Mar 12, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Great things are not accomplished by those who yield to trends and fads and popular opinion.” – Jack Kerouac

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Money Movers yesterday to discuss the moves in the energy market and their impact on the equity market. To view the segment, click on the image below.

After a mixed session yesterday where the Nasdaq finished up 8 basis points (bps) while the S&P 500 fell 8 bps, US futures are firmly lower this morning, with the S&P 500 and Nasdaq both indicated to open down by about 35 bps. The primary culprit is crude oil, where prices are up over 5% and back above $90 as Iran stepped up attacks on tankers in the Persian Gulf. Energy Secretary Chris Wright was also just on CNBC and noted that the US is not yet ready to escort tankers through the Strait of Hormuz, but could be mobilized later this month. As long as the bottlenecks around the Strait continue, oil prices will remain elevated, raising the risk that the conflict makes its mark on the economy.

With crude oil prices rising, treasury yields are higher again as investors focus on the potential inflationary impacts. Gold prices are essentially flat, silver is up 2%, and Bitcoin is down fractionally but still above $70K.

Stocks were down across the board in Asia overnight, as the Nikkei was down 1.0%, while China’s Shanghai Composite was only down 0.1%, and the Kospi fell 0.5%. Relative to the last two weeks, it was a muted session! Given the spike in crude oil prices and the region’s dependence on energy imports, you could make the argument that it could have been worse.

In Europe, equities are also taking the overnight spike in crude oil prices in stride. The STOXX 600 is down just 0.4%, while Germany is fractionally higher. We’re also starting to see impacts of the conflict showing up in corporate results as UK travel firm On the Beach lowered guidance, citing a sharp slowdown in travel bookings for locations in the Eastern Mediterranean.

On the economic calendar this morning, we just had jobless claims, Building Permits, and Housing Starts at 8:30. Initial claims came in 2K lower than expected, while continuing claims were 1K higher, so from this perspective at least, the labor market remains very well behaved. With respect to the housing numbers, permits were lower than expected (1376K vs 1410K) while starts were much higher than expected (1487K vs 1341K), although much of the strength was due to multi-family units.

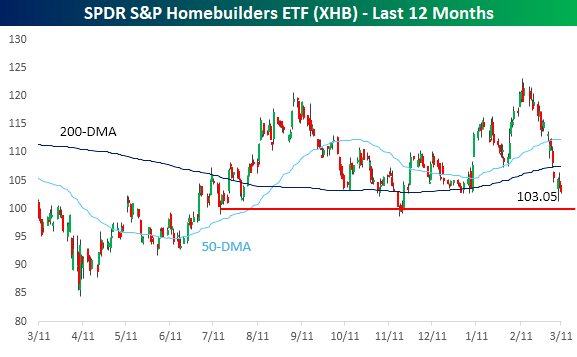

With treasury yields moving higher, it’s been a rough month for homebuilder stocks. The SPDR S&P Homebuilder ETF closed at $121.36 on 2/13, but has since declined more than 15% through yesterday’s close. Those highs in February were enough to push the group to 52-week highs, but the gains for 2026 quickly evaporated, and it’s now close to testing support at the $100 level.

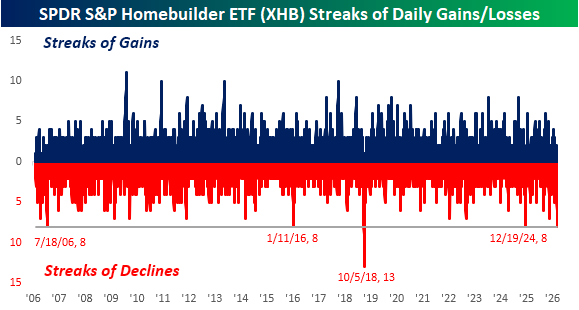

Part of that 15% decline since the February highs includes what is now an eight-day losing streak, which is tied for the longest losing streak in the ETF’s entire history. The last time there was a streak this long was over a year ago in late 2024, and the only longer streak was 13 days ending in October 2018.

