Sep 22, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A man who is certain he is right is almost sure to be wrong.” – Michael Faraday

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 closed at its 27th record high of the year on Friday as investors continued to bask in the light of the Fed’s rate cut on Wednesday. The 28th record high of the year will likely have to wait at least another day, though, as futures on all three major averages are indicated to open down by a little more than 0.30%. Small caps, which also hit a record high last week after a long drought, are also lower but not by as much (0.23%) as the S&P 500.

Asian stocks were mixed overnight, with the Nikkei rallying 1% to another record high, while Hong Kong was down close to 1% and China was marginally higher. While Japanese stocks keep hitting record highs, JGBs keep falling as the 10-year yield hit the highest level since 2007.

In Europe, the tone is more one-directional with the STOXX 600 down 0.2% while Germany leads the way lower with a decline of 0.7%. There’s no economic data in the region this morning, but auto stocks are weaker with both Volkswagen and Porsche trading lower after lowering guidance.

As we noted in last week’s Bespoke Report, we’re in a data lull. While multiple FOMC members will speak today, last week’s cut is behind us, and earnings season doesn’t kick off for another two weeks. Newton’s first law of motion says that an object in motion tends to stay in motion unless acted upon by force, so that would suggest more gains ahead. However, it is late September, which is historically a weak time of year, and investors have seen some large gains over the last five months, so you can’t fault anyone for wanting to take some profits.

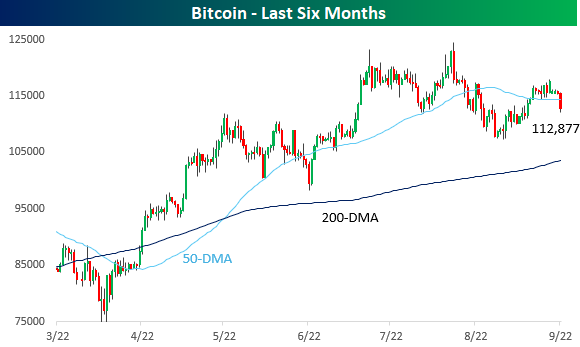

Crypto will be one place to watch for a measure of risk appetite in the market, and this morning’s action is showing a more defensive posture. Bitcoin is trading down over 2% this morning as it has broken below $113,000 and below its 50-day moving average (DMA). With today’s decline, Bitcoin is essentially trading right where it was back in May.

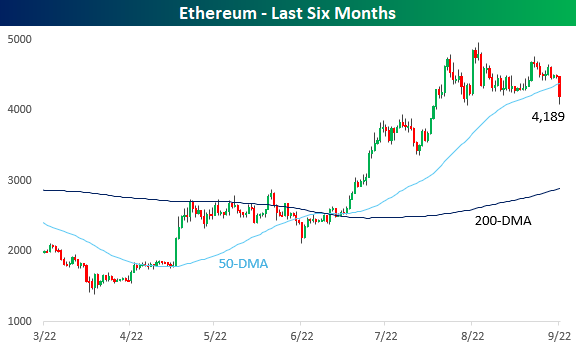

Unlike Bitcoin, which has been moving sideways, Ethereum prices had a much steeper run-up over the Summer, even as it has traded in a sideways range for the last month. This morning’s weakness in Ether has been more magnified with a decline of over 6%, and it too is below its 50-DMA for the first time in months.

Sep 19, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Language fits over experience like a straight-jacket.” – William Golding

