Bespoke’s Morning Lineup – 10/16/25 – Sentiment Weakens

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“‘That didn’t work’ is cool, but ‘that won’t work’ is not a way to go through life.” – John Mayer

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

A triple play from Taiwan Semiconductor (TSM)—beating on earnings, revenue, and guidance—is lifting US equity futures, with technology stocks at the forefront. This rally is notably happening despite the President stating yesterday after the close that, “We are in one now,” in reference to a trade war with China. There are also signs that China’s aggressive stance on rare earth exports could be backfiring, as it has started to cause a more unified front between the US and other international partners.

Today was supposed to be a busy one for economic data, but the government shutdown put the kibosh on that, and the only report released was the Philly Fed Manufacturing report, which came in weaker than expected. The pace of earnings, however, remains active, and once again this morning, we’re seeing generally strong results.

Outside of equities, crude oil is fractionally higher but still well below $59 per barrel, the 10-year yield is trying to hang on to 4%, gold and other precious metals are rallying (what else is new), and crypto is also rallying after what has been a rough week for the sector.

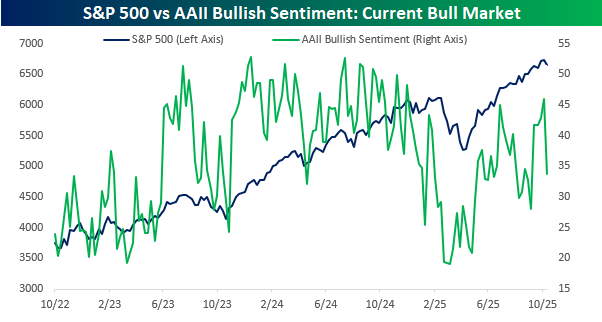

It’s been a somewhat rocky week for US equities, although by the standards of October, it’s hard to get too worked up. After trading at an all-time high intraday last Thursday, the S&P 500 closed modestly lower on the day. That modest decline was followed on Friday by a sharp 2.7% decline in the S&P 500 as trade issues with China and concerns over corporate credit in the auto sector nudged investors to take some risk off the table. This week started on a positive note as the S&P 500 erased half of the losses from last Thursday and Friday, but intraday trading has been more volatile, and there’s been more of a tendency to sell rips than buy dips.

The skittishness showed up in investor sentiment this week as the weekly American Association of Individual Investors (AAII) survey showed that bullish sentiment dropped from 45.9% to 33.7% for the lowest reading in a month. The decline in bullish sentiment comes even as the S&P 500 closed within 2% of a record high yesterday. While bullish sentiment was routinely near 50% throughout 2024 as the market rallied, in the bounce off the April lows, investors have been much less willing to hop on the bandwagon.

Along with the modest weakness in US stocks over the past five trading sessions, global equities have also been under pressure. Of the US-traded ETFs tracking the stock markets of the seven G7 countries, all but France (EWQ) traded lower in the five trading days ended yesterday, and the US was stuck right in the middle with a decline of 1.2%. The biggest laggards have been Italy (EWI) and Germany (EWG) as their the only two below their 50-DMAs. Markets have certainly been on a tear this year as six of the seven ETFs listed have rallied at least 20% this year, but in the short run, they’ve mostly worked off their overbought conditions as France is the only country still in extended territory.

The Closer – La Cucaracha, Beige Book, Credit Cards – 10/15/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a note on the two significant credit blow ups in September and a quantitative look at the Beige Book (page 1). Next, we review the latest credit card delinquency rates (page 2) and wrap up with a recap of the latest transport earnings (page 3).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Wealth Management Report – October 2025

Please click here or on the link below to read our latest quarterly Wealth Management Report. You can learn more about Bespoke’s wealth management services available to investors here or by calling our office at 914-315-1248.

Below are links to prior quarterly Wealth Management Reports:

Bespoke’s Morning Lineup – 10/15/25 – You Can’t Take it Back

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Stock prices have reached what looks like a permanently high plateau” – Irving Fisher, 10/15/29

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a sell-off into the close yesterday, equity futures are rallying this morning on the back of strong rallies in Asia and Europe. S&P 500 futures are up 75 bps while the Nasdaq is up 1%. In the commodities space, crude oil is little changed, while gold is up another 1% and now over $4,200 per ounce.

While there’s little economic data on the calendar again today, it’s been another strong showing for earnings this morning as eight of the ten companies reporting exceeded bottom-line results, while Progressive (PGR) was the only miss. Revenues have also been strong as the pace of beats has been nearly as strong.

We’ve all said things that we wish we could take back, and we can all come up with countless examples involving a boss, friend, family member, spouse, and/or our kids. You don’t need us to give you examples. In a less personal sense, it’s always funny to look back at past comments from public figures and, with the benefit of hindsight, see how foolish or wrong their comments turned out to be.

