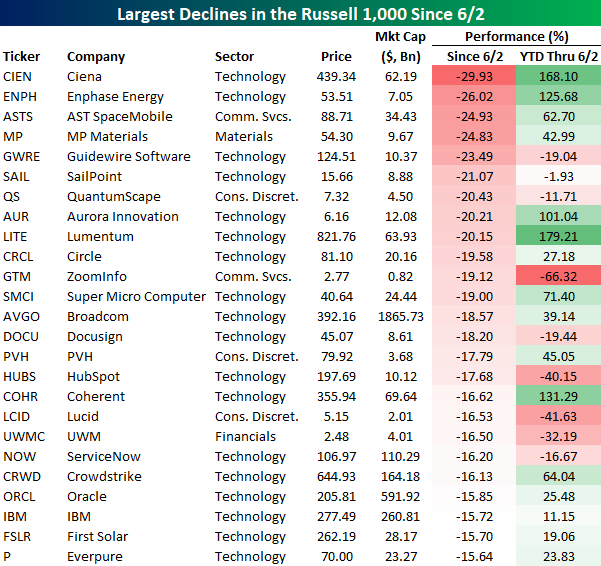

Raining on the Russell 1000’s Parade

The Russell 1,000 is down more than 3% since its June 2nd high, but several of its biggest losers have lost more than a fifth of their value. In just a week, Ciena (CIEN) has tumbled almost 30%, making it the biggest loser in the index after an 168% upswing on the year before the 6/2 close. Enphase Energy (ENPH), AST SpaceMobile (ASTS), MP Materials (MP), Guidewire Software (GWRE), SailPoint (SAIL), QuantumScape (QS), Aurora Innovation (AUR), and Lumentum (LITE) are the other eight names that have fallen at least 20% over the past week.

On average, the 25 stocks below rallied 35.5% on the year before last week’s peak, but they’re all down at least 15% since. For nine companies, the losses over the past week add to an already rough 2026. For three of those companies, GWRE, SAIL, and QS, the losses over the past week are even worse than the YTD losses leading up to the 6/2 Russell 1,000 peak.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

Bespoke’s Morning Lineup – 6/10/26 – Truth Be Told

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I believe in the idea of the rainbow. And I’ve spent my entire life trying to get over it.” – Judy Garland

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US stocks are down and bond yields up ahead of the open after President Trump suggested on Truth Social that the US will resume bombings of Iran. Leading up to Trump’s comments, futures were already pointed lower, however, led by Tech.

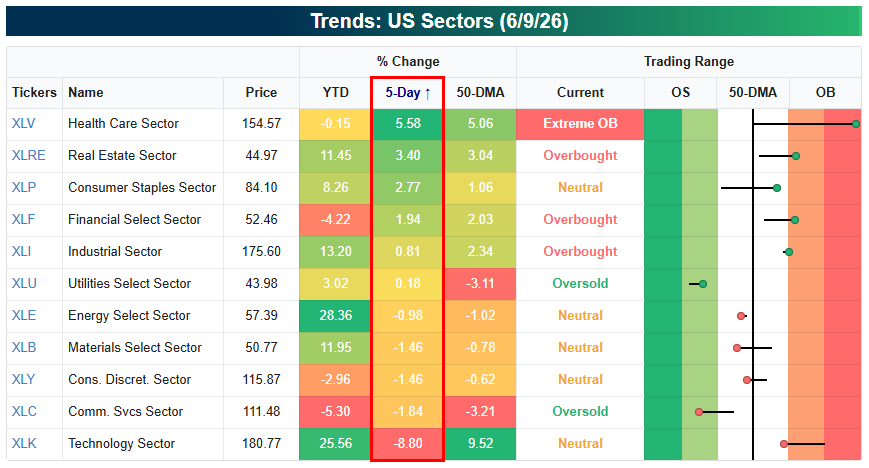

It’s important to note that we’re seeing rotation within the market rather than out of the market. Yes, the broad indices are down because of Tech’s large weighting, but we’ve seen nice gains for sectors like Health Care, Real Estate, Consumer Staples, and Financials as Tech has been selling off.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Tech Tumble, Breadth Disconnects, Trade – 6/9/26

Log-in here if you’re a member with access to the Closer.

- Tech has experienced a painful 5-day selloff that has taken it down 8.9% off of its high one week ago.

- Price and breadth were disconnected once again with today marking the 37th time this year that price and breadth moved in opposite directions.

