Explorer, the 100 Most Recent Triple Plays, and much more.

High Yielders

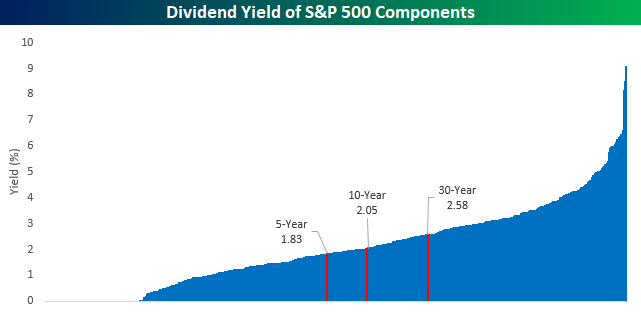

With US Treasury yields so low right now, yields on equities have become increasingly competitive. Granted, Treasuries have considerably less capital risk than equities, but from a historical perspective, it isn’t typical for stocks to yield more than Treasuries. Then again, is anything typical these days? While there have been short periods in recent history where the S&P 500 has had a higher dividend yield than the 10-year US Treasury, right now the 10-year yield (2.05%) is just under 20 bps higher than the dividend yield of the S&P 500 (1.87%).

For a large percentage of the S&P 500’s individual components, though, it’s a different story. As shown in the chart below, 225 of the S&P 500’s individual components had a dividend yield of more than 2.05% (the yield on the 10-year) while 173 of those have a higher yield than the 30-year US Treasury. Also, relative to the 5-year US Treasury, more than half (259) of the S&P 500’s components have a higher yield.

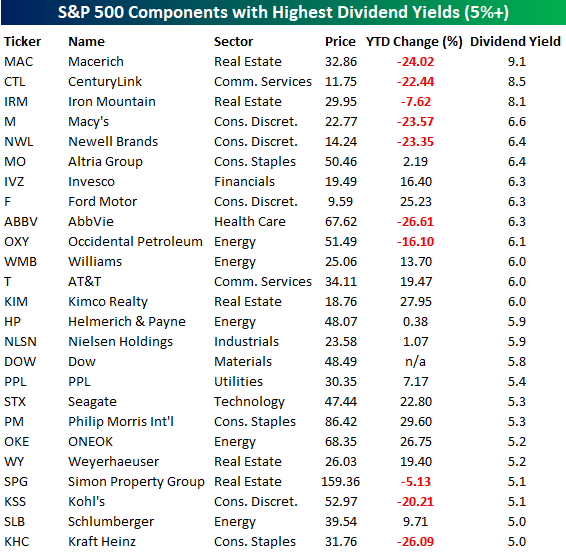

Turning to the highest yielding S&P 500 stocks, 25 of them now have a yield of 5% or more. Normally, you would expect to see stocks from the Financials and Utilities sectors comprise a large portion of a list like this, but each of these sectors only has one stock on the list. The two stocks with the greatest representation are Energy and Real Estate, each with five. Perhaps the most notable aspect of the list is that all eleven of the S&P 500’s sectors are represented on the list – even Technology (Seagate)!

While high dividend yields sound attractive, it’s important to be careful with these types of names as they often have high yields for a reason. Just look at the five highest yielders; they’re all down YTD and by an average of 20% compared to the S&P 500 which is up over 20%. Year to date, the 25 names listed below are up an average of just 1.11%.

One theme that stands out on the list is just how out of favor brick and mortar retail is. Not only is that evident with names like Macy’s (M) and Kohl’s (KSS) but more importantly the retail-related REITs like Kimco (KIM), Macerich (MAC), and Simon Property (SPG) that own much of the real estate that the brick and mortar retailers lease.

Of all the names listed below, a year or two from now a number of these names will likely be big winners, but there will also undoubtedly be a number of names that either cut their dividends substantially or simply go out of business. Start a two-week free trial to Bespoke Institutional to access our full research suite.

