Sep 30, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is easy to ignore the rain if you have a raincoat” – Truman Capote

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Be sure to catch Paul Hickey today on CNBC’s Squawk on the Street at 10 AM.

It’s a modestly negative tone this morning as S&P 500 futures trade down 0.2% and the Nasdaq is down slightly less. Headline writers are attributing the weakness to concerns over a government shutdown, but those fears didn’t seem to bother anyone yesterday. Maybe it’s just Tuesday (see below). Treasury yields are slightly higher, crude oil is down nearly 1%, gold and other precious metals are lower across the board, as is crypto.

Overnight, Asian stocks were mostly lower. Japan traded down 0.3% as market expectations for a rate hike increase, and the government raised its forecasts for consumer spending for the first time in over a year. PMI data in China was mixed, with the manufacturing component coming in slightly ahead of forecasts (but still below 50) while the services index missed expectations.In Europe, most major indices are little changed as economic data in Germany (Retail Sales) and France (CPI) missed expectations.

In the US today, we’ll get the Chicago PMI, which always seems to disappoint, at 9:45 followed by JOLTS and Consumer Confidence at 10 AM. The only earnings report of note is Nike (NKE) after the close.

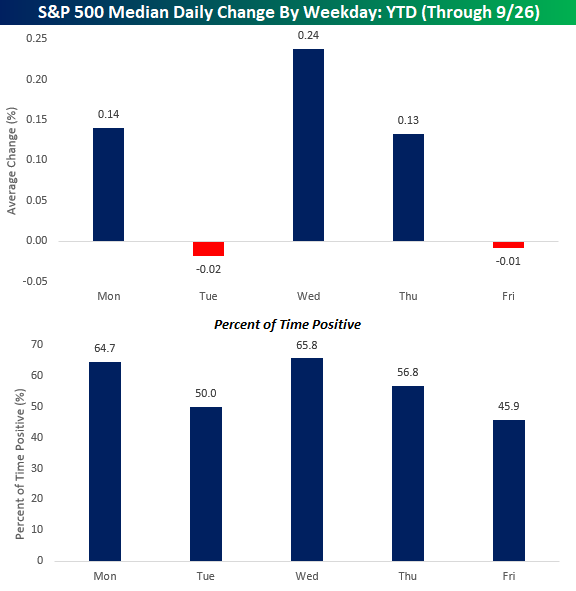

What’s so bad about Monday anyway? Lately, not much. The S&P 500 rallied 0.26% yesterday for its fourth straight positive start to the week and continuing a trend that has been in place for most of the year. Through last Friday, Mondays have been the second most positive weekday of the year with a median gain of 0.14% and gains 64.7% of the time. The only day of the week that has been stronger this year is Wednesday, with its median gain of 0.24% and gains 65.8% of the time.

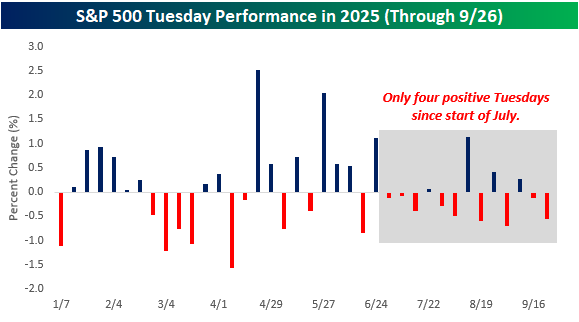

\While Mondays have been strong, Tuesday is the new Monday as it ranks as the weakest weekday of the year with a median decline of 0.2% this year and gains just half of the time. The only other day of the week that has experienced negative returns on a median basis this year is Friday. So, maybe it shouldn’t come as any surprise that futures are lower this morning.

Looking at Tuesday performance more closely, the third quarter has been especially weak. Since the start of July, only four of the twelve Tuesdays have seen gains, so if the S&P 500 can manage to squeeze out a gain today, it would break what has been a pretty consistent trend of recent weakness.