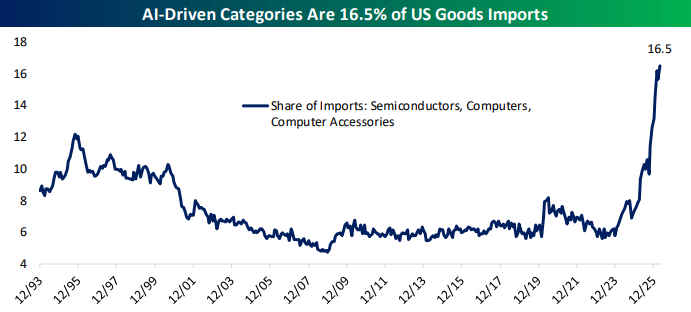

- AI-linked categories of imports continue to rise exponentially; accounting for 16.5% of total goods imports in April

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Morning Lineup – 6/9/26

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s not supposed to be easy. Anyone who finds it easy is stupid.” – Charlie Munger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

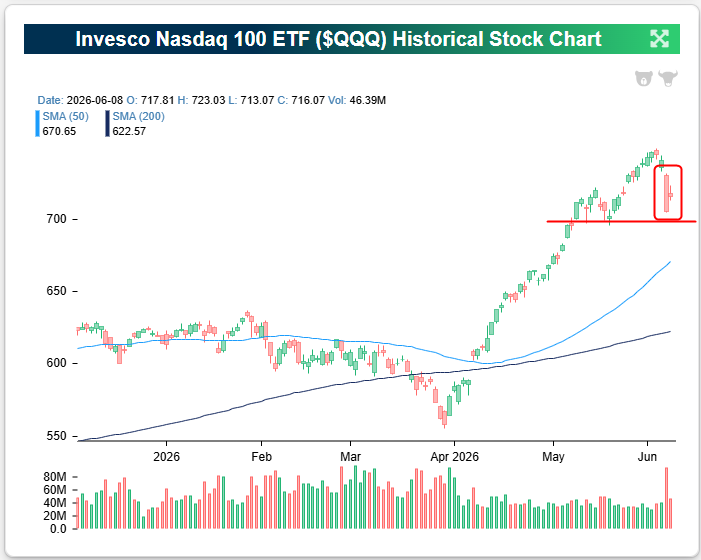

Crude oil is back below $90 this morning after President Trump suggested that a deal with Iran could be reached in the next 2-3 days. Equities are rallying as well with SPY up 40 bps pre-market and QQQ up double that at 80 bps.

Semis, AI, and quantum names are dominating the list of pre-market winners as investors rotate back into the areas that got hit hardest late last week.

After a 4%+ drop on Friday, the Nasdaq 100 (QQQ) rallied back 1.5% yesterday to start the new trading week. As shown below, the intraday range yesterday looks tiny compared to the huge red bar seen Friday. QQQ still needs to gain 3.3% just to get back to its closing level last Thursday.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Closer – Consumer Stocks and Expectations – 6/8/26

Log-in here if you’re a member with access to the Closer.

- Consumer facing stocks like durables, apparel, and lenders have made lower highs recently.

- The New York Fed’s Survey of Consumer Expectations saw a multiyear low in the range of one year inflation expectations.

- Consumer expectations for their financial situation in the year ahead had the worst showing since October 2022.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

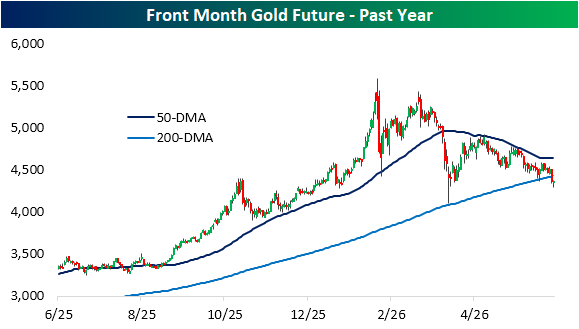

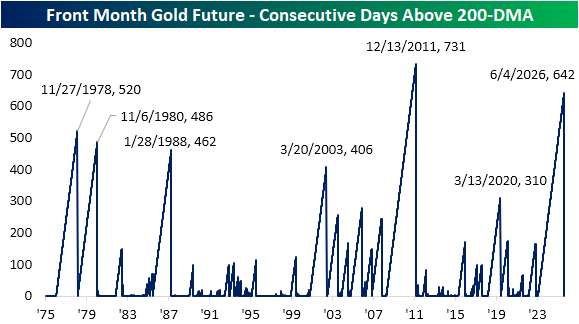

Gold Back Below the 200-DMA

Precious metals had a banner year in 2025, and that strength pulled through into the first month of 2026, peaking on January 29th. Closing in on the midpoint of the year, gold has been falling and is now basically back to flat on the year (now up 0.6% YTD). In the past few months as gold has reversed earlier gains, it has been consolidating between an upward trending 200-DMA to the downside, and a downward trending 50-DMA to the upside. Last Friday, the yellow metal picked a direction as it closed below its 200-DMA for the first time in two and a half years.

