Jul 8, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If your only goal is to become rich, you will never achieve it.” – John D. Rockefeller

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Subdued is the tone once again this morning as equity futures are little changed on either side of the unchanged line. Nasdaq futures are showing the biggest move with a gain of 0.25%. Crude oil is fractionally lower, just below $68 per barrel, while the 10-year yield is up 2 bp,s taking the yield back above 4.4%. Gold is slightly lower, while Bitcoin and Ethereum both are trading up about 1%.

In Asia overnight, most major indices were little changed, except for China, which was up 0.70% while Hong Kong’s Hang Seng was up just over 1%. The modest gains came even as President Trump sent letters to many countries in the region, including Japan and South Korea, informing them that their exports to the US would face tariffs of at least 25%.

European stocks are little changed in the early going this morning, with the STOXX 600 up 0.10% while Germany and the UK are up fractionally, while France is lower. The EU was one region of the world not to receive a letter on tariffs, and that has raised hopes that a deal with the bloc could be near. Reports this morning suggest that the base rate will be 10% with some exceptions for aircraft and parts, medical equipment, and spirits.

Today in the US, it’s another quiet day on the calendar. NFIB Small Business Optimism came in right in line with expectations at 98.6, which was down very slightly from last month’s reading of 98.8. The only other report on the calendar is the New York Fed’s Survey of Consumer Expectations, where 1-year inflation expectations are expected to come in at 3.2%.

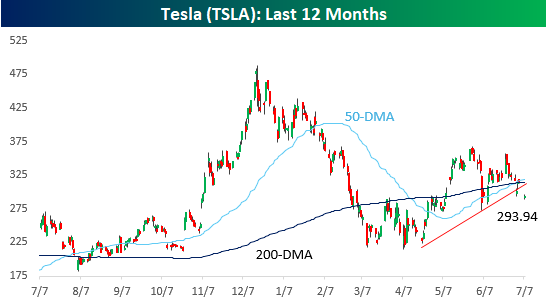

With Elon Musk announcing the creation of the America Party over the weekend and the potential of a third party to hurt Republican majorities in the mid-term elections, investors headed into the new week with concerns that potential retribution from President Trump would hurt Tesla’s business. In response, the stock opened down over 6% yesterday and basically stayed there, finishing the day with a decline of nearly 7%.

Yesterday’s decline broke TSLA’s uptrend off the April lows, and that came after making a lower high in late June. All this came after the stock made a golden cross (50-day moving average cross above the 200-day moving average as both are rising) last week, which technicians consider a positive technical formation. Fitting for a stock like TSLA, the stock’s trading pattern has been sending mixed signals.

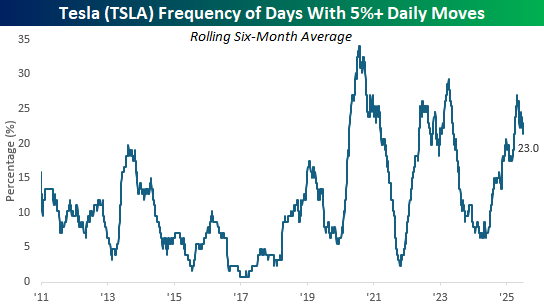

Normally, as companies become larger in terms of market cap, their share prices become less volatile, but that’s not the case with TSLA. Yesterday was the 29th daily gain or loss of 5%+ in TSLA over the last six months, which works out to 23% of all trading days. While the company went public in 2010, it wasn’t until 2020 that TSLA routinely started to see 5%+ daily moves on 20% or more of trading days over a rolling six-month period.

Jul 7, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“History is a guide to navigation in perilous times. History is who we are and why we are the way we are.” – David McCullough

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Investors are being eased back into the market this morning, with futures showing modest losses after a more significant decline overnight. The market may be open, but with no economic or earnings reports on the calendar, things are relatively quiet to kick off the new week. That’s generally the case for the rest of the week too, with very few reports on the calendar in the next four trading days. That will leave plenty of time for investors to focus on trade, and Treasury Secretary Scott Bessent says to expect several announcements in the next two days, and for those that don’t make a deal by August 1st, tariffs on their exports to the US will go back to the levels announced on April 2nd

