May 23, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you want to keep your memories, you first have to live them.”– Bob Dylan

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Can you feel it? It may not feel like it in many parts of the country, but the unofficial start to summer kicks off in less than eight hours as the three-day Memorial Day weekend kicks off. There’s still one more trading day left in the week, though, and futures have been moving lower this morning and just recently took two legs lower. The first followed a Truth Social post from the President saying, “I have long ago informed Tim Cook of Apple that I expect their iPhone’s that will be sold in the United States of America will be manufactured and built in the United States, not India, or anyplace else. If that is not the case, a tariff of at least 25% must be paid by Apple to the U.S.” In response to that post, shares of Apple (AAPL) plunged over 3% and took the Nasdaq down with it.

Shortly after that, the President shifted his attention to the EU, saying, “Our discussions with them are going nowhere! Therefore, I am recommending a straight 50% Tariff on the European Union, starting on June 1, 2025.” As you can imagine, that didn’t help matters, and futures took another leg lower, but stocks in Europe are down even more, with the STOXX 600 down 2%. Interestingly, while the S&P 500 was firmly higher, heading into the final half hour of trading yesterday, it fell sharply into the close, finishing the day slightly lower. Did somebody have wind of these Truth Social posts beforehand? We may have a three-day weekend coming up, but the President can post at any time…

This morning’s earnings and economic calendar are on the light side with little in the way of earnings reports, and the only economic report on the calendar is New Home Sales at 10 AM.

The period covering Memorial Day through Labor Day overlaps with the “Sell in May and go away” period, but the S&P 500’s performance during the unofficial summer period has generally been positive, most notably during years when the S&P 500 was already up YTD. The chart below shows the performance of the S&P 500 from the Friday before Memorial Day through the Friday before Labor Day over the last 50 years. The S&P 500’s median performance during this period has been a gain of 3.7%, with positive returns 72% of the time. In years when the S&P 500 was up YTD heading into the unofficial summer period, the S&P 500’s median performance was a gain of 4.3%, with positive returns 74% of the time. However, in the 15 years when the S&P 500 was down YTD, the median performance was just 1.4%, with gains 67% of the time.

Looking at the week after Memorial Day, the chart below shows the performance of the S&P 500 from the Friday before Memorial Day to the Friday after over the last 50 years. Overall, the S&P 500’s median performance has been a gain of 0.6% with positive returns 64% of the time, and there’s very little difference in performance depending on whether the S&P 500 was up or down YTD heading into the holiday weekend.

May 22, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The president wants lower rates… He and I are focused on the 10-year Treasury and what is the yield of that.” – Scott Bessent

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity futures have been weakening all morning as yields have risen. Oil prices are lower as OPEC+ mulls another production increase, and Bitcoin is above $111K. The House passed its tax bill, and we’re approaching a slew of economic data about to be released after what has to this point been a quiet week for data.

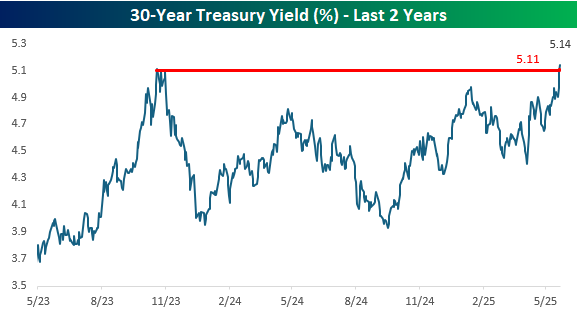

The President and Treasury Secretary may want and be focused on the level of yields, but that’s not what they’re getting. While the 10-year US Treasury yield still hasn’t reached a new high for the year, the 30-year yield broke out above resistance yesterday, trading as high as 5.11% and then adding to those gains this morning and reaching a yield of 5.14%. From a technical perspective, the move higher in yield looks like a textbook breakout, and if that pattern played out, it would suggest higher rates ahead.

From a longer-term perspective, 5.11% was an important level for the 30-year yield. Looking at a two-year chart, it represents the high from Q4 2023, and if current levels of 5.14% hold, we could be in for a new leg higher in yields, which would spell more headaches for equities.

May 21, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Zeroing in on the best sectors or the best regions of the world is great, but zeroing in on the very best individual stocks is the key to making truly impressive profits.” – Lou Navellier

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Below is a link to our recent appearance on Lou Navellier’s show — Market Buzz — where we had a nice conversation about stocks! Please watch when you have a chance.

It’s not a good day to be a bull this morning as S&P 500 futures are down about 0.50%. It was a steady move lower right up until around about 6:30 AM Eastern when there was some stabilization and even a modest bounce.

There’s not much in the way of catalysts driving the market weakness, but yields are higher as the 30-year treasury ticks up above 5% while the 10-year yield jumps back above 4.5%. As Republicans look to pass the Big Beautiful Bill, there has been some headway made in the SALT Cap negotiations with Speaker Johnson confirming that the cap will be lifted to $40,000, and the deficit implications of that agreement could be helping to drive the move higher in yields.