As shown below, Friday’s close below the 200-DMA was the first instance since November 10, 2023. That 642-trading day streak ended what was the second longest on record behind the 731-trading day streak ending in December 2011. For all streaks since 1975, it is only the seventh time it has extended to 300 trading days or more.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

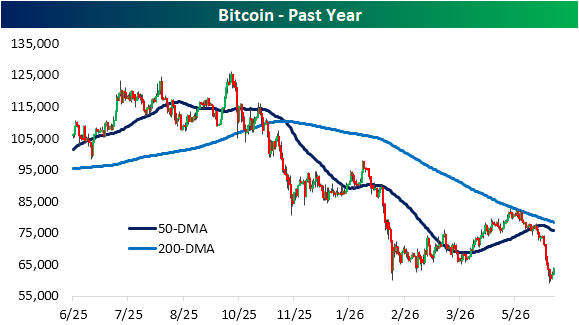

Bitcoin Cut in Half

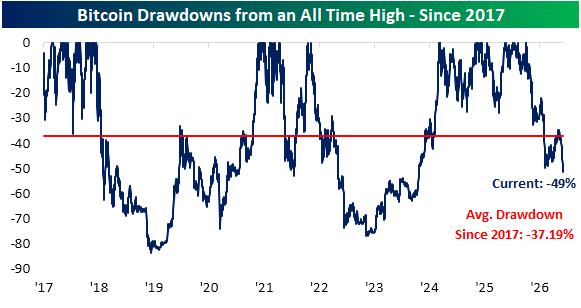

While there was a small rebound in weekend trading in addition to the start of the week on Monday, Bitcoin remains one of the more notable pain trades of late. As shown below, the world’s largest cryptocurrency has been in a downtrend since last fall when it broke below its 200-DMA. With a series of lower highs and lower lows since then, Bitcoin made an attempt to run up to that moving average as recently as mid-May, but the steep leg lower since then has resulted in 52-week lows last week when it traded below $60K for the first time since October 2024.

Talk about an ugly chart…

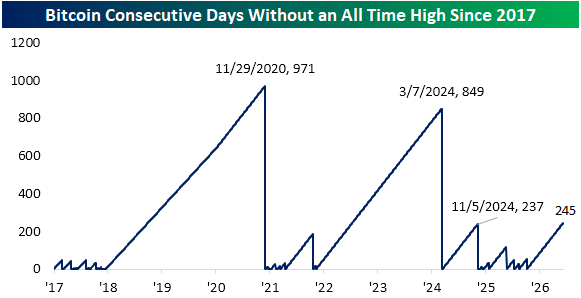

In the chart below, we show bitcoin drawdowns from all time highs since 2017 (when the crypto first traded above $1,000 and roughly when it came into the mainstream). It goes without saying that Bitcoin has been a volatile instrument. Since the start of 2017, it has been in a 37% drawdown on average. That includes a couple extended periods without new highs such as from 2018 through 2020 and 2022 through 2024. The crypto again finds itself in not only a longstanding drawdown (as of Monday it is on its 245th day without a fresh high, the third longest streak on record), but nearly cut in half versus its high from last October.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

The Triple Play Report: 6/8/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 6/8/26 – Assessing the Damage

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It takes less courage to criticize the decisions of others than to stand by your own.” – Attila the Hun (attributed)

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures are bouncing back to start the new trading week with the S&P 500 trading up roughly 0.7% pre-market, and the Tech-heavy Nasdaq 100 up about 1.3%.

