Bespoke’s Morning Lineup — Jobs and Jerome

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – STIRs Specs Burned In Dash For Trash – 9/5/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick things off with a look at the massive move on the front end of the curve and a decile analysis of S&P 500 stocks with respect to performance since the index’s all-time high. After taking a look at the near breakout for copper, we then review the relationship between FX and rates. Turning to macro data, we also show the relationship between the manufacturing and non-manufacturing counterparts of the most recent ISM data. We also review the new orders component of the ISM data in addition to other new order, manufacturing sales, and inventories data reported by the US Census. We finish with a look at the move in crude oil given this week’s inventory data

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

B.I.G. Tips – August Employment Report Preview

With fears of a recession on the rise, investors are looking for any potential signs of cracks in the economic picture. Tuesday’s ISM Manufacturing report, which showed the first contraction in the manufacturing sector in a couple of years, was one of those signs, but the stronger than expected report from the ISM Services report earlier today helped to allay those concerns. When it comes to the market, trade talks, or economic data, lately it seems like we’re simply running in place. For every good market day, tweet, or economic report, it seems as though there is a negative one to offset it. Today’s rally in equities looks to be an attempt by the market to break out of the rut it has been in, so will tomorrow’s payrolls report start another positive streak for the economy?

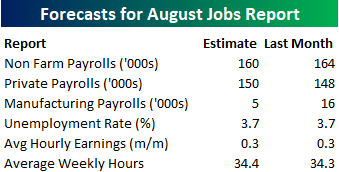

Heading into tomorrow’s report, economists are expecting an increase in payrolls of 160K, which would be a slight decline from July’s reading of 164K. In the private sector, economists are actually expecting a slight increase from July to 150K from 148K. Not surprisingly, job growth in the Manufacturing sector is expected to slow from 16K from 5K. The unemployment rate is expected to remain unchanged at 3.7%, average hourly earnings growth is expected to remain at 0.3%, and average weekly hours are expected to increase to 34.4 from 34.3.

Ahead of the report, we just published our eleven-page preview of the August jobs report. This report contains a ton of analysis related to how the equity market has historically reacted to the monthly jobs report, as well as how secondary employment-related indicators we track looked in August. We also include a breakdown of how the initial reading for August typically comes in relative to expectations and how that ranks versus other months.

For anyone with more than a passing interest in how equities are impacted by economic data, this August employment report preview is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!

Bespoke’s Sector Snapshot — 9/5/19

B.I.G. Tips – A Bounce for Internationals

Sentiment Back to Normal

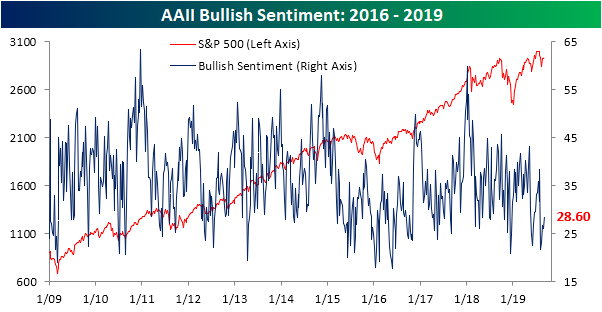

Bullish investor sentiment as measured by AAII’s sentiment survey rose 2.5 percentage points to 28.64% this week. While this is an improvement, bullish sentiment is still in the 18th percentile of the data over the past decade. We must also note that the survey would not have captured any benefit from today’s news on the trade front and the technical breakout of stocks and other assets like crude oil. Save a tweet or a headline reversing what appears to be optimism given today’s positive price action, we’ll likely see a bigger jump in bullish sentiment next week.