Mar 11, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I attack ideas. I don’t attack people. Some very good people have some very bad ideas.” – Antonin Scalia

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be on CNBC at 11 AM Eastern to discuss markets and today’s CPI.

Futures were in a holding pattern ahead of today’s CPI, with the S&P 500 and Nasdaq both indicated to open down about 0.1% despite Oracle (ORCL) trading up over 10% in reaction to earnings. Treasury yields moved higher ahead of the report, with the 10-year yielding 4.17%, and crude oil was up over 4% to $87 per barrel. Gold and Bitcoin prices are down about 1%.

For Asian equities, the last several days have been something of an all-or-nothing trade where the major averages in the region are either all sharply higher or lower. Last night, there was more dispersion. While Japan and South Korea were both up 1.4%, Hong Kong was fractionally lower, and India declined 1.7%. In South Korea, exports for the first 10 days of March were up 55.6% y/y, with chip exports surging more than 175%. In Japan, PPI fell 0.1% versus expectations for an increase of 0.1%.

In Europe, the move was more uniform, and unfortunately for bulls, it was mostly lower. The STOXX 600 is down nearly 0.5%, with Germany leading the losses with a decline of nearly 1% as German CPI for February rose 0.2%, which was right in line with forecasts.

In the US, the only economic report on the calendar today is February CPI, which given the events of the last two weeks, has become much less pertinent to the market. While it may not be a major focus of the market this morning, CPI was right in line with expectations as headline increased 0.3% m/m and core increased 0.2%

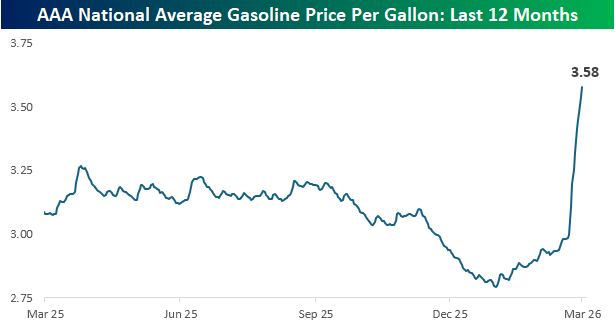

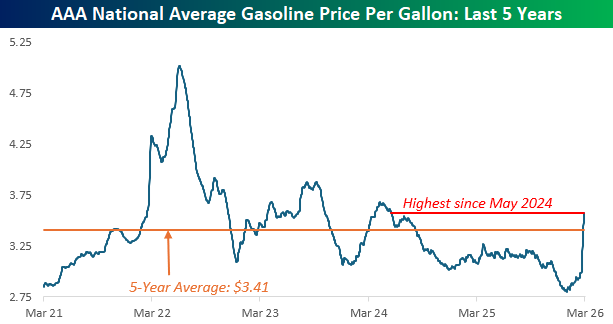

Through yesterday’s close, average prices at the pump have now surged to $3.58 per gallon, which represents a 20% increase this month alone. In the span of two months, prices have spiked from a 52-week and multi-year low to a 52-week high, easily surpassing the prior peak from last spring.

As shocking as the one-year chart looks, taking a longer-term look at crude oil prices shows a less dire picture. Current gasoline prices are now at the highest level since May 2024, but they’re still nearly 30% below the 5-year peak from June 2022, and less than 5% above the 5-year average. That doesn’t make it any easier to stomach, but at least it provides some decent perspective.