The economic calendar is light once again today, and in terms of earnings reports, since the close yesterday, some of the more notable reports have come from Palo Alto (PANW), Toll Brothers (TOL), Lowe’s (LOW), and Target (TGT).

After missing EPS forecasts yesterday, Home Depot (HD) broke a streak of 19 straight quarters of exceeding bottom-line forecasts, which was the longest streak of EPS beats for the stock since at least 2001. This morning, HD’s largest competitor, Lowe’s (LOW), reported earnings, and unlike HD, it was able to beat EPS forecast and extended its record streak of EPS beats to 24. That’s six years!

The chart below shows historical streaks of EPS beats for both stocks, and while they’re in identical industries, their streaks of earnings beats haven’t followed the same trajectories. While the current period has seen a longer streak of EPS beats for LOW, over the last 20+ years, HD has done a better job of managing expectations and then beating them, as evidenced by the fact that it has seen several more extended streaks of EPS beats than LOW.

Just because both stocks have done a good job of beating EPS forecasts over the last five years, doesn’t mean it has translated into their stock prices. While both stocks are higher now than they were five years ago, they have both been dead money for the last 3+ years. Coming out of the COVID lows, both stocks rallied sharply through late 2021, but then as the Fed started talking about rate hikes, they cratered and have been trading sideways ever since. While LOW’s managed to make a new high late last year, it has pulled back since then and is back below its 2021 high.

The culprit behind the relative weakness in both stocks has been rising interest rates. The chart below shows the 10-year yield since the start of 2020, and the peak in both stocks came right before the 10-year yield started to surge in early 2022. While yields have essentially been sideways for the last 2+ years, until yields start to move lower, it will be hard for both home-improvement stocks to move higher. Think of it as a scale. For one side to go up, the other has to go down.

May 20, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Every man who says frankly and fully what he thinks is so far doing a public service.” – John Stuart Mill

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Is it summer already? Summer doesn’t officially start for another month, and the unofficial start isn’t until this weekend, but we’re in the doldrums regarding futures. Depending on the index, futures are slightly higher or lower, but they’re all off the overnight lows. There’s no economic data on the calendar this morning, but several Fed speakers are scheduled to speak throughout the day.

The only major earnings report of the day is Home Depot (HD). The company reported weaker-than-expected EPS and broke a streak of 19 straight quarters of EPS beats. Revenues were higher than expected, though, and the company reiterated full-year guidance and said they do not plan to raise prices due to tariffs. In response, the stock is up about 2%.

Like the S&P 500, the Nasdaq 100 also comes into today riding a six-day winning streak. After yesterday’s gain, the index is currently within 4% of its all-time high, meaning that all it would take is a rally almost as strong as the last six days to get us there. Given the magnitude of the gain over the last six days, though, it’s unlikely we’ll see a move like that in the next several days, not only because we’re now sitting at overbought levels in the short term but also because the index is bumping up against potential resistance.

May 19, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs.” – Moody’s, 5/16/25

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After being the lone holdout with a AAA credit rating on the sovereign debt of the US, on Friday evening, Moody’s joined Standard and Poor’s and Fitch in downgrading US debt. As you might expect, equity futures are lower and interest rates are higher in response to the news. As Moody’s noted in its statement, the downgrade is the result of ‘successive US administrations’, and the buildup of debt in the US has been a long-running issue. The news, therefore, is surprising to no one, but it still reinforces the problem and brings it to the forefront.

The chart below shows the 10-year US Treasury yield dating back to 2010, with each AAA downgrade notated on the chart. In the case of both the S&P and Fitch downgrades, the actions did little to change the trend in interest rates. When S&P downgraded US debt in 2011, yields were already falling and continued to decline, whereas the Fitch downgrade in 2023 came in the middle of a period when rates were rising. So, while each action garnered headlines, the ratings agencies didn’t tell us anything the market didn’t already know.

May 16, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The most important decision you make is to be in a good mood.” – Voltaire

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The biggest individual stock story of the week and probably of the last year is UnitedHealth Group (UNH). The stock is down 28% this week alone and has been more than cut in half in just a month! It’s hard to remember what was once considered a blue-chip stock falling out of favor so fast.

UNH is also a member (for now) of the Dow Jones Industrial Average (DJIA), and because that index is price-weighted, the stock used to be one of the index’s largest components. That has made its fall from grace even that much more impactful on the index. The chart below shows the Dow’s performance over the last six months, and we have also created a theoretical index price that doesn’t include UNH (green line).

While the DJIA is still 6% below its recent high, without UNH, it would be just 2% from its high, and the spread between the current Dow and the Dow Ex UNH is 4.6% percentage points! From a technical perspective, the Dow would look much better without UNH. Through yesterday’s close, the Dow was still below potential resistance at its late-March/pre-Liberation Day high, but backing out UNH, it cleared those levels earlier this week. Taking out the index’s weakest component involves cherry-picking, but we think it provides some good perspective.