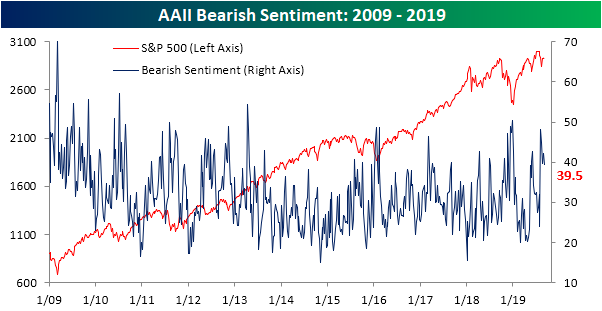

Bulls borrowed from the bears this week as bearish sentiment fell from 42.2% last week to 39.5%. As with bullish sentiment, this is not necessarily a dramatic improvement as it is still higher than 83% of weeks over the past 10 years. Bearish sentiment also remains the predominant sentiment level among investors as the bull-bear spread is still fairly wide at -10.87 percentage points. Granted, that is the narrowest spread since the last week of July when it was only 28 bps in favor of bears.

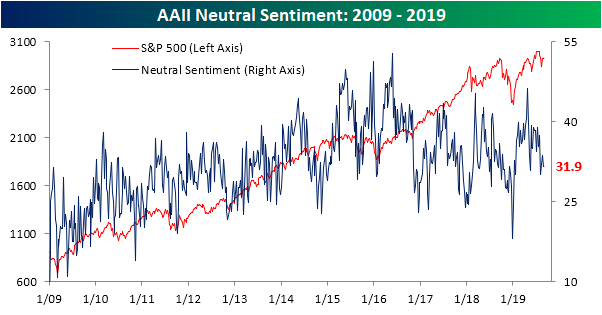

The bulk of the loss in bearish sentiment went to bulls, but a small portion also went to the neutral camp as the percentage of investors reporting as neutral grew to 31.9%. While bullish sentiment is still several percentage points below its historical average and the opposite applying to bearish sentiment, neutral sentiment has been pulling back to its historical average over the past few months. Where it currently sits at 31.9%, it is only 0.33% from that average. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

ISM Services Shows Little Pressure in Inflation

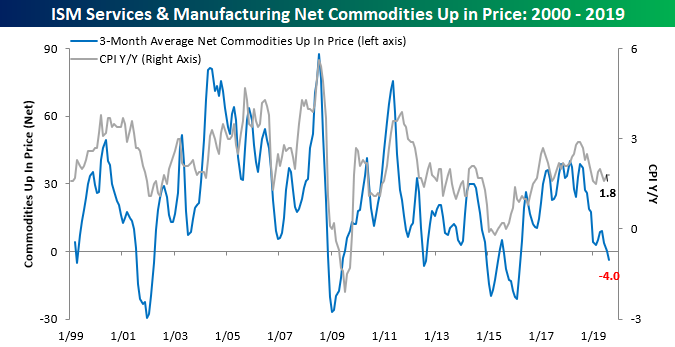

Following Tuesday’s ISM Manufacturing report, we noted the extremely low reading in the monthly ISM Commodities Survey, which measures the number of commodities rising and falling in price. After today’s report for the Non-Manufacturing sector, that trend remained in place. In this morning’s report, respondents noted price increases in just 6 commodities and decreases in 4. That net reading of +2 is the weakest reading since January. Combining the results of both reports, in August we saw a total of just 8 commodities up in price and 15 lower. That reading of negative 7 was the lowest since February 2016, while the three-month moving average of -4.0 was the lowest since April 2016.

As we noted on Tuesday, low readings in the commodities survey usually track the direction of inflation readings pretty closely and would imply that the current y/y reading of 1.8% in CPI will see downward pressure in the months ahead. For example, in the eight prior months where the three-month moving average in the combined reading was between zero and negative five, the average y/y reading in CPI was +0.45% while the median level was +0.65%. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: Down Goes Energy