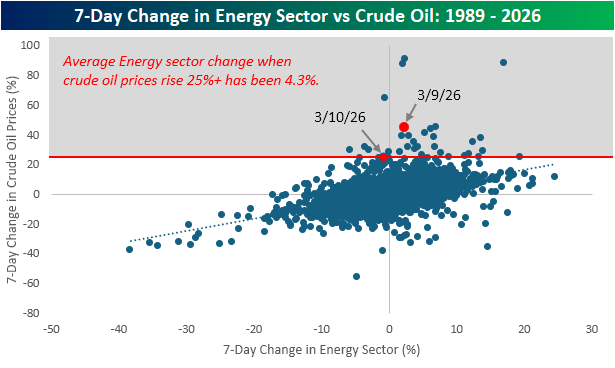

In the seven trading days since the war on Iran started, crude oil prices are up 25%, and as of yesterday, the seven -day change was over 45%. With such large increases, it seems like a disconnect that the S&P 500 Energy sector is up just 2%. The chart below compares the 7-day change in the S&P 500 Energy sector to the 7-day change in crude oil prices. While there has historically been a positive correlation between the two, in periods when crude oil prices have spiked 25% or more, the average change in the Energy sector has been a gain of 4.3%. The implication of those muted gains? The market views these price spikes as temporary.

Mar 10, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think we’re at a bottom. I really do.” – Mark Haines, CNBC, 3/10/09

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a dramatic reversal late in yesterday’s session on hopes that the war in Iran would be ‘complete’ soon, futures were higher for the overnight session and into this morning. As the opening bell approaches, though, futures have been drifting lower, and all of the major averages are on pace to open fractionally lower. Treasury yields are little changed, and crude oil has been volatile, sitting under $90 per barrel. While that seems low relative to Sunday night, it’s still much higher than anything seen in the months leading up to the war in Iran. Gold prices are up over 1.5%, and silver is surging 5% as it’s currently trading at the same price as WTI! Bitcoin has been quietly grinding higher over the last few days, and this morning, it’s above $70K.

Earnings season is largely in the rearview mirror, but after the close, we’ll hear from Oracle (ORCL), which could be a major catalyst tomorrow for different parts of the AI ecosystem. The only economic reports on the calendar today are small business optimism from the NFIB, which came in weaker than expected (98.8 vs 99.5), and then at 10 AM, we’ll get Existing Home Sales for February.

Asian markets followed the lead of the late-day reversal in US equities and traded sharply higher overnight. It wasn’t enough to entirely erase Monday’s losses, but the Nikkei rallied just under 3% while South Korea surged over 5%. Chinese stocks rallied a more modest 0.7%, and while February exports surged 39.6% y/y, exports to the US declined 17%. Those lost exports to the US were scattered across Europe and Southeast Asia, and many of those likely ended up finding their way into the US in a roundabout way. In Japan, GDP rose 0.3% q/q, which was higher than expected, and in South Korea, growth contracted less than expected.

European stocks are also sharply higher this morning as the US reversal occurred after those markets closed for trading yesterday. The STOXX 600 is up 2.3%, and Germany, Italy, and Spain are all up over 2% as well.