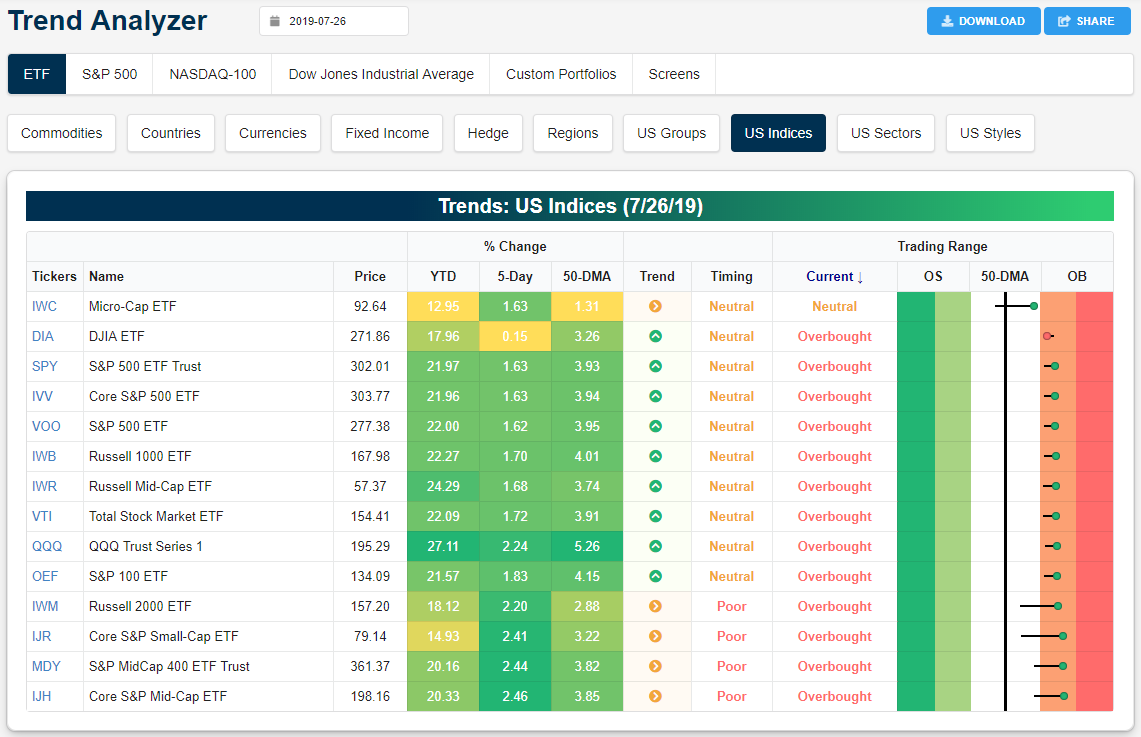

Trend Analyzer – 7/29/19 – Small Caps Surge, Large Caps Mixed

Small and mid-caps have surged in the past week as the Russell 2000 (IWM) and Core S&P Mid-Cap (IJH) gained well over 2%. These strong gains came in spite of their sideways trends; except for the Russell Mid-Cap (IWR) which saw more middling gains and is also in an uptrend. Last week’s gains also resulted in sizable movements within each ETFs’ respective trading ranges. While they were in neutral territory last week, many have moved to overbought levels. Although it has gotten close, the only one of the index ETFs not at overbought levels the Micro-Cap (IWC).

No major index ETFs finished lower last week, but the Dow (DIA) was a significant laggard with a gain of only 15 bps. While DIA underperformed (largely due to Boeing), the Nasdaq 100 (QQQ) surged 2.24% and the S&P 500 (SPY) rallied 1.63%. Whith these gains, the S&P 500 and Nasdaq managed to finish last week at new all-time highs, but the Dow still has some progress to make until it can do the same. Start a two-week free trial to Bespoke Institutional to access our Trend Analyzer and much more.

Bespoke’s Morning Lineup – Small Gains to Start to a Big Week

Premarket futures couldn’t be much quieter ahead of the first opening bell of the week, but that doesn’t mean there isn’t any news. While the economic calendar is quiet today, there’s already been major deal news, and the pace of economic activity will pick up as the week goes on. Also, don’t forget this Wednesday’s FOMC meeting! The dollar is up for a 6th day out of the last 7, crude oil is continuing to consolidate with little movement in the past week and a half, and rates are lower across the curve.