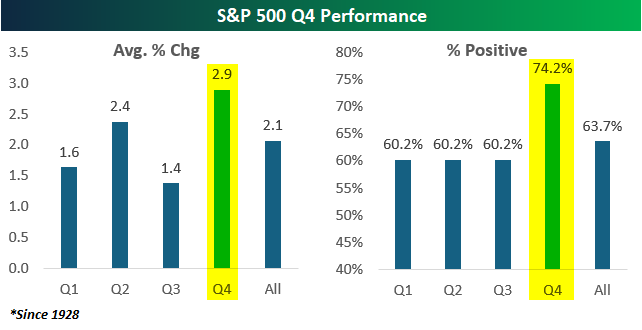

Today marks the last trading day of Q3, which has historically been the weakest quarter of the year. Since 1928, the S&P 500’s average performance during Q3 has been a gain of 1.4% with positive returns 60.2% of the time, but returns in Q4 have been better than and more consistent to the upside with an average gain of 2.9% and gains just under three-quarters of the time. For more analysis on quarterly seasonality, make sure to check out Monday’s Chart of the Day.

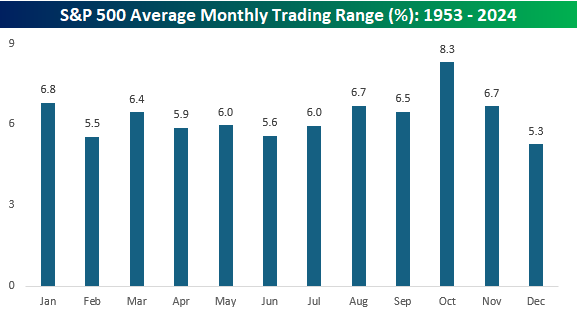

While Q4 has historically been strong, buckle up for some volatility. The chart below shows the average monthly trading range of the S&P 500 since 1953 (when the five-day trading week in its current form started). October’s average high-low spread (%) has been 8.3% which far surpasses the average monthly range of any other month. The next closest month is January at 6.8%. What’s notable about the 1.5 percentage point spread between the most volatile and second most volatile months is that it’s also the same as the spread between the second most volatile (January) and the least volatile months (December).

Sep 29, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Never make anything more accurate than it needs to be.” – Enrico Fermi

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After last trading to record highs last Monday, US equities are kicking off the week on a positive note once again this week as deal-making activity provides a boost to investors concerned about market valuations. Both the S&P 500 and the Nasdaq are indicated to open up by over 0.50%. Crude oil is down over 2%, which also helps, while gold is up over 1% and Bitcoin and Ethereum are both up close to 2% after some rough trading last week.

The pace of earnings activity will be incredibly slow this week, with Nike (NKE) the only notable report of the week (Tuesday). Economic data will pick up the slack, though, with multiple PMI readings, Consumer Confidence, and Non-Farm Payrolls.

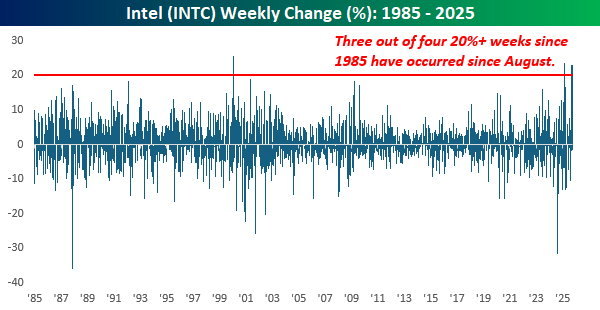

Like the S&P 500, which hit an all-time high last week before pulling back modestly, the Philadelphia Semiconductor Index (SOX) also hit an all-time high last Monday and then pulled back a little bit but still managed to finish the week up by 1.2%. What’s been interesting about the SOX this year, though, is which stocks are leading. A list of some of the index’s best performers this year looks like a time warp from the late 1990s, with stocks like Rambus (RMBS), Micron (MU), Lam Research (LRCX), and Intel (INTC) all up over 75%! INTC was up over 20% just last week! Meanwhile, Nvidia (NVDA), the leader of the AI revolution, has been in the middle of the pack, managing a gain this year of ‘only’ 33%.

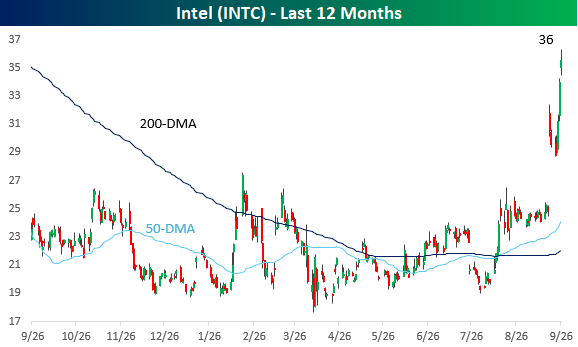

On a one-year basis, INTC’s chart looks a lot like ones from the 1990s as the stock has gone parabolic over the last two months, surging close to 90%!