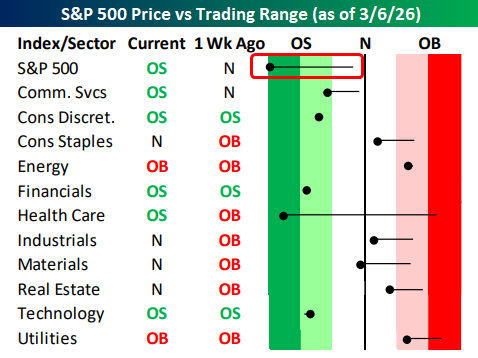

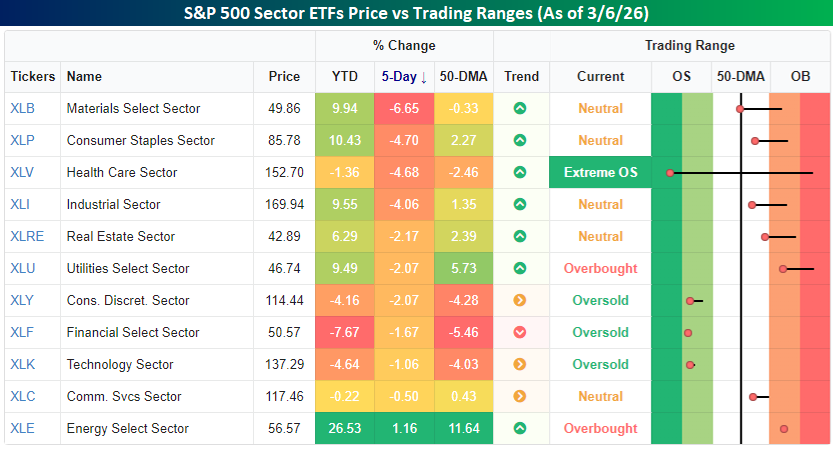

When you looked at page two of the Morning Lineup to see where sectors closed out last week relative to their trading ranges (image below), you may have done a double-take at seeing that the S&P 500 was in ‘extreme’ (2+ standard deviations) oversold territory and more oversold than any sector. In fact, the only other sector in extreme oversold territory was Health Care (after being in extreme overbought territory a week earlier), and just four other sectors were oversold while five were still above their 50-DMAs.

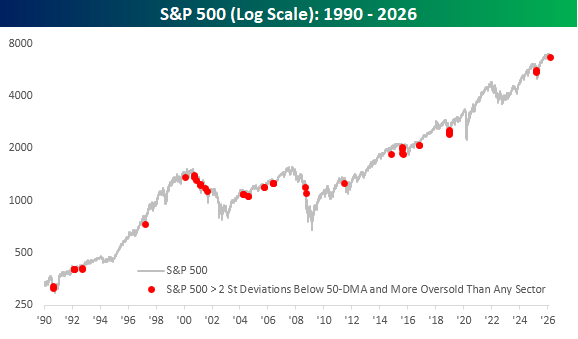

We were curious to see how often it is that the S&P 500 trades in ‘extreme’ oversold territory and is also more oversold than any other sector. Since sector data begins in 1990, there have only been 49 other days when this was the case, and a lot of them occurred during the dot-com bust from early 2000 to late 2001, but as the chart below illustrates, it’s hardly just a bear market phenomenon.

Mar 9, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is no instance of a nation benefitting from prolonged warfare.” – Sun Tzu, The Art of War

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If there’s ever a day that feels like a Monday, today is it. As much as we may like daylight savings time for the later sunsets, we could do without the later sunrises after already missing an hour of sleep. Couple that with triple-digit oil prices and much lower equity prices, and we almost wish our alarms didn’t go off this morning.

Equity futures are down over 1% across the board this morning, treasury yields are higher with the 10-year yield now up to 4.17% (it was below 4% less than two weeks ago), and WTI crude oil is up over 10% to $102 per barrel. Incredibly, that’s down around 15% from just under $120 overnight. There’s been no flight to safety in gold either, as prices are down over 1% there too.

Equities in Asia plunged overnight, with the Nikkei down over 5%, while South Korea fell 6.0% after circuit breakers were triggered during the session. In China, CPI for February rose much more than expected, rising 1% after an increase of 0.2% in January. And that was before the spike in oil prices. European equities are also down more than the US. The STOXX 600 is down 1.6% with France down over 2% and Spain down just under 2%. We can try to read into different catalysts for the weakness, but it’s pretty much all oil. Until those prices stop rising, equity prices will continue falling.

The economic calendar is quiet today, and there will be no Fedspeak as the blackout period ahead of next week’s meeting started this weekend. The economic calendar will be very busy, though, with CPI on Wednesday, Jobless Claims, Housing Starts, and Building Permits on Thursday, and Personal Income and Spending, as well as GDP, among others, on Friday.