Continue reading in today’s Morning Lineup.

Bespoke Morning Lineup – 7/29/19

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 7/28/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Food

No One Knows Why a Mystery In-N-Out Burger Was Found Abandoned in Queens, 1,500 Miles from Home by Morgan Phillips (Mediaite)

How on earth did a fresh In-N-Out Burger make it from Kansas City (if not much further afield) to the streets of Queens early in the morning? [Link]

Chicago’s Real Signature Pizza Is Crispy, Crunchy, and Nothing Like Deep Dish by Jason Diamond (Bon Appétit)

You’ve been getting pizza all wrong. Specifically, the thick, deep dish sausage and cheese cakes are less genuine than thin, cheap, and crunchy bar snacks. [Link]

Investing

The Patsy, Revisited by Rusty Guinn (Epsilon Theory)

An ode to the combined importance and utter impossibility of knowing who else owns the assets you own, be they stocks, bonds, or anything else. [Link]

The Cannabis Opportunity by Meb Faber (Meb Faber Research)

A long read on the investing approach that might lead to owning cannabis stocks and why that bet may well be correct in the long term. [Link]

Mercy Withheld

Businessman: Wyoming Valley West board president denied 22K school lunch debt donation offer by Bob Kalinowski (The Citizens’ Voice)

After a Pennsylvania school board received national attention for its zero-tolerance approach to school lunch debt, a Philadelphia businessman offered to cover the debt but was rebuffed by school board officials. [Link]

Trump administration proposed rule would cut 3 million people from food stamps by Tom Polansek and Humera Pamuk (Reuters)

In 43 states, residents can become eligible for SNAP (commonly referred to as food stamps) if they already qualify for another benefit program, the Temporary Assistance for Needy Families. A new rule would end that practice. [Link]

Media

Inside the Democrats’ Podcast Presidential Primary, Where Marianne Williamson and Andrew Yang Rule by Oar Sanchez (The Wrap)

With more than 20 Democrats running for the top of the Presidential ticket, they’ve collectively logged more than 1200 podcast appearances. [Link]

22 Books That Expand Your Mind and Change The Way You Live by Darius Foroux (Pocket)

A range of interesting reads ranging from novels to history to philosophy that open up new worlds for readers. [Link]

The moon landing was a giant leap for movies, too by Jake Coyle (AP)

Touching down on the moon stimulated the national imagination in all kinds of ways, but the wave of movies before and after the moon landing drove a public fascination with space that has continued to this day. [Link]

Autos

Citroën Sabotaged Wartime Nazi Truck Production in a Simple and Brilliant Way by Jason Torchinsky (Jalopnik)

One small change to oil dipsticks meant French-produced trucks broke down at the worst times, but it was such a small change that it was easy to effect and basically undetectable. [Link]

Ford F-150 EV pickup prototype tows more than 1 million pounds by Dalvin Brown (USA Today)

An electric version of Ford’s classic pickup has demonstrated epic torque capable of moving a million pounds 1000 feet, a performance that would be literally impossible with traditional fuels. [Link]

Regulation & Competition

Equifax Data Breach Settlement (Federal Trade Commission)

A settlement with the FTC has created a series of benefits for the nearly 150mm consumers impacted by the Equifax Data Breach. [Link]

Justice Department to Open Broad, New Antitrust Review of Big Tech Companies by Brent Kendall (WSJ)

Facebook, Google, Amazon, and Apple are all in the crosshairs of Washington, reversing a light-touch regulatory approach to competition that has prevailed inside the Beltway for years. [Link; paywall]

Asia

In Hong Kong Protests, Faces Become Weapons by Paul Mozur (NYT)

In a war fought between protestors and authorities, identification and correlation between what’s said online and offline are key battlegrounds. [Link; soft paywall]

The #NoMarriage Movement Is Adding to Korea’s Economic Woes by Jihye Lee (Bloomberg)

