Mar 4, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In wartime, truth is so precious that she should always be attended by a bodyguard of lies.” – Winston Churchill

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s been an up-and-down overnight session for US equity indices, and as we type this now, both the S&P 500 and Nasdaq futures are basically flat with moves of less than 10 bps to the upside. Treasury yields are slightly higher, crude oil is flat, and gold is up less than 1%. Pretty quiet day, huh?

Iran will have the potential to continue dominating market action for the day, but don’t forget about the ADP Employment report, ISM Services, and then Broadcom (AVGO) earnings after the close. Earlier this week, the ISM Manufacturing report had the highest Prices Paid reading since 2022, so that will be a key metric to watch in today’s report for the services sector.

The bottom fell out of Asian stocks overnight as the Nikkei fell 3.6%, and every other major benchmark index in the region fell at least 1%. The real damage, though, was in South Korea, where the KOSPI fell over 12% for its worst day on record. There have been major market panics over the last 40 to 50 years, but none of them featured a day when South Korean stocks had a worse one-day decline. Fallout from the war in Iran was the primary driver of the declines, but Chinese PMI data for the Manufacturing and Services sectors also came in weaker than expected.

European stocks are following a different path than Asia, as the STOXX 600 is up over 1%, and the only major country up by less than 1% is the UK. Spanish stocks have managed a gain of 1.4% despite threats from the Trump Administration to cut off trade with the country. Service sector PMIs for the Eurozone and individual countries were basically in line with or slightly better than expected.

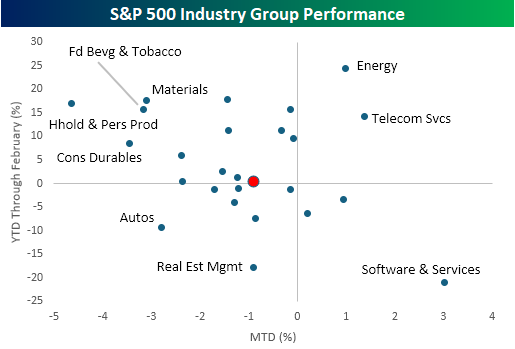

After two full sessions of trading since the war in Iran started, the overall market reaction has been subdued, but there have been some larger moves among individual industry groups. While the S&P 500 is down less than 1%, 16 out of 25 industry groups are up or down more than 1%.

This morning, we wanted to focus on some of the extremes. Starting with the winners that have continued winning, the only two groups that were up YTD heading into the conflict and have continued higher since are Energy and Telecom Services. Along with those two groups, the only others that are up this week are Software & Services (3.0%), which took the opposite path of South Korea by going from worst to first, Commercial Services (0.9%), and Banks (0.2%).

To the downside, some of the worst-performing sectors this week were some of the best YTD performers heading into the conflict. Household & Personal Products, Food Beverages & Tobacco, and Materials were all up over 15% YTD heading into the week, and they’re all down over 3% this week. As painful as the declines may feel this week, they’re coming off of a high base. It’s also worth noting that while Software stocks have bounced, Autos and Real Estate Management- the second and third worst performing groups YTD heading into the conflict have continued lower.

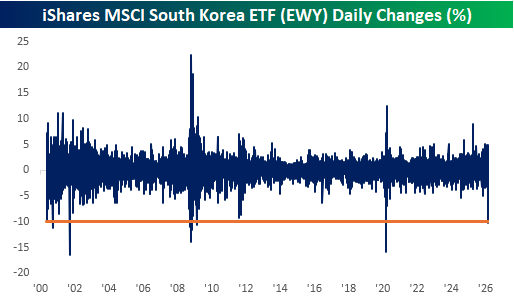

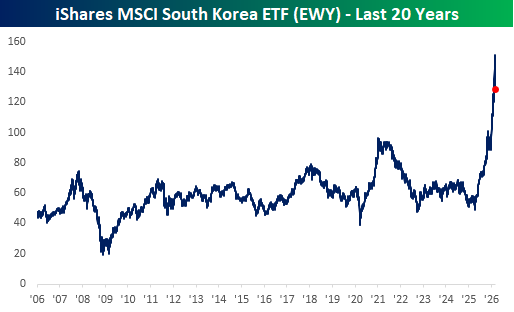

Outside of the US, we’ve also seen some major reversals this week. In yesterday’s Chart of the Day, we noted the outperformance of US stocks relative to the rest of the world. Nowhere has this reversal been more evident than in the performance of South Korean stocks. On Monday, the iShares MSCI South Korea ETF (EWY) fell more than 10% for its largest one-day decline since the Covid crash (South Korea’s KOSPI last night had its worst day on record). As shown in the chart below, declines of this magnitude have only been seen during periods of major crises like Covid, the Financial Crisis, and the dotcom bust.