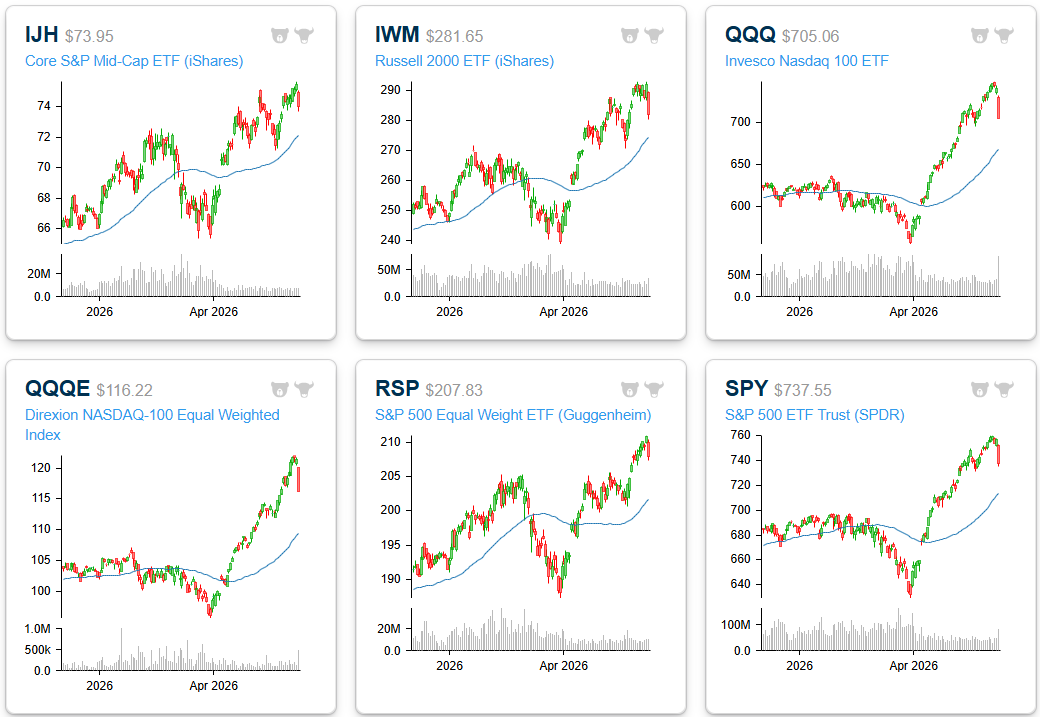

After a 33.7% rally from March 30th through last Tuesday’s close (6/2), traders finally rotated out of the QQQs late last week with a 5% drop from Wednesday through Friday. The S&P 500 ended a nine-week winning streak, and both the S&P and Nasdaq 100 moved out of overbought territory back to “neutral” levels.

As shown below, even with the drop on Friday, there’s still quite a large gap between current levels and the 50-DMA for both QQQ and SPY.

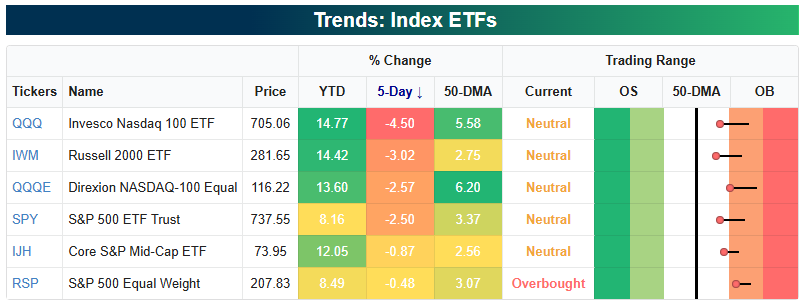

You can see the pullback into neutral territory in the snapshot of key index ETFs from our Trend Analyzer:

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Brunch Reads – 6/7/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

