Bespoke Matrix of Economic Indicators

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Bespoke Market Calendar — March 2025

Please click the image below to view our March 2025 market calendar. This calendar includes the S&P 500’s historical average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases. Click here to view Bespoke’s premium membership options.

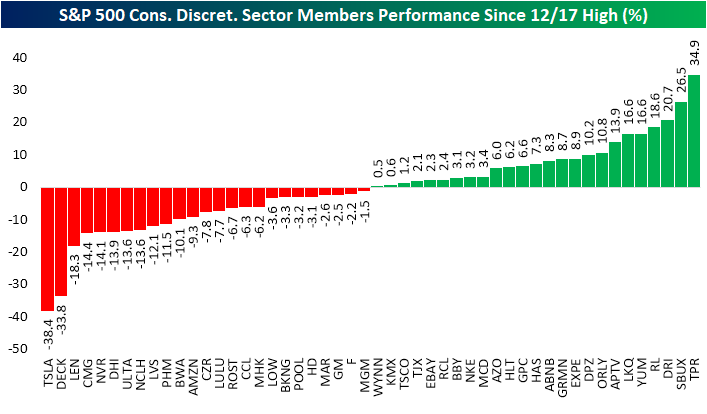

Where’s the Weakness in Discretionary?

Entering the final month of the first quarter, most S&P 500 sectors are sitting on year-to-date gains, although there are two notable exceptions. The Tech sector is currently down 5.29%, which has dragged on broader market performance, given it’s by far the largest sector by market cap. Consumer Discretionary is down an even worse 5.65% year to date, and returns look even worse when compared to the December 17th high. Since then, the sector is down just under 12%. As shown below, using the sector ETF (XLY) as a proxy for the group, that latest correction leaves it in no-man’s-land between the 50 and 200-day moving averages with the recent low finding some support around the November post-election low.

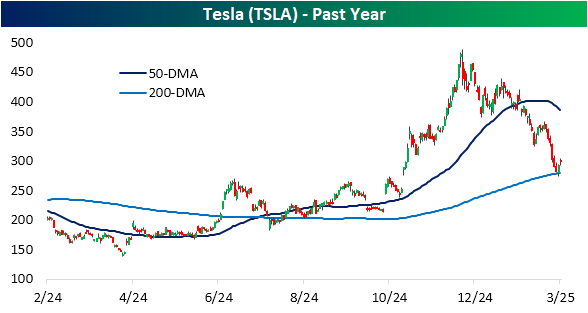

Taking a look under the hood, breadth since that December high hasn’t been that bad. Of the 50 stocks in the sector, half are higher, and half are lower since the high. However, there is a far larger weight in the losers than the winners. Among the decliners are the sector’s largest names: Tesla (TSLA) and Amazon (AMZN). Given that the S&P 500 is weighted by market cap, those declines in the mega caps—namely the outsized 38.4% drop in TSLA shares—have acted as significant drags on broader index performance.

Zeroing in on Tesla (TSLA), the stock peaked a day after the Consumer Discretionary sector, closing at a 52-week high on December 18. Regardless, it’s been a brutal period of selling since then. The stock’s nearly 40% decline saw it crash through its 50-DMA, and in the past few days, it has found support at its longer term 200-DMA.

Again, the S&P 500 and its sectors use a market-cap-weighted methodology, meaning stocks with larger market caps (like Tesla) will have a greater impact on the index than smaller peers. That also makes equal-weight versions of the indices useful in canceling out some of that noise and providing a better look at breadth. As shown below, whereas the market-cap weighted sector ETF (XLY) is down 9.6% from a 52-week high, the equal weight version (RSPD) is down less than 3%. Furthermore, whereas XLY looks like a falling knife, RSPD has just been bouncing sideways along the 50-DMA. The latest lows for RSPD came right at the uptrend line off of last summer’s lows. So all together, while the weakness in the Consumer Discretionary sector may cause some alarms to go off as a sign of stress for the consumer, the current situation is more looking like a lesson in index weighting methodologies and mega-cap volatility.