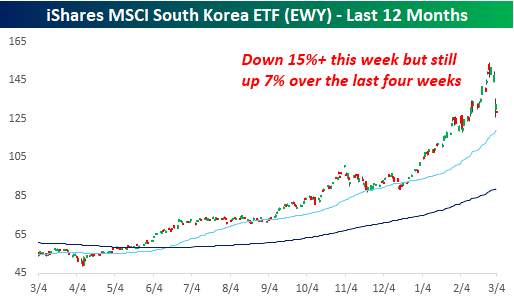

Besides Monday’s decline, EWY continued lower yesterday and is indicated down by another 3% this morning. That takes its decline this week to over 15%, and as sharp as that may sound, the ETF is still up over 7% in the last four weeks. It’s been a rocky few sessions, but if someone told you four weeks ago that you’d have a 7% gain in a month despite a major war in the Middle East, who wouldn’t have signed up for that?

From a longer-term perspective, EWY still looks extremely extended relative to its historical range. After breaking out above its 2021 highs late last year, it is still up over 32% YTD, making it the top-performing major country ETF, so it’s hardly oversold.

Mar 3, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The hardest hits are yet to come from the U.S. military,” – Marco Rubio, US Secretary of State

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are off their overnight lows, but the optimism from the close yesterday evaporated quickly. The S&P 500 is indicated to gap down 1.4% at the open, while the Nasdaq will open down closer to 2%. These are even larger downside moves than at yesterday’s open! Treasury yields continue to move higher as the 10-year yield is back to 4.10%, and oil is on pace for its second day in a row of 6%+ gains. Unlike yesterday, though, there’s been no bid for gold or other precious metals as they’re all sharply lower. Bitcoin is also down 3%.

In Asia, markets are lower again this morning as the Nikkei fell 3.1%, China was down over 1%, and South Korea, after being closed on Monday, tanked 7.2%. It’s the same sea of red in Europe as well. The STOXX 600 is already down 3% on the day, on some of the most negative breadth we have seen in quite some time (24-1 to the downside and every group is down over 1.55%). As bad as US futures look this morning, the losses are a scratch relative to the gash in international markets. From an energy perspective, the US is much more insulated than the rest of the world is to Middle Eastern oil and gas. Therefore, the longer the conflict drags on, the more US assets should catch a bid, at least on a relative basis.

After an impressive turnaround from the morning lows yesterday, the ink was barely dry on the closing prices for the day when US Secretary of State Marco Rubio briefed the press with a statement that included the quote above. That, along with Iranian drone attacks on the US embassy in Riyadh, comments from the IRGC that the Strait of Hormuz was “closed” and any ships that attempted to traverse through it would be set ablaze, and a directive from the State Department for all personnel in Bahrain, Iraq, and Jordan to evacuate those respective countries, has caused a sharp reversal in sentiment as to the scope and duration of the current war situation in the Middle East.

At points yesterday, there was growing confidence that the operation against Iran would be quick, but this morning, we’ve seen some warnings from analysts that it already looks as though the US is getting involved in a prolonged quagmire (even though it hasn’t even been four days to this point). The next several days promise to feature multiple swings in sentiment as the situation unfolds, but remember this: no one knows exactly how this will all play out. The comments from Rubio above and the ones from the IGRC regarding the Strait of Hormuz sound dire, but what else do you expect them to say in the middle of a war?

