See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We are seeing unprecedented internal and external demand for AI compute resources.” – Anat Ashkenazi, CFO, Alphabet

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It was called a make-or-break night for earnings, and the bulls made it through. While the four major hyperscalers aren’t moving in unison this morning, futures are higher with the Nasdaq leading the way, trading up 0.5% while the S&P 500 is up slightly less (+0.40%). Next on the list? Apple (AAPL) after the close. Treasury yields are moving lower after yesterday’s spike, while crude oil is finally seeing a pullback for a change, although WTI is still trading at $105 per barrel. Gold and Bitcoin are both trading up by about 1%.

International markets had a mixed session. Asian stocks declined pretty much across the board, with Japan down just over 1%, but the yen surged as the BoJ gave a final warning regarding yen intervention. In Europe, stocks are generally higher with the STOXX 600 trading up 0.7%, led higher by the FTSE 100, which is up over 1%.

It’s a busy day for economic data in the US on top of tons of earnings, and outside of Chicago PMI at 9:45, all of the reports hit the tape at 8:30. We don’t have time to go through all of them here, but the results were generally OK. GDP was weaker than expected, inflation data was generally inline, Personal Income was stronger than expected, and jobless claims were much better than expected as initial claims fell below 200k!

This morning on CNBC, in a conversation between Gary Gohn and Andrew Sorkin, the former highlighted several positive aspects of the US economy right now. In response, Sorkin asked if it was “right that the market is just ignoring what’s going on in the Middle East right now?” It may feel as though, with the market hitting new highs, that it is ignoring what’s going on in the Middle East, but the reality is that up until this point, it hasn’t had much of an impact on the US economy.

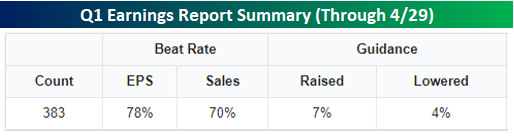

Over the last several weeks, we’ve cited numerous examples of economic data coming in better than expected, and last week’s Beige Book reinforced that trend. The Fed is even less concerned about economic weakness now than it was several weeks ago. This morning, jobless claims dropped below 200K! The latest round of earnings reports also reinforces this trend. Through yesterday, 78% of companies reporting exceeded EPS forecasts while 70% topped revenue estimates.

Those numbers are impressive but also backward-looking. What really stands out is the guidance. 7% of companies reporting have raised guidance this earnings season compared to just 4% that have lowered estimates. These companies see the same dire headlines regarding the Middle East each morning as you and I, but they also see what’s going on in their businesses. Things are strong enough that they feel confident in raising forecasts when they could easily use the uncertainty over the war and energy markets as an excuse to play it conservative.

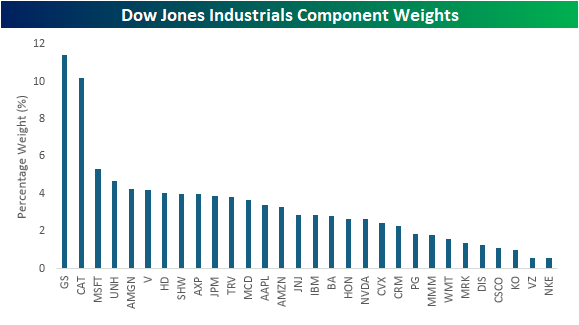

Yesterday’s earnings headline was the hyperscalers and how companies representing around 18% of the S&P 500’s market cap reported in one after-hours session. It wasn’t just the S&P 500. Since the close yesterday, companies representing more than 20% of the Dow reported earnings, but the main drivers weren’t Microsoft (MSFT) or Amazon.com (AMZN). These two companies represent a combined 8.7% of the index, but the big kahuna reporting in the Dow is Caterpillar (CAT). Because the Dow is price-weighted and CAT has a share price above $800 (second largest behind Goldman Sachs), it alone has a weighting of more than 10% in the index.

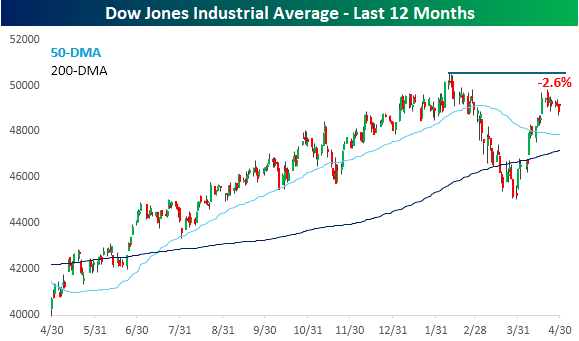

With shares of CAT trading up $48 in response to earnings, its gain will push the Dow higher by 300 points this morning. Combining that with the loss in MSFT and the gains in Amazon.com (AMZN) and Merck (MRK), these four companies will have a net positive impact of 320 points at the open. While that works out to a gain of over 0.6% for the index this morning, it still won’t be enough to push the Dow to new highs, as it would still be 2.6% below its record high from earlier in the year.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.