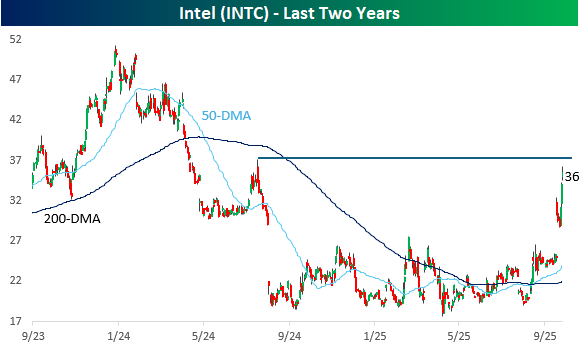

On a two-year basis, INTC’s move looks more modest. Last Friday’s surge topped out just shy of the high it reached in the summer of 2024 right before it plunged 50% in a matter of weeks!

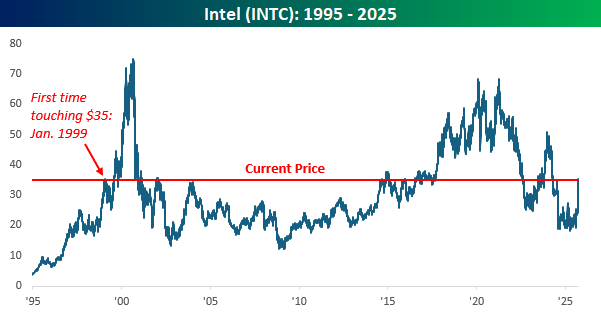

As impressive as INTC’s run has been in the last couple of months, it is still a shell of its former self. It’s still down close to 50% from its high in 2021. Additionally, while there has been a lot of talk lately about the market feeling like 1999, with INTC closing at $35 and change last Friday, it’s back to levels it first crossed back in January 1999!

Perhaps the most amazing thing about the recent moves in INTC is that last week’s gain of 20% was the third week in the last seven that the stock rallied 20%+. How crazy is that? Since 1985, there has only been one other week outside of the last seven that the stock rallied 20%+.

Sep 26, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“This is the way the world ends, not with a bang but a whimper.” – T.S. Eliot

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures were higher heading into this morning’s economic data, and after the 8:30 batch of data, equities have built modestly on their gains. Personal Income and Personal Spending were both a tenth higher than expected, and PCE inflation was in line with forecasts at both the headline and core levels. While the inflation data was right inline, it remains at uncomfortably high levels with y/y headline coming in at 2.7% while the core reading was 2.9%. As long as these readings can stay below 3%, markets should be able to handle it.

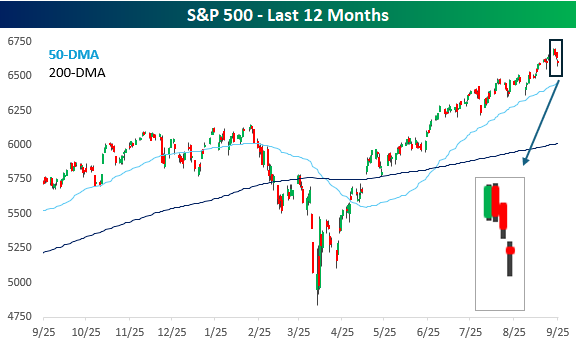

Mondays aren’t usually a day we look forward to, but looking back, it’s been the best day of the week. After riding the optimism of Fed rate cuts to record highs last week, investors took the weekend to think about it and liked what they saw. On Monday, the S&P 500 rallied for the third day in a row, hitting its eighth record high of the month and the 28th record high of the year.

Since that record high on Monday, however, the S&P 500 has traded down for three straight days and is now trading back to where it closed last Tuesday – before the Fed cut rates. Instead of optimism for lower rates, investors are increasingly worried that the market is getting ahead of itself as terms like euphoria and bubble enter the lexicon.