We’ve only had one day of trading since the war began, and already the market action has been a roller-coaster. After gapping down more than 1% at the open yesterday, the SPDR S&P 500 ETF (SPY) bounced throughout the trading day to finish marginally higher, in what was only the 60th time since its launch 33 years ago that the ETF gapped down at least 1% and finished the day higher. With futures trading sharply lower again this morning, SPY is on pace to gap down more than 1% again today, and of those 59 prior reversals, SPY only gapped down more than 1% the following session six other times

This type of volatility only occurs under one condition – massive uncertainty. As shown by the red dots in the chart, the prior back-and-forth reversals were in December 2002, coming out of the dotcom bust, late 2008 following the collapse of Lehman, January 2022 when inflation started to spike, and last April during the tariff-tantrum. What’s somewhat unique about the current period, however, is the level of the VIX. In the six prior occurrences, the average level of the VIX was 40, and it was never below 30. As of this morning, the VIX is trading just under 26. Also, while the S&P 500 remains close to 52-week highs, all of the others, except the one in January 2022, occurred closer to 52-week lows.

While these types of reversals have been rare for SPY, the Nasdaq 100 is inherently more volatile, so it shouldn’t come as a surprise that they have been more common in QQQ. Today’s reversal will be the 19th such reversal. As shown in the chart below, most of these reversals occurred during the dot-com bust, with 12 between the March 2000 peak and the October 2002 lows. As the Nasdaq has ‘matured’ since then, occurrences have been much less frequent, with three during the financial crisis, one in early 2019, another in January 2022, and most recently in April of last year.

Mar 2, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If what you have done yesterday still looks big to you, you haven’t done much today.” – Mikhail Gorbachev

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Markets are poised to open the week sharply lower following the start of the war in the Middle East. Both the S&P 500 and Nasdaq are indicated to open down by over 1%, crude oil is sharply higher, gold is surging, and even Bitcoin is higher.

Overnight in Asia, major averages were all lower except for China, which rallied 0.5%. European markets are also joining in on the weakness, with the STOXX 600 down 1.5% and Spain and Germany both down over 2%.

It’s tempting to look at the initial moves in the opening hours of trading and extrapolate them to a specific endpoint, but we’d stress that we’re still very early in this process. While a short conflict would likely be received positively by the market, the longer it drags on, and the higher energy prices stay, the more of an economic/market impact this will have.

Markets are mostly reacting just as you’d expect given the news of the weekend. Crude oil is sharply higher, stocks are down, and the dollar is up. The only asset class not following the playbook is the 10-year yield. US Treasuries are actually selling off modestly this morning, with the yield on the 10-year up about 3 bps to 3.98%. Higher yields will inevitably raise questions over the sell America trade, but two points are worth highlighting. First, on Friday, yields closed right near 52-week lows even as PPI came in higher than expected, so there was certainly some front-running of the attack on Iran heading into the weekend. Secondly, it’s not just US yields that are higher. Sovereign yields are also higher by similar amounts in Europe as well, so the move is more a reflection of concerns over inflationary impacts of the war.

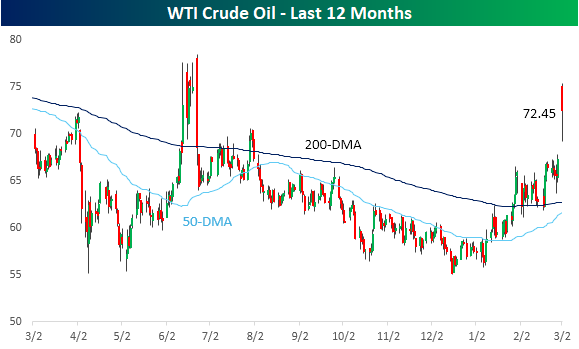

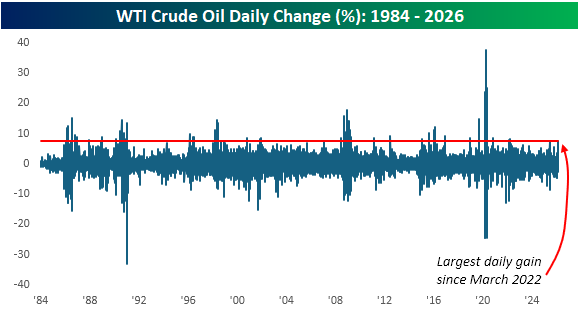

Crude oil has followed the playbook just as you would expect, though. If the pre-market gains hold through the end of the session, it will be the largest one-day rally in WTI crude oil since the early days of the Russia-Ukraine war in March 2022. While crude oil is off the highs from overnight, at over $72 per barrel, it’s right near its highest levels of the last year.

It’s been a large move, but today’s gain would only rank as the 80th largest one-day gain in crude oil since 1984. Given the enormity of the military action, an even larger move in crude oil wouldn’t have been a surprise.