Bespoke’s Morning Lineup – 3/3/25 – In Like A…

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We so often look so long and so regretfully upon the closed door, that we do not see the ones which open for us.” – Alexander Graham Bell

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Well, at least it’s March. Anyone with a net long position in the stock market was happy to see February end. Although the S&P 500 finished the month down just 1.42%, the Nasdaq was hit with a decline of just under 4%, and nearly all of it came last week as the index declined 3.5%. Remember, it was only seven trading days ago that the S&P 500 closed at a record high!

This morning, equities are looking to build on last Friday’s gains as investors await the release of the February ISM Manufacturing report. In Europe, the STOXX 600 kicked off the week with gains of close to 1%, driven by a 2%+ rally in Germany. Manufacturing PMI readings for the region generally came in better than expected, but the rally in Germany has also been driven by a 10%+ rally in defense contractor Rheinmetall based on expectations that the EU will increase military spending to support Ukraine.

Getting back to last week’s trading, it was mostly positive at the sector level. As shown in the snapshot below, just four out of eleven sectors finished the week in the red. Technology (XLK) was the big loser, falling close to 4%, along with Utilities (XLU), which fell 1.3%. The two other sectors to finish lower were Communication Services (XLC) and Consumer Discretionary (XLY), which each shed around 1%. The losses in these two sectors were driven by mega caps like Tesla (TSLA) and Amazon.com (AMZN) in the Consumer Discretionary sector and Alphabet (GOOGL) and Meta Platforms (META) in the Communication Services sector. Besides these four sectors, most others were up at least 1%, including Financials (XLF) and Real Estate (XLRE), which gained over 2% each.

Relative to their short-term trading ranges, nine out of eleven sectors remain above their 50-day moving averages (DMA), but then there’s Consumer Discretionary and Technology, which both remain at oversold levels.

Get Invested: “Be Greedy When Others Are Fearful”

Our “Get Invested” series is a simple yet powerful resource designed to help anyone understand why investing in stocks for the long term is one of the best financial decisions they can make. The slide below from our Get Invested piece is titled “Be Greedy When Others Are Fearful.”

One of Warren Buffett’s most famous quotes is to “be greedy when others are fearful.” Unfortunately, many anxious investors can’t stomach losses in the stock market, causing them to go to “all cash” at exactly the wrong times. Take large declines, for example. Since WW2, the S&P 500 has fallen more than 15% in nine different quarters. Following every single instance, the index was higher a year later with an average one-year gain of 25.1%. Similarly, the S&P 500 has had two-quarter drops of 20%+ just eight times, and over the next year, the index was up by at least 17% with gains every single time.

If you have any questions about our Get Invested resource, please email us or give us a call at 914-315-1248. You can view the full piece by becoming a Bespoke client.

Click here to learn more about Bespoke’s wealth management services.

Brunch Reads – 3/2/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Oh, the Places You’ll Go: On March 2, 1904, Theodor Seuss Geisel, better known as Dr. Seuss, was born. His impact on generations of readers cannot be overstated. Books like The Cat in the Hat and Green Eggs and Ham introduced millions of children to reading through simple vocabulary, rhythmic patterns, and engaging illustrations. Beyond literacy, Dr. Seuss infused his stories with profound social and moral messages. The Lorax warned about environmental destruction long before it was a widespread concern, while Horton Hears a Who! told a story of compassion and the importance of standing up for others. Dr. Seuss’s influence extends beyond the pages of his books. His legacy continues through initiatives like Read Across America Day, which is celebrated annually on his birthday and promotes early childhood literacy. His stories have been adapted into films, TV specials, and stage productions.