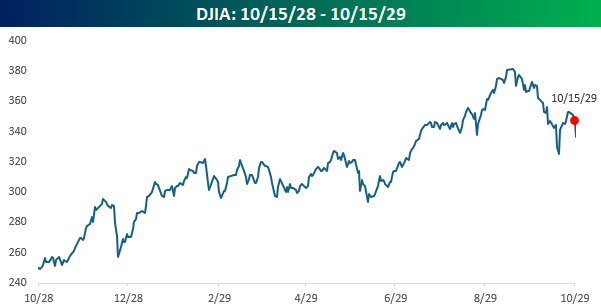

The stock market has seen a lot, but one of the most famously disastrous comments was made exactly 96 years ago today when an economist named Irving Fisher spoke at an industry trade dinner in New York. Fisher was one of the most well-known economists of his generation. Joseph Schumpeter called him the “greatest economist the United States has ever produced”. His theories on the velocity of money helped him forecast swings in inflation and the economy, and he wrote a weekly economic column that was read by millions of readers. He spoke to audiences all over the country, and they hung on every word.

The most famous or infamous of those speeches came on 10/15/29 when he made the quote above, and then followed it up later on in an informal Q&A session, saying he expected “to see the stock market a good deal higher than it is today, within a few months.”

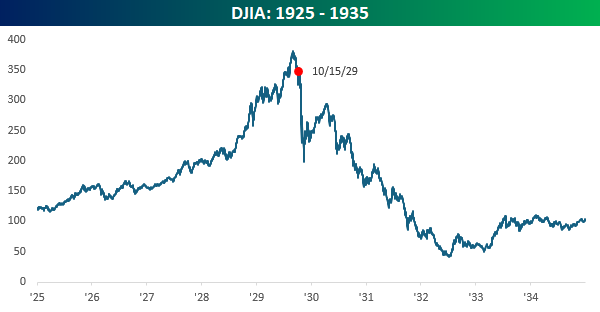

When Fisher made those comments, the equity market was coming off a solid year of gains. While the Dow was down about 8% from its September high, it was still up over 40% in the prior year. And that was coming off what had been one of the strongest four-year stretches in stock market history, where the index had tripled! Given the path equities had taken, Fisher’s comments were hardly out of consensus. At that point, gains were expected.

While investors were feeling entitled to gains, what the market giveth, it can quickly take away. The day after his comments, the Dow fell by over 3%. Then, after a one-day bounce of 1.7%, it had back-to-back declines of over 2.5%. Then, it kept falling from there. On 10/23, the DJIA fell 6.3%. On 10/24, it fell another 2%. Then, on 10/28, the crash came as the Dow fell 13% followed by another decline of 12% the day after that. Just after Labor Day of 1929, the Dow was at record highs, basking in the heat of the roaring 20s. Now, less than two months later, it was down 40%.

Looking at a ten-year window of the Dow from 1925 to 1935, from its peak in 1929 to the low three years later, it lost nearly 90% of its value. The economy sank into the Great Depression, erasing generations of wealth and causing permanent damage to the fabric of the US economy. Maybe not creative, but destruction nonetheless!

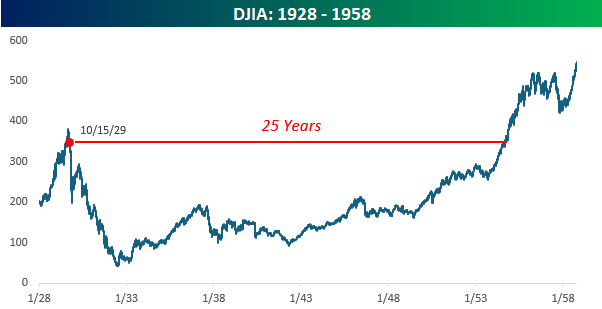

The S&P 500 closed at record highs just a week ago today, so no matter how steep the selloffs have been over time, the market has always come back. Sometimes, though, the comebacks take longer than others. After the peak this February, it only took a few months. After the 2022 peak, though, it took two years for the market to make new highs. Coming out of the Financial Crisis, it took close to five years. After the dotcom bust, it took seven years. The takeaway is that it’s all about time horizons. If you’re invested in the stock market, long periods of drawdowns shouldn’t necessarily be a baseline expectation, but they should be part of the plan. Coming out of the 1929 peak and Fisher’s comments from October 1929, those levels on the Dow wouldn’t be seen again for another 25 years! That type of drought should certainly not be a base case for investors, but it should provide some balance to a growing feeling of entitlement in some areas of the market where double-digit daily percentage gains are starting to feel like an Inalienable right.

The Closer – Energy Glut, First Earnings, Freight Fumble – 10/14/25

Log-in here if you’re a member with access to the Closer.