Feb 27, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I wonder why progress looks so much like destruction.” – John Steinbeck

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be a guest on “Making Money with Charles Payne” today at 2 PM on Fox Business. Make sure to check it out!

Futures have been steadily losing steam all morning as the S&P 500 and Nasdaq both look to open down over 0.6%. Weakness has been focused on the usual suspects of software stocks, as Salesforce (CRM) drops 3% while Microsoft (MSFT) falls over 1%. A Disappointing earnings report from CoreWeave (CRWV) hasn’t helped either, as that stock is down over 10%. Nvidia (NVDA) is also adding to yesterday’s 5%+ decline with a drop of 1% in the pre-market.

With the weakness in equities, treasuries are rallying as the 10-year yield falls below 4% for the first time since before Thanksgiving. Oil prices are sharply higher with a gain of more than 3% heading into another weekend of uncertainty over whether the US will attack Iran. That uncertainty also has gold trading nearly 1% higher while other metals see even larger gains. Crypto, however, is down over 2% and back below $66K after trading above $69K two days ago.

Asian markets finished the week mixed but broadly higher for the week. South Korean stocks fell 1% but still gained 7.5% for the week and closed to 20% for February. Not bad for the shortest month of the year! Japan and China traded higher, adding to their gains for the week with Japan up 3.6% and China up 2.0%. Inflation data in Japan decelerated relative to January (1.8% y/y from 2.0%) but was higher than the 1.7% y/y consensus forecast. Japan’s economic minister took the glass-half-full view of the data and commented that inflation is slowing and expects real wages to turn positive in the coming months. In Europe, it’s been a modestly positive session in early trading with the STOXX 600 up 0.2%, putting it on pace for a 0.5% gain for the week. At the country level, markets are broadly higher on both the day and the week.

On the data front, January PPI just hit the tape and came in higher than expected for the second month in a row. Futures have dipped lower in reaction to the report, although the 10-year yield hasn’t moved much in reaction. The only other reports on the calendar between now and the weekend are the Chicago PMI at 9:45 and Construction Spending at 10 AM.

As mentioned above, with the 10-year yield below 4.0%, it is on pace for its first close below 4% since the day before Thanksgiving and the lowest close since late October. As shown in the chart below, if the current levels in the 10-year yield hold, today would be just the ninth time in the last 12 months that the yield closed below 4%. These levels come just over a month after yields were as high as 4.3%, as market fears over inflation outweighed any concerns over future employment losses due to AI. We also wouldn’t be surprised if, at some point in the coming weeks, the narrative shifts once again!

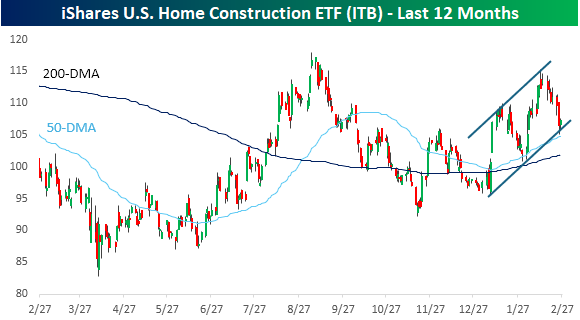

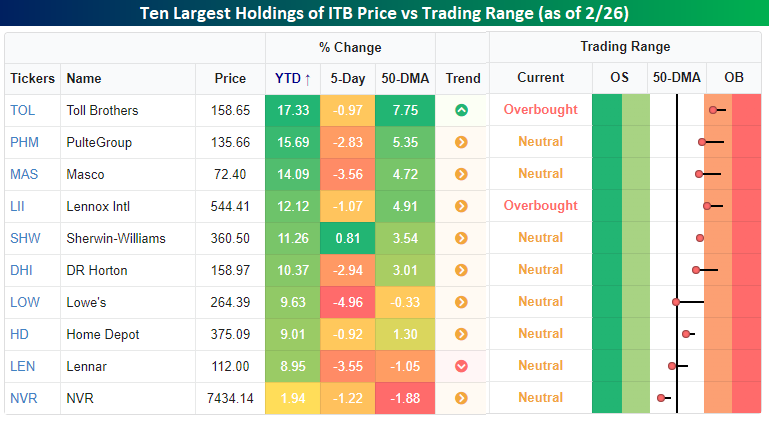

Prime beneficiaries of lower yields are the homebuilders, and up until this week, the group was performing very well, but on Wednesday, the iShares US Home Construction ETF (ITB) fell more than 3% following the President’s State of the Union (SOTU) speech. Usually, when a stock or sector falls after one of the President’s speeches, it’s because he said something combative about it. In this case, though, it was what the President didn’t say.

