Jul 31, 2025

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Jul 31, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“’Deserves’ is an impossible thing to decide. No one deserves anything.” – Milton Friedman

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

With the Fed and the Ms of the mega-caps behind us, we’re just about halfway through what has been a monster week of economic, earnings, and Federal Reserve data. Through yesterday’s close, the S&P 500 was down 0.4% for the week, which wasn’t that bad. If you take into account the overnight gains that followed the monster earnings from Meta Platforms (META) and Microsoft (MSFT), though, we’re up about 0.5%, which is pretty good.

Futures are sharply higher this morning following positive earnings reports from the megacaps. Today and tomorrow will provide a lot more economic data to deal with, though. This morning, it’s Personal Income and Spending, PCE, and jobless claims, while tomorrow’s focus will be the Non-Farm Payrolls report. On the earnings front, it’s the As turn tonight with Amazon.com (AMZN) and Apple (AAPL) on the calendar, so we’ll see if they can keep the positive streak alive.

Despite the positive overnight action in equity futures, Chinese stocks were down sharply, with declines of over 1% while Japan was up 1%. The rally in Japan followed a BoJ rate decision where rates were left unchanged. In Europe, the tone is also mixed with the STOXX down fractionally.

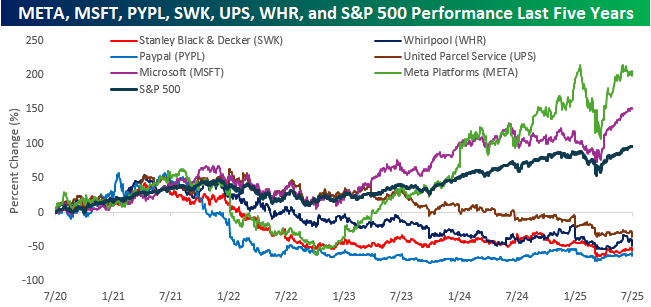

Yesterday, we mentioned that a number of commentators were pointing to negative reactions in the stocks of PayPal (PYPL), Stanley Black & Decker (SWK), United Parcel Service (UPS), and Whirlpool (WHR) as a potential red flag for the economy. We thought those concerns were misplaced, given that these stocks have been disasters in terms of their performance over the last five years. On a combined basis, they also have a market cap of just $156 billion.

Last night, we got reports from Meta Platforms (META) and Microsoft (MSFT). META has a market cap of more than 10 times the four stocks mentioned yesterday, while MSFT’s market cap is more than 20 times larger. As shown in the chart below, both stocks have also been a much better representation of the economy over the last five years.

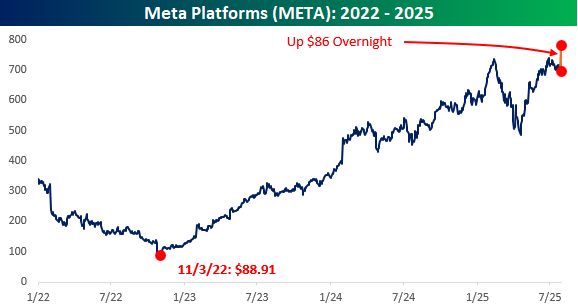

In the case of META, it’s hard to believe how far this stock has come since its bear market lows less than three years ago. Think about this for a second. At its low on 11/3/22, META closed at $88.91 per share, and earlier this morning, shares were up $86. In other words, META was up almost as much overnight as its entire share price was at the low in November 2022.

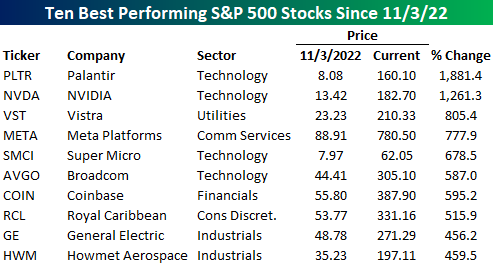

Given the massive rally in META, it’s not a big leap to conclude that it has been one of the top-performing stocks since its low in November 2022. As shown on the table below, taking early morning gains into account, the stock is up nearly 780% which is only enough to rank as the fourth-best performing stock during that time. Palantir (PLTR) tops the list with a gain of over 1,800% followed by Nvidia (NVDA) at 1,261%, and then Vistra (VST) with its gain of 805%. Even after rallying 777%, META is still underperforming a Utility stock!

On a final note, while META and MSFT are on pace for big gains today, watch how they trade intraday. Earlier this week, we saw Boeing (BA) rally on good news at the open only to sell off intraday. That’s not a pattern bulls want to see becoming a trend!