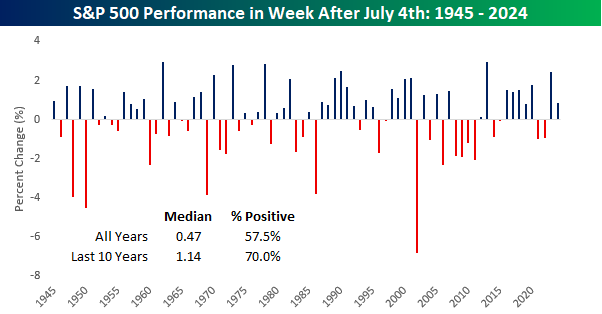

The long holiday weekend is over, and it’s time for investors to get back to business as Q2 earnings season is right around the corner, and the tariff situation is likely to become more concrete. One thing bulls have going for them heading into this week is the seasonal calendar. Since WWII, the S&P 500’s median performance during the week after the July 4th holiday week has been a gain of 0.47% with positive returns 57.5% of the time. More recently, performance has been even stronger with a median gain of 1.14% and positive returns 70% of the time.

Jul 3, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Governments are instituted among Men, deriving their just powers from the consent of the governed.” – Declaration of Independence

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Happy Fourth! In an outcome that most would not have predicted over the last several days and weeks, the House is likely to pass the Reconciliation Bill ahead of the July 4th holiday. Just yesterday, the odds of passage by that date were less than 50%, but the bill cleared a procedural vote overnight, and Polymarket now has the odds of passage at 91%. Whatever side of the aisle you position yourself, the ability of Speaker Johnson to pass legislation over the last six months with such a slim majority has been impressive.

That’s the biggest news event of the market day so far, but there’s a jam-packed economic calendar this morning that includes Jobless Claims, Non-Farm Payrolls, Factory Orders, and ISM Services. Besides being a busy day for data, it’s also a short session as the equity market closes at 1 PM ahead of the holiday, and the bond market closes at 2 PM.

Despite the big political news and the busy day of data ahead, futures are eerily quiet as the S&P 500, Nasdaq, and Dow are all indicated to open less than 0.10% higher. Crude oil is marginally lower, gold is unchanged, and treasury yields are lower. That last point is notable; for all the talk about how the Reconciliation Bill will be a budget buster and blow out the deficit, the 10-year yield has been going down as passage of the bill has become more likely. From a longer-term perspective, too, the 10-year yield is the same now as it was on Election Day.

Heading into the July 4th holiday, the fireworks of the second quarter have put eight of the eleven sectors into overbought territory. Over the last five sessions, every sector has traded higher, and Utilities (XLU) is the only sector ETF with a gain of less than 1%. Leading the way to the upside, Materials (XLB) have rallied over 5% pushing the sector into extreme overbought territory and a gain of nearly 9% YTD.

Jul 2, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Never do things others can do and will do, if there are things others cannot do or will not do.” – Amelia Earhart

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view yesterday’s CNBC interview from Closing Bell Overtime, click the image below.

US futures are little changed this morning as the S&P 500 looks to erase Tuesday’s modest losses. The major issue of the day will continue to be the Big Beautiful Bill and whether the House can pass the Senate’s version. A vote on that will be held either today or tomorrow, depending on when members can return to DC for the vote. Even when representatives return, passing the bill will be no easy task, as the slim Republican majority means Speaker Johnson can only afford a few no votes from his caucus. Betting against Johnson, however, hasn’t been a profitable strategy so far this year.

Overnight in Asia, equities were mixed with Japan falling just over 0.5% while Hong Kong rallied by a similar magnitude. The weakness in Japan stemmed from comments by President Trump, who expressed doubt that a deal with Japan would be reached by July 9th, in which case he could increase tariffs on the country to 35%.

The tone in Europe has been much more positive, with the STOXX 600 trading up about 0.5%. Unemployment in Europe ticked up to 6.3% which was higher than the 6.2% forecast, while Italy saw its jobless rate surge from 6.1% to 6.5%. That weakness should help to keep the ECB biased towards more easing.

In the US this morning, employment is also at the fore following this morning’s release of the ADP Employment report, which showed a 35K decline in payrolls in June, which was the first decline in over two years and well below the consensus forecast for growth of 95K. The ADP report has been consistently weaker than government data in recent months, and we’ll get the June Non-Farm Payrolls report tomorrow morning, but for now, this weakness lends to concerns over economic growth against a backdrop of uncertainty related to trade. With this report, you can practically hear President Trump’s fingers tapping out the next Truth Social post to Fed Chair Powell.