ISM Non Contraction Index

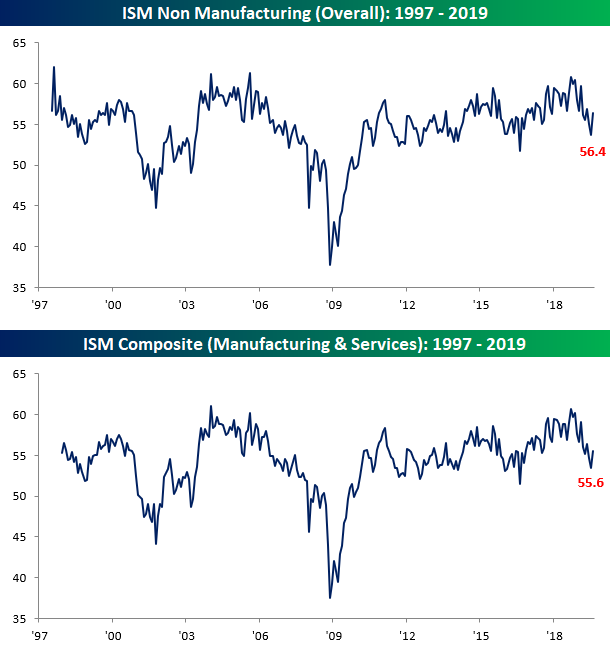

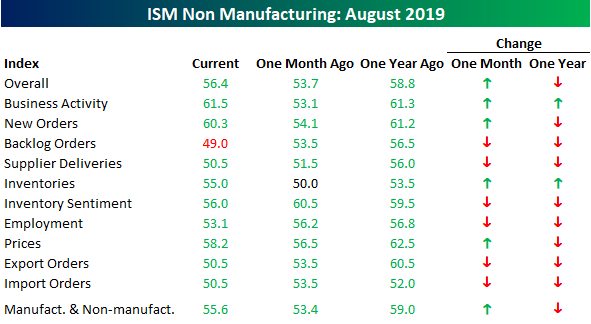

Just two days after one of the weakest ISM Manufacturing reports in years, Thursday’s release of the ISM Non-Manufacturing report for the month of August was a complete 180 from its Manufacturing counterpart. While economists were expecting the headline index to rise from 53.7 in July up to 54.0, the actual reading was considerably higher at 56.4. While it’s only the highest reading since May, the fact that it increased at all was a surprise to many. On a combined basis and accounting for each sector’s share in the overall economy, the Composite ISM for August rose from 53.4 up to 55.6 for its biggest monthly gain since February.

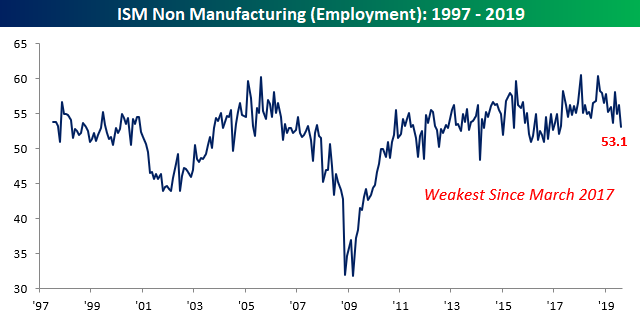

In terms of the breadth of this month’s report, it wasn’t particularly strong, but it wasn’t bad either. On a m/m basis, just four components increased while six declined. On a y/y basis, though, things were much weaker as just two components (Business Activity and Inventories) were higher this August than last. The biggest gainers on a m/m basis were Business Activity and New Orders, while on the downside Backlog Orders, Inventory Sentiment, and Employment saw the largest declines. In the case of Business Activity, that component’s 8.4 m/m increase was the largest since February 2008. Ahead of Friday’s Non-Farm Payrolls report, though, the decline in the Employment component is especially notable as its level is now the lowest since March 2017. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