Despite being the longest SOTU speech of all time, the speech was noted for its lack of any meaningful comments regarding housing or increasing housing supply. In fact, the only real mention of housing was in protecting home prices, which can only be done by lowering demand or not meaningfully increasing supply.

While homebuilder stocks had their worst day in over six months the day after the President’s SOTU speech, ITB remains in a steady uptrend and bounced yesterday right at the bottom of that trend channel. If rates remain below 4%, a move back to the high end of that range wouldn’t be an unreasonable expectation.

It’s been a good year all around for homebuilders and housing-related stocks. Of the ten largest holdings in ITB, all but one are up at least 8% YTD, even after this week’s declines. Pure-play homebuilders have led the ETF’s gains, with Toll Brothers (TOL) and PulteGroup (PHM) both rallying more than 15% YTD.

Feb 26, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Bang! Zoom! To the moon, Alice!” – Jackie Gleason

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity futures have moved fractionally into positive territory off their overnight lows as shares of Nvidia (NVDA) turned positive with a gain of nearly 1%. The 10-year yield is down 1 bps to 4.04% while crude oil trades down 2% to $64 per barrel. Gold prices are also down by about 0.5%, while silver plunges nearly 5% and Bitcoin drops over 1% to just over $68K.

Asia was mostly positive overnight. The Nikkei finished higher by a modest 0.3%, and Hong Kong declined more than 1%. South Korean stocks, however, continued to surge as the KOSPI rallied 3.7%, taking its YTD gain to 49.7%! Nearly 50%! Japanese PM Takaichi nominated two dovish candidates for roles within the BoJ, and the yen is weakening as markets now price the odds of a rate hike in April down to just 50%. This comes even as Leading Indicators in Japan came in better than expected.

European stocks are positive again this morning, with the STOXX 600 up 0.2%, with France’s 0.9% gain leading the way higher. February Business and Consumer Confidence unexpectedly declined, although Confidence in Italy bounced.

In the US this morning, the only reports on the calendar are Jobless Claims at 8:30, followed by the KC Fed Manufacturing report at 11. At 10 AM Eastern, Fed Governor Bowman will also testify in front of a Senate panel.

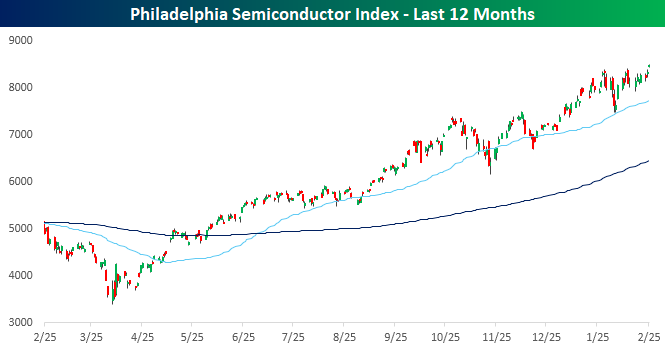

Jackie Gleason, best known as the hot-tempered bus driver Ralph Kramden from the 1950s sitcom The Honeymooners, would have turned 110 years old today. Ralph’s most iconic line from the show was “To the moon, Alice”, and that’s the way things seem to be going for semiconductor stocks. While Nvidia’s (NVDA) stock price, despite surging profits and revenues, has been rangebound for months now, the Philadelphia Semiconductor Index (SOX) hit another record high yesterday, taking its YTD gain to just under 20%.

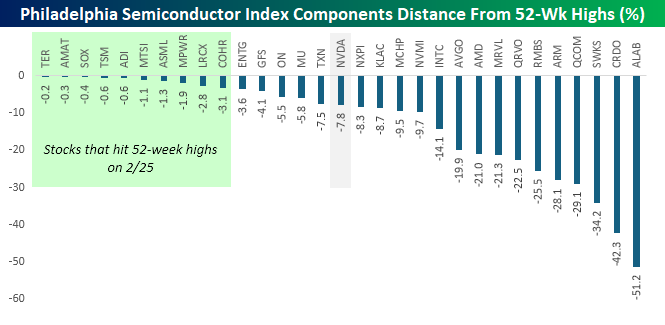

Along with the index itself, breadth in the sector has also been strong. Yesterday alone, nine of the index’s 30 components hit 52-week highs, even as NVDA closed nearly 8% below its respective high.