As we highlighted in the Chart of the Day, yesterday’s trading was all about rotation, where the best-performing areas of the market in Q2 lagged while the Q2 laggards outperformed. Another example of the rotation was in sector performance. The scatter chart below compares the performance of S&P 500 sectors during Q1 (x-axis) versus on 7/1 (y-axis). Here, you can see the rotation from the Q2 haves to the Q2 have-nots. The five worst-performing sectors of Q2 were the five best performers yesterday. Technology and Communication Services, easily the best-performing sectors of Q2, were the only two sectors to trade lower yesterday. As Andy Warhol once said, everyone gets their 15 minutes of fame, and yesterday it was the Q2 laggards’ chance to grab the spotlight.

Jul 1, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Every story needs an element of suspense – or it’s lousy.” – Sydney Pollack

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s a new month, a new quarter, and a new half this morning, and while investors would certainly be happy with a repeat in terms of the returns during the half, they would prefer to do without the volatility. This morning, futures are drifting moderately lower after two straight days of record closing highs. The quarter is also getting off to an active start with the June ISM Manufacturing report at 10:00 AM, along with the May reports on Construction Spending and JOLTS.

While these reports will likely impact the market upon their release, so far this morning, there aren’t many headlines driving the market in either direction. While futures are lower, the magnitude of the losses has been pretty modest so far. In Washington, the Senate is still trying to pass the GOP Reconciliation Bill. That ongoing process has led to a resurgence in the war of words between Elon Musk, who hates the bill and is threatening to primary conservatives who vote for it, and President Trump, who responded with comments that Elon owes all his success to government subsidies and said DOGE should look into them.

Besides another flare-up in the spat between President Trump and Elon Musk, Tesla (TSLA) has been in the news this week as the company marked the 15th anniversary of its IPO on Sunday. Based on its performance this year, the stock hasn’t exactly been celebrating the milestone. While well off its April lows, it’s still down over 20% on the year, and this morning, it’s on pace to open down by another 5% after the President ‘truthed’ that DOGE should look into all the subsidies that Musk’s various companies receive. If these pre-market losses hold, it will also put the stock below both its 50 and 200-day moving averages, just as it experiences a ‘golden cross’ where the 50-day moving average (DMA) crosses up through the 200-DMA as both are rising.

Even with its 20%+ decline YTD, TSLA still ranks as the third best performing stock out of the current Russell 1000 members with an eye-popping gain of 19,849% since its IPO. The only two stocks that have performed better are Nvidia (NVDA), which has tripled TSLA’s gain, and Axon Enterprise (AXON), which is up just under 22,000%. Trailing behind TSLA, Broadcom (AVGO), and Texas Pacific Land (TPL) round out the top five stocks that have all rallied more than 10,000%. That’s a 100-bagger!

While the last 15 years have been great for TSLA, the road for traditional auto OEMs hasn’t been much bumpier. While the S&P 500 has rallied nearly sevenfold over the last 15 years, Ford (F) and General Motors (GM) have essentially gone nowhere.

Jun 30, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It would be good to be a fake somebody rather than a real nobody.” – Mike Tyson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The market enthusiasm that took the S&P 500 to new highs last Friday has followed through to the new week as the S&P 500 looks to gap up about 0.5% at the open. Financials are leading this morning’s gains as the Fed announced last Friday that all of the banks passed the stress tests. Goldman Sachs (GS) is leading the way with gains of over 3%, but all of the other major banks and brokers are up around 1% or more.

The only economic indicators on the calendar this morning are the Chicago PMI at 9:45 and the Dallas Fed Manufacturing report at 10:30. Washington will be a focus for the market today as investors look to see if the Senate can pass a version of the GOP tax bill.

Last Friday’s close in the S&P 500 marked the first new all-time closing high for the S&P 500 in over four months and now fully puts the tariff-induced near-bear market in the rearview mirror. It also completes one of the more stunning market cycles where the S&P 500 experienced one of its sharpest sell-offs from an all-time high on record, followed by one of its swiftest rebounds.

With the new high, we can also resume the count of new all-time closing highs for the S&P 500, which for 2025 now totals four. That may sound like a meager number, but two months ago, the thought of new highs for the S&P 500 seemed like a pipe dream. With roughly 125 trading days left in the year, we’re unlikely to get anywhere near last year’s total of 57 record closing highs this year, but you have to start somewhere.