Korea’s government has tried to boost birth rates, but more citizens are dying than being born, but many women feel the patronizing and sexist approach is making motherhood even less attractive. [Link; soft paywall, auto-playing video]

Wealth

Billionaire Behind Victoria’s Secret Built His Version of the American Heartland by Sophie Alexander (Bloomberg)

There’s a certain kind of rich that sparks a taste for buying things far beyond what most can imagine. For instance: an entire town. [Link; soft paywall, auto-playing video]

Yacht Owners Ditch Life on Land for the High Seas by Emily Nonko (WSJ)

For some retirees, no fixed address and constant access to the open ocean means cutting ties with land and moving permanently into the nautical world. [Link; paywall]

Economics

Why dynamic and personalized pricing strategies haven’t taken over retail — yet by Ben Unglesbee (Retail Dive)

E-commerce has allowed companies to show consumers different prices in order to maximize the revenue from sales, but there still isn’t much of that in the real world. [Link]

Internal Trade in Canada: Case for Liberalization by Jorge Alvarez, Ivo Krznar, and Trevor Tombe (IMF)

A quantification of the barriers to trade between Canadian provinces, which unlike American states are not governed by a uniform commercial scheme. [Link]

Sports

The World’s 50 Most Valuable Sports Teams 2019 by Kurt Badenhausen (Forbes)

More than half of the most valuable franchises are American football teams, which are magnets for valuation in a way that global soccer teams just can’t manage to match. [Link]

Central Banking

The New York Fed Has a Black Swan Hunter by Craig Torres (Bloomberg)

A special unit inside the New York Fed is charged with questioning orthodoxy, arguing against convention, and trying to pick out the biggest threats to the economy before they become visible. [Link; soft paywall]

Swiss policymakers caught in crossfire over franc by Eva Szalay (FT)

Efforts to reduce the value of the Swiss franc may catalyze an international reaction against the exchange rate-obsessed Swiss National Bank. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — Global Macro Outlook

This week we’re outlining how we see the global economy at present, along with its influence on US interest rates, credit, commodities, and equity markets. One of the topics we discuss in detail is the strong performance of US GDP in Q2, which in addition to upward revisions from 2014-2018 also showed newly-reported Q2 growth that was far stronger than analyst estimates. Smaller-than-expected headwinds from trade and inventory and a massive surge in consumer spending helped push growth above expectations despite weak investment. With the Fed set to join the global central bank easing party at its July meeting, it’s part of the reason to expect that the global backdrop is set to improve. Read more after signing up for a free trial below!

We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Closer: End of Week Charts — 7/26/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

B.I.G. Tips – Earnings Ideas

Nearly 600 stocks have reported earnings over the last two weeks, and 67% of them have beaten consensus analyst EPS estimates. In our newest B.I.G. Tips report, we break down a number of important earnings indicators and feature a number of individual stocks with bullish chart patterns following their recent earnings releases.

To read this report and see which stocks we like most coming out of earnings, start a two-week free trial to Bespoke Premium!