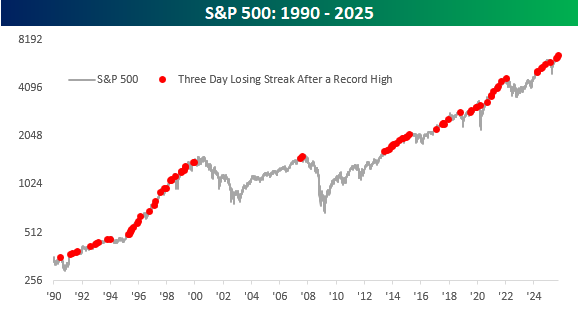

The severity of the declines this week has been extremely modest. Over the course of the three-day losing streak, the S&P 500 is down less than 1%, so if this type of ‘pullback’ makes you nervous, you’re taking too much risk. Besides the shallow nature of the decline, the fact that the S&P 500 is down three days in a row after hitting a record high is hardly unusual. The chart below shows the S&P 500 dating back to 1990, and the red dots show every three-day losing streak that followed a record closing high. Just this year, there have been three other occurrences. One occurred back in February ahead of the tariff-tantrum, but there was also another one in late July and then again in mid-August. Remember those? We didn’t either.

Looking at other occurrences, yes, similar scenarios have played out right around major market tops, but there were dozens more that no one remembers anymore. The only way we’ll know if this occurrence is a significant one is with hindsight, but the odds are that it’s not.

Sep 25, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The best fiction is far more true than any journalism.” – William Faulkner

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Just when it seems like the market can only go up, it does nothing but go down. Futures on the S&P 500 and Nasdaq are in firmly negative territory this morning, putting both indices on pace for their third straight day of losses. The S&P 500 is indicated to open down by about 0.4% while the Nasdaq is on pace to open down closer to 0.6%. The weakness in US stocks follows a weak morning in Europe, where the STOXX 600 is down over 0.75%, and other major country-level indices are down by 0.15% to 1.0%.

Despite the weaker tone in equities, investors aren’t rotating into treasuries as yields are modestly higher as well. Crude oil is also lower, although gold and other precious metals are all up at least 0.5%. One are where investors certainly aren’t rotating is into crypto. Bitcoin is down nearly 2% while Ethereum is down over 3.7% as it struggles to hang onto the $4,000 level. There may have been a decent amount of froth in the sector heading into the month, but it has definitely worked itself off over the last several days.

We also have a ton of economic data to contend with this morning, with Wholesale Inventories, GDP, Personal Consumption, Durable Goods, and Jobless Claims at 8:30, followed by Existing Home Sales at 10 and the KC Fed Manufacturing report at 11. Besides those reports, there are also a ton of Fed speakers on the calendar. Should be fun! Of the reports hitting the tape at 8:30, most of them came in better than expected, with a much weaker-than-expected initial jobless claims reading of 218K being the big standout. The market response has been even higher yields and lower futures.

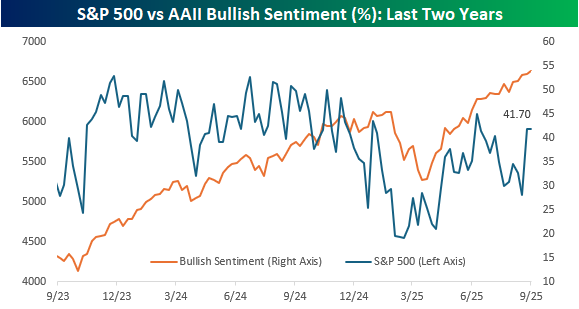

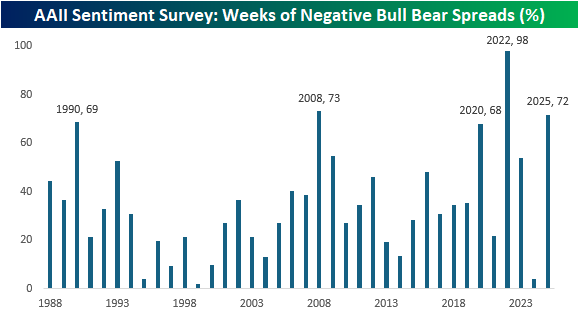

While the last couple of days have started to show some cracks in the market, sentiment was little changed based on the weekly survey from the American Association of Individual Investors (AAII). Bullish sentiment remained unchanged at 41.7% while bearish sentiment dropped to 39.2% and neutral sentiment increased to 19.1%. As shown in the chart below, even as stocks have recovered from their April lows, sentiment hasn’t experienced anywhere nearly as big a lift.

In fact, while the bull-bear spread in sentiment broke a streak of seven weeks in a row of negative readings, nearly three-quarters of all weeks this year have had negative spreads, and if the year were to end now, it would rank as the third-most weeks of negative bull-bear spreads in the survey’s history. The only years with a higher percentage were 2022, when the spread was only positive once (March 2022), and 2008, when 73% of weekly readings were negative. Outside of those two years, the only others when the bull-bear spread was negative more than two-thirds of the time were 1990 (69%) and 2020 (68%).

