Fixed Income Weekly – 2/5/20

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we take a look at which types of stocks are most closely tied to interest rates.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Bespoke’s Global Macro Dashboard — 2/5/20

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

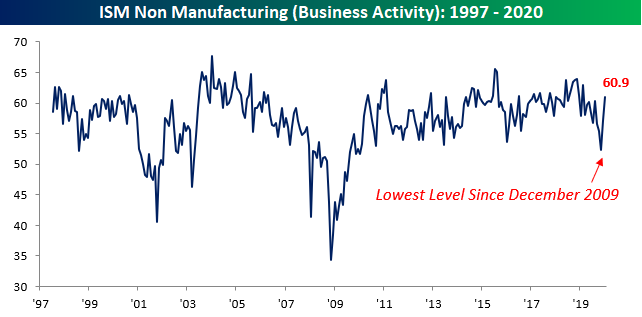

Services Sector Bouncing Back

Just like we saw with the Manufacturing sector earlier in the week, the services sector of the US economy also continued to bounce back in January. According to the ISM Non-Manufacturing report for January, activity bounced more than expected rising from 54.9 up to 55.5 and compared to expectations for a level of 55.0. After falling to its lowest level in over three years last September, activity in the services sector has now rebounded to its highest level since August. On a combined basis and accounting for each sector’s weight in the overall economy. the combined ISM for January bounced from 54.1 up to 55.0.

Respondents also appeared to be a lot more optimistic about business in January. As shown in the commentary snapshot below, there were a number of positive statements. In fact, Energy was the only sector where there wasn’t anything positive to say. No surprise there.

The table below breaks down the ISM Manufacturing report by each of its sub-categories and shows their changes over the last month and year. Despite the positive reading this month, the majority of sectors were actually down on both a m/m and y/y basis. On the positive side, Business Activity (chart below) topped 60 for the first time since last May, and along with Import Orders is the only category that was higher on both a m/m and y/y basis. To the downside, Backlog Orders and Inventories (lower two charts) have both steadily declined in recent months and are now at their lowest levels since 2012. Start a two-week free trial to Bespoke Institutional to access our full library of reports and interactive tools.

Big Gap Down For Ford (F)

As Tesla’s (TSLA) meteoric rise has been in the spotlight this week, another US automaker is moving in the opposite direction. Although it highlighted plans to attempt to breach into the electric vehicle market as the company’s future, Ford (F) reported a disappointing quarter after the close yesterday. Revenues came in at $39.7 bln which was handily above estimates of $36.5 bln, but also down 5% compared to the prior year. Wholesale units sold for 2019 totaled just 5.386 million compared to 5.982 million in 2018 as market share fell from 6.3% to 6.0%. Additionally, EPS missed estimates by 5 cents as the company continues to try to cut costs and reiterated plans to close six European plants. Perhaps the biggest disappointment in last night’s report was the guidance. The company is now forecasting full-year 2020 adjusted EBIT of $5.6 bln to $6.6 bln compared to analyst estimates of $7.37 bln. Given these results, the stock gapped down over 8% this morning. This would bring the stock to its lowest level since the end of October and would be the largest gap down the stock has experienced in reaction to earnings since at least 2001 as shown in the snapshot of our Earnings Explorer below.

If it is any consolation, the fourth quarter has historically experienced the weakest stock price performance for Ford (F) in reaction to earnings. It is the only quarter’s report where the stock has averaged a gap down at the open, and in terms of full-day reactions, F has been higher only 28% of the time following its Q4 report. As a result of today’s losses, Ford’s (F) already high dividend only lifted higher. Ford shares now yield well above 7% compared to ~6.5% as of yesterday’s close. So, in addition to having the lowest share price in the index, F now also has one of the highest dividend yields in the S&P 500. Start a two-week free trial to Bespoke Institutional to access our interactive Earnings Explorer, Chart Scanner, and much more.

Russell 1,000 Most Heavily Shorted Stocks

In Monday’s Closer, we detailed the short squeeze in Tesla (TSLA) that has been playing out. Back in May, when short interest as a percentage of float for TSLA topped out at 33.16%, it was the third most highly shorted stock in the Russell 1,000. Today, you will not find Tesla in the top 10, 20, or even 30 of the most heavily shorted Russell 1,000 stocks. In fact, after rallying well over 100% so far in 2020, it is the 37th most highly shorted stock with 17.55% of the float short. Of the most heavily shorted stocks, TSLA by far is the largest with a market cap of $127.32 bn.

The table below lists the 40 stocks in the Russell 1000 with the highest short interest as a percentage of float. Behind TSLA, the second-largest stock in terms of market cap of the stocks listed is Match Group (MTCH) which is less than a fifth the size of TSLA. Currently, MTCH is also the only stock in the Russell 1000 with more than half of its shares shorted (60.14%). That is after it was one of the top performers of the group last year, rising 95.79%. Some other big winners in 2019 which are now being bet against the most are Beyond Meat (BYND) that rose over 200% since its IPO, Carvana (CVNA) which rose 187%, Ubiquiti (UI) which rose over 93%, and Caesars Entertainment (CZR) which is also up over 100%. On the other hand, big losers like Range Resources (RRC), Antero Midstream (AM) and 2U (TWOU) continue to be bet against amidst major declines in the past year, and they have not found any respite so far in 2020.