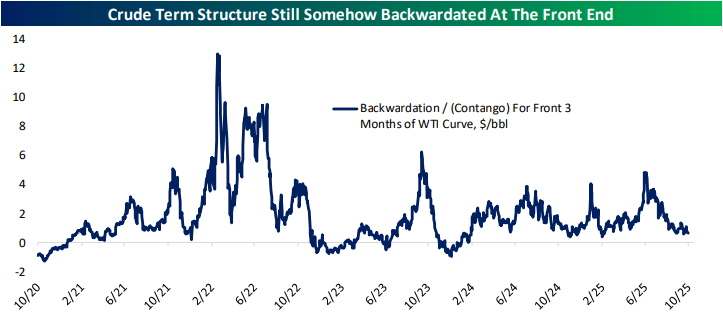

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a look into the growing supply glut of crude oil (page 1) in addition to how that functions into the term structure (page 2). We also review how oil companies look in addition to recapping today’s earnings and Fedspeak (page 3). We finish with a recap of the latest freight data and the lagging performance of associated stocks (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

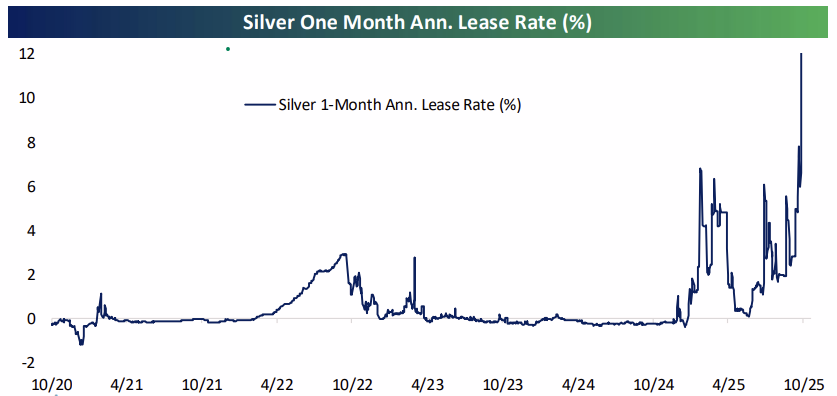

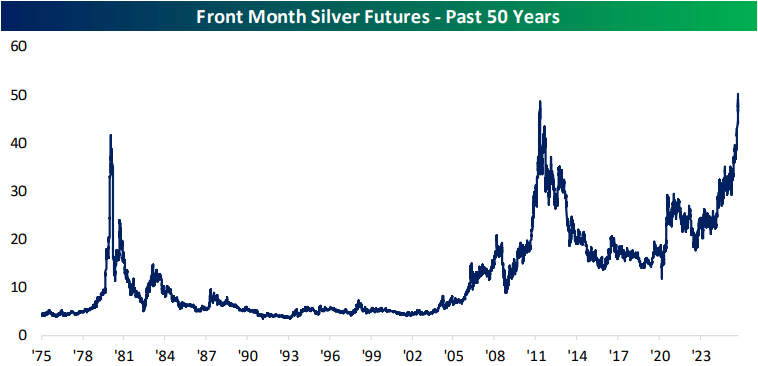

Silver Squeeze

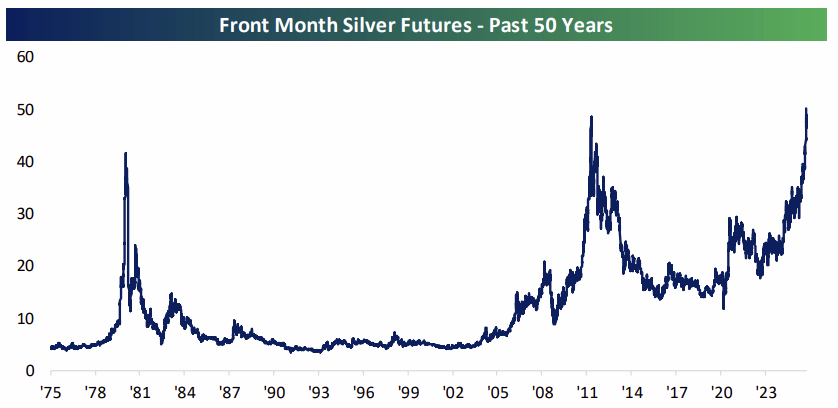

Silver futures paused their breathtaking rally today after its first trip over $50/oz since the 1980s on Friday. Year-to-date, spot silver has risen over 70%, outperforming gold’s 56% gain or bitcoin’s 19% advance, let alone the downright pedestrian 14% move in stocks.