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

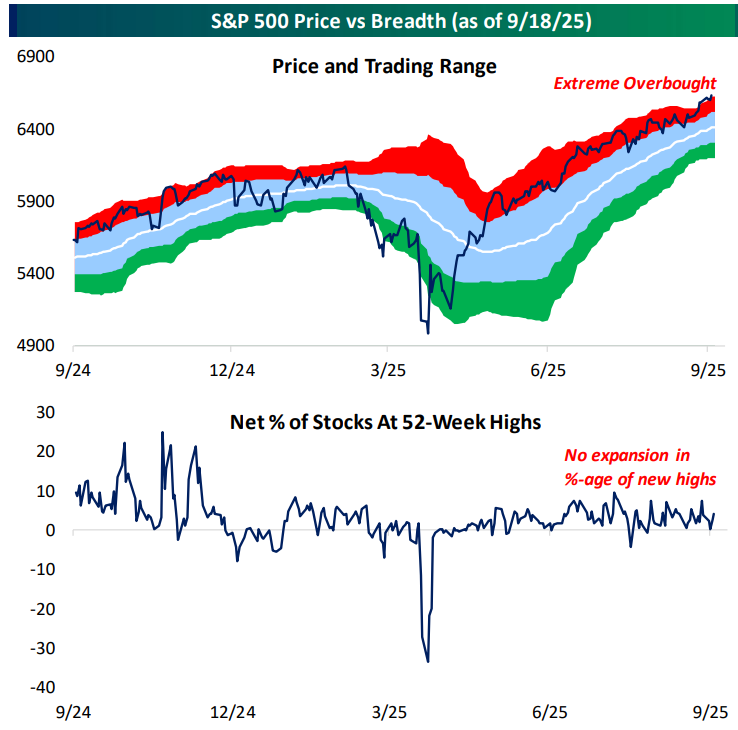

It’s important to continue to note that the S&P is trading in extreme overbought territory, but there hasn’t been a similar move with underlying breadth. Yet another breadth indicator that remains totally neutral is the percentage of stocks in the S&P trading at new 52-week highs.

Sep 18, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“He who waits to do a great deal of good at once will never do anything.” – Samuel Johnson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Investors apparently slept on the Fed’s announcement yesterday and woke up in a good mood. The S&P 500 is on pace to open up by 0.75% this morning, while the Nasdaq is on track to open up by more than 1%, and small caps are leading the way with a gain of 1.25%. The US strength follows what was a mostly positive night in Asia, where China was the only country to trade lower, while Japan and Korea both shot higher by over 1%. The strength in Japan came even as Machinery Orders fell 4.6% m/m compared to forecasts for a drop of just 1.8%. In Europe, stocks are also higher across the board as the STOXX 600 rallies 0.8%.

This morning in the US, there’s little in the way of earnings data, and the only reports on the economic calendar are jobless claims at 8:30 and the Philly Fed and Leading Indicators at 10 AM.

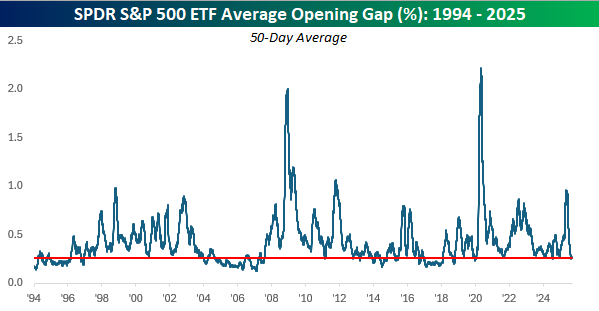

Like the quote above, the market’s grind higher for the last several months has been more gradual than a move concentrated into a handful of days. There are several ways to illustrate this, and we’ll start with the VIX. At 14.8 this morning, the VIX is on pace for its lowest close since late August, not exactly a level you would expect for what historically has been one of the most volatile months of the year. As shown in the chart below, if the VIX was an EKG, we’d be putting a sheet over the patient as it has flatlined since first falling back below its 200-DMA in June.

In addition to the low VIX, another example of the gradual moves is by looking at the S&P 500’s average opening gap. Using SPY as a proxy, the S&P 500’s average change at the open relative to the prior days’ close over the last 50 trading days has been 0.25%, and there has only been one day when the S&P 500 gapped up or down more than 1% (9/2/25: -1.17%). After volatility at the open rocketed to the highest levels since COVID back in April, the average daily change has sunk like a stone to some of the lowest levels of the last five years.

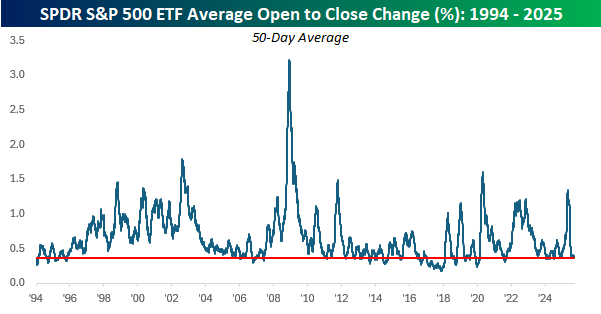

Just as volatility has been subdued at the opening bell, it has also been tamed during regular trading hours. Just like the average opening gap, intraday volatility shot higher in April only to come crashing down in the summer to around the lowest levels of the last five years. The old cliché says to never short a dull market, and that’s the only piece of advice an investor has needed over the last few months.