Jul 30, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Measuring programming progress by lines of code is like measuring aircraft building progress by weight.” – Bill Gates

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are modestly higher this morning after the July ADP report came in better than expected, erasing a streak of three months of weaker-than-expected readings. Q2 advance GDP was also just released and came in stronger than expected (3.0% vs 2.6%). Personal Consumption was weaker than expected (1.4% vs 1.5%) while the inflation data was mixed (lower than expected at the headline, higher than expected on a core basis). While these would be big reports on a normal day, we still have the Fed this afternoon and earnings from Meta and Microsoft after the close.

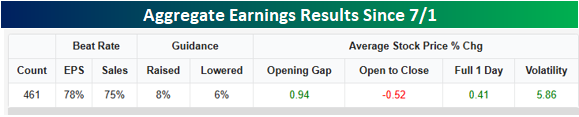

We’re right in the thick of earnings season, and we’ll see hundreds of more reports between now and the end of the week. From the start of July through Tuesday morning, we’ve already got 461 reports, and of those, 78% exceeded EPS forecasts while 75% have topped sales estimates. Looking forward, 8% of companies reporting have raised their guidance, while just 6% have lowered their estimates. These are all better than average readings, and as you would expect, companies are reacting positively to these reports. Overall, the average opening gap of the companies reporting has been a gain of 0.94%, but from the open to close, we’ve seen selling into strength with an average decline of 0.52% for a full-day gain of 0.41%. On the one hand, the average positive reaction to earnings reports is a good signal, but the weakness from the open to close indicates that investors are taking profits.

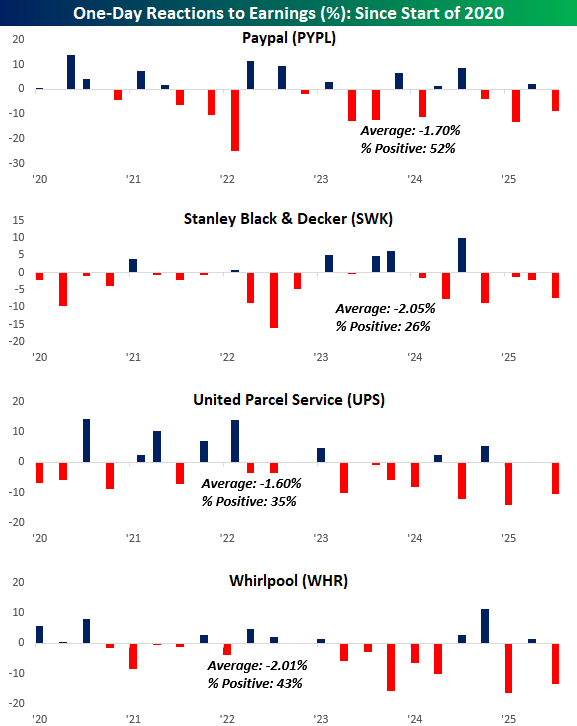

Despite the overall positive tone of reports, yesterday we saw multiple stories highlighting four stocks and their negative reaction to earnings as a potential warning sign for the economy and market. Those four stocks were PayPal (PYPL), Stanley Black & Decker (SWK), United Parcel Service (UPS), and Whirlpool (WHR), and all of them were down at least 7%.

Besides the fact that these four stocks have a combined market cap of less than $160 billion, which wouldn’t even be enough to rank in the top 75 companies in the S&P 500, they have all historically had weak reactions to earnings, especially in recent years. The chart below shows each stock’s performance on its earnings reaction days over the last five years. All four have averaged declines of at least 1.6% on their earnings reaction days, and only PYPL has reacted positively more often than it has reacted negatively.

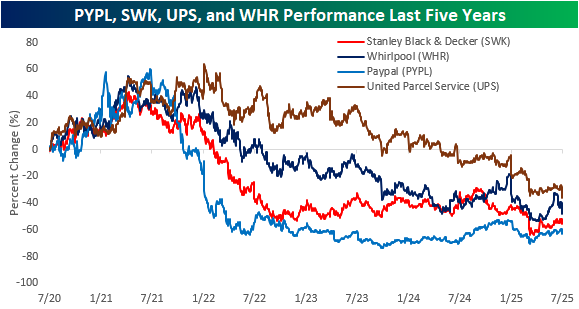

More importantly than the performance on their earnings reaction days, all four stocks have been horrendous performers over the last five years. As shown in the chart below, at one point in the last five years, all four stocks were up at least 40% from where they traded five years ago, but they have erased those gains and more over the last five years. UPS is down 36%, WHR is down 48%, while PYPL and SWK have both lost over half of their value. During this same period, the S&P 500 has rallied 96%. Far from being economic or market bellwethers, these stocks have been among the S&P 500’s worst performers over the last five years! We could highlight any number of reasons why investors should be more cautious heading into the end of summer, but the fact that four stocks that have historically performed poorly on earnings saw weakness yesterday is not one of them.