The war in Iran hasn’t had much of a benefit on any sector, except, of course, Energy. Since the fighting broke out just over a week ago, Energy has rallied over 1% while every other sector is in the red, with nine down more than 1%. Four sectors declined by over 4%, with Materials leading the losses at 6.65%, followed by Consumer Staples, Health Care, and Industrials. Health Care’s losses have taken that sector into ‘extreme’ oversold territory after trading in ‘extreme’ overbought territory just over a week ago. War has a way of changing market conditions very quickly!

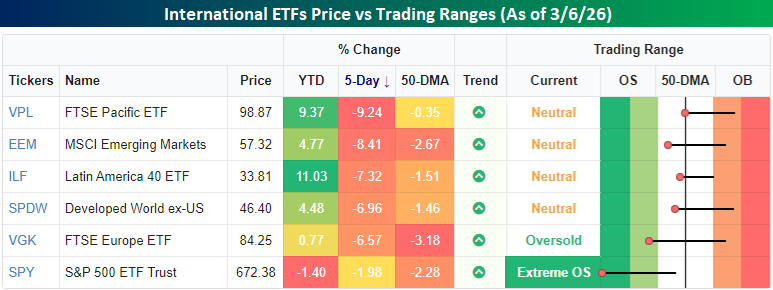

As bad as the US markets have been since the war broke out, it’s peanuts compared to the losses in the rest of the world. Below, we show the performance of various regional ETFs last week. While the S&P 500 was down nearly 2% last week, every other region of the world was down at least 6% and, in most cases, even more. Europe was down 6.6%, emerging markets were down over 8%, and stocks in the Asia Pacific region were down over 9%. As much as higher oil prices are a pain for US consumers and businesses outside of the Energy sector, other areas of the world are much more dependent on external sources for energy than the US.

In terms of the US vs. the rest of the world trade, the Developed World Ex US ETF was down nearly 7%, or five percentage points more than the S&P 500, in a week! As much as the US outperformed the rest of the world last week, it’s still significantly underperforming the rest of the world on a YTD basis (-1.4% vs +4.5%).

With the S&P 500 on pace to gap down 1% at the open for the fourth time in six days today, volatility has been on the rise, and the VIX is trading above 30 for the first time since last spring during the tariff-tantrum. Back then, though, the VIX briefly breached 60 before pulling back. So far during the current war, the highest the VIX has traded is 35.3. Last week may seem like a rough period for the markets, but relative to other points in just the last year, it could be a lot worse. The longer this conflict lasts and oil supplies remain disrupted, the more likely it is that conditions will worsen.

Mar 6, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I never worry about the problem. I worry about the solution.” – Shaquille O’Neal

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Did you know that there’s an employment report today? With geo-politics in the forefront, economic data has largely taken a back seat this week, but the data will keep coming (unless there’s a shutdown, of course!), and heading into this morning’s report, the S&P 500 and Nasdaq are indicated to open down by between 0.75% and 1.0%, continuing a week of lousy market action. Treasury yields are higher, crude oil is surging, and gold is fractionally higher.

In Asia, most major indices were flat to lower, but still finished the week sharply lower, with the Nikkei down 5.5%, China down 2.1%, and South Korea down more than 10%. In Europe, the losses are even larger, with the STOXX 600 down over 1%, taking its decline for the week to over 5%. Across the continent, every major benchmark is down over 5% this week.

Besides the Employment report, Retail Sales also hit the tape at 8:30. The employment report was a disappointment across the board as Non Farm Payrolls fell 92K versus forecasts for an increase of 55K, and the Unemployment Rate increased to 4.4% versus forecasts for 4.3%. Average hourly earnings were slightly higher than expected, rising 0.4% versus forecasts for an increase of 0.3%. As bad as that report was, it will be interesting to see if there were any weather-related impacts. While the jobs picture was weaker, Retail Sales came in better than expected.