Sep 17, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To hell with facts! We need stories!” – Ken Kesey

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The long-awaited Fed decision day has arrived, and despite an Atlanta Fed GDPNow forecast for growth of 3.4% in Q3, stronger-than-expected retail sales in August, still relatively low (but admittedly rising jobless claims), and higher-than-normal inflation, the Fed will likely cut rates this afternoon. That’s not to say there is no justification for a rate cut. Continuing jobless claims remain elevated, job growth has practically evaporated, and both the manufacturing sector of the economy and housing remain weak. Additionally, other secondary indicators, such as heavy truck sales, have been particularly weak. There are very few people who would say that the Fed should not be cutting rates today, but given how fast sentiment towards rate cuts has shifted, it’s hard to argue that the President using the bully pulpit of the White House hasn’t at least played in role in shifting the conversation.

Heading into today’s session, equity futures are modestly negative along with treasury yields, crude oil, gold, and crypto. Housing Starts and Building Permits were also just released, and both reports missed expectations by a relatively wide margin, providing more justification for a cut today.

Overnight in Asia and this morning in Europe, equity markets had mixed returns. CPI in the Eurozone came in lower than expected, while it was hotter than expected in the UK. On a y/y basis, CPI for the Eurozone came in slightly lower than expected at 2.0% compared to forecasts for 2.1%.

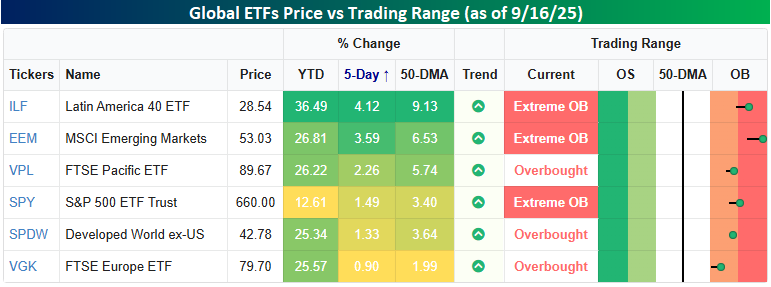

As we head into this afternoon’s expected rate cut from the Federal Reserve, US stocks have been in rally mode, but they’re not alone, at least from the perspective of a US investor. The snapshot below from our Trend Analyzer shows where various global ETFs closed yesterday relative to their short-term trading ranges. The S&P 500, as measured by the SPDR S&P 500 ETF (SPY) is up 1.5% over the last five trading days and closed yesterday in ‘extreme’ overbought territory (more than 2 standard deviations above its 50-DMA), but it’s not the only one and certainly not the best performer. Of the ETFs shown in the spotlight, three have outperformed the US over the last week, and SPY is the worst performer on a YTD basis.