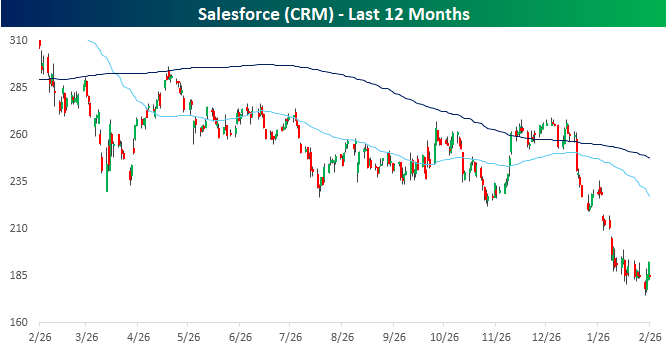

While semis have been strong, software stocks continue to try digging out from the AI-pocalypse. The latest setback for the sector was earnings from Salesforce (CRM) last night. CRM exceeded EPS forecasts on inline revenues. Guidance was mixed with the company raising Q1 EPS forecasts while keeping full-year forecasts in line with expectations. Despite a somewhat positive report at the surface, CRM is down more than 2% in the pre-market.

As software stocks have been cratering in recent weeks, investors have been asking where company managements are with respect to purchasing their stocks. If the declines were a major overreaction, as CRM CEO Benioff and others say, shouldn’t they be buying back stock hand over fist?

CRM addressed that last night when the company announced a $50 bln buyback. CRM’s market cap is $180 billion, so $50 billion represents more than a quarter of the company’s entire market cap. Ideally, investors would like to see company executives putting their own actual money where their mouths are, but a $50 billion stock buyback is a step in the right direction.

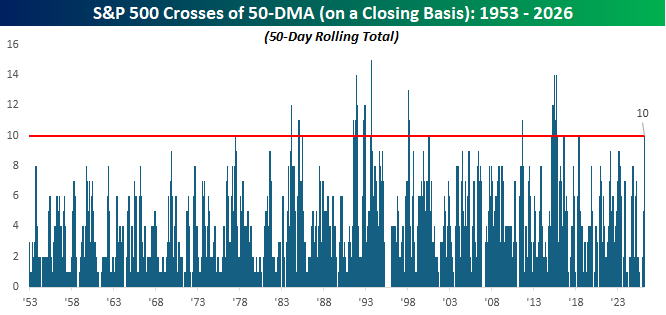

Semis and software are two of the market’s largest sectors, and each one moving in the opposite direction has contributed to the ping pong action at the overall index level. As we noted on X yesterday, the S&P 500 has now crossed its 50-day moving average on a closing basis ten times in the last 50 trading days. That’s the longest streak since March 2018 and one of only a handful of periods with that many crosses in such a short period of time. As we’ve all said to someone close to us multiple times, make up your mind already!

Feb 25, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To devastate is easier and more spectacular than to create.” – Anthony Burgess

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity markets are looking to build on yesterday’s turnaround Tuesday gains and are on pace to erase much of Monday’s losses, but whether these gains stick through the end of the week could depend on Nvidia’s (NVDA) report after the close. It’s widely assumed that the results will be strong, but will they be strong enough? And ff they’re too strong, will that also be interpreted as further future disruption in the software space?

Crude oil is higher this morning, trading just above $66 per barrel, even as Reuters reports that OPEC+ is considering a 137K barrel increase to daily production. Gold is also fractionally higher, back above $5,200 per ounce as silver surges 4% and platinum spikes 8%. Even bitcoin, yes bitcoin, is higher by more than 2%.

Asian stocks finished the day higher across the board, with the Nikkei up over 2% and South Korea up just under 2%. Chinese stocks also traded higher even as the Ministry of Commerce threatened to impose countertrade measures in response to the new tariff policies of the Trump Administration.