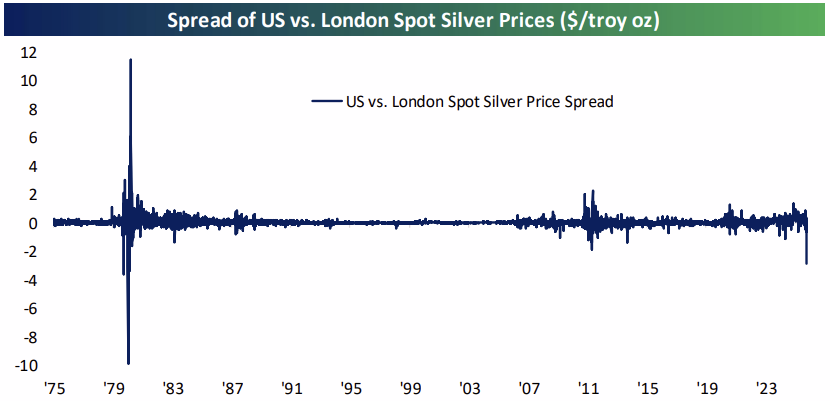

One massive driver of the move has been a physical short squeeze in the London silver market specifically. Earlier this year, US imports of silver surged with much of the bullion being sourced in London. Traders were trying to make sure they could inventory silver in the US for financial speculation and industrial uses before tariffs hit, and as a result, inventories of silver in London cratered while they surged in New York. The blistering rally in silver that has taken place since helped drive the London market into chaos as it didn’t have enough physical bullion to be delivered amidst rapid price gains. The result is an epic short squeeze, not as large as the infamous Hunt Brothers squeeze in US silver markets back in 1980 but nonetheless impressive. New York spot silver now trades at the largest discount to silver in London since the Hunt Brothers episode and the volatility that came with it.

With not enough silver to go around, lease rates on silver in vaults have soared; borrowing silver to deliver on futures contracts and other derivatives is still possible, it’s just a lot more expensive to accomplish than has been the case in recent years as shown in the chart below.

The soaring cost of borrowing silver thanks to a lack of bullion in London is a good example of the pitfalls of a precious metal-backed financial system. The oddity of tariffs have served as a sort of supply shock, similar to mines going offline due to a natural disaster. When supply drops, price (the lease rate) rises. In an economy reliant on bullion to anchor its money supply, positive or negative supply shocks can have a huge impact on money supply, regardless of whether economic circumstances like growth or inflation justify changes in the cost of money (interest rates). That’s one very good reason that the world shifted from gold or silver anchors to fully fiat currencies during the 20th century.

Like this content? This analysis was included in our nightly macro note, The Closer, on 10/13. We are sharing it here on a complimentary basis. To receive our Closer in your inbox daily, start a two-week trial to Bespoke Institutional today.

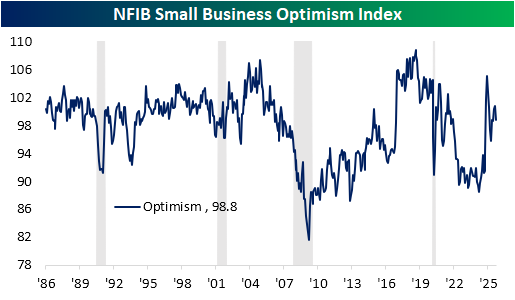

Small Business Hesitation

The continued US government shutdown means there remains a drought in official economic data, putting extra emphasis on unofficial data points. One such set of data is monthly small business optimism from the NFIB released this morning. The headline index dropped to 98.8 in September versus 100.8 previously in August. As we often note, including in our discussion of the report’s labor market readings in today’s Morning Lineup, the NFIB survey has historically leaned right similar to how Michigan Confidence has leaned left. Such biases mean that the data has to be taken with a grain of salt and some categories become more worthwhile in gauging economic health than others. As shown below, optimism surged in the wake of President Trump’s election last year. A similar surge was seen following the 2016 presidential election and vice versa after President Biden won in 2020. At current levels, optimism is middling versus the past decade’s range.

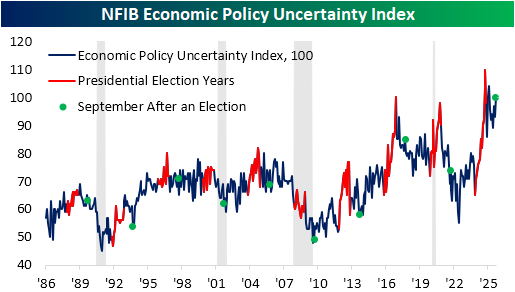

One area that is far from middling is uncertainty. Again, this is another indicator from NFIB that is a bit more sensitive to politics. Typically, the Economic Policy Uncertainty Index soars during Presidential election years and then pulls back in the following months; usually that pullback is regardless of which party came out on top. During last year’s run up to the election, this index saw a record climb, but interestingly, it has yet to reverse lower as it usually does after elections.