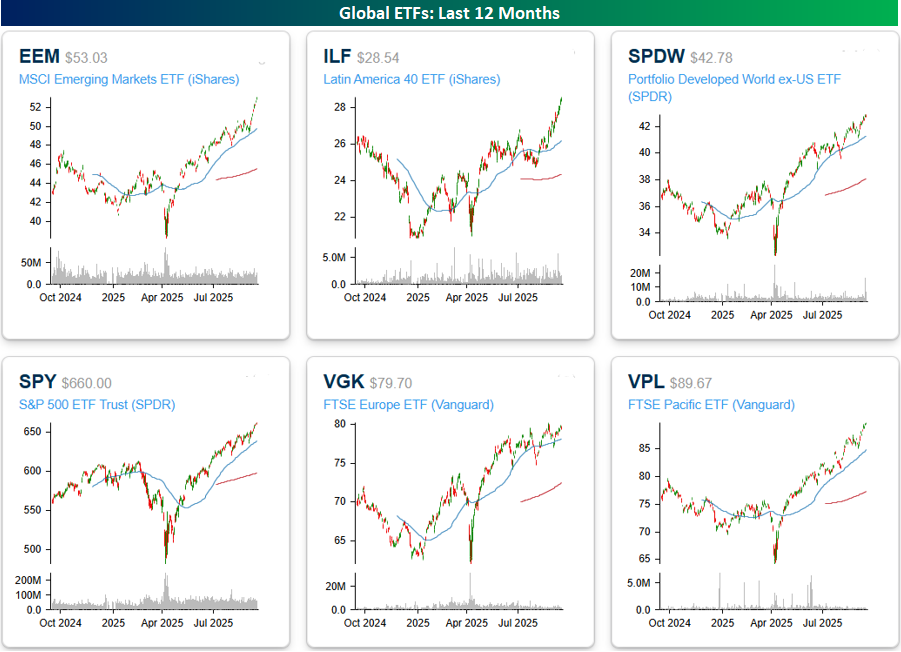

A look at one-year price charts of all six ETFs shows that they’re all either at or right near 52-week highs heading into today’s session. The only difference is the slope of their advances heading into those highs. The MSCI Emerging Markets ETF (EEM) and the Latin America 40 ETF (ILF) have been moving almost vertically over the last couple of weeks, while the FTSE Europe ETF (VGK) has been moving in more of a sideways range.

Sep 16, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The beautiful thing about learning is nobody can take it away from you.” – B.B. King

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We’re looking at another positive start to the market this morning, with futures modestly higher and the Nasdaq leading the way as mega-caps continue to lead the way. This morning’s economic calendar includes Retail Sales and Import Prices at 8:30, Industrial Production and Capacity Utilization at 9:15, and then Business Inventories and Homebuilder Sentiment at 10. After that, pretty much all of the focus will shift to tomorrow’s announcement from the FOMC, where rates are widely expected to be cut 25 bps.

This morning’s gains follow what was mostly a positive session in Asia. The highlight of the region was South Korea, where the Kospi rallied more than 1% for its 11th straight daily gain. In Europe, the tone isn’t as positive as the STOXX 600 trades down 0.2% even as the ZEW survey of economic sentiment unexpectedly increased, although Industrial Production for the Eurozone rose less than expected (0.3% vs 0.4%).

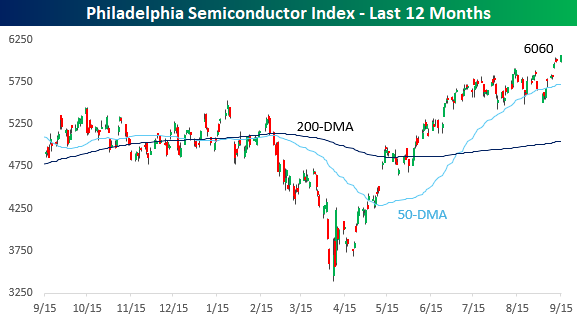

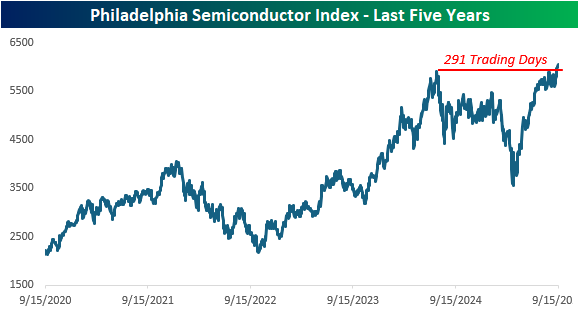

Like the major indices, semiconductor stocks have been lurching to new all-time highs, and when the semis are rallying with the overall market, it’s usually a good sign. After several successful tests of the 50-day moving average (DMA) in the summer, the Philadelphia Semiconductor Index (SOX) finally broke out above resistance last Wednesday.

The breakout to new highs also ended a streak of more than a year during which the index had not traded at an all-time high. At 291 trading days, it was the fifth-longest drought without a new high in the SOX’s history, dating back to 199,4, and the sixth-longest that lasted longer than a year. The longest streak was nearly 4,500 trading days ending in January 2018, and the second-longest ended less than two years ago in December 2023 at 488 trading days.