Jul 29, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I can’t change the fact that my paintings don’t sell.” – Vincent van Gogh

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Can we get lucky number seven? Futures on all three major indices are indicated higher this morning as the market prepares for a surge in economic and earnings-related news. On the economic calendar, the two major reports of the day are JOLTS and Consumer Confidence at 10 AM, and then after the close, we’ll get several notable earnings reports, including Starbucks (SBUX) and Visa (V). Already this morning, we’ve gotten reports from Boeing (BA), Procter & Gamble (PG), and UnitedHealth (UNH), to name a few.

In Asia, markets were mixed, with Japan down nearly one percent while China was up fractionally. Investors are still waiting for details and results from the US-China trade talks in Stockholm, but there have been no major economic reports to speak of. In Europe, yesterday’s session experienced weakness throughout the trading day as most major indices finished near their lows of the day, but this morning, there have been broad-based gains with the STOXX 600 up nearly 75 bps while Germany, France, Italy, and Spain are all up over 1%.

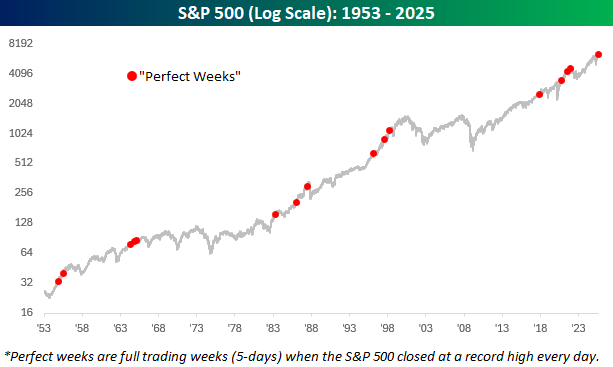

While it’s not the longest winning streak of the year, and the magnitude of the daily gains has been far from impressive, yesterday was the S&P 500’s sixth straight day of closing at a record high. That’s already impressive, but looking back at where the market was three months ago, it’s hard to even believe that the S&P 500 is anywhere near a new high! As things currently stand, this streak is tied for the longest since the six days ending last July, and if we close higher today, it will be the longest streak since the eight days ending on 11/8/21.

Yesterday’s positive session followed what had been a ‘perfect week’ for the market, where it not only closed higher every day, but it also closed at record highs on each one of them. That doesn’t happen often. The last time there was a full week of trading, and the S&P 500 closed at a record high on all five days, was in November 2021. Since the five-day trading week in its current form started in late 1952, there have now only been sixteen perfect weeks, which are highlighted in the chart below.

Jul 28, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I want to live my life, not record it.” – Jacqueline Kennedy Onassis

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We hope you had a restful weekend, because the last four days of July and the first trading day of August are going to be jam-packed with earnings and economic data. Among the hundreds of companies reporting earnings this week, Meta (META) and Microsoft (MSFT) will report on Wednesday, followed by Amazon.com (AMZN) and Apple (AAPL) on Thursday. Regarding economic data, besides the Non-Farm Payrolls report on Friday, we’ll also receive the ISM Manufacturing report on the same day, along with the Michigan Sentiment. However, these reports will be followed by Consumer Confidence on Tuesday, ADP, GDP, and PCE on Wednesday, and jobless claims on Thursday. Don’t forget that there’s also an FOMC meeting this week that ends on Wednesday and the August 1st deadline for trade deals on Thursday. We already need a break just thinking about everything on the calendar!

This morning, equity futures are in a modestly positive position leading up to the onslaught of events and following a perfect week for the S&P 500 where it traded higher and at a record close every day last week. European stocks are also higher in the wake of the US–EU trade deal announced yesterday, and the STOXX 600 is up just over 0.5%. In Asia, it was more of a mixed session where Australia traded slightly higher, Japan was down over 1%, while China was fractionally higher.

Outside of equities, treasury yields are slightly higher, crude oil is up over 1%, while natural gas is down 1%. Gold, silver, and copper are basically unchanged to start off the week, but platinum and palladium are both up over 2%. In crypto, Bitcoin is trading just under $119K while the rally in Ethereum continues as it trades just below $3,900.