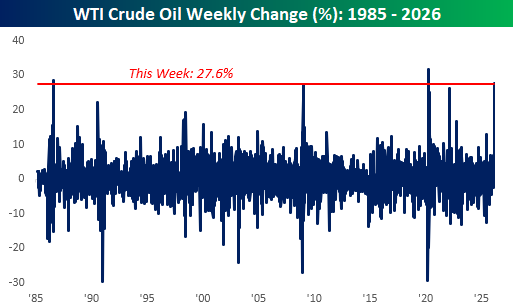

When markets opened for trading on Monday, and crude oil prices rallied a bit over 5%, it was viewed as a surprisingly muted reaction to a monumental event in the Middle East. It looked like we got off easy. As the days have gone on and the conflict has continued, crude oil prices rose every day this week with a 4.7% gain on Tuesday, a 0.1% gain on Wednesday, an 8.5% gain on Thursday, and what’s shaping up to be a 6.5% gain today. The frogs in the market pot had no idea what was coming.

Adding them all together, WTI is on pace for a 27.6% gain this week, which would rank as the third-largest weekly gain since at least 1985. The only two larger gains were 31% in early April 2020 during Covid and 28.4% in August 1986 when OPEC announced a surprise production cut. One-week rallies of this magnitude aren’t very common.

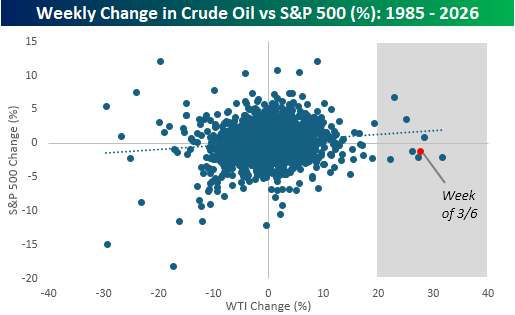

With oil prices up so sharply, it’s not surprising that equities have been under pressure, but looking at past moves shows that the inverse relationship isn’t as strong as you would think. The chart below compares the weekly change in crude oil to the S&P 500 going back to 1985, and there’s little correlation between the weekly direction of crude oil prices and the S&P 500. If anything, the correlation is slightly positive.

The shaded area includes each of the prior weeks when crude oil prices were up 20%, and of the seven occurrences, the S&P 500 was up three times and down four. For all seven weeks, the S&P 500’s median decline was 1.2%. Based on where futures are trading right now, guess how much the S&P 500 is down this week? 1.2%!

Mar 5, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The world makes much less sense than you think.” – Daniel Kahneman

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 crept into positive territory for the week, which was incredible given the circumstances, but futures are set to erase those gains at the open. Both the S&P 500 and Nasdaq are indicated to open down by 0.25%. The biggest driver of weakness is crude oil, where prices are up another 3% to $77. It’s simple at this point: the more crude oil rises, the bigger a headwind it will be for equities.

In Asia, stocks were higher across the board, with the biggest gains coming from South Korea, where the KOSPI rallied 9.6% following the 12% decline on Wednesday. Talk about a rational market! In Europe, the tone is less positive. While markets in the region started the day higher, they have been giving up those gains as the UP open approaches and are now all broadly looking at modest declines.

It’s been a busy morning for economic data, and most of it was better than expected. Initial jobless claims were slightly weaker than expected, and continuing claims were modestly higher. Import Prices were lower than expected, while both Non-Farm Productivity and Unit Labor Costs came in higher than expected.

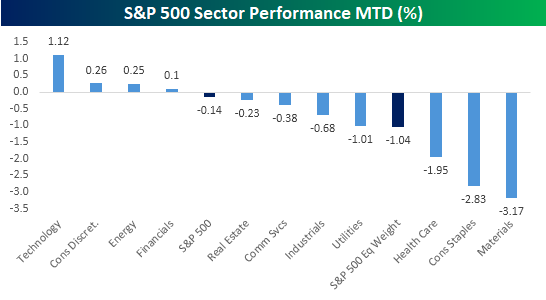

We’re less than a week into the war in Iran, but it’s never too early to see what trends within the equity market may be starting to emerge. At the sector level, you would expect to see a rush into defensive areas as investors rein in risk at the expense of cyclicals. So far, we’ve seen nearly the opposite play out. While the S&P 500 is up so far this week, which is surprising in itself, the four sectors outperforming the market are Technology, Consumer Discretionary, Energy, and Financials. If you had asked most people what sectors would outperform the market following a full-scale breakout of war in the Middle East, the only one of those four sectors that would come to mind is Energy.