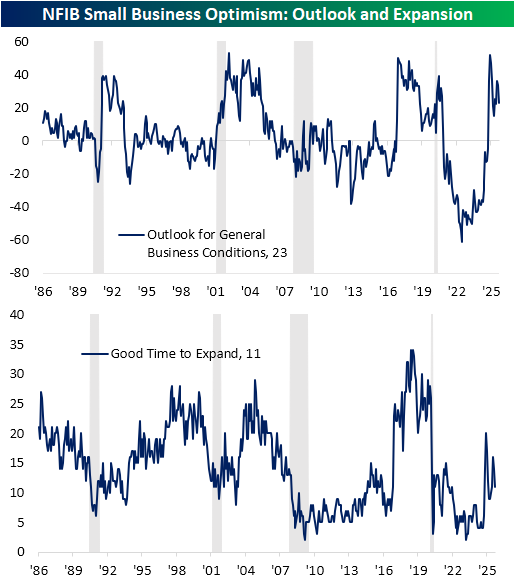

In other words, small businesses are still on edge when it comes to policy. That is putting a dampener on sentiment with fewer businesses reporting a positive outlook for the economy/general business conditions. Similarly, fewer respondents reported that they view now as a good time to expand their businesses.

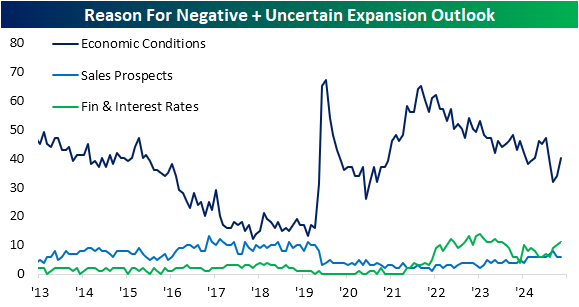

When it comes to the question of business expansion, respondents are also asked for the reasons for given outlooks. For those reporting negative and uncertain outlook, the largest share of respondents (40%) reported that it is due to economic conditions. That is up versus the multi-year low of 32% two months prior. While that reading is rebounding, it hasn’t really reversed the downtrend of the past several years. While not shown in the chart below for legibility, the next two most common reasons given were cost of expansion and political climate; each of those came in at 12% which is right in line with their respective average over the past year. Finances and interest rates were right on their heels at 11%, and this reading has the more interesting trend. The share viewing rates and finances as restrictive to expansion has steadily been climbing despite the latest rate cuts.

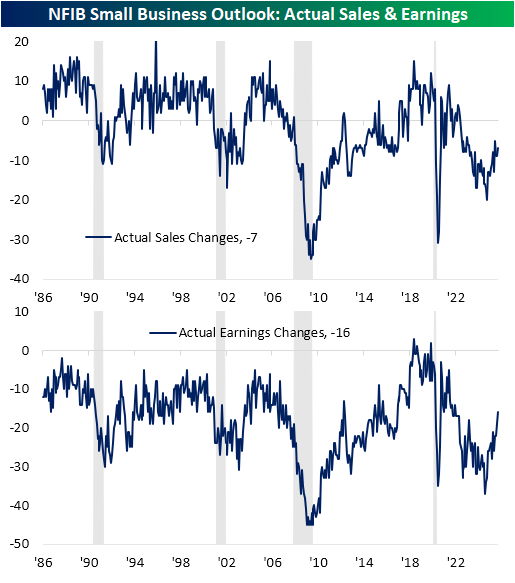

Finally, we would note that sales prospects are not a very common reason given for a negative or uncertain expansion outlook, and paired with other categories in the report, would overall suggest solid demand. As shown below, actual sales changes are negative (as has been the norm for the better part of the past 20 years) but approaching some of the strongest levels since Q1 2023. Meanwhile, actual earnings changes have rocketed higher up to the best level since December 2021.

Bespoke’s Morning Lineup – 10/14/25 – Stuck in the Middle

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Pessimism never won any battle.” – Dwight Eisenhower

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If the market rallies on a bank holiday, does it count? Judging by the declines in US equity futures and cryptocurrency markets, it appears not. S&P 500 and Nasdaq futures point to a drop of about 1% at the open, which would erase about two-thirds of Monday’s gain. Declines in the crypto space look even scarier as Bitcoin drops 4% and Ethereum traded back down below $4,000 with a decline of nearly 7%.

The catalyst for this morning’s weakness stems from continued trade tensions with China as both countries start charging additional fees on each other’s cargo ships, and China imposed further sanctions on certain US shipping subsidiaries. The weakness also comes even after a strong batch of earnings reports on what is really the first busy day of earnings for the Q3 reporting period.

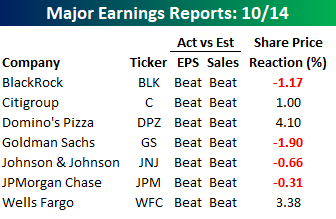

As shown in the table below, of the seven major reports this morning, all seven reported better-than-expected EPS and sales, but only three are trading higher in reaction to the reports. Domino’s (DPZ), Wells Fargo (WFC), and Citigroup (C) are all up 1% or more, while Goldman (GS) leads the declines with a drop of nearly 2%.