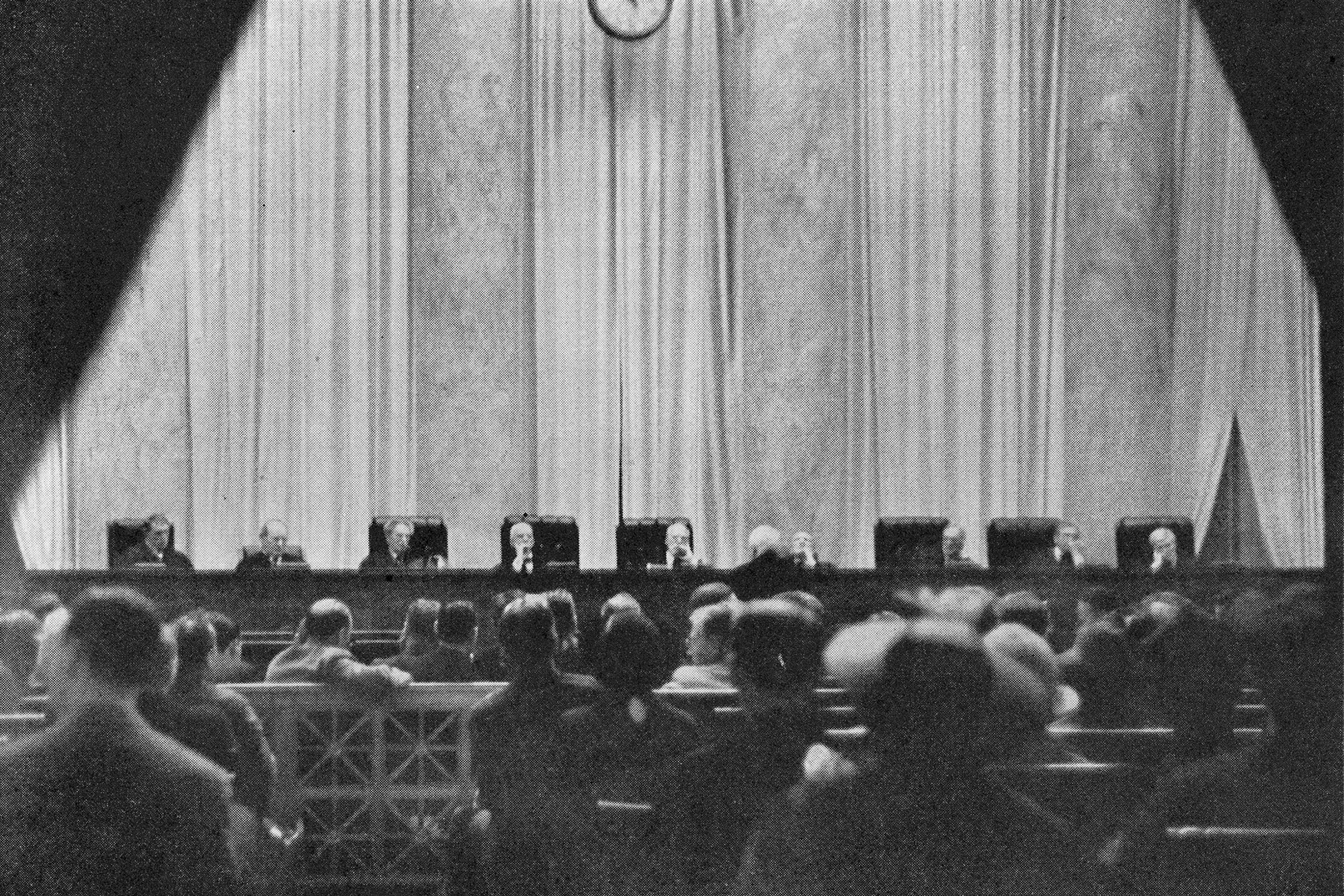

A Camera in the Courtroom: The June 7, 1937 issue of Time magazine featured something most Americans had never seen before: a photograph of the US Supreme Court in session. Today, that might not sound particularly noteworthy, but at the time, cameras were strictly prohibited inside the courtroom while the court was in session, making the image an extremely rare look at one of the country’s most influential institutions at work.

The photo was reportedly taken by a woman who smuggled a small camera into the courtroom hidden inside her handbag. By cutting a hole in the purse and taking the picture without looking through the viewfinder, she managed to capture the justices hearing arguments from the bench. The image was only the second known photograph of the Court in session and the first taken in the Supreme Court’s new building, which had opened just two years earlier in 1935.

The timing added to the photo’s significance. The Supreme Court was at the center of national attention in 1937 as President Franklin Roosevelt fought with the Court over New Deal legislation and pushed his controversial plan to expand the number of justices. Americans were reading about the Court almost daily, but few had ever seen what it actually looked like during proceedings.

While the photograph didn’t reveal any secrets about how the justices reached their decisions, it did provide a rare visual connection to an institution that largely operated out of public view. Nearly 90 years later, the Supreme Court still does not allow cameras during oral arguments, making that image from Time a reminder of how uncommon it has been for the public to get a firsthand look inside the courtroom.

AI & Technology

Hackers Simply Asked Meta AI to Give Them Access to High-Profile Instagram Accounts. It Worked (404 Media)

Hackers reportedly used Meta’s AI support chatbot to change the email addresses associated with Instagram accounts, allowing them to take over a number of high-profile profiles before the company fixed the flaw. The method circulated in Telegram groups for months and involved using a VPN, initiating a password reset, and convincing the chatbot to swap an account’s recovery email. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.