A& & Technology

AI cracks superbug problem in two days that took scientists years (BBC)

An AI tool from Google just cracked a microbiology mystery in 48 hours, a problem that took human scientists a decade to solve. Given only a short prompt, the AI independently reached the same conclusion about how superbugs spread, even though the research hadn’t been published anywhere. It confirmed the hypothesis and even suggested four additional ideas, one of which the research team is now pursuing, leading Professor José R. Penadés to call it a game-changer for science. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

Get Invested: Ignore the Noise

Our “Get Invested” series is a simple yet powerful resource designed to help anyone understand why investing in stocks for the long term is one of the best financial decisions they can make. The slide below from our Get Invested piece is titled “Ignore the Noise.”

It’s hard to avoid monitoring the day-to-day action of the market when your hard-earned money is at stake, but for money that’s invested for the long-term, it’s best to try and ignore the noise.

The left chart below shows daily closing prices for the S&P 500 since the start of 2023. The right chart shows the S&P 500’s average daily closing price over the prior 200 trading days over the same time frame. Ignoring the daily ups and downs of the market and focusing on the longer-term trend is a helpful way to reduce unforced anxiety and potential disruptions to a buy and hold strategy.

If you have any questions about our Get Invested resource, please email us or give us a call at 914-315-1248. You can view the full piece by becoming a Bespoke client.

Click here to learn more about Bespoke’s wealth management services.

The Bespoke Report – 2/28/25 – Uncertainty Reigns

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. In this week’s report, we look at the rising tide of uncertainty reported by factories and consumers, the outlook for growth in the rest of the first quarter, the message companies are sending in earnings this season, recent cross-asset price trends, and much more! Don’t miss it.

When the Weekend Was a Good Thing

Through yesterday’s close, the S&P 500’s average daily performance during the second Trump administration has been a decline of 0.8%. The magnitude of the declines hasn’t been spread out evenly across each of those days. The chart below shows the S&P 500’s daily performance on every trading day since the inauguration, and we have also highlighted Mondays and Fridays in red. The days surrounding the weekend have been notably weak. Of the nine Friday and Monday sessions since 1/21, the S&P 500 has traded lower eight times for a median decline of 0.5%. These are some pretty weak numbers, but in the early days of this administration, we have seen no shortage of Friday afternoon and weekend headlines that the market has been forced to adjust to.

It’s still extremely early in this administration, so the extreme weakness of the market on Fridays and Mondays could easily shift, but we found it interesting how much these numbers differ from average weekday performance under President Biden. During his four years in office, Friday and Monday were easily the best days of the trading week, with average gains of 9.8 bps and 8.5 bps, respectively. Just like in life, for the markets, no news is sometimes good news, and unlike the first few weeks of the second Trump Administration, weekends during the Biden Administration tended ot be quiet from Friday afternoons through early Monday.

Bespoke’s Morning Lineup – 2/28/25 – Not Another Weekend!

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Everybody deserves a fresh start every once in a while.” – Bugsy Siegel

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s been a rough few days for the equity market since last Wednesday’s record closing high, but at least futures are trading modestly higher. Maybe the market is getting a fresh start! After these last six trading days, if positive futures still make you optimistic, what market have you been watching? On five of those six days, the S&P 500’s intraday high came in the first ten minutes of the trading day, and there has been a reliable pattern of afternoon selling the entire time. Just look at the chart below of the S&P 500 ETF (SPY); since last Wednesday’s record high, there have been six straight days where SPY finished the day below where it opened. Is it too much to ask for just one day when Lucy doesn’t pull the football away from Charlie Brown?

We just got a bunch of economic data hitting the tape, and it was mixed. Personal Income increased more than expected, but Personal Spending was weaker than expected. More importantly, though, PCE data, which the market was most focused on, came in right in line with expectations. The immediate reaction in equity futures has been positive, but we’ll see how that plays out as the market digests the numbers.

While you may be thinking TGIF, that hasn’t been the case in the early days of the second Trump Administration. The chart below shows the S&P 500’s performance on every trading day since President Trump was inaugurated, with Fridays and Mondays highlighted in red. Of the nine trading sessions that have occurred on Friday or Monday during this time, the S&P 500 has only been up once (2/10, +0.67%), and the median performance has been a decline of 0.50%.