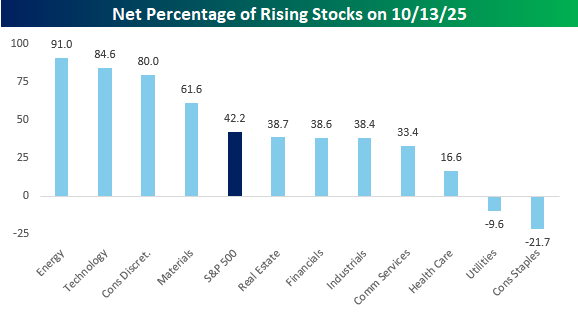

The S&P 500 had a good day to start the week yesterday, but breadth wasn’t exactly strong, especially for a day when the index rallied over 1.5%. As shown in the chart below, only four sectors saw a net of 50% or more of their components finish higher on the day. Energy and Technology led the charge with 90%+ of each sector’s components finishing higher on the day, while Consumer Discretionary (+80%) and Materials (+62%) were the only two other sectors where net breadth was stronger than the S&P 500. On the other end of the spectrum, Consumer Staples (-22%) and Utilities (-10%) both had negative net breadth, while Health Care also was relatively weak at just 17% net positive.

What was unique about yesterday’s trading, though, was that it was an extreme ‘inside’ day for the S&P 500 tracking ETF (SPY). An inside day in the market occurs when the intraday high for a day stalls out short of the prior session’s high, while the intraday low is higher. Not only did we have an inside day yesterday, but the intraday high was 1.3% below Friday’s high, while the intraday low was 1.1% above Friday’s low. We finished the day stuck right in the middle of the prior day’s range!

Inside days in SPY where both the intraday high and intraday low were more than 1% below or above the prior session’s extreme have been extremely rare. Since 1993, there have only been 11 other occurrences, with the most recent occurring back in April, right after the tariff-tantrum low. But before that, you have to go back to December 2020, and then before that, August 2015.

The Closer – AI Deal Flow, Consumers & Cattle, Silver Squeeze – 10/13/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with an overview of the interdependence of the mega-caps (page 1) followed by a check up on today’s rotation (page 2). Given a lack of official economic data, we next dive into a handful of alternative health checks on consumer spending (page 3). After that, we review food commodity prices including the new highs in beef prices (pages 4 and 5). We finish with an overview of the squeeze that has driven silver to new record highs (pages 6 and 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q3 Earnings Season Begins

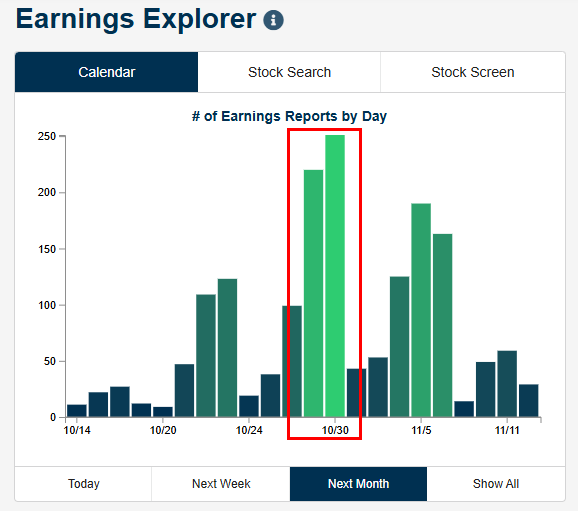

The Q3 earnings season will begin in earnest tomorrow morning with four big banks and brokers set to report ahead of the open.

As the snapshot below from our useful Earnings Explorer tool shows, though, the peak of earnings season is still a couple of weeks away later this month. This quarter’s biggest day for earnings will be Thursday, October 30th, when roughly 250 companies will report Q3 numbers.