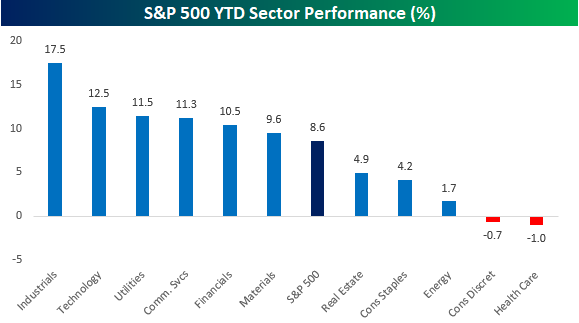

With all the talk about how market performance has been unbalanced between the mega-caps and everyone else, we wanted to look at performance within the S&P 500 on a YTD basis. At the sector level, most sectors (6) have outperformed the S&P 500 on YTD basis. Yes, Technology is one of the sectors that’s ahead of the S&P 500, but other non-tech sectors like Industrials, Utilities, Financials, and Materials have also outperformed on a YTD basis. On the other side of the performance spectrum, Health Care and Consumer Discretionary are the only two sectors in the red on a YTD basis.

Jul 25, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When you’re good at something, you’ll tell everyone. When you’re great at something, they’ll tell you.” – Walter Payton

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are sitting on modest gains as the S&P 500 looks to close out the week with a 1% gain. The S&P 500 has traded higher every day this week, and the number of record closing highs is starting to pile up with 13 on the year so far. That’s nowhere near last year’s total of over 50, but considering where the market was three months ago, it’s impressive to say the least.

While US equity futures hang onto positive territory, Asian stocks finished in the red even as the Nikkei started off the session at new highs. The reversal stemmed from concerns over a more aggressive BoJ. European stocks are also firmly in negative territory, with the STOXX 600 down about 0.5%. Outside of equities, energy commodities are modestly higher, while metals prices are lower across the board. In crypto, Bitcoin and Ethereum are both lower. It’s also worth pointing out that Bitcoin is now down near $116,000 after hitting a high of $123,000 eleven days ago.

The pace of earnings so far this month has been positive, economic data has been hanging in there, and we’re even starting to get some sense of clarity on tariffs, so you can’t fault investors for being optimistic. Today, we’ll get a bit of a break from the data, though, as the earnings and economic calendars are relatively light, but you never know when the President will drop a tariff-related headline.

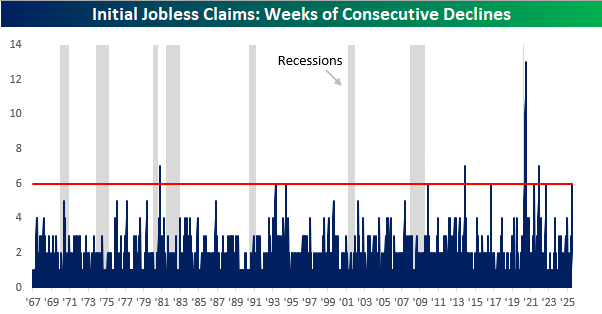

While there’s not a lot of economic data today, we wanted to take a moment to look back at yesterday’s initial jobless claims report, which came in weaker than expected and declined on a week-over-week basis for the sixth time in a row. As shown in the chart below, this was just the 11th streak of six or more weekly declines. Of those prior ten streaks, only four were longer, with just one stretching more than seven weeks. That record was the 13-week stretch coming out of the Covid lockdowns. We also included shading to indicate recessions, and you typically don’t see these kinds of streaks leading up to the onset of a recession.

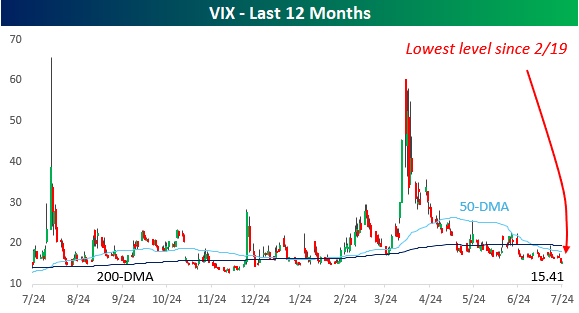

The market has been treading a steady path higher over the last several weeks, and one place the lack of volatility has shown up is in the VIX. This week, it dropped below 16 to its lowest levels since 2/19. That was right at the peak before the tariff-takedown, so it’s only natural to wonder if there’s a sense of complacency setting in.