Sep 24, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life starts all over again when it gets crisp in the fall.”- F. Scott Fitzgerald

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 was only down 0.55% yesterday, but that was enough to be the worst day for US stocks since the first trading day of the month. This morning, futures are showing modestly positive gains, with the S&P 500 up 0.13% and the Nasdaq trading 0.21% higher. Treasury yields are also higher as the 10-year has ticked up to 4.13% and is on pace for the fifth daily increase in the six trading days since last week’s cut. Crude oil is up 1% and back up to $64 per barrel for the first time since the middle of the month, but gold is giving back some of the gains from the last two days as it trades back down to $3,800 per ounce. It’s been a rough few days for crypto, but the sector is catching a break this morning as Bitcoin rallies more than 1% while Ethereum is up a more modest 0.55%.

Overnight in Asia, stocks were mixed, with Japan and China trading higher, while India and South Korea slid by about 0.5%. As we saw in many European PMI readings yesterday, Japan’s flash Manufacturing PMI slid further into contraction, falling from 49.7 to 48.4 versus forecasts for a more modest drop to 49.5.

European markets are more negative this morning, with the STOXX 600 trading down 0.3%, as luxury stocks drag the major averages, especially in France, lower.

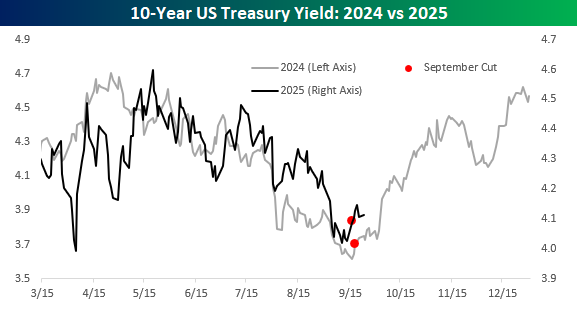

It’s been a week now since the Fed cut rates, and so far the equity market has seen a modestly positive reaction while treasury yields have moved higher, with the 10-year yield moving up to 4.11% from 4.03% last Tuesday, the day before the cut. The rise in yields over the last week undoubtedly is at least partially a reflexive response to what happened after last year’s cut. Back then, yields were in a steady decline in the six months leading up to the cut, falling from 4.7% to just over 3.6%, but the cut rang the bell, and from there, rates retraced all their previous decline by year’s end.

This year, we’ve seen a similar pattern where yields steadily declined leading up to last week’s cut and have been moving higher ever since. The one difference is that last year, most investors expected yields to continue falling into year-end, while this year, the consensus is expecting yields to rise and the curve to steepen. Will history repeat itself, or is it too obvious?

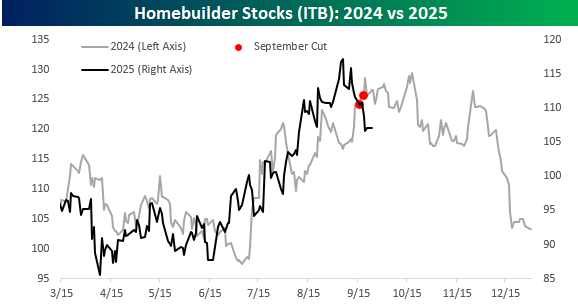

Homebuilder stocks are one of the most interest rate-sensitive sectors of the market, and like treasury yields, they’ve followed a similar pattern this year compared to last year. The one difference is that while the iShares Homebuilder ETF (ITB) was hitting highs for the year at the time of last year’s September cut, this year the ETF peaked about two weeks before last week’s cut. The fact that investors were starting to take profits in the homebuilders ahead of the cut illustrates the sentiment that there was less optimism towards long-term yields continuing lower after the September cut this year, compared to last year.

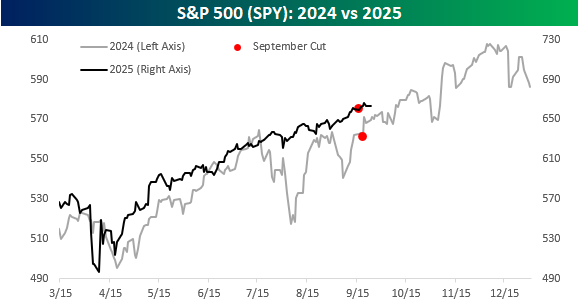

The S&P 500’s pattern this year varied from last year in that it has been much less volatile leading up to the cut than it was last year. In each case, though, it was trading either right at or very close to new highs at the time of the cut.