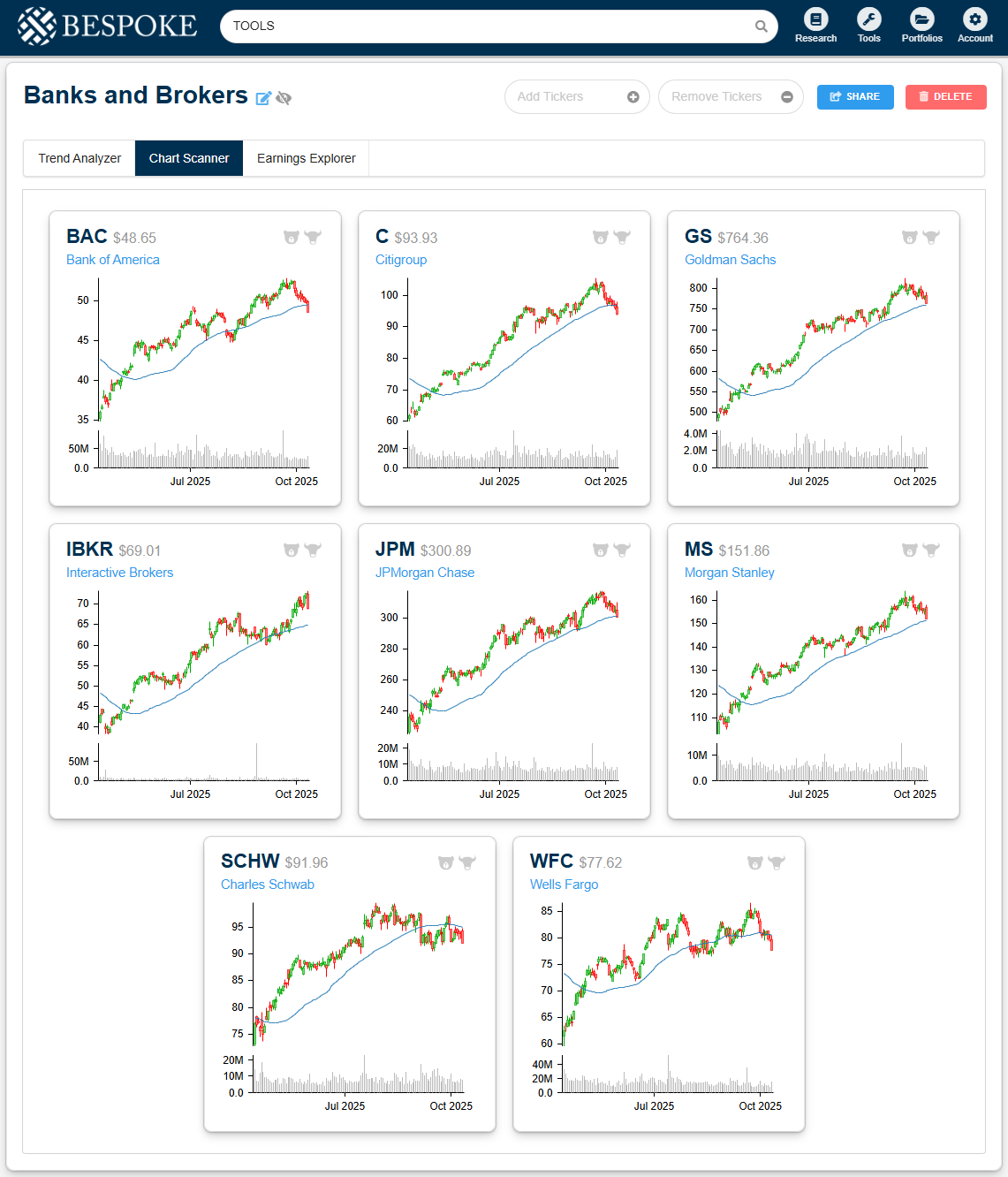

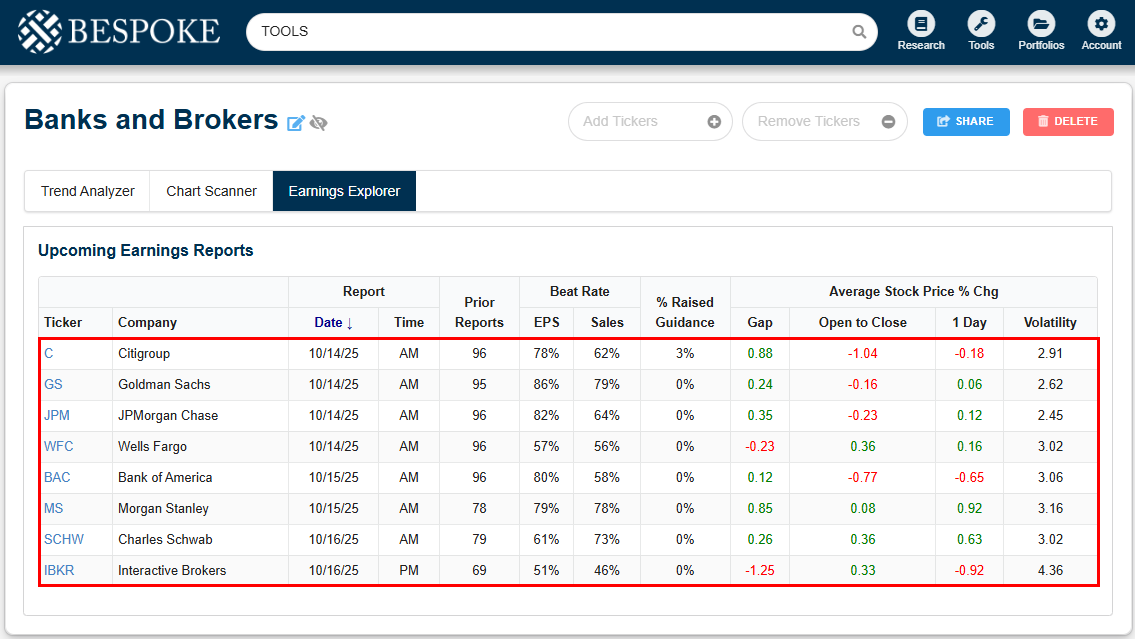

Eight big banks and brokers will report Q3 numbers in the next few days. We created a custom portfolio — just like subscribers can do — that includes each of these eight stocks so that we can take a closer look at them.

