Bespoke Morning Lineup — Another 1%+ Monday Open Lower

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. This morning we take a close look at how SPY usually trades following big gaps lower of 1%+ at the open.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Trading Places

New US tariffs against Chinese imports took effect at midnight and the rest of the world pretty much yawned. Chinese stocks rallied more than 3% for their best day in a month, and European equities are all in the green. US futures, however, haven’t followed the global rally. They are now actually near their lows of the day, taking another leg lower after April CPI just missed expectations by a tenth of one percent on both the headline and core measures.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

As markets have faltered a bit in the last several days, one sector that has given up its leadership status is Technology. As highlighted in our Sector Snapshot report last night, just 52% of stocks in the sector are currently trading above their 50-day moving average, which is only slightly better than the 50% reading for the S&P 500. So, where have Tech sellers been going in place of Technology? One sector that has benefitted is Health Care. As shown below, just as the Technology sector’s relative strength topped out in the last several days, Health Care has seen a big improvement.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Semi-Concern

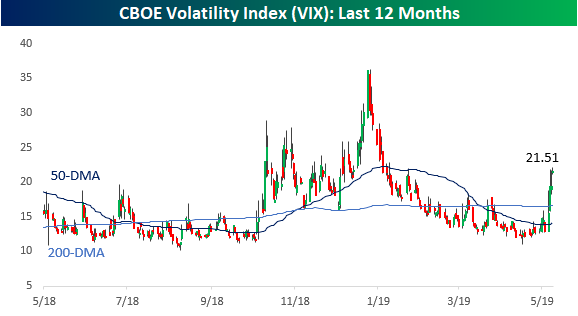

The usual headlines with regards to China are circulating this morning, and there’s more where that came from for the next two days as a Chinese delegation arrives in Washington today. Further complicating things, North Korea launched its second missile test in less than a week overnight which just happened to coincide with a visit from a US envoy to South Korea. Geopolitics are no doubt starting to heat up, and so is the VIX as it poised to close above 20 for the first time since early January!

Outside of geopolitics, there’s also a fair amount of US economic data today after a number of days this week with few or no reports. PPI for April was inline with expectations at the headline level (0.2% m/m) but weaker than expected at the core level (0.1% vs 0.2%). Jobless claims, meanwhile, came in higher than expected at 228K versus estimates for a reading of 220K. On the earnings front, we saw a little bit of a switch this morning as the pace of revenue beats is actually ahead of the pace of EPS beats since yesterday’s close. Of the over 150 companies that have reported since Wednesday’s close, just 56% have exceeded EPS forecasts by 59% have beat top-line forecasts. It would have been preferable to see the switch take place as a result of an improvement in the revenues beat rate rather than a big drop in the EPS beat rate.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

As shown below, the VIX has seen quite a surge in the last week. Last Friday, it wasn’t even a teenager and today it’s over the legal drinking age. My how they grow up!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Quick Change

Futures are down again this morning as global equities sell-off in the wake of yesterday’s brutal day in the US. Traders are in no mood to take a stand right now as the uncertainties regarding China and Iran take center stage. The flight to safety has provided a big boost for treasuries, re-flattening the yield curve closer to the inversion zone. And to think, just three trading days ago, the S&P 500 was flirting with a record high close! Change happens fast!

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Each morning on page two of the Morning Lineup, we show the daily percentage of S&P 500 stocks trading at overbought and oversold levels over the last year. In the chart below, we combine those two series to show the daily reading on a net basis. After reaching extreme negative levels back in late December, this indicator saw a sharp rebound at the turn of the calendar and has basically been in positive territory for most of this year. Following yesterday’s shellacking in the market, though, the net percentage of overbought stocks turned negative for the first time since mid-January. While there may have been short-term froth in prices heading into this week, the rekindling of Chinese trade issues as well as geopolitical issues bubbling up in the Middle-East, has been more enough to settle sentiment down in the short-term.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Trade Not the Only Headline Weighing on Stocks

It’s not just US-China trade headlines weighing on global equities this morning. Equities in Europe are trading lower after Factory Orders in Germany showed a much lower than expected increase in March (0.6% vs 1.4%). Along with that weak report, the European Commission just released economic forecasts and lowered 2019 GDP growth forecasts for the region from 1.3% down to 1.2% and said risks from global trade tensions and Brexit remain ‘pronounced’. Not to be left out of the discussion, the Federal Reserve issued its May 2019 Financial Stability Report which included the warning that “elevated valuation pressures are signaled by asset prices that are high relative to economic fundamentals or historical norms.”

Even the flow of earnings reports hasn’t been anything special in the last 15 hours. Since the close on Monday, 155 companies have reported earnings and of those, only 61% have exceeded EPS forecasts, while a slightly lower percentage (59%) managed to exceed topline revenue estimates.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Along with the general rebound in equities across the board, small caps managed to finish the day slightly in the green yesterday as the Russell 2000 closed at its highest level since 10/9/18. Yesterday’s strength served as a follow-through to Friday’s breakout above resistance where the Russell finally managed to break above a level that has repeatedly acted as resistance over the last six months.

In addition to positive price action in small caps, breadth has been holding up well too. While not yet at a new high, last Friday, the Russell 2000’s cumulative A/D line reached its highest level since September 21st. Unlike the S&P 500, though, the peak breadth reading for the Russell was at the end of last August. Still, as evidenced by the recently widening gap between the two lines below, breadth has been increasingly outpacing price in the Russell 2000 for the last two months.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Morning Lineup – Here We Go Again!

Just when you thought the days of markets opening down sharply in reaction to an overnight headline concerning trade negotiations with China were over, we get this morning. There isn’t a whole lot of earnings data to contend with and the economic calendar is blank for today, so it looks like just three days after Kudlow decided to spike the ball in reaction to Friday’s NFP report, the President is shaking things up a bit with his tweet-storm last night.

US futures are set to open down over 1%, but the gains don’t look to be anywhere near as severe as what happened in China where the decline was more like 5%. Also, ever since the initial gap down, things have been extremely steady. Today’s decline is set to be the 9th gap down of 1% or more for the S&P 500 since the start of 2017, and in today’s Chart of the Day we looked at how the index performed following prior occurrences as well as what the catalyst for each decline was, so if you haven’t already seen it, check it out.

We’ve just published today’s Morning Lineup featuring all the news and market indicators you need to know ahead of the trading day. To view the full Morning Lineup, start a two-week free trial to Bespoke Premium.

Last night’s sell-off in Chinese equities put a big dent into this year’s gains for the Shanghai Composite. With a drop of more than 5.5%, it was the largest one day decline for Chinese stocks since February 2016. Year to date, the Shanghai Composite is now up 16.54% on the year and has nearly cut this year’s gains in half. More noteworthy is the fact that with the S&P 500 up 17.5% YTD heading into today, the US is now outperforming Chinese stocks YTD. Obviously, with futures down over 1%, the US lead may not last for long, so we’ll have to see how things shake out over the course of the trading day.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.