Next Week’s Economic Indicators – 7/26/19

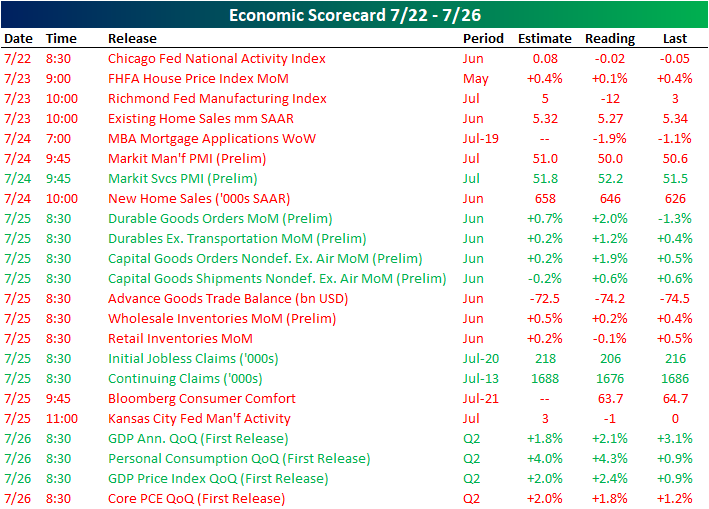

The Chicago Fed’s National Activity Index kicked off this week’s busy macroeconomic data slate on a disappointing note with a still negative reading that was below forecasts. Weak data continued to come in on Tuesday with FHFA home price growth slowing to 0.1% and the Richmond Fed Manufacturing index reaching a multi-year low. Existing Home Sales also came in weaker. Preliminary Markit PMIs released on Wednesday came in below estimates and weaker than the previous month while the services portion saw the opposite results. The release of preliminary Durable Goods and Capital Goods on Thursday came in much stronger than both expectations and the May release. Meanwhile, weekly labor data once again came in at a multi-month low. We ended the week with stronger than expected GDP data, but it still showed the economy slowed versus the first quarter. Overall, economic data didn’t have the greatest of weeks with over half of the indicators released weakening or coming in below estimates.

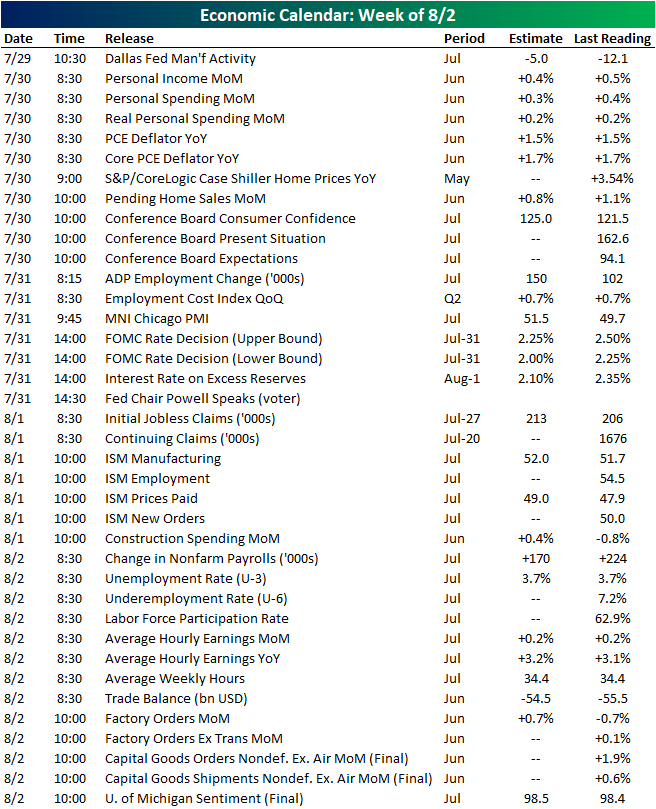

Next week is a busy one when it comes to macroeconomic developments. The week starts off quiet with only the Dallas Fed’s Manufacturing Activity Index out on Monday. It is expected to rebound to -5 off its multiyear low of -12.1 from its June release. Things pick up on Tuesday with the release of personal income and spending data which are forecast to fall 0.1%. PCE data, Pending Home Sales, and consumer confidence will also be out that day. Ahead of Friday’s Nonfarm Payrolls report, which is expected to show 170K added jobs in July, on Wednesday ADP will release their own employment data. Also on Wednesday, there will be an FOMC rate decision followed by a presser by Fed Chair Powell. Markets are anticipating a 25 bps cut in this meeting. After digesting the results of this meeting, on Thursday ISM will release their manufacturing report for July. In addition to the NFP report, the release of the June trade balance, factory orders, and the University of Michigan’s sentiment data will all round out the week on Friday. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – Strong Earnings; GDP on Tap

Ahead of US GDP today earnings headlines are flying, rates are slightly lower, and commodities are mixed. With huge names in tech (GOOGL, INTC, TWTR), quick service food (SBUX, MCD) and health care (ABBV) reporting very good numbers since the close yesterday, the market is poised to gap up over a quarter percent despite relatively weak AMZNnumbers. European earnings are also relatively strong once again.

Continue reading in today’s Morning Lineup.

Bespoke Morning Lineup – 7/26/19

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.