Starting with earnings, tomorrow morning we’ll hear from Citigroup (C), Goldman Sachs (GS), JP Morgan (JPM), and Wells Fargo (WFC). Of these four stocks, Goldman has the strongest “beat” rates, while Wells Fargo has the weakest. (A stock’s beat rate represents the percentage of the time it has beaten consensus analyst estimates.)

Bank of America (BAC) and Morgan Stanley (MS) will then report on Wednesday morning, while Charles Schwab (SCHW) and Interactive Brokers (IBKR) will report on Thursday.

In terms of share price reactions to earnings, Morgan Stanley (MS) is the name that has historically averaged the biggest gains on its earnings reaction days. IBKR has averaged the biggest declines and been the most volatile of the names listed.

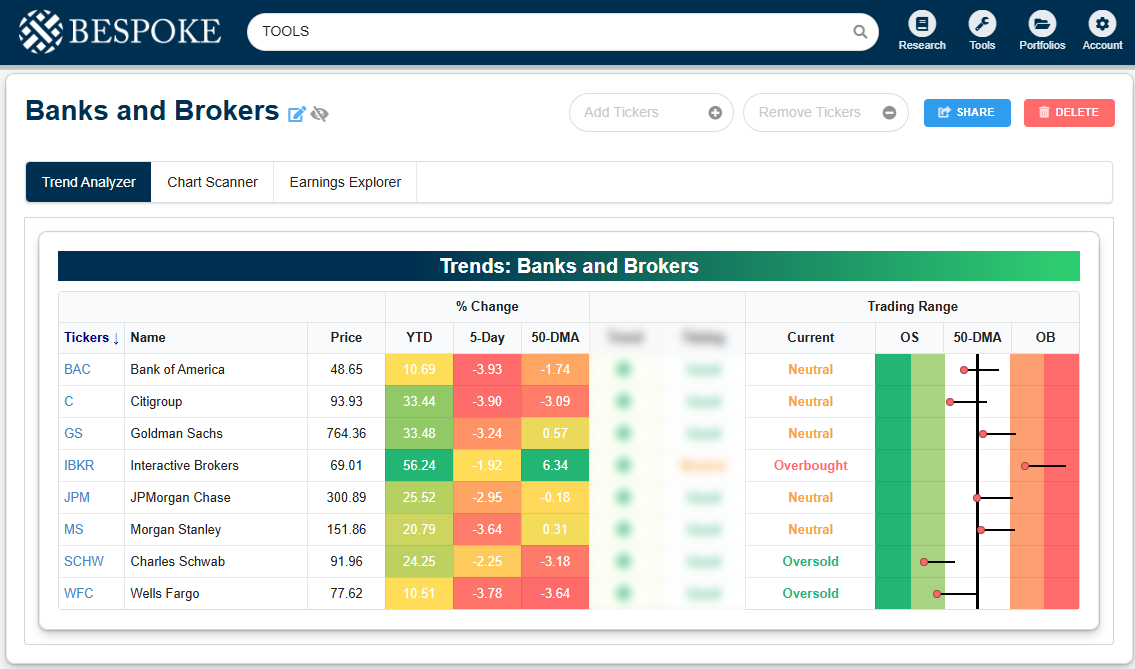

Our Custom Portfolios tool also lets you create baskets like the one below in a few simple clicks to monitor trends and trading ranges for the stocks and ETFs you care about most.

For our “Banks and Brokers” basket, you can see that all of these stocks have pulled back sharply within their ranges over the last week, following Friday’s big pullback. Heading into this week, IBKR was the only name still in “overbought” territory, while SCHW and WFC had both moved into “oversold” territory.

Regardless of recent moves, all eight of these stocks are up at least 10% year-to-date, with IBKR up the most at 56.2%, followed by Goldman and Citi with YTD gains of more than 33%.

Along with the ability to easily monitor upcoming earnings reports as well as trend and timing measures, our Custom Portfolios tool lets you quickly scan price charts as well.

Below is a snapshot of six-month price charts for our Banks and Brokers basket. Notably, Goldman (GS), Morgan Stanley (MS), and Interactive Brokers (IBKR) were the only three that managed to hang on above their 50-DMAs following last Friday’s big market drop. The rest broke hard below their 50-DMAs, which puts their long-term uptrends at risk.

If you like this analysis and want to try it out with your own stocks and ETFs, simply start a Bespoke Institutional trial now and proceed to the Custom Portfolios tab. It’s super easy! Use this link to get a complimentary two-week trial plus 20% off the regular monthly rate if you choose to stick with it.