Sep 23, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I am who I am today because of the choices I made yesterday.” – Eleanor Roosevelt

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

S&P 500 futures are unchanged as we type this, indicating an uneventful day for equities, although the persistent bid we have seen for months now could pull things higher throughout the session. The only economic data on the calendar this morning is New Home Sales at 10 AM and preliminary PMI data from S&P for the manufacturing and services sector at 9:45. There’s also a heavy dose of Fed speakers, including Chair Powell shortly after noon.

Overnight in Asia, markets were mixed. While Japan was closed, Hong Kong and China were lower, while the Kospi traded higher to record highs. The tone in Europe is decidedly more positive with broad-based strength pushing the STOXX up by 0.3% even as PMI data for the manufacturing sector showed lower than expected growth.

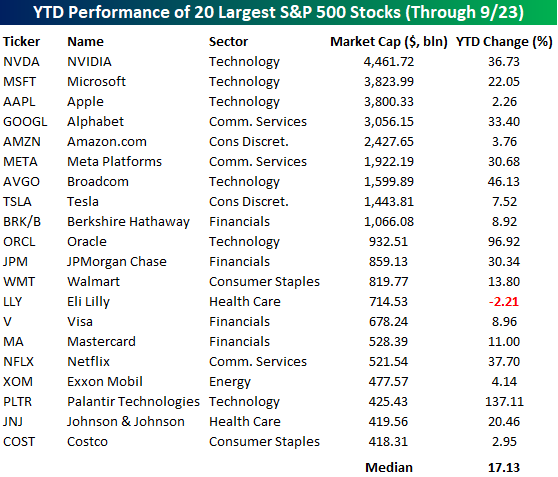

In terms of market leadership, the largest companies in the market continue to dominate. The table below lists the 20 largest stocks in the S&P 500 along with their YTD performance. All but one of them – Eli Lilly (LLY) – is up on the year, and it’s only down 2%. The median performance of the 20 stocks listed is a gain of 17.1%, with half of them rallying at least 20%, including Palantir (PLTR) and Oracle (ORCL), which are up 137% and 97%, respectively.

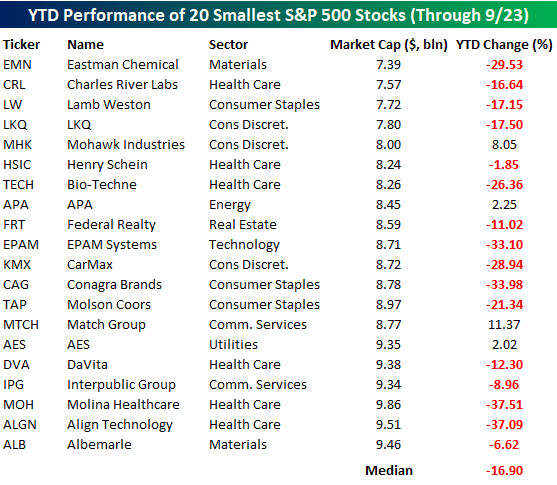

Now, contrast the performance of the 20 largest stocks with the 20 smallest stocks. Only four of the 20 smallest stocks in the S&P 500 are up YTD, and their median performance is a decline of close to 17%. It’s basically a mirror image of the 20 largest stocks. In an investment environment where passive flows should be a tide lifting all boats in the S&P 500, investors are actively abandoning ship on the smallest stocks in the index.

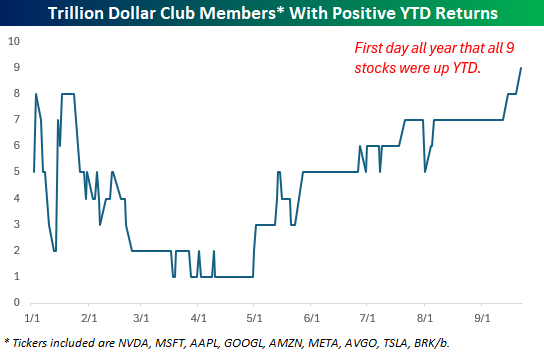

While the largest stocks in the S&P 500 have been leading the market all year, yesterday was a notable one in the fact that it was the first time all nine current members of the trillion-dollar club finished the day with a positive YTD performance. Earlier in the year, we got close with eight stocks in the black, but Apple (AAPL) was the holdout. For the first time all year, though, AAPL finished the day with a positive YTD gain yesterday, joining the eight others in the party.