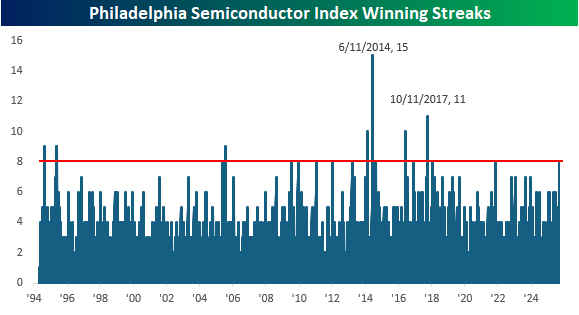

In the process of breaking out to new highs, the SOX has also traded higher for eight straight trading days, trailing the Nasdaq 100’s streak by a day. That eight-day streak is tied for the longest streak since October 2017, when it went more than two weeks in a row without trading lower. The longest streak was three weeks long, ending in early June 2014.

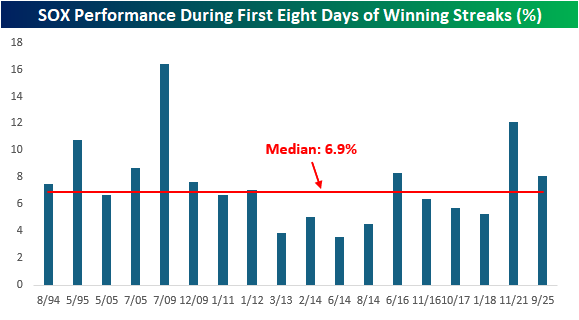

Over the course of the SOX’s eight-day streak, the index has rallied 8.1%, which comes in modestly ahead of the median gain of 6.9% during the first eight days of all 18 streaks and the sixth best overall.

Sep 15, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The best way to make your dreams come true is to wake up.” – Muhammad Ali

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a strong week, markets are getting off to a positive start this week ahead of this week’s Fed meeting. The S&P 500 is indicated to open with a gain of 0.25%. Overnight, Asia was mixed, but Europe has been higher across the board. The economic calendar is light to kick off the week, as the Empire Manufacturing report came in weaker than expected. Later on this week, things will pick up with Retail Sales highlighting Tuesday’s schedule and Housing Starts and Building Permits coming on Wednesday, along with the Fed.

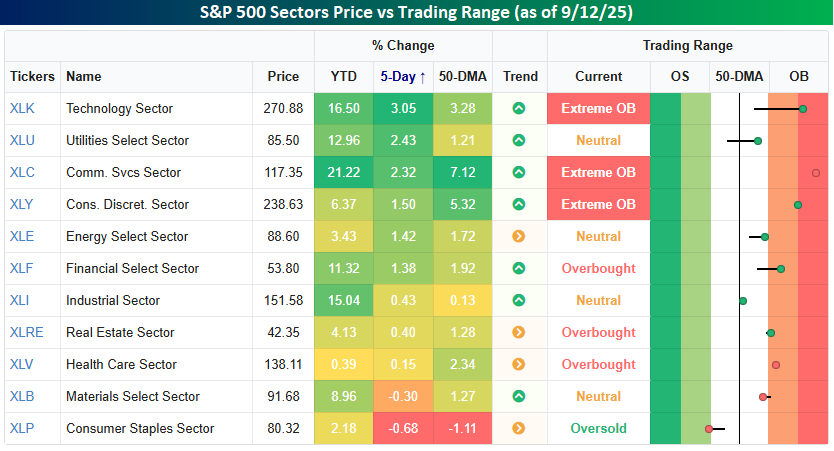

Markets are always forward-looking, and last week they looked forward to this week’s FOMC meeting, where Powell & Co will announce a cut of at least 25 basis points (bps) on Wednesday. Last week, six sectors rallied by at least 1%, including Technology, Utilities, and Communication Services, which rallied more than 2% each. We’ve grown accustomed to seeing Tech and Communication Services rally in unison. However, it’s still hard to get used to seeing the traditionally defensive-oriented Utilities sector rallying alongside those two sectors, but markets are always evolving. On the downside, the only sectors to finish lower last week were Consumer Staples and Materials. They’re also the only two sectors to finish last week below their 50-day moving averages. Consumer Staples is even oversold as well!

Six sectors finished last week at short-term overbought levels heading into this week’s Fed meeting, including three at ‘extreme’ overbought levels. While there is nothing prohibiting overbought sectors from becoming more overbought in the short term, it also sets up the possibility of a sell-the-news reaction to this week’s rate cuts. Just something to be on the lookout for.