In Europe, stocks are also broadly higher but at a more restrained pace. The STOXX 600 is up 0.5%, led higher by 1% gains in Italy and the UK. Eurozone GDP fell more than expected (-0.6% vs -0.5% forecast) and German GDP was in line with expectations, growing 0.3% q/q.

Besides some important earnings reports after the close from NVDA and Salesforce (CRM), it’s a quiet day for data, but we will hear from many Fed speakers, including Barkin, Schmid, and Musalem.

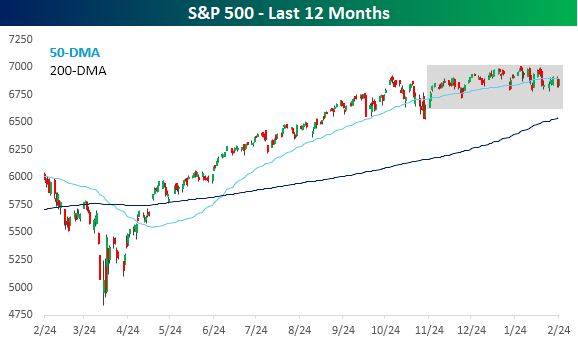

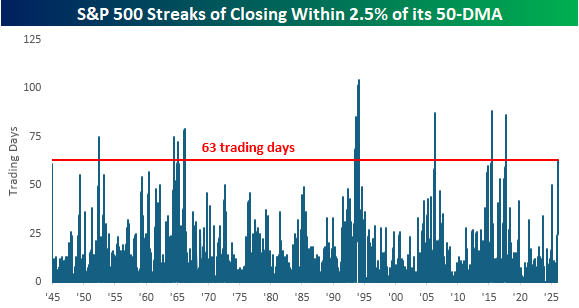

Given the ongoing weakness we have seen in certain areas of the market, which investors now think will be devastated by AI, it’s still hard to believe how range-bound the S&P 500 has been. Yesterday, the S&P 500 closed less than 0.1% below its 50-day moving average. You can’t get much closer than that! And it wasn’t just yesterday. The rangebound morass has been going on for months now, as there hasn’t been a day in the last three months where the S&P 500 closed more than 2.5% above or below its 50-day moving average.

Periods where the S&P 500 has been so closely anchored to its 50-DMA haven’t been all that common throughout history. The chart below shows streaks when the S&P 500 closed within 2.5% of its 50-DMA (above or below), and the current streak, which reached three months (63 trading days) yesterday, is the longest since the first Trump administration in August 2017. Since WWII, there haven’t been many other extended periods where price was consistently so close to its 50-DMA.

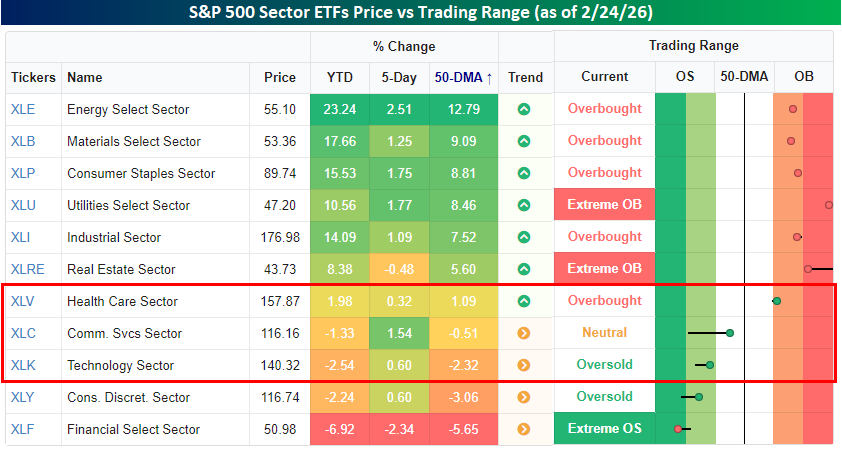

What makes the current streak even more incredible is that most sectors haven’t been showing the same pattern. As of yesterday’s close, just three of eleven S&P 500 sector ETFs – Health Care (XLV), Communication Services (XLC), and Technology (XLK) – closed within 2.5% of their 50-DMAs, and most sectors aren’t even close. Six are more than 5% above their 50-DMAs, and another is more than 5% below its 50-DMA. Like a sleeping volcano, the S&P 500 looks placid from above, but underground, the molten lava bubbles.