The sectors you would expect to outperform in the event of war would be defensives like Utilities, Consumer Staples, and Health Care. But guess what? They’re three of the four worst-performing sectors with declines of at least 1% each! While the S&P 500 is surprisingly higher this week, the rally is primarily due to the 1%+ gain in the Technology sector. On an equal weight basis, the index is down 1.04%, and 60% of its components are down MTD.

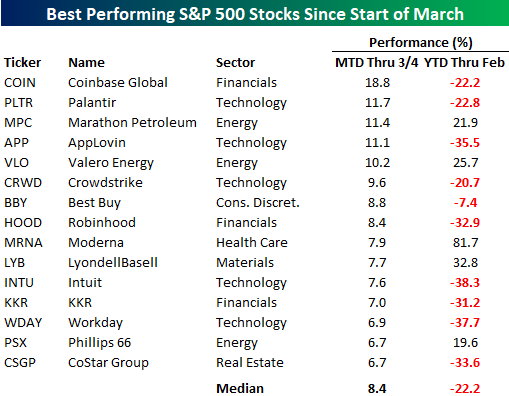

At the individual stock level, the list of winners is mostly devoid of defensive stocks. Instead, it’s littered with stocks that were recently considered some of the hottest growth stocks in the market before falling on hard times in late 2025 and earlier this year. Of the 15 top-performing stocks in the S&P 500 since the war broke out, their average YTD change in the first two months of the year was a decline of 22.2%, and ten of them were in the red. The two top-performing stocks – Coinbase (COIN) and Palantir (PLTR) – were both down over 20% in the first two months of 2026. While PLTR, with its military contracts, benefits from geopolitical instability, it’s hard to look at most of the other non-Energy stocks and see the obvious reason as to why they would benefit.

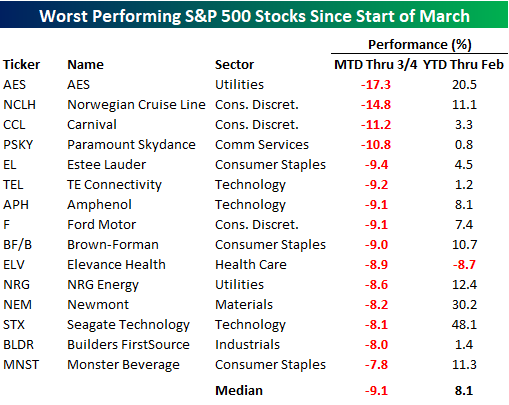

While the list of winners is mostly stocks that were down sharply YTD, all but one of the stocks on the list of losers were up YTD heading into March. Their average YTD gain was 8.1%, and seven were up by double-digit percentages. Leading the way lower, AES was up 20%+ YTD heading into March, but it has given most of that back in the first few days of March. Behind AES, cruise operators Norwegian Cruise Line (NCLH) and Carnival (CCL), along with Paramount Skydance (PSKY), are the only other stocks down by double-digit percentages. The declines in NCLH and CCL make sense given the geopolitical uncertainty, but the drop in PSKY is company-specific and tied to the merger with Warner.

Looking both at sector and individual stock performance since the war broke out, it seems as though investors have taken a back-to-basics approach, focusing on what had been working rather than what was working at the time that hostilities broke out. Whether that’s due to trade unwinds and short-covering given the heightened uncertainty or a reversion to tech remains to be seen, but in the early going, market performance and internals have done what they always do – surprise nearly everyone.