In terms of performance for most heavily shorted stocks so far this year, of the stocks listed below, the average YTD change is a gain of 1.3%. However, if you take Tesla (TSLA) out fo the mix, the average performance shifts to a decline of 1.75% as 23 of the 40 stocks listed are down YTD. Start a two-week free trial to Bespoke Institutional to access our full library of reports and interactive tools.

Bespoke’s Morning Lineup – 2/5/20 – 2.0

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Global equities are in rally mode again this morning on easing concerns over the impact of the coronavirus and news of possible treatments. One number we’ve been watching closely over the last couple of weeks is the mortality rate which continues to drop. Through the latest reported global statistics, the mortality rate has dropped down to 2.01% which is the lowest we have seen since statistics have been published.

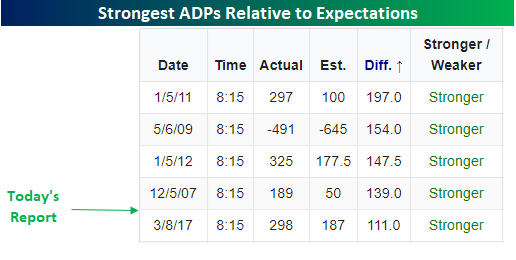

In economic news this morning, the ADP Private Payrolls report came in much higher than expected (291K vs. 157K). This was the strongest monthly print since May 2015 and the best report relative to expectations since the December 2011 report on 1/5/12 (325K vs 178K).

In economic news this morning, the ADP Private Payrolls report came in much higher than expected (291K vs. 157K). This was the strongest monthly print since May 2015 and the best report relative to expectations since the December 2011 report on 1/5/12 (325K vs 178K).

The Closer – Yield Bounce, Earnings Interest, Manufacturing Sales, States Lead – 2/4/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at the move higher in rates from a technical perspective as well as news out of Disney (DIS) and Facebook (FB). We then recap today’s durable goods data and Mexican remittance numbers. We finish tonight with a look at state-level leading indices.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

JetBlue (JBLU) Fading Airline Blues

Earlier today, we updated our weekly Stock Scores with major US airliner JetBlue (JBLU) taking the number one spot. Our Stock Scores ranks every company in the S&P 1500 based on a fusion approach, combining proprietary ratings across fundamental, technical, and sentiment analysis. JBLU is one of the smaller US airlines with a total market cap of $5.2 bn compared to competitors like Delta (DAL), Southwest (LUV), United (UAL), and American Airlines (AAL), which all have market caps between $10 bn and $32.8 bn. While earnings for this industry have not necessarily been weak, those companies exposed to the ongoing Boeing 737 MAX saga have continued to report headwinds, and shutdowns on account of the coronavirus have added more uncertainty to the overall outlook of the industry. But for JBLU, the picture is a bit rosier. Unlike some of its larger competitors, JBLU does not fly the 737 MAX, and its flights to Asia are limited when compared to other airlines as it focuses on the domestic, Caribbean, and Latin American markets. This contributed to a solid quarter recently as the company exceeded EPS estimates and reported stronger than expected revenues which were up 3.2% YoY.

Headed into its most recent earnings report on January 23rd, JBLU reached the upper end of the past two year’s range as shown in the chart below. The 6.41% rally on earnings lifted the stock back above the $20 resistance level which it has since come back and successfully retested.

Meanwhile, the charts of other airline stocks are not looking as strong with many having broken down or sitting in short term downtrends. Members can view the charts of all of these airline stocks using this custom portfolio we created.

Again, JBLU’s breakout has been more of an exception rather than the rule for the industry. The chart below of the U.S. Global Jets ETF (JETS), which tracks the global airline industry including operators and manufacturers, shows exactly this. Like JBLU, in the first weeks of this year, the ETF had been testing the past year’s highs, but once coronavirus fears began to ramp up (namely as Delta, American Airlines, and United Airlines began to suspend service to China), JETS turned sharply lower and has fallen out of the past few months’ range.

After these declines, the average airline stock in the S&P 1500 now has the lowest P/E ratio of all GICS Level 3 Industries. Given this, JETS has one of the cheaper valuations of the ETF universe. The fund’s P/E ratio is now only 8.76 which is also especially cheap when compared to a 23.12 P/E for the broader Industrial Sector ETF (XLI). Overall, although the 737 MAX and more recent coronavirus headwinds have not gone away, the airline industry is now looking relatively cheap to the rest of the market and JBLU appears to be the best of breed of these stocks. Start a two-week free trial to Bespoke Institutional to access our Stock Scores, Custom Portfolios, and much more.

Bespoke’s Morning Lineup — Another Turnaround Tuesday — 2/4/20

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Tesla Soars, Google Flops, Construction, SLOOS – 2/3/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a dive into Tesla’s massive run-up over the past few weeks and where that leaves the company relative to other global auto manufacturers. Next, we review Alphabet’s (GOOGL) earnings before turning to today’s macroeconomic data including construction spending and the Federal Reserve’s first-quarter Senior Loan Officer Outlook Survey (SLOOS).

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!