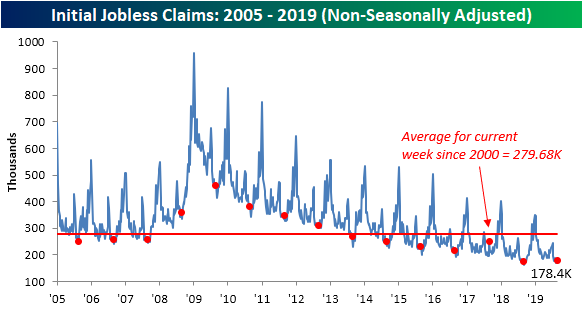

No New Lows Despite 100 Week Streak For Claims

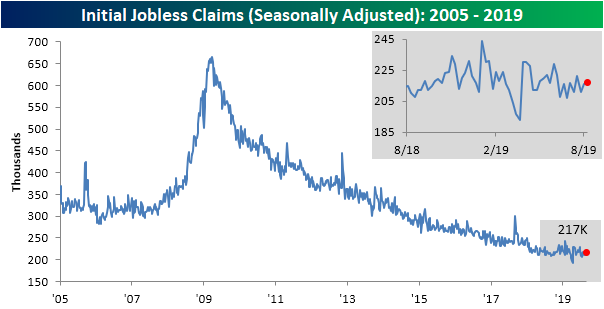

This week’s reading on initial jobless claims was expected to come in unchanged from last week at 215K. Instead, the indicator disappointed slightly with last week’s number being revised up to 216K and this week’s data showing 217K new jobless claims filed. In terms of the seasonally adjusted data, claims continue to remain in the middle of the past year’s range. Even though they were also flat over the past year (visible in the inlaid chart below), claims have in fact still been at very healthy levels. The streak of consecutive weeks at or below 300K has now grown to 235 weeks. This week also marked the 100th straight week of claims coming in at or below 250K! As has been the case for some time now, claims may not be improving or degrading at any significant rate, but the labor market is still holding up just fine.

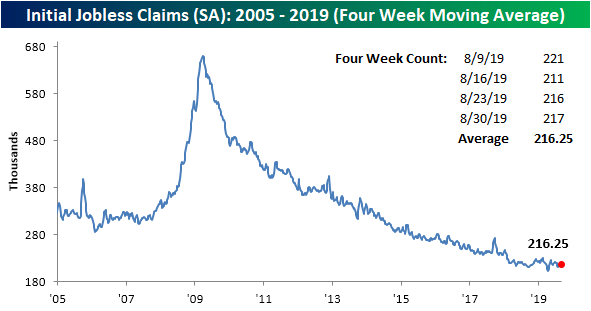

The four-week moving average reinforces this point as it has also been flat for the past year and a half outside of the spike lower in April. This week, the moving average ticked up to 216.25K as the lower reading of 211K from the first week of August rolled off the average to be replaced with this week’s higher 217K. Again, as with the weekly seasonally adjusted data, the moving average is still at healthy levels relative to history even though the pace of improvements has slowed. Fortunately, looking ahead to next week, there is a good chance the moving average can make a move lower as the recent high of 221K will come off the average.

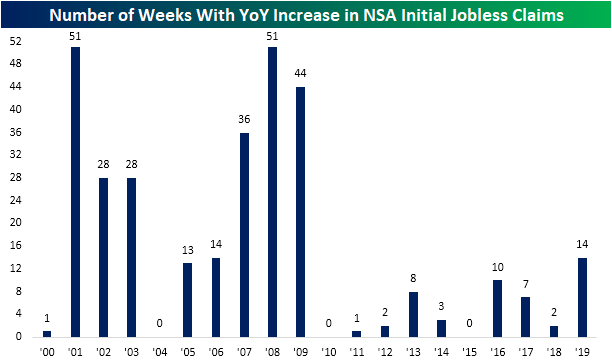

As we discussed last week, the end of August and beginning of September typically see the smallest average week-over-week changes in non-seasonally adjusted initial jobless claims data despite the yearly low typically coinciding around this time of year as well. That continues to hold true this week as the NSA data only rose by 1.5K compared to the average absolute move of 8K. This week’s reading of 178.4K is still well below the average for the current week since 2000, but it was 4.8K higher than the comparable week last year. The only other year of the cycle that the current week saw a YoY increase was in 2017 when it saw an unusual 32.9K increase YoY. Looking ahead to next week, the comparable week last year marked the lowest level in NSA data of the cycle at 162.6K. It would be a promising sign to see this low taken out, but given the higher frequency of YoY increases this year (second chart below), it